SpaceX, OpenAI, and Anthropic's "super IPOs" are crowding to enter the U.S. stock market.

Written by: Zhao Ying

Source: Wall Street Watch

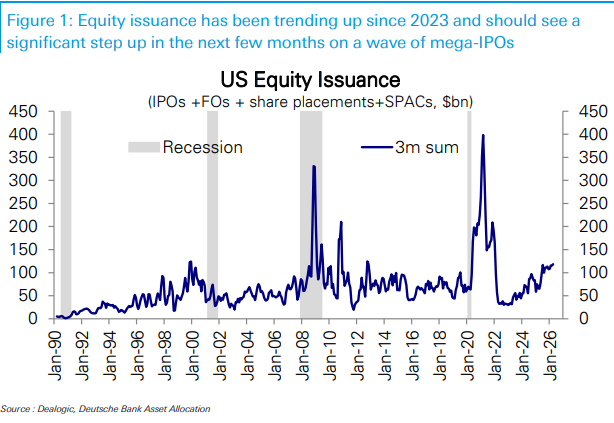

U.S. stock equity financing has rebounded from its low point in 2023, and it may accelerate significantly in the coming months: a slew of super-large IPOs are lined up, with individual financing possibly reaching hundreds of billions of dollars. The market's most direct concern is that these new stocks will "bleed" existing U.S. stocks, especially when index funds and large-cap stocks are already heavily positioned.

SpaceX, OpenAI, and Anthropic's "super IPOs" are crowding into the U.S. stock market. SpaceX's prospectus (S-1) was officially disclosed last week, with the listing date expected to be scheduled for the second week of June, making it the first of the three companies to complete its public offering. OpenAI plans to go public as early as September this year, which is significantly ahead of previous market expectations, while Anthropic might seek to go public as early as October this year.

According to Wind Trading Desk, Deutsche Bank securities strategist Parag Thatte wrote in a report on May 22: "In our demand-supply framework, the rebound in issuance itself may indeed pose a negative impact on stocks, but the impact is only moderate; past academic literature and empirical evidence during issuance waves clearly show that issuance waves are usually accompanied by strong stock market returns, as they occur during periods of strong stock demand."

The core judgment of this research is not "issuance is harmless," but rather "issuance is not the main cause." An increase in supply may bring short-term disturbances; a maximum IPO alone might drag the market down by about 1%. If the listing rhythm is concentrated and crowds out other stocks in the index benchmark, the impact might be greater. However, this still resembles a common trigger factor for a correction rather than a sufficient condition for the end of a bull market. On average, there is a minor pullback of over 3% in the U.S. stock market every 1 to 2 months, with many potential triggers, and IPOs are only one of them.

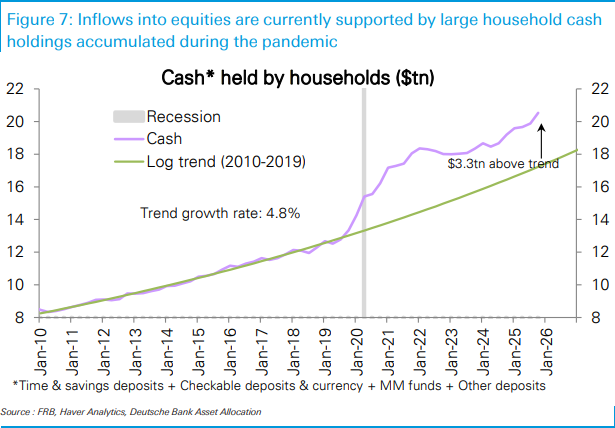

The real support for this judgment is that the demand side has not collapsed. The household sector still has high cash balances, corporate profit growth is strong, stock funds continue to flow in, and buyback announcements remain high. The issue is not whether there is enough money to buy new stocks, but whether demand can continue to outweigh supply; another boundary condition is that large-cap stocks, especially large-cap tech stocks, are already heavily positioned, which is a more sensitive area.

This round of issuance seems large, but within the context of the entire U.S. stock market, it is not exaggerated

The quarterly rhythm of U.S. equity issuance has risen from a low point of about $30 billion at the beginning of 2023 to the current approximately $120 billion. In the coming months, a batch of super-large IPOs may push the pace even higher.

Looking solely at IPOs, some of the upcoming large projects might amount to the total value of all U.S. public financing over the past 9 months. Expanding the scope to all U.S. equity issuances, including secondary offerings, it is equivalent to about two months of issuance volume.

But looking at it from another scale, the pressure is much smaller. Even for the largest anticipated IPOs, the financing amount is just slightly over 0.1% of the current total market capitalization of the S&P 500. This is also why "increased supply" alone is insufficient to conclude that "U.S. stocks will inevitably fall": the absolute amount is eye-catching, but in relation to market size, it is not extreme.

Historically, issuance waves have been more like byproducts of bull markets

Over the past 30 years, there have been several cycles of equity issuance upswings in the U.S. stock market. Historically, the stock market in these phases has typically performed very well: during the first 3 months after the start of an issuance wave, the median return of the S&P 500 is about 8%; extended to 12 months, the return exceeds 20%.

The exceptions are also very clear: during the 2008-2009 global financial crisis, entities such as financial institutions were forced to raise capital, and the increase in issuance occurred amid significant sell-offs. This type of "forced capital replenishment" issuance is not the same as companies financing during normal market conditions when valuations and demand are favorable.

