Written by: Eli5DeFi

Compiled by: AididiaoJP, Foresight News

Token issuance in 2026 needs to face a harsh reality.

It is not a celebration, nor a reward for your hard work.

It is more like an "open coliseum"—any part of your token economic model that is not designed well will be seized by experienced individuals with better models, amplified, and utilized publicly.

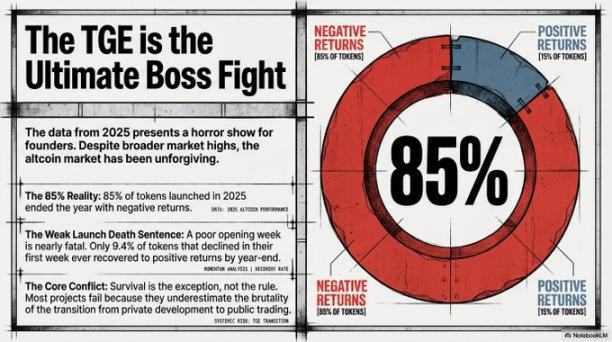

Arrakis Research has compiled data from 2025, and the results are clear: 85% of token issuance projects ultimately end up with negative returns.

This cannot be blamed on poor market conditions; bear markets do not specifically target poorly designed token economics, nor do they spare well-designed ones.

This number is a market alert for founders: Most people clearly prepare for a fight but only arrange a ribbon-cutting ceremony.

The good news is? The 15% that survived did not get lucky. They are simply meticulous in their work, and their methods are replicable.

"Poor performance in the first week is essentially a death sentence. Data shows that only 9.4% of tokens that drop in the first week manage to recover later." — Arrakis Research

This statement is worth pondering.

Summary

- Your token fails not due to bad luck, but because you didn't design it with success in mind.

- Tokens issued in 2025 saw 85% decline throughout the year. This is a design issue, not a market issue.

- Issuing at a "fully diluted valuation (FDV)" of over 1 billion dollars is akin to giving money to those who will never use your product, helping them "cash out high."

- Staking, governance, and custody are not "additional features"; they are the immune system of the token. Without them, the token can't withstand pressure once it launches.

- Only 9.4% of tokens that drop in the first week can recover; the performance in the first week basically determines life or death.

The "Laws of Physics" Behind TGE

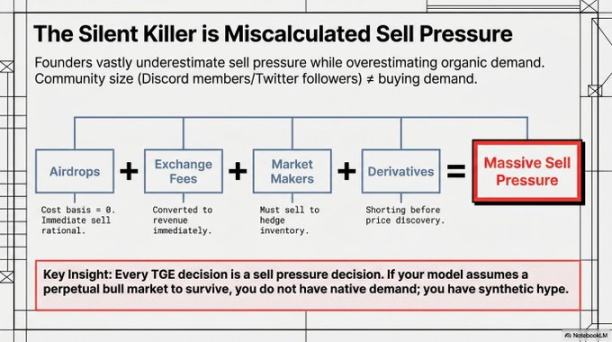

There is a useful mental model borrowed from physics concepts. Each token issuance has two opposing forces:

- Sell-off pressure = Gravity. It exists objectively, is patient, and does not care about your grand vision.

- Real demand = Rocket Engine.

The issue is not whether gravity exists (it always does), but whether your engine is strong enough to break free from gravity. Unfortunately, most teams build rockets without engines, then blame the planet's gravity.

Who Will Sell on the First Day? (It's Not Their Fault)

Many founders make a grave mistake here: treating sell-offs as betrayal. In fact, it’s simple mathematics.

The cost for airdrop users is zero. The rational choice is to exchange something received for free for real money. Data shows that 80% of airdrop users will sell their tokens within the first 24 hours. This isn't disloyalty; it's human nature.

Centralized exchanges receiving tokens as listing fees is their income. They rationally liquidate inventory.

Market makers, if cooperating using a "lending model" to hedge risks and prepare quotes with stablecoins, must also sell a portion of borrowed tokens. This isn't betrayal but part of the agreed model, which includes a mathematical formula.

Early short sellers jump in before the price stabilizes. They are seasoned professionals, often with more experience than you. They are not the issue; the problem is that you did not anticipate their arrival.

Many projects assume the above groups do not exist when designing their tokens. But they do exist. You either factor them in or learn a lesson from them.

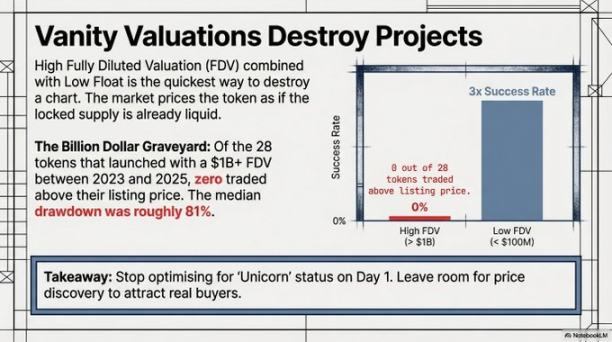

Valuation Traps (How to Fool Yourself with Math)

The most expensive vanity item in the crypto world isn't the avatar images but the ridiculously high "fully diluted valuation (FDV)."

