Written by: Rita

Trends Guide

In the past month, the US stock market has experienced significant fluctuations, with the Nasdaq rebounding from a high retreat. JPMorgan's fund flow report on July 15 provided a judgment: the deleveraging that started in June has not yet ended, and there is further room for compression in leveraged ETFs, options, and margin accounts; the US stock market still faces pressure in the short term.

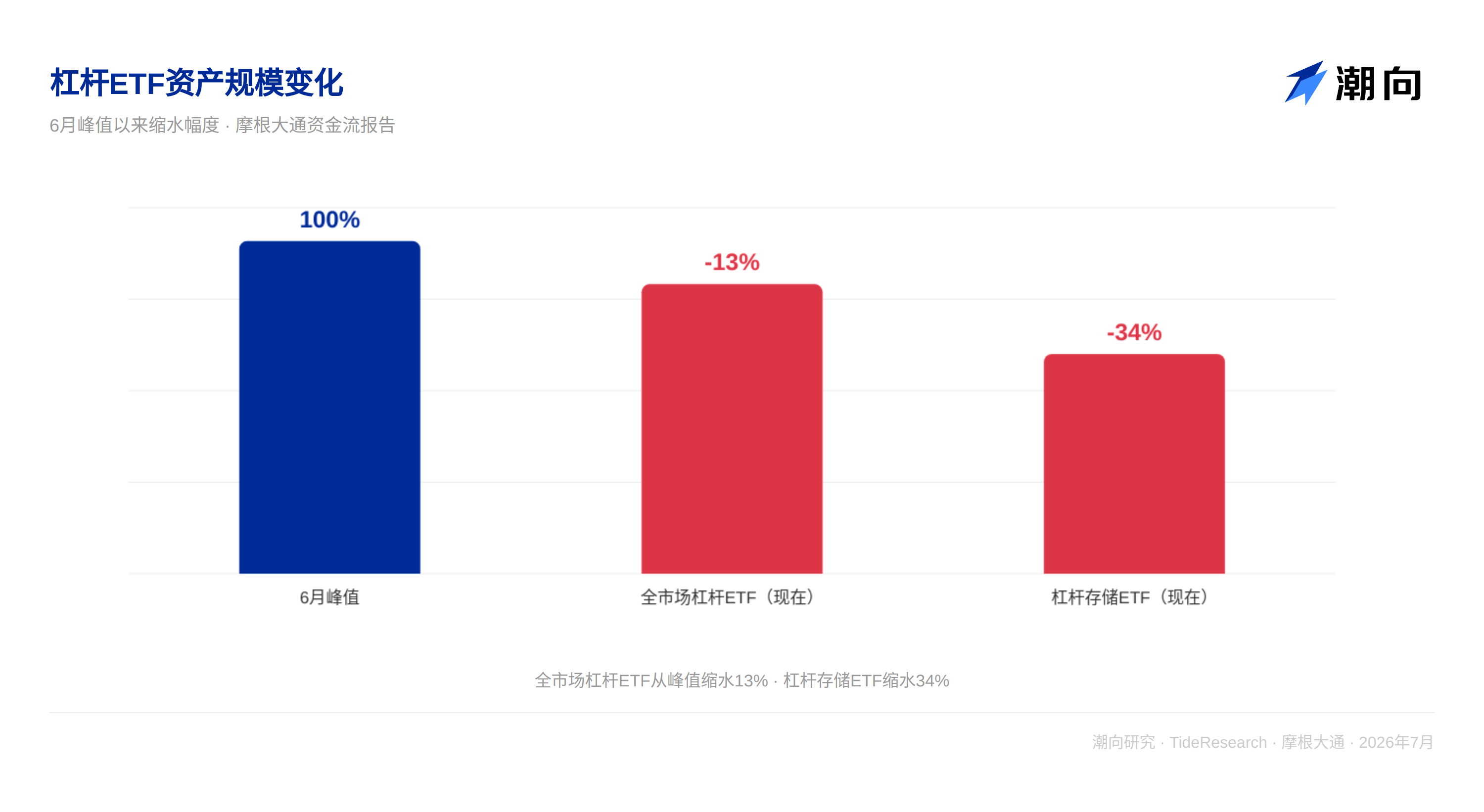

Leveraged ETFs were specifically mentioned by JPMorgan. These products can self-consume during volatile markets. An index that falls by 10% and then rises by 11.1% to return to its original position results in a 3x leveraged ETF losing 7%. This is the cost of convexity. Since the peak in June, the size of leveraged storage ETFs has shrunk by 34%, and the entire market's leveraged ETFs have decreased by 13%. However, JPMorgan believes that at the current pace, it will take about three more months of volatility for the scale of leveraged ETFs to return to the level before April.

