This is a market with a scale of 2 trillion dollars.

Written by: Vaidik Mandloi

Translated by: Block unicorn

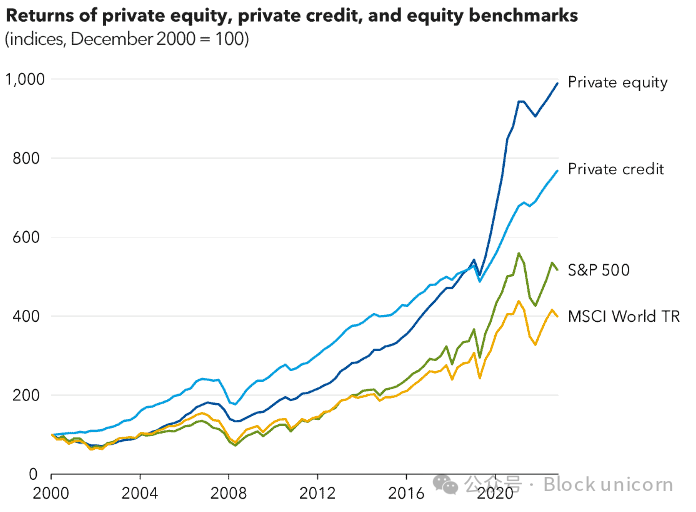

In the 1970s, Bruce Bent and Henry Brown created the first money market fund in history. The idea was incredibly simple. Due to a regulation during the Great Depression, the interest rate cap for savings in American banks was 4.5%. Although the yield on U.S. Treasury bonds exceeded 9% at that time, the minimum investment to purchase these bonds was as high as 10,000 dollars. Therefore, Bent and Brown decided to pool small deposits to purchase Treasury bonds on a large scale and return the profits to investors. Today, the size of money market funds has reached approximately 8 trillion dollars.

Stablecoins have been engaging in similar operations, but this time the asset is private credit, a market worth 2 trillion dollars, which requires at least 1 million dollars to enter. Yield-stable coins are used to gather small deposits and channel them into the credit space.

Today, I will delve into how this has happened and how Goldfinch (the first attempt to conduct such operations with real funds) collapsed, resulting in 56 million dollars of depositor funds being trapped in motorcycle loans in Kenya.

How Stablecoins Became Money Market Funds for Private Credit

In the 1990s, U.S. banks provided about half of the debt capital to businesses and consumers, but today that figure has dropped to approximately 20%. This is because new capital rules enacted after 2008 made it too expensive for banks to hold leveraged loans. As a result, banks completely exited the mid-market lending business, and private credit funds took their place.

Apollo, Blackstone, and KKR raised funds from pension funds and insurance companies, began lending to companies abandoned by banks, and charged high premiums because these borrowers had no other choice.

The market size has grown from less than 200 billion dollars in 2008 to over 2 trillion dollars today, with almost all of this funding coming from institutional investors writing checks of 5 million dollars or more.

One of the main reasons for the million-dollar minimum threshold in private credit loans is the difficulty in managing them. Each transaction requires due diligence, restructuring, and years of monitoring. Managing a fund where ten institutional limited partners (LPs) each contribute 50 million dollars is far easier than managing a fund where individual investors each contribute 500 dollars, and even then, large-scale investments often struggle to be profitable. For this reason, only pension funds and insurance companies have been able to access such yields over the past decade, with returns typically ranging from 8% to 12%.

It was at this time that yield-stable coins changed the game, much like Bent and Brown opened access to the Treasury in the 1970s. Although the associated procedures are still handled by institutions, with funds like Apollo responsible for underwriting and managing risk, tokenized sub-funds can now accept deposits of any size and invest them into institutional strategies without the need to manage thousands of individual investors.