A common trick is: the team only puts 5% of the tokens into circulation ("low circulation") but claims an FDV of 1 billion dollars.

When the market calculates: the remaining 95% of unreleased tokens are valued as if they "will never unlock"? That is impossible; they will eventually unlock. When that day comes, the price will drop like a "ski jump."

The data is shocking, and every founder should see it:

FDV at issuance

- Above 1 billion dollars: By the end of the year, not a single token's price will be above the issuance price. Median drop: 81%.

- Below 100 million dollars: The probability of good performance in the first month is three times that of tokens with over 500 million FDV.

The failure rate is 100%, not 70%, not 90%, but 100%.

Yet founders continue to flock in because having "billion-dollar FDV" looks good in press releases, allowing early investors to showcase attractive figures on paper before they can actually sell. In plain terms, this is a "pricing illusion," which the market will burst without mercy.

Being infatuated with the FDV on issuance day is like measuring a company’s success by how good the PowerPoint looks. It can deceive those who do not look at the long term. A lower valuation instead leaves room for real price discovery, which is essential for a sustainable market. Discreet issuances often survive, while vain issuances generally perish.

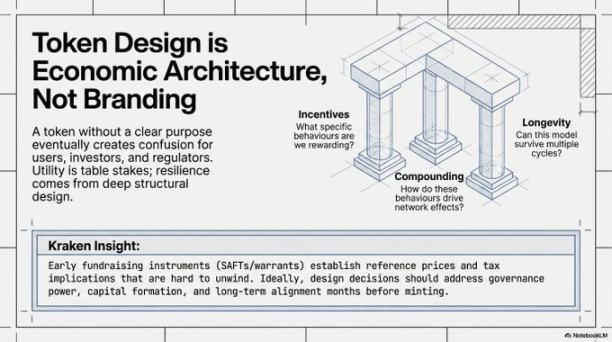

Four Charms (Truly Useful Items)

Arrakis summarized four key pillars that distinguish who survives from who merely pays tuition. We add our own understanding.

Charm 1: Witch Defense — Filter Before Issuing

A comparison of two cases makes the outcome clear:

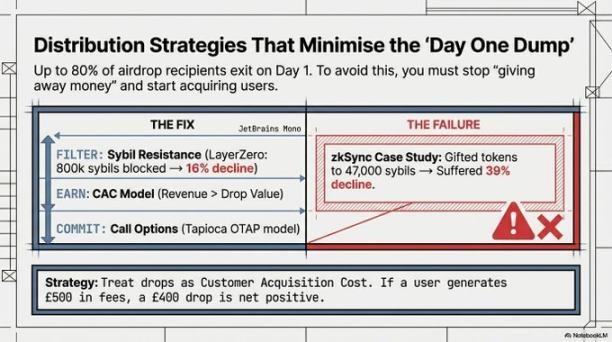

- @LayerZero_Core put in considerable effort, identifying 800,000 "witch addresses" (accounts created to exploit airdrops) before issuing tokens. These individuals will only sell the tokens instantly and never return. Result: A mere 16% drop in the first month.

- zkSync did not filter effectively, and as a result, 47,000 witch addresses received airdrops. Result: A 39% drop during the same period.

The difference between 16% and 39% is the cost of not doing due diligence.

Witch defense may seem troublesome, but you need to be clear: You are paying for actual users, not nurturing parasites. Those who farm airdrops are not interested in your product; they only want your tokens. You need to increase the cost for those who do not use your product to obtain tokens.

Charm 2: Revenue-Based Airdrops — Treat Airdrops as "Customer Acquisition Costs"

View airdrops from a different perspective: Don’t treat them as "community rewards"; treat them as "customer acquisition costs."

If a user contributes $500 in fees to your protocol, you reward them with $400 worth of tokens. Even if they sell all the tokens immediately, this customer acquisition is still profitable (net profit of $100). Real economic activity has already occurred; tokens being sold are just a number in the ledger, not a disaster.

Charm 3: Infrastructure Ready — Don’t Push Out a Car Without an Engine

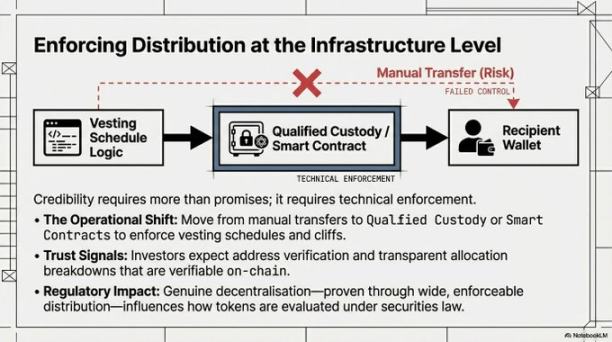

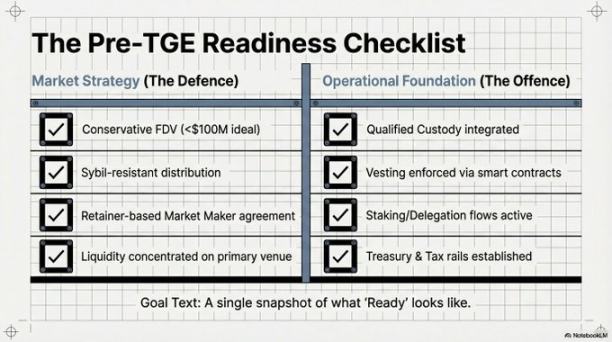

Staking and governance functions must be available at the moment the token is launched. Not "coming soon," not "under development," but "immediately available."

