The balance sheet of Strategy can withstand the accounting fluctuations of 840,000 bitcoins, but it may not withstand a fading story.

Written by: ChandlerZ, Foresight News

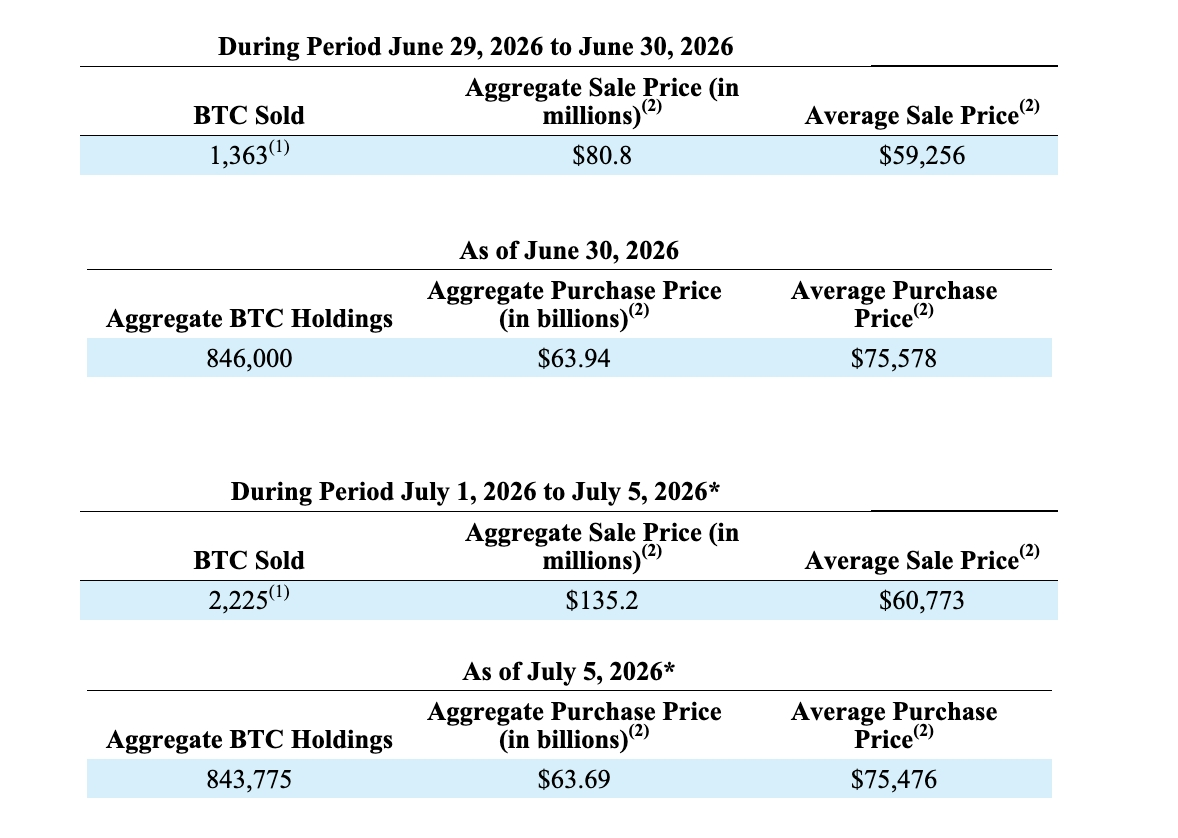

On July 6, Strategy (formerly MicroStrategy) disclosed in an SEC 8-K filing that the company sold 1,363 bitcoins at an average price of approximately $59,256 from June 29 to 30, totaling around $80.8 million; from July 1 to 5, it sold 2,225 bitcoins at an average price of approximately $60,773, totaling around $135.2 million, with the proceeds used to pay preferred stock dividends and replenish dollar reserves.

This was the largest net sale since Strategy launched its bitcoin strategy in 2020, and it marked the first time in six years that the company systematically reduced its core assets. The average selling price was approximately $60,200, lower than the company's holding cost basis of about $75,476, resulting in a loss of $15,276 per bitcoin, totaling $54.81 million.

As of July 5, Strategy held a cumulative total of 843,775 bitcoins, with a total holding cost of approximately $63.69 billion. It remains the publicly traded company with the largest bitcoin holdings in the world.

According to official statements, as of July 5, Strategy's dollar reserve balance was $2.55 billion, unchanged from the previous week. In the second quarter of 2026, the company's digital assets experienced a loss of approximately $8.32 billion, with unrealized losses of about $8.31 billion and realized losses of approximately $900,000. As of June 30, the book value of the bitcoin holdings decreased to $49.67 billion, below the holding cost, prompting Strategy to make a full valuation allowance for associated deferred tax assets.

After the news was disclosed, bitcoin quickly dipped below $61,500, then reversed after the U.S. stock market opened, with buy orders pulling it back up to around $64,500. The price of MSTR retraced about 2% after a 21% increase the previous week, but it is still down over 35% for the year.

From 32 to 3,588, a 100-fold increase in six weeks

Selling bitcoins was once a taboo for Strategy. In September 2020, after founder Michael Saylor completed his first bitcoin purchase of $425 million, he told CoinDesk in an interview, "I didn’t buy it to sell it. Ever." For the next five years, Strategy only bought and did not sell, using the company’s balance sheet to be a permanent holder of bitcoin.

December 2022 was the only exception; Strategy announced the sale of 704 bitcoins at an average price of approximately $16,776, but two days later, it immediately bought back 810 bitcoins, increasing its net holdings instead. The SEC filing characterized this operation as tax-loss harvesting, using capital losses to offset previous capital gains for tax benefits.