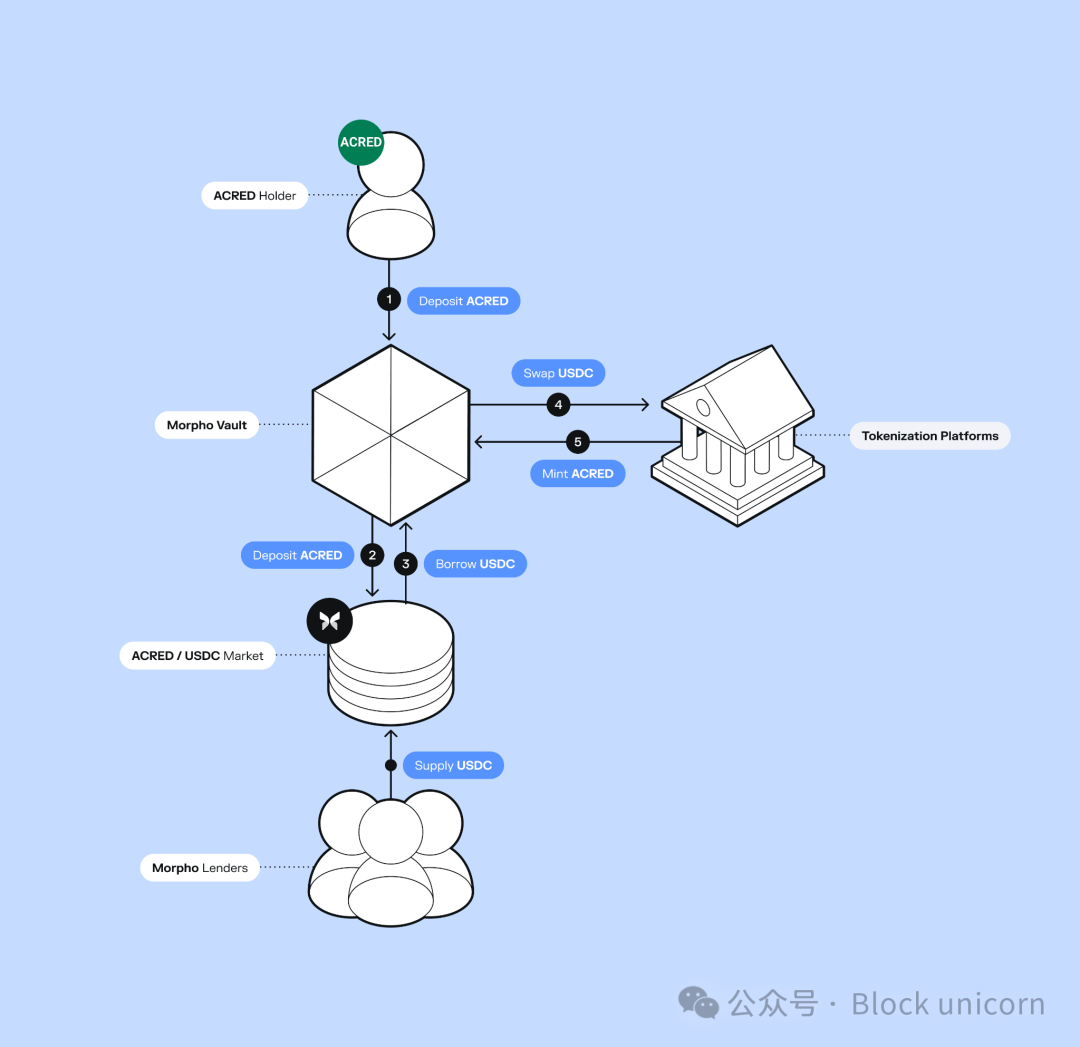

Apollo recently launched the tokenized fund ACRED, which has attracted 109 million dollars in capital inflows for its diversified credit fund. Investors can even use it as collateral on the Morpho platform for collateralized loans and revolving investments, thus gaining leveraged returns.

Figure has built a complete on-chain lending system, issuing 21 billion dollars in loans, successfully listing on Nasdaq, and launching YLDS—a yield-stable coin with a circulation of 376 million dollars. Other protocols, such as Pyse and Glow, go further by tokenizing solar projects, allowing investors to fund solar installations in developing countries with just a few hundred dollars and earn an annualized percentage yield (APY) from monthly electricity bills.

This does not mean that minimum investment restrictions for the fund itself have disappeared. The ACRED fund still requires a direct investment of 5 million dollars. However, once the fund is tokenized, its tokens can be traded on the secondary market, and there is no minimum investment threshold. It can also operate in coordination with the DeFi (decentralized finance) system in ways that traditional fund shares cannot reach.

In traditional private credit, your funds could be locked up for years, with a quarterly redemption cap of 5%. But on-chain, funds can be flexibly pooled and are liquid 24/7. For companies like Apollo and Figure, this allows them to access 315 billion dollars in stablecoin funds that are actively pursuing yield. After tokenization, these funds can directly enter this pool, creating new distribution channels without having to build retail infrastructure from scratch.

A year ago, the total amount of on-chain private credit was only 400 million dollars; it has now reached 5.87 billion dollars, a 15-fold increase in 12 months, but this still only accounts for 0.30% of the 2 trillion dollar global private credit market. In the first quarter of 2026, half of the newly issued stablecoin supply came from yield-stable coins, indicating that most of the new stablecoin funds are now chasing active yield rather than just being pegged to the dollar.

Moreover, since every dollar of on-chain credit can be used as collateral and recycled through DeFi protocols, the actual financial activity generated is several times the dollar amount.

For example, with ACRED. An investor deposits 10,000 dollars on Morpho, uses this deposit as collateral to borrow 7,000 dollars in USDC, then uses this USDC to buy more ACRED and deposits it again as collateral. This way, the deposit generates over 17,000 dollars in credit risk exposure. In comparison, in traditional private credit: the same 10,000 dollars would sit idle in the fund for 5 years without any yield. But on-chain, this compound effect occurs simultaneously at multiple levels, which is why the growth rate of the ACRED market's scale significantly exceeds the level shown by its original dollar amount. However, this also means that once the underlying loans default, losses will affect every layer of the cycle.

Tokenization does not mean that potential risks will also decrease. Generally, these risks are ignored due to the constant influx of funds, as these new funds are sufficient to pay redemption amounts. But as the capital inflow slows, the gap between token promises and actual loan values begins to emerge. Investors try to exit, but liquidity is insufficient, or the token price is decoupled from its intrinsic value.