If not, the outcome will be as follows:

Early supporters receive tokens only to find they can neither stake to earn interest nor participate in voting. Capital becomes idle. Idle capital that does not earn yields will be sold off. This is not disloyalty, but basic investment management.

Furthermore, from day one, there must be a qualified custody solution in place that institutional investors will definitely assess as a hard indicator. If custody is merely a "multisig" without a compliance framework, large funds will not dare to enter. This is not creating trouble; it's about their need to control risks.

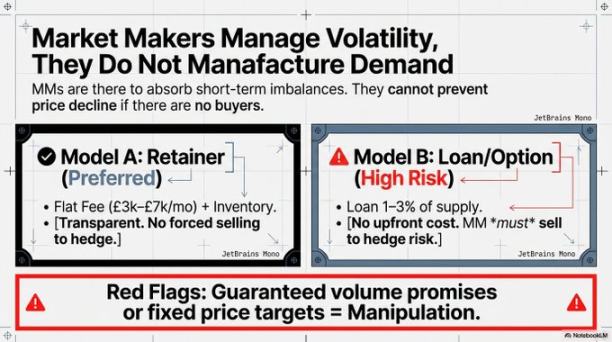

Charm 4: Choose the Right Market Makers — Understand What Service You're Buying

Market makers provide "depth" (market thickness) and not "demand" (buyers). This is important; some founders hire market makers thinking they've hired a "price security team." They only facilitate existing buying and selling but do not create buyers.

- A "hire-based" model is more transparent and better.

- A "lending model" can also be useful, but the market maker's own hedging requirements conflict with your pricing stability goals.

When looking for market makers, these are danger signs:

- Guarantees of trading volume targets

- Refusal to accept your conditions

- Promises to support during heavy sell pressure

These may imply they want to use "wash trading" instead of making a real market.

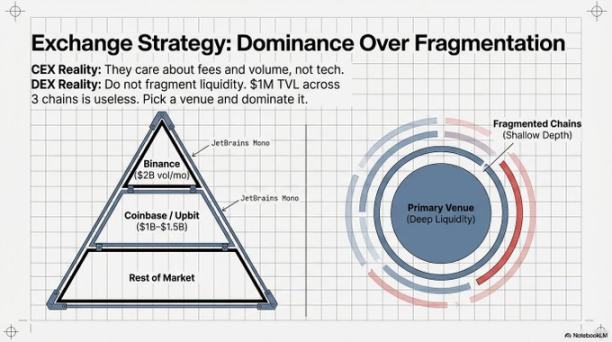

Liquidity should be concentrated. Spreading one million dollars across three chains, with shallow "depth" on each chain, wouldn't hold up under any turbulence. It's better to choose a main battleground and deepen that liquidity. One place with depth is better than three places with thin coverage.

Ultimate Goal: Decentralization

The infrastructure and distribution mentioned earlier are all defensive measures. The real long-term goal is to mature the protocol in four aspects:

- Decentralized Development: Not just the core team being able to code, but third parties can also participate in development through funding programs.

- Decentralized Governance: A transparent decision-making process with multi-party involvement, where proposals can truly be implemented.

- Decentralized Value Distribution: Economic design benefits more people instead of just enriching a small internal circle.

- Decentralized Participation Channels: Global users can participate in staking and voting in a compliant manner with low barriers, not limited to crypto veterans.

The brilliance of the Arrakis framework lies here. If a protocol is only well-prepared at launch but does not push for true decentralization, it merely postpones "centralized risks" without resolving them.

Final Thoughts

Arrakis's research is one of the most rigorous TGE analyses of the first quarter this year. The core point is correct: Token issuance is about deploying infrastructure, not about marketing activities.

Teams that treat it as marketing often create impressive "first-week charts," followed by "ski jump" declines. Those that treat it as infrastructure—seriously analyzing sources of sell pressure, preparing months in advance, not chasing inflated FDV, filtering out opportunists—often become part of that surviving 15%.

We want to add: The real demand for a token must come from the functionality of the protocol itself, not from marketing hype. People must genuinely need this token to utilize the value created by the protocol. If the only purpose of the token is to "govern a protocol that no one uses," then no matter how well you defend against witches or how compliant your custody is, it won’t matter. Governing something useless has no value in itself.

Before thinking about how to issue, first think about how to create real demand.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。