Written by: Meltem Demirors

Translated by: Saoirse, Foresight News

Institutions have finally "entered the crypto industry" — but they are not here to take over.

They are here to turn the crypto economy into a fee cash flow machine for expanding their assets under management (AUM).

This is neither a judgment nor a critique, but simply an observation of the facts.

Please note: my views below primarily target crypto assets as tokens/digital currencies, and may not necessarily apply to blockchain as financial infrastructure (the latter can exist without tokens, as demonstrated by the vast majority of current DeFi governance tokens).

Since the digital asset summit last year, I have held this view. At that time, my keynote speech was titled "Believe in Something." In the past year, nothing has changed my perspective; instead, it has made the picture clearer.

Recently, my friends — Evgeny from Wintermute and Dean from Markets Inc — each wrote two excellent articles discussing the so-called "institutional adoption" in the crypto space and its implications for market cycles. They inspired me to write a third piece, adding a new perspective on top of their views: the rapidly changing landscape of capital and the intensifying battle for AUM.

No time to read the full version? Here’s the summary in one sentence:

"Institutional adoption" is not a mission, but a profit extraction strategy.

The real question is: can the crypto industry establish and support its own native institutions quickly enough to keep economic value on-chain instead of flowing continuously into traditional finance (TradFi)?

Traditional finance has been extracting most of the profits from the crypto economy

Looking at the flow of funds, it is clear who is actually profiting in the crypto space:

It is not the DeFi protocols, but those financial institutions that Satoshi originally intended to replace in the Bitcoin white paper.

- Just USDT and USDC alone can generate about $10 billion in net interest income each year, with profits going to Tether, Coinbase, and Circle. They are important participants in the crypto ecosystem, but ultimately serve only their shareholders.

- Cantor Fitzgerald, under U.S. Commerce Secretary Howard Lutnick, earns hundreds of millions each year by managing U.S. Treasuries for Tether and arranging trades for digital asset companies and investment products.

- President Trump, his family, and partners have collectively profited billions of dollars through a series of crypto-related projects and token tools.

- BlackRock's IBIT Bitcoin ETF reached an asset management scale of about $100 billion within approximately 18 months, becoming the fastest-growing ETF in history, and also BlackRock's most profitable product.

- Institutions like Apollo Asset Management are quietly directing crypto collateral and treasury funds into their own credit and multi-asset funds.

Every year, traditional financial institutions extract hundreds of billions or even trillions in assets and profits from the crypto economy, often earning more than the native protocols that actually create value.

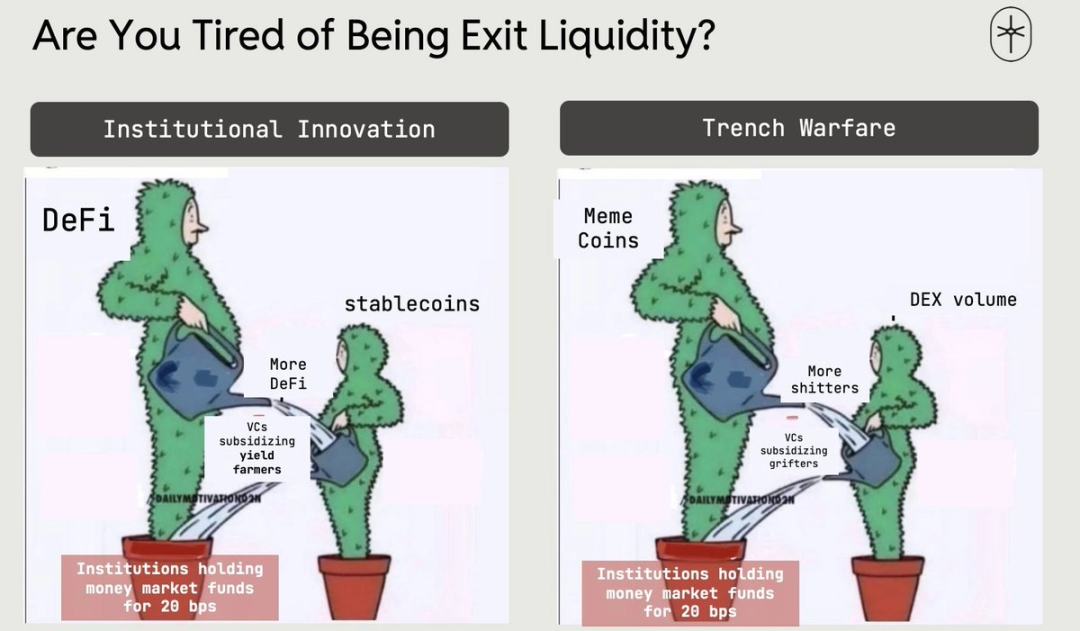

Those "industry innovators" who shout for institutional entry at countless conferences and the "frontline warriors" who fervently speculate on meme coins are actually more similar than you might think.

We should stop blindly following and start thinking independently.

What are institutions really thinking?

Businesses have only one goal: to maximize profits.

Crypto can help them make money in two ways:

- Cost reduction

Distributed ledgers, on-chain collateral, and instant settlement can significantly reduce back-end and middle-office costs, while enhancing collateral liquidity and utilization.

- Revenue generation

Packaging crypto into ETFs, tokenized funds, structured products, custody services, lending, cash management solutions... all can generate substantial and ongoing fees, while gaining fervent support from the crypto community.