The good news is that once the deleveraging ends, the supply-demand dynamics of long-term funds will provide support. Retail investors are still continuing to buy, sovereign funds are increasing allocations against the backdrop of rising oil prices, and overall demand still exceeds supply.

Leveraged ETFs are self-correcting but not yet complete

The issue with leveraged ETFs is structural. The daily returns of these products are a fixed multiple of the index returns for that day, performing well in a one-sided upward market but being repeatedly worn down in a volatile market.

JPMorgan used a simple example to illustrate: an index that falls by 10% and rises by 11.1% the next day to return to its original position results in a 3x leveraged ETF losing 7% over two days. This is the cost of convexity, which continues to erode asset size during range-bound fluctuations.

This mechanism is self-correcting. The higher the leverage, the greater the volatility, and the faster the loss. Since the peak in June, the AUM of leveraged storage ETFs has shrunk by 34%, and the entire market's leveraged ETFs have decreased by 13%. However, relative to the market value of the held stocks, the decline is still far from enough. JPMorgan believes it will need approximately three more months of fluctuating market conditions for the market value of leveraged ETFs to return to levels seen before April.

Additionally, since July, leveraged ETFs have continued to receive inflows, which will lengthen the deleveraging timeline. The market value of leveraged storage ETFs is three times that of ordinary ETFs, meaning the volatility source of storage stocks is highly concentrated in leveraged products.

