Author: Nancy, PANews

Reversing the downward trend at the end of June, the cryptocurrency market has recently welcomed a significant rebound. Leading with Bitcoin, mainstream crypto assets have rapidly reclaimed previous losses, with several on-chain indicators gradually releasing signals of reaching a bottom, adding optimistic expectations for future market trends.

However, while the market shows signs of warming, issues such as insufficient spot demand, institutional funds standing by, and continued pressure on altcoins still bring uncertainties for the subsequent market moves.

Is the July reversal market here? The crypto market sees a collective slight rebound

Historical patterns indicate that July is usually the strongest month for summer performance in the crypto market. With the arrival of July, the market is experiencing a turnaround, with crypto assets overall warming up and regaining upward momentum.

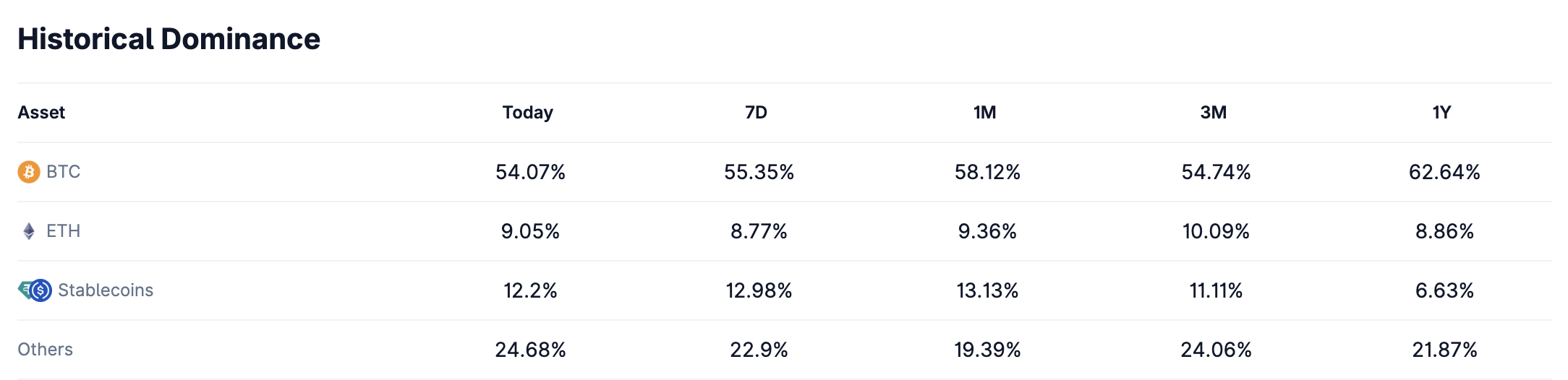

According to CoinGecko, the total market capitalization of cryptocurrencies has rebounded from a recent stage low of $2.1 trillion to the current $2.28 trillion. Bitcoin has strongly rebounded, regaining above $63,000, reaching a new high in two weeks and recovering all losses from the end of June; Ethereum continued its uptrend, rising 12.9% over the week, with its market capitalization share increasing to 9.05%; the altcoin market (excluding stablecoins) has also significantly warmed up, with its market cap share rebounding from 19.39% one month ago to 24.68%.

It is worth mentioning that due to the promotion of celebrity coins like ANSEM, CZ and TCC, the MEME coin sector on Solana and BNB Chain has recently shown signs of warming, with on-chain trading volume and active address numbers significantly increasing.

The recent slight rebound is mainly driven by multiple factors such as improved macro expectations, capital inflow, and short squeezing in the derivatives market.

On the macro level, it has become an important catalyst. The U.S. non-farm payroll data for June significantly underperformed expectations, with only 57,000 new jobs added, well below market expectations, and the labor participation rate falling to a five-year low, causing a notable cooling of expectations for a Fed rate hike in September. Meanwhile, the newly appointed Fed Chair Waller released slightly dovish signals, further dampening expectations of rate hikes for the year. As liquidity expectations improve, capital is flowing back into crypto assets and gold, with risk appetite significantly warming up.