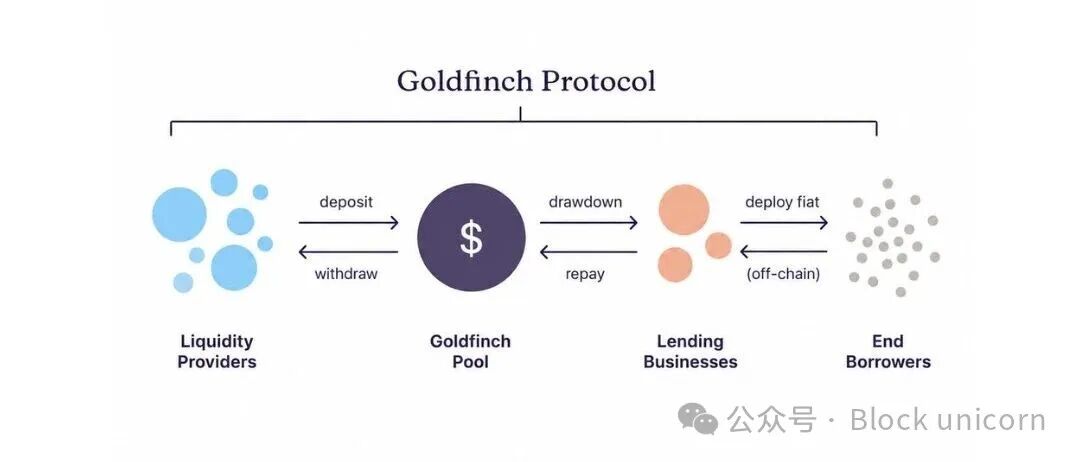

Goldfinch has experienced a similar situation; it was one of the first protocols to put private credit on-chain in 2021, but recently had to close due to 56 million dollars of depositor funds being trapped in Kenya and Nigeria.

Where Did Goldfinch Go Wrong?

Goldfinch raised 25 million dollars from a16z in 2021, injecting cryptocurrency funds with yields of only 2% to 3% in DeFi lending pools into businesses across Africa and Southeast Asia. Borrowers at these companies had to pay interest rates of 15% to 25% because local banks were unwilling to serve them.

The idea was to allow anyone holding USDC to deposit into the Goldfinch fund pool, and then a smart contract would allocate the funds to the corresponding borrower accounts within seconds. However, underwriting a loan for a motorcycle finance company in Nairobi means someone must understand the transport economy in Kenya and personally verify the borrower's accounts. If payment disruptions occur, they may even need to visit the borrower’s office in person.

But on the blockchain, these things cannot be realized. Once USDC is converted to Kenyan Shillings and placed into the loan book, depositors have no way of knowing how their funds are being used, how the borrower’s financial situation is, or even whether the loan terms are being fulfilled. All key information related to the loan performance has left the blockchain and is in the hands of borrowers in countries where most depositors have never set foot.

This is why, months later, it was noticed that Tugende Kenya had transferred 1.9 million dollars of its 5 million dollar loan limit to Tugende Uganda without authorization in 2022. Nearly 40% of the loans were transferred to another legal entity in another country. Meanwhile, depositors continued to earn what they thought was 10% to 12% interest, completely unaware that the principal supporting their returns had flowed to places not mentioned in the loan agreement.

If a traditional private credit institution discovered such a serious default, it would recall the loan and enforce a restructuring within days, but Goldfinch’s depositors only learned about this through posts on the corporate governance forum, and their only option was to vote on a proposal, which had no legal authority to seize assets or audit remaining assets.

By 2023, Tugende had completely defaulted and vanished. Goldfinch issued a total of 24 asset pools over its 113.3 million dollar lifespan, of which only 13 eventually paid back in full. The remaining 8 asset pools had a total of 53.82 million dollars in unpaid loans, and none were fulfilled as originally agreed. Most asset pools were undergoing restructuring, with monthly repayments for each asset pool being less than 51,000 dollars, meaning at this rate, recovering all 53.82 million dollars would take 8 to 15 years.

Goldfinch assumed all the risks associated with currency fluctuations in emerging markets and limited credit histories, while lacking the infrastructure that traditional lending institutions spend decades establishing and managing to mitigate these risks. For instance, banks providing loans in Kenya have local offices and relationships with regulators, giving them greater bargaining power when issues arise in transactions.

However, Goldfinch sent funds from global anonymous wallets to the same type of borrowers without any such supporting structure, which made the information gap between lenders and borrowers larger than in traditional transactions and left depositors with almost no ability to intervene when things fell apart.

The transfer of on-chain funds accounts for only about 10% of the overall process required for lending. The remaining 90% is underwriting and fund recovery, which is highly localized and costly work. Such underwriters need to establish a credibility baseline for the entire asset class, which is still struggling for its right to exist. Every dollar lost in underwriting makes it harder for the next institutional partner to go on-chain and diminishes the credibility of the entire asset class. The difficulties in credit are not related to on-chain operations, and anyone building in this space without understanding this is akin to crafting the next "Goldfinch" (a reference to a failed case).

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。