Retail options and margin accounts are also deleveraging

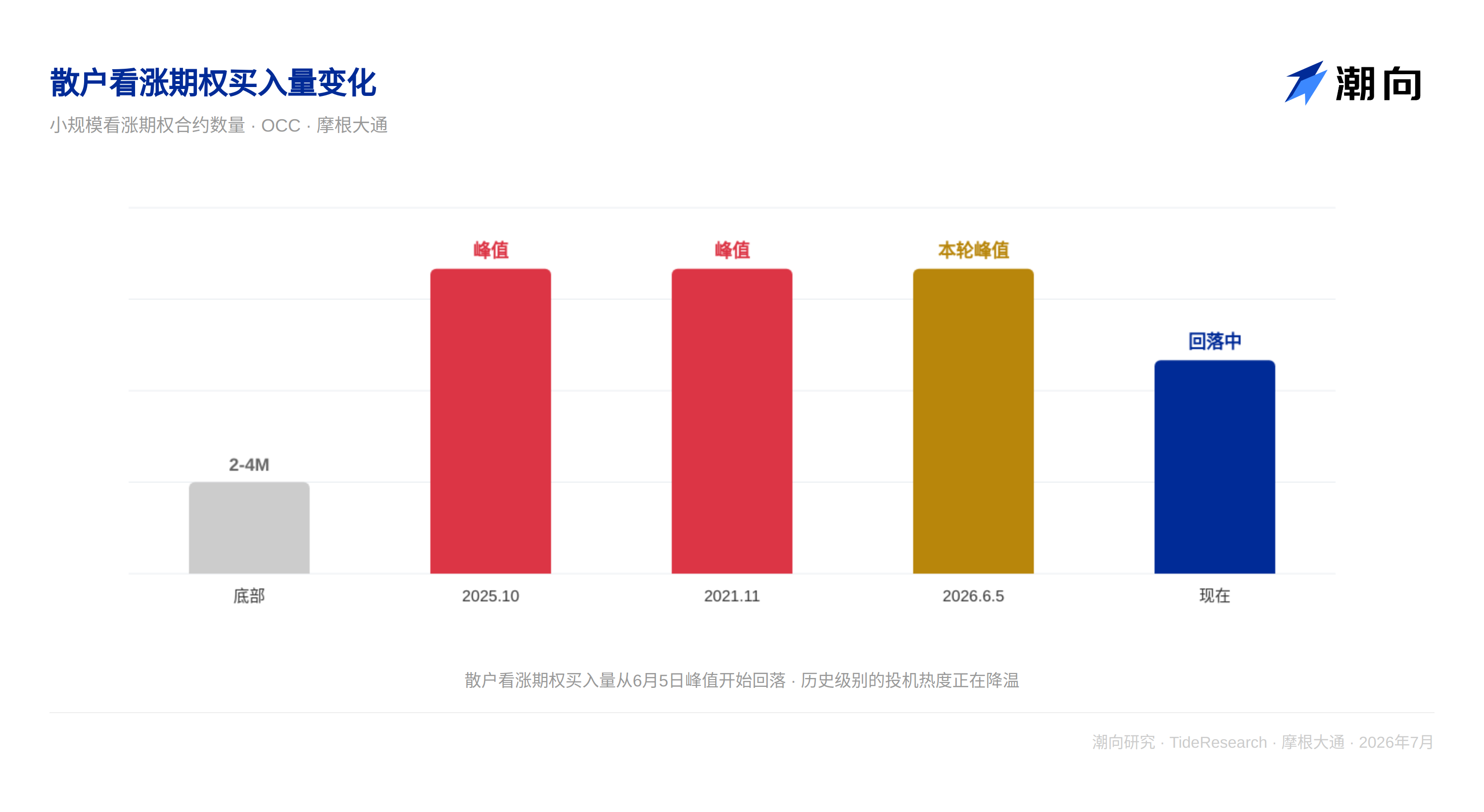

On June 5, the indicator tracking small-scale bullish options purchases by retail investors reached 14 million contracts, comparable to the peaks in October 2025 and November 2021. After the previous two peaks, technology stocks underwent months of corrections until this indicator fell to between 2 million and 4 million contracts.

The current indicator has fallen from its peak, but it is still far from historical lows. JPMorgan believes that the retail impulse in the options market is fading, which continues to be a suppressive factor for technology stocks (the sector preferred by retail investors).

The leverage in margin accounts is also at extreme levels. The net borrowing balance tracked by JPMorgan shows that the current level is comparable to the peaks at the end of 2021 and mid-2018. After the previous two peaks, the market underwent months of adjustments. Currently, this indicator has only just begun to show initial signs of decline, far from returning to normal.

Hedge funds are already reducing positions

In June, despite the declines in the S&P 500 and Nasdaq, long/short equity hedge funds and TMT sector funds still achieved positive returns (up 1.2% and 3.7%, respectively). The reason is that their overweight positions in semiconductors hedged against losses. The SMH Semiconductor ETF rose 9.5% in June, while large-cap technology stocks fell 14.5%.

However, the situation changed in July. The daily frequency hedge fund leverage indicator tracked by JPMorgan shows that the leverage of long/short equity funds has fallen from historical highs in June, and their correlation with semiconductors is also weakening. This suggests that hedge funds may have reduced their semiconductor positions in July.

The leverage of risk parity funds has returned to normal levels and no longer poses additional selling pressure.

Long-term funds are still waiting

Retail investors are the largest buyers, with a net purchase of about $550 billion year-to-date, and the total for the year is expected to exceed $1 trillion. CTAs (Commodity Trading Advisors) and long/short equity hedge funds have accumulated purchases of about $40 billion this year. Sovereign wealth funds and central banks are expected to contribute about $110 billion in stock demand for the year due to rising oil prices.

Pension funds and insurance companies are stable net sellers, expected to sell about $470 billion for the year, but half of this has already been completed. On the supply side, due to large IPOs and refinancing, the net supply this year is about $200 billion, an increase from last year's zero supply but still within a controllable range.

In summary, the total stock demand for the year is about $775 billion, with supply at about $200 billion, resulting in a net demand of about $275 billion. There is still about $200 billion of net demand to be released in the second half of the year; once deleveraging ends, this capital will become a bottom-supporting force in the market.

Trends Perspective

This JPMorgan report helps investors differentiate between two time scales of forces. In the short term, deleveraging is a self-correcting process that requires time. The convexity losses of leveraged ETFs, the fading enthusiasm for retail options, and the compression of margin accounts cannot be completed in one or two weeks. JPMorgan estimates a timeline of "three months", which serves as a useful reference anchor.

However, looking at a longer time dimension, the liquidity is not poor. Retail investors are still buying, sovereign funds are increasing allocations, and CTAs and quantitative strategies still have room to increase positions. The reason this capital has not pushed up stock prices now is due to the short-term impact of deleveraging counteracting their influence.

For investors, this means that the short-term market fluctuations may be the tail end of deleveraging rather than the beginning of a new decline. The key is to distinguish between "deleveraging" and "deteriorating fundamentals"; the former is a structural self-correction, while the latter is the real risk.

Disclaimer

This article is an organization and interpretation of the research report from a third-party broker (JPMorgan, July 15, 2026) by Trends Research. The ratings, target prices, earnings forecasts, and related judgments quoted in this article are solely the opinions of the analysts of that brokerage and do not represent the views of Trends Research, nor do they constitute any investment advice.

The market carries risks, and decisions should be made independently. This article should not be used as a basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。