For the past decade, institutions only cared about the first point.

When we founded DCG in 2015, I spent three years pitching the advantages of Bitcoin's global ledger and final settlement to all financial institutions. At that time, financial institutions did not see crypto as a new income source, but only viewed it as too risky; engaging with Bitcoin and token systems was utterly impractical for boards of directors.

In early 2018, I left DCG to join CoinShares, and our AUM grew from tens of millions to billions. A few independent managers who boldly invested in Bitcoin at that time achieved astonishing returns.

Early 2024 was a turning point: institutions began to see crypto as a second path — a new revenue machine.

The launch of BlackRock's IBIT was the tide that broke the dam.

IBIT became the most successful ETF in history, greatly enhancing BlackRock's profit margins.

A few key facts:

- Within a year of its launch, IBIT's scale surged to $70 billion, increasing at approximately five times the rate of the previous record-holder, the gold ETF GLD.

- After IBIT options launched at the end of 2024, it attracted over $30 billion in funding, with shares outperforming all competing products and accounting for more than half of the total market for Bitcoin ETFs.

- IBIT is BlackRock's most profitable ETF: with about $100 billion AUM, it generates hundreds of millions in fees annually, exceeding the income of BlackRock's nearly trillion-dollar S&P 500 flagship index fund.

IBIT has showcased a standard answer for the entire industry:

Bundle Bitcoin and digital assets into traditional fund structures, list them, and then turn them into stable, substantial fee cows.

From DAT, tokenized treasuries to on-chain money market funds, all are copy-pasting this playbook.

The AI capital expenditure supercycle is consuming global capital

Let’s slightly shift topics to discuss another key trend — this is also a significant reason why I immediately founded Crucible after the IBIT launch in 2024.

The value chain of computing power and energy is reshaping the global capital landscape in real time.

Over the next decade, building the AI economy (chips, data centers, power, factories, etc.) will require tens of trillions in capital expenditures.

Where will the money come from?

All liquid assets that are not directly tied to AI — cryptocurrencies, non-AI stocks, and even credit assets — are being sold off, swapped for what the market sees as "must-have AI assets."

At the same time, many LPs (limited partners) have overallocated in the private equity market, and with slower exits and returns, are quietly reducing or delaying new contributions to private credit and PE.

The financing cycle is becoming longer, less stable, and harder to predict.

The competition for quality AUM channels is becoming extremely intense.

The result is:

Asset management firms and private equity institutions are frantically raising money from insurance funds, retail and affluent individuals, sovereign wealth platforms — while traditional pensions and endowments are retreating.

The market is desperately thirsty for cash.

Anything that looks like a pool of funds will be drained.

On-chain capital is the next main battlefield for AUM

In the wave of competing for AUM (assets under management), crypto is no longer a strange toy —

It represents potential AUM worth trillions of dollars, just laid out in front of us.

IBIT has proven that crypto can become a huge profit machine, a "honey pot" for institutional allocators.

The Trump administration also stated that it would do everything possible to create an extremely favorable environment for crypto innovation.

Now, on-chain asset management and treasury funds have reached several hundred billion in scale.

- The total issuance of stablecoins is approximately $300 billion, with USDT accounting for about 60% and USDC about 25%.

- The total value locked (TVL) in multi-chain DeFi is approximately $90–100 billion.

- Tokenized money market funds, tokenized gold, consumer credit products, and other real-world assets (RWAs) add hundreds of billions in scale.

- However, the average yield on-chain is only 2%–4%, far lower than the 4.1% level of traditional money market funds; even Lido's nearly $18 billion stETH pool has a yield of only about 2.3%.

In the eyes of asset accumulators who are thirsty, this is not "DeFi locked value", this is yet-to-be-fully-monetized cash flow — ready to be packaged, staked, lent out again, and charged for.

This is not a moral judgment, but an instinct of institutions, as natural as breathing.

Source: DefiLlama

Tokenization and compliance packaging have transformed the originally "forbidden" crypto capital into fee-generating AUM compliant with traditional custody and risk control frameworks.

As enterprises, DAOs, and protocols accumulate vast crypto treasuries and seek safer external yields, asset management institutions can repackage these assets into tokenized funds, money market funds, structured products.

For companies facing funding pressure and intensifying competition for traffic:

"Plundering" crypto assets from their balance sheets is one of the cleanest paths to expand fee-generating AUM without squeezing already saturated traditional channels.

A wake-up call: if we don't act now, we will be swallowed up

Just as Western economies have allowed groups that do not identify with their culture and values to enter, and are now paying social and economic costs as a result, the crypto industry is facing a similar survival crisis.

The crypto economy and its core opinion leaders are bringing in traditional financial institutions that do not share the core values of the industry and are not committed to native economic growth.

The entire industry will soon pay a social and economic price for this.

If the situation continues to develop unchecked, the crypto economy will ultimately only become another liquidity appendage for the expansion of AUM (assets under management) by traditional financial institutions.

The only way out:

Establish and grow our own native institutions as soon as possible.

This includes on-chain asset management, risk control and underwriting, native financial products, crypto-native allocators...

They can compete for treasury AUM, design products that serve the long-term interests of crypto, and keep economic value within the crypto ecosystem instead of flowing out to inflate the profit statements of traditional giants.

If we do not prioritize supporting crypto-native institutions now, so-called "institutional adoption" will not be a victory, but an annexation.

Hold on to something, or we will have nothing.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。