On May 5, 2026, during the Q1 earnings call, Strategy sent its first signal to sell. Michael Saylor said, "We may sell some bitcoins to pay dividends, so the market can adjust in advance."

In a subsequent interview with Fortune, he stated that the purpose of his comments was to "create panic to squeeze shorts and detractors." However, three weeks later, an SEC filing showed that Strategy sold 32 bitcoins between May 26 and 31, cashing out approximately $2.5 million.

Six weeks later, the number jumped from 32 to 3,588.

$1.25 billion selling authorization, burning 17% in a week

The sale of 3,588 bitcoins was not a spontaneous decision. On the same day as the first bitcoin sale (June 29), Strategy released a new capital framework titled "Digital Credit Capital Framework," formally incorporating bitcoin sales into the company's system.

The core terms of the framework include a dollar reserve policy, adjustments to the STRC dividend policy, a preferred stock repurchase plan, a common stock repurchase plan, and a BTC monetization plan. The core includes authorizing management to sell up to $1.25 billion worth of bitcoin (approximately 20,800 bitcoins at current prices, accounting for 2.5% of total holdings) when necessary; establishing a dollar reserve system with a minimum level equal to the total of preferred stock dividends and interest expenses for the next 12 months; increasing the annualized dividend rate of STRC preferred stock from 11.5% to 12%, effective July 1; and additionally authorizing up to $1 billion for preferred stock buyback and $1 billion for common stock buyback.

As of June 28, Strategy's cash reserves were $2.55 billion. The signal the company tried to convey when the framework was released was that selling bitcoin was merely one option in a broader capital management toolbox, and the company had sufficient cash reserves to meet its dividend obligations. However, it was clear that the selling pace exceeded market expectations; 3,588 bitcoins, totaling $216 million, meant that 17% of the $1.25 billion sell authorization was consumed in just the first week of its effectiveness.

From 2020 to 2025, Strategy's bitcoin buying strategy was built on an aggressive financing scheme, issuing convertible bonds, increasing the issuance of common stock, and issuing preferred shares to finance bitcoin purchases with all raised funds. This model operated perfectly while bitcoin prices rose, as the appreciation of assets covered financing costs, creating a positive spiral between the company's stock price and bitcoin.

Strategy currently has four preferred stocks traded in the market: STRC (12% annualized dividend), STRK (8%), STRF (10%), and STRD (10%), with a total annual dividend obligation of about $1 billion. Preferred stock dividends are a rigid expense that must be paid on time regardless of bitcoin price fluctuations. The company's software business (formerly MicroStrategy's BI products) generates annual revenue of less than $500 million, not enough to cover the dividends.

This creates a very contradictory point: Strategy raises funds through issuing preferred stocks to buy bitcoin, but the dividend obligations of the preferred stocks force the company to sell bitcoin to pay dividends. When bitcoin prices are above the holding cost, this contradiction is concealed.

Bitcoin has sharply retreated from its historical high in October 2025, with Strategy's aggregate holding cost of approximately $75,476, while the average selling price of this batch was only about $60,200, resulting in a loss of over $15,000 per bitcoin. Q1 reports recorded a $12.5 billion impairment loss on digital assets, and Q2 recorded another $8.32 billion. The company is selling bitcoins at prices below costs to pay dividends on the securities issued to purchase bitcoin.

Premium collateral

3,588 bitcoins account for 0.4% of the total holdings of 840,000, thus having a limited impact on bitcoin markets. The $1.25 billion sell authorization cap represents 2.5% of total holdings, and even if fully utilized, it would be far from a complete liquidation. From a balance sheet perspective, Strategy is not under repayment crisis.

However, MSTR's stock price has never been priced based on the balance sheet. This stock has been trading at a premium of 1.5 to 3 times the BTC net asset value for a long time; the consideration that investors pay for this premium corresponds not to the 840,000 bitcoins themselves (buying BTC or ETF directly is cheaper), but rather to a narrative product provided by Michael Saylor, namely a bitcoin absorption machine that only takes in and never lets out, with holdings that always grow and never appear on the seller side. This promise is the collateral for all premiums of MSTR.

As of June 28, Strategy’s dollar reserves were $2.55 billion, with preferred stock annual dividends of about $1 billion, providing enough cash coverage for over two years. Michael Saylor does not need to sell bitcoins now for financial reasons. Yet, he initiated a systematic selling framework, raised the STRC dividend rate, and executed a $216 million sale within a week. The four preferred stocks generate monthly cash expenditure obligations, while the promise of "never selling bitcoins" excludes the possibility of paying dividends with core assets.

When these two matters occur on the same balance sheet, one of them must yield, and what Michael Saylor yielded is the latter.

After the first bitcoin sale this year, Michael Saylor offered a new narrative stating that if the interest/dividends on issued bonds or preferred stocks can be managed at a lower financial cost, Strategy could leverage to buy bitcoin at low prices and lock in more. As the appreciation of overall assets during bull markets far exceeds the interest costs, theoretically, for every bitcoin sold, the company would purchase 20 bitcoins through convertible notes and other derivatives.

However, every time Saylor sells bitcoin, he needs to explain why this does not count as breaking his promise, and the explanation itself is consuming his credibility that he has built over six years.

The premium of MSTR relative to BTC net asset value has never been because the company’s method of holding bitcoin is more efficient than an ETF; rather, it is because Saylor has turned "never selling" into a corporate governance-level religious ceremony. Once the ritual is interrupted, MSTR is just a leveraged bitcoin holding tool, with many cheaper alternatives already existing in the market.

The balance sheet of Strategy can withstand the accounting fluctuations of 840,000 bitcoins, but it may not withstand a fading story.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。