Original author: Dong Jing

Original source: Wall Street Watch

Samsung Electronics delivered a historic report with a profit surge of 19 times, yet faced a heavy decline in stock price in a single day. This is not due to poor performance, but because the market had already priced in "perfection" beforehand - the financial report's release was merely a signal for fund withdrawal.

On July 7, an article from Wall Street Watch stated that Samsung Electronics' operating profit for the second quarter skyrocketed by about 19 times year-on-year, reaching 89.4 trillion won (approximately 58.4 billion USD), not only setting a quarterly historical record but also surpassing NVIDIA's operating profit of 53.536 billion USD from the previous quarter, making it the company with the highest quarterly operating profit globally. Revenue doubled to 171 trillion won, both figures exceeded analysts' average expectations. However, after the financial report was released, Samsung's stock price dropped 8% in a single day, the KOSPI index fell 6%, and SK Hynix dropped over 7%.

Wall Street Watch also mentioned in an article that "the logic of 'buy the expectation, sell the fact' played out clearly again." The night before the financial report release, the Philadelphia Semiconductor Index rose 2.2%, the S&P 500 rose 0.7%, and the NASDAQ 100 rose 1.3%. As the positive news was realized, funds quickly withdrew.

Brian Cho, portfolio manager at Causeway Capital Management, bluntly stated that what the market really wants to see is whether the improvement in free cash flow can form a sustainable stepwise change, and how management treats shareholder returns - the pricing logic has shifted from "how fast profit growth is" to "whether these profits can be turned into real cash distribution to shareholders."

Moreover, the sharp reversal in market sentiment has its macro backdrop. Last week, Meta was the first to hint at tightening capital expenditures, triggering the largest two-day sell-off of high beta momentum stocks since the pandemic. Samsung's decline also put pressure on peer chip stocks SK Hynix and Micron, as the high valuation logic of the entire memory chip sector is facing systemic reassessment.

Impressive performance, but not good enough

Wall Street Watch reported that Samsung's operating profit for the second quarter is expected to reach 89.4 trillion won, a quarter-on-quarter increase of 56%, whereas analysts had previously predicted an average of 84.2 trillion won; for the same period, revenue was 171 trillion won, surpassing the market estimate of 169.2 trillion won, and increasing by approximately 129% year-on-year. The company plans to release a complete financial report on July 30, at which time it will disclose net profit and categorization data of various business units.

The core logic driving this round of growth is the continued tight supply of memory chips. The strong demand for high-bandwidth memory (HBM) from AI data centers has prompted manufacturers to tilt production capacity towards high-end products, leading to shortages in traditional DRAM and NAND memory chips, pushing prices up comprehensively.

According to data from HSBC, the average price of DRAM in the second quarter rose by over 40% quarter-on-quarter, while NAND prices rose by over 50%. Citigroup's research data closely aligns with this, showing that the average prices of DRAM and NAND both rose by 44% and 53%, respectively, compared to the previous quarter.

However, while the revenue of 171 trillion won was higher than analysts' average expectations, it fell short of some institutions' optimistic forecast of 173.9 trillion won. In the context of valuations already pushed to high levels, this slight gap is enough to trigger profit-taking.

The brilliance of the memory business has obscured several cracks in the company's overall structure. Analysts expect losses in Samsung's foundry and logic chip (LSI) business may further widen this quarter, partly due to bonus expenses being proportionately accounted for in the overall costs of the semiconductor sector.

In May this year, Samsung reached a compensation agreement with employees in the chip sector, tying performance bonuses to operating profits, and stipulating that under certain profit targets, 10.5% of the semiconductor department's annual operating profits would be allocated for special bonuses. Some analysts pointed out that if this provision were not accrued, Samsung's operating profit would exceed market expectations further.

AI demand supports the memory boom, but marginal signals trend weaker

The core logic driving this super cycle of memory chips remains valid: the large-scale expansion of global AI data centers has created strong demand for high-end memory chips, and the memory shortage has become a key bottleneck for AI development.

Industry executives, including NVIDIA CEO Jensen Huang and OpenAI COO Brad Lightcap, have warned about this. Major manufacturers are prioritizing high-end storage products, leading to simultaneous shortages in traditional storage products, and analysts expect the supply shortage will persist at least until 2027.

