Author: cryptoslate

Translation: Blockchain Knight

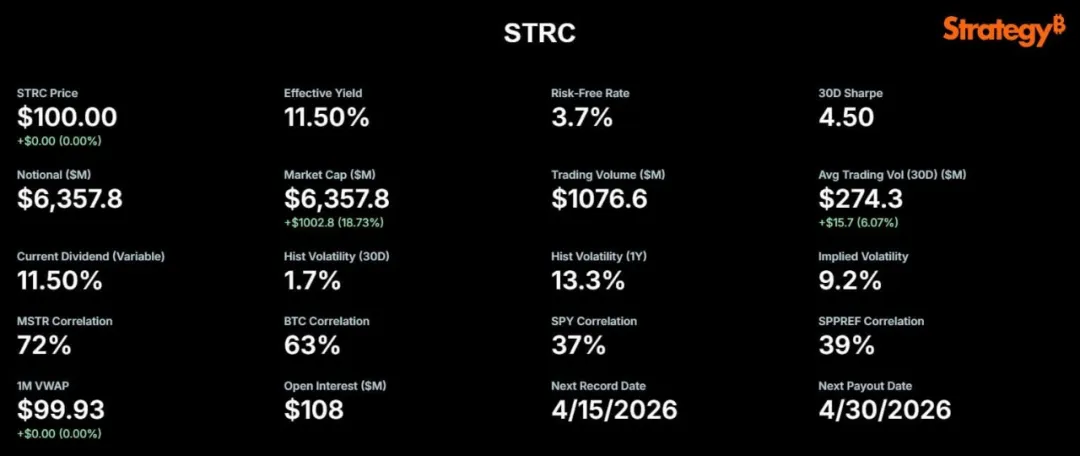

The perpetual preferred stock STRC from Strategy has played a key role in the company’s Bitcoin strategy this week, with a daily trading volume exceeding $1.1 billion.

In a post on X, Strategy announced April 13 as the record date for STRC's equity.

Michael Saylor also noted that after a liquidity influx of $1.156 billion into the market, the closing price of the security remained stable at par value, with fluctuations of only "one cent".

The trading volume surged after Strategy disclosed it purchased 13,927 Bitcoins for about $1 billion between April 6 and April 12.

With this acquisition, the company now holds 780,897 Bitcoins, with a total purchase price of $59.02 billion and an average price per Bitcoin of $75,577.

The company stated that this acquisition was fully funded through the sale of 10.02 million shares of STRC at market price, with net proceeds of about $1 billion.

Meanwhile, the record trading activity of STRC combined with the weekly Bitcoin purchases fully funded by this preferred program marks a significant shift in the company’s focus.

For equity investors, this shift could significantly change the balance of potential returns versus risks.

With a reduction in the issuance of preferred stock, an increase in preferred shares could reduce short-term equity dilution for common stock shareholders.

However, preferred stock grants fixed rights that have priority over common stock shareholders in the capital structure, meaning preferred shareholders are entitled to dividends before common shareholders receive any dividends.

In other words, preferred shareholders enjoy priority payment rights, meaning that only if the company fulfills those obligations will common shareholders benefit from any remaining profits.

If Bitcoin performs well, this approach may enhance returns, but it also increases reliance on ongoing market access and strict dividend management.

While this shift may enhance short-term purchasing power and reduce equity dilution, it could increase financial leverage and execution risks for common stock shareholders in the long run.

How STRC Preferred Stock Leads BTC Purchase Strategy

STRC was launched in July 2025 and operates very differently from Strategy’s common stock MSTR.

The preferred stock has an annualized dividend yield at a floating rate of 11.50% as of April. Its floating rate structure is designed to incentivize strong trading around its par value of $100.

This stable price anchoring mechanism allows Strategy to efficiently utilize its ATM issuance program.

Issuing new STRC shares at a consistent price enables the company to quickly raise funds and convert them into Bitcoins, minimizing friction and discounts typically associated with large-scale secondary market issuances.

Market observers note that STRC aims to provide investors with double-digit returns and minimal price volatility, combining high yield income with capital stability.

Strategy’s Executive Chairman Michael Saylor essentially stated, "STRC offers stability akin to a money market, along with market-leading risk-adjusted returns."

According to the STRC.live website, since its inception, STRC has funded the acquisition of nearly 70,000 Bitcoins. The recent $1 billion trading volume on April 13 may be sufficient to purchase over 6,000 additional Bitcoins.

Not surprisingly, the market capitalization of STRC has skyrocketed alongside the booming demand for this utility, nearly doubling from $3.4 billion in February to its current $6.36 billion.

STRC still has $21.6 billion worth of stock available for future issuance, indicating significant room for further accumulation of Bitcoins.

Reserves, Refinancing, and Risks of Preferred Stock

Despite optimistic market sentiment, some analysts express concerns about the sustainability of this model, citing Strategy’s own financial disclosures.