The causal direction indicated in the academic literature also leans towards this point: a stronger stock market and higher expected profitability often occur first, leading to a wave of issuances; the issuance itself has limited reverse impact on the market during the same period. The later stages are more troublesome—the stock market returns will ultimately weaken after an issuance wave, but this "ultimate" can take a long time, and it cannot simply be used as a short-term sell signal.

The model indicates an impact of about 1%, but concentrated listings will amplify perceptions

The demand-supply framework puts several factors together: changes in investor positions, stock fund inflows, buybacks, and issuances. Issuance belongs to the increased supply and, under unchanged conditions, is naturally a negative factor.

Calculations show that the largest scale IPO, viewed alone, may cause the market to decline by about 1%. If the listing timings are highly concentrated, or if the new stocks, once they enter index benchmarks, crowd out other constituent stocks, the actual pressure may be even more significant.

However, it's essential to distinguish between "downside risk" and "systematic selling pressure." A pullback of over 3% occurs on average in the U.S. stock market every 1 to 2 months. The IPO wave may become a catalyst for a specific pullback but does not necessarily change the market direction. Unless the demand side weakens concurrently, it is hard for supply shocks to independently crush the index.

The demand side still holds: cash, earnings, and buybacks are sustaining

The household sector remains a critical buffer. The cash balances accumulated during the pandemic remain very high, with households holding approximately $3.3 trillion more in cash than trends from 2010 to 2019. Relative to personal income, cash holdings are also at a high level, enabling residents to allocate a larger portion of new savings toward financial assets, including stocks.

Earnings are another supporting factor. The correlation between stock fund inflows and S&P 500 earnings growth has been about 54% since 2003. Earnings growth in the first quarter has been described as one of the strongest in over 20 years, which explains why funds remain willing to follow stock assets.

Buybacks are also an essential component of demand. S&P 500 buyback announcements remain robust, indicating that companies themselves are still providing buying power. While increased issuance brings supply, buybacks and fund inflows provide absorption capacity; the current balance has not significantly tilted toward the supply side.

Positions are not comprehensively overheated; crowding is mainly in large-cap tech stocks

Overall stock positions are only slightly overweight, sitting at the 53rd percentile since 2010. Active investor positions are lower, around the 47th percentile, close to neutral; systematic strategy positions are somewhat higher, around the 64th percentile.

The real crowding is in large-cap stocks, especially large-cap tech. Large-cap stock positions are at the 85th percentile, while large-cap tech hits the 93rd percentile. This means that if the IPO wave triggers fund rebalancing, the market will likely focus not on "all stocks," but on sectors that are already heavily held.

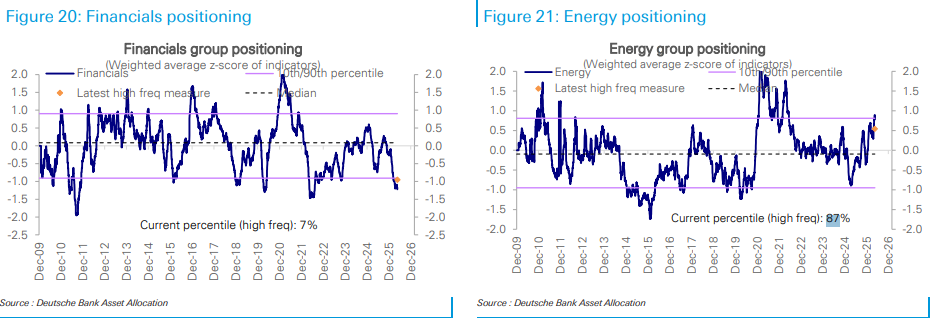

The distribution of sectors is also uneven. The energy sector is overweight, sitting at the 87th percentile; large-cap growth and technology are slightly overweight. Financials are significantly underweight, at the 7th percentile; materials are even more extreme, at the 0th percentile. The U.S. stock market is not evenly positioned, and supply shocks will not uniformly impact every corner.

Fund flows are not overwhelmingly optimistic; strength is in the U.S. and technology

In the past week, stock fund inflows decreased to $2.4 billion, showing a significant slowdown. U.S. stock funds still saw inflows of $9.5 billion, while broad global funds brought in $10.3 billion, but sizable outflows occurred in regions outside the U.S.

Japanese stock funds experienced an outflow of $4.4 billion, the largest in five weeks; European funds had an outflow of $2.3 billion, marking six consecutive weeks of outflows; emerging markets saw outflows of $7.9 billion, also for six straight weeks. Among them, Chinese-related funds had outflows of $9.7 billion, while South Korea and Taiwan saw inflows of $3 billion and $1.7 billion, respectively.

Industry funds are more concentrated. Technology funds saw inflows of $9 billion, the largest in seven months. At the same time, bond funds inflowed $30.5 billion, reaching a five-month high. Funds are not flowing unidirectionally into risk assets but are instead exhibiting differentiated movements among U.S. stocks, technology, and bonds.

This is also the most noteworthy aspect of the IPO wave: it's not about the quantity of new stocks but whether demand continues to concentrate on a few strong assets. If earnings, buybacks, and inflows into U.S. stocks continue to provide support, the issuance wave may resemble short-term noise; if crowded tech positions loosen and stock inflows cool down, supply pressure may shift from "about 1% model disturbances" to more challenging issues.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。