Market research firm Counterpoint projects that the average operating profit margin for the top three memory manufacturers, Samsung, SK Hynix, and Micron, will remain between 75% and 80% in the second quarter of this year. The firm noted in its report that some opinions suggest that such high profit margins constitute "excessive profitability," and warned that "if this situation continues, memory manufacturers may face regulatory pressure."

Additionally, Wall Street Watch mentioned that more attention should be paid to the signals released from the upstream of the supply chain than to the financial report itself. Recently, Meta hinted at setting a cap on AI capital expenditures, which the market interpreted as an early warning that tech giants' investments in AI infrastructure may have peaked, directly triggering one of the most severe two-day sell-offs of high beta momentum stocks since the pandemic.

Jean Boivin's team from BlackRock Investment Institute stated the issue more directly: the core of the AI bubble debate is not the current valuations, but whether future profits can remain at extraordinary levels. If AI fails to convert the current scarcity into real productivity gains, the extremely high profit expectations will face corrections.

Samsung underperforms SK Hynix, Korea bets on AI chip dominance

From a national strategic perspective, the South Korean government views Samsung and SK Hynix as the core pillars in the competition for global AI leadership. Samsung Group and SK Group plan to build two chip factories in the southwestern part of Korea, with a total investment scale of 80 trillion won to rapidly expand production capacity. South Korea aims to double memory chip production capacity within five years, and Samsung has announced it will invest over 70 billion USD in capacity expansion and R&D by 2026.

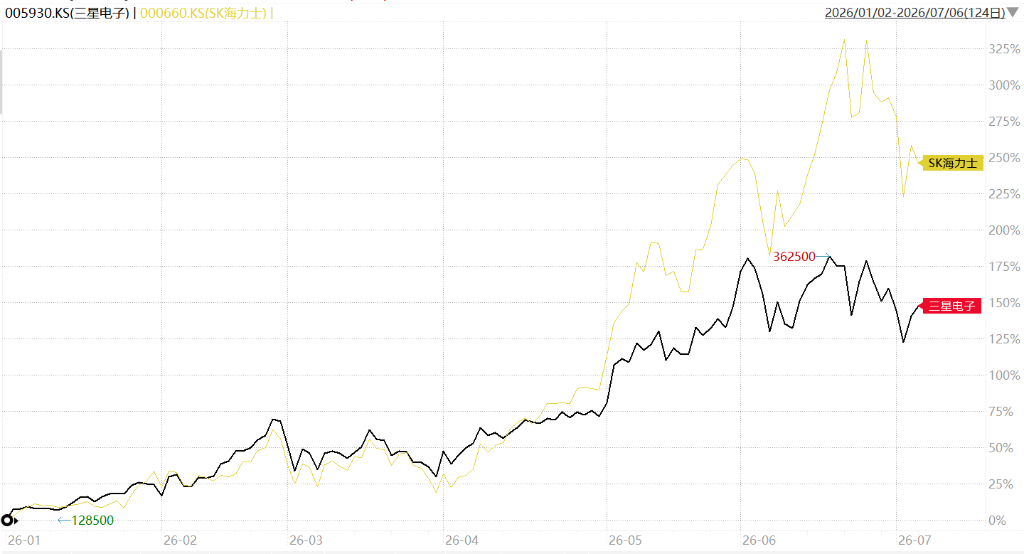

In terms of stock performance, Samsung has seen a cumulative increase of about 165% this year, but significantly underperformed its competitor SK Hynix, which has risen about 260%. The difference between the two stems mainly from differences in product structure - SK Hynix's business is highly concentrated on high-end memory chips that meet AI computing demands, while Samsung's product portfolio is more diversified, spanning chips and consumer electronics. This differentiation transmits a clear signal: in the current race, focus is favored over scale by capital.

Samsung's complete financial report will be released at the end of this month, and at that time, the disaggregated data of various business units will inform the market how much real value has been transformed from this round of AI capital expenditures. That number will become an important reference coordinate for the next stage of AI hardware investment logic.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。