Due to insufficient operating cash flow from Strategy's software business to meet its financial obligations, the company established a $2.25 billion reserve in early February.

This reserve serves as a financial safety net intended to cover nearly 2.5 years of preferred stock dividends and interest on outstanding debts.

The reserve is necessary as, in the absence of sufficient regular business revenue, the company needs to rely on this reserved cash to meet fixed payments.

If this reserve is depleted before Strategy generates sufficient new revenues or finds alternative financing sources, the company may face pressure to sell assets or issue more stock, putting both preferred and common stock shareholders at risk.

Critics argue that relying on a structure dependent on ongoing market access may appear stable until financing conditions change.

Independent Bitcoin analyst Derin Olenik recently published a critical analysis of the company's debt situation, warning that the current ATM growth rate is unsustainable.

According to Olenik’s calculations, STRC's debt is growing at an alarming rate, with a nominal value increasing at a compound growth rate of about 30% per month.

At this pace, the company’s debt could double every three months and potentially increase tenfold in a year, which would significantly exacerbate cash flow and reserve pressures.

If this trend continues, Olenik estimates that Strategy will exhaust its $2.25 billion reserve in just nine to ten months instead of the expected two and a half years.

He warns that in order to make up for such losses without selling Bitcoins, Strategy will need to significantly dilute the equity of its common stock shareholders.

Even if MSTR returns to its previous all-time highs, Olenik calculates that the company would still need to issue over 1 billion new shares to pay preferred stock dividends, diluting existing common stock by nearly 400%.

With that in mind, he concludes, "If the ATM stops issuing, the accumulation of Bitcoins will also stop. If issuing continues, regardless of the stock price, the mathematics indicates that equity will be excessively diluted. From the perspective of common shareholders, STRC should not be regarded as digital credit, but rather as a digital suicide attack."

STRC Is a Convenient Way to Add Bitcoin

However, supporters of Strategy dispute the grim scenario put forth by Olenik.

They claim that Strategy has successfully attracted a unique group of investors who are yield-focused buyers willing to accept the fixed claims of STRC and limited upside potential.

By channeling these conservative investors' funds into assets with expected long-term volatility and higher upside, the strategy maintains Bitcoin exposure for common stock shareholders.

Preferred investors will receive a yield-oriented instrument currently trading more like short-term credit than a cryptocurrency alternative.

In fact, "short-term credit" refers to debt securities or financial instruments with relatively short terms (usually less than five years).

These investments are typically considered to have lower risk since their value is less sensitive to interest rate changes and is expected to return principal more quickly.

For STRC, this means its trading behaviors are more stable and predictable, resembling short-term corporate bonds rather than experiencing the typical price volatility of cryptocurrencies.

Notably, Strategy itself has consistently referred to STRC as its flagship "digital credit" instrument.

Bitcoin analyst Adam Livingston stated, "STRC is a machine that converts capital market access into long-term Bitcoin exposure, and if Bitcoin continues to compound in value, the fixed claims will become increasingly small relative to the assets."

Supporters believe that as long as the appreciation of Bitcoin outpaces the cash cost of paying preferred stock dividends, the model is effective.

In this case, each successful issuance of STRC converts capital market demand into additional Bitcoin holdings, and as Bitcoin appreciates over time, the fixed preferred claims will diminish relative to the asset base.

Saylor also reassured anxious investors, stating, "Our Bitcoin breakeven accounting yield is about 2.05%. If Bitcoin grows faster than this level, we can indefinitely pay dividends without issuing new MSTR stock."

MSTR Common Stock Shareholders Remain the Primary Audience

For MSTR holders, the real question is whether this financing model can continue to increase the value of common stock over time.

In the short term, the outlook is optimistic. STRC's trading volume has reached record highs, and the stock price remains at par, allowing Strategy to purchase $1 billion worth of Bitcoin in just a week using this market channel.

This result supports management’s view that STRC can serve as a reliable and repeatable funding channel rather than a one-off financing tool.

In the long run, matters are inherently far more complex. Each successful capital raise through STRC adds a layer of fixed equity claim before common stock.

The risk disclosures of the strategy itself acknowledge that future issuances of preferred stock may dilute the interests of existing shareholders, and unfavorable changes in financing conditions may make it more challenging to maintain the necessary dividend reserves.

Equity dilution refers to the reduction in the ownership percentage of existing shareholders when new shares are issued, thereby decreasing each shareholder's claim to the company's assets and profits.

Financing conditions are crucial because if the company cannot access low-cost or stable funding, it may struggle to raise sufficient capital to pay dividends or maintain its financial structure, increasing the overall risk to preferred and common stock shareholders.

In conclusion, STRC showcases both its advantages and exposes its risks. It is functioning as expected, attracting significant liquidity, and maintaining a price level close to par.

However, this has also created tension, as each round of issuance ties broader strategic arguments to the company’s ability to maintain market access, sustain dividend support, and uphold Bitcoin's value sufficiently to justify the financial system built around it.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。