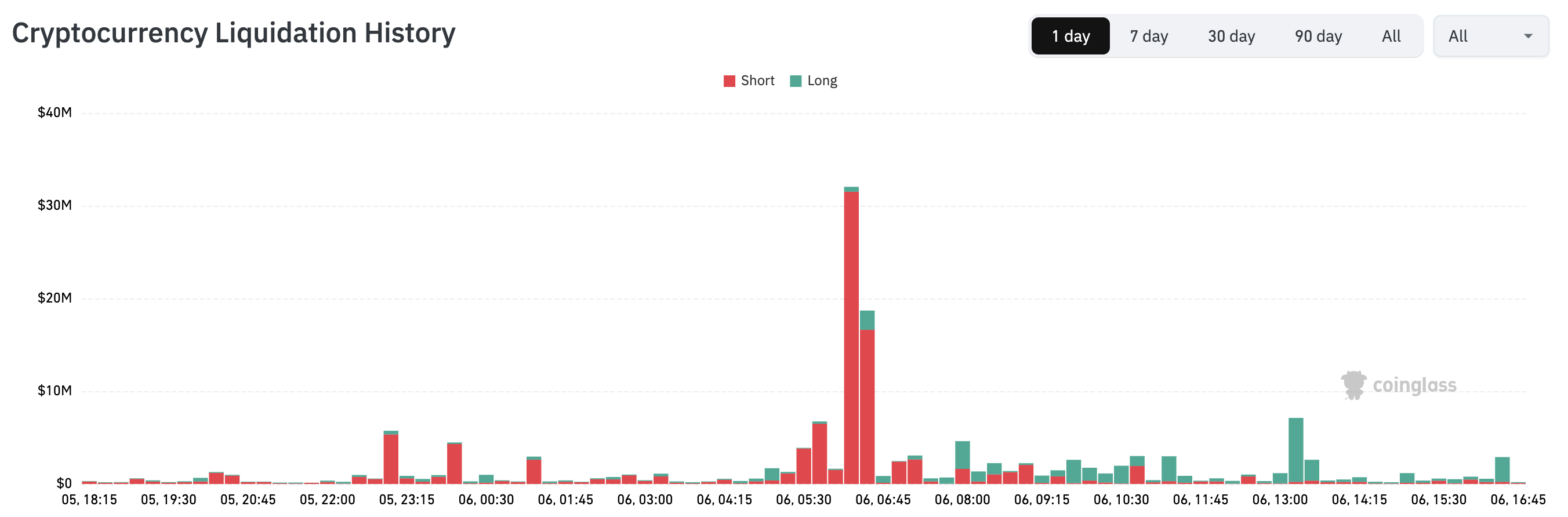

The derivatives market has further amplified the strength of this rebound. With Bitcoin quickly breaking through resistance levels, many short positions were forced to close, leading to a short squeeze that pushed prices higher. For example, on July 6, Coinglas data showed that the total amount of liquidated short positions across the network exceeded $92.04 million, far exceeding the $40.71 million of liquidated long positions.

The capital side also shows positive signals. The U.S. spot Bitcoin ETF ended a consecutive 10-day net outflow, with a net inflow of approximately $220 million on July 2. Meanwhile, Bitcoin whales continue to buy in at lower levels. According to Bitfinex analysts, wallets holding more than 1,000 BTC have been increasing their positions contrary to market sell-offs, accumulating over 270,000 BTC (approximately $16.7 billion) in the past two weeks, with their holdings returning to a six-month high.

Multiple bottom indicators are lighting up, but still face emotional and capital tests

Despite multiple on-chain indicators frequently releasing bottom signals, the overall crypto market has not yet shaken off the pessimistic atmosphere, and emotions and capital fronts have not seen substantial improvement.

Currently, market sentiment in the crypto market remains at historical lows. As for the crypto market fear and greed index, it currently stands at only 23, still in the "extreme fear" range, with 7-day and 30-day averages of 18 and 16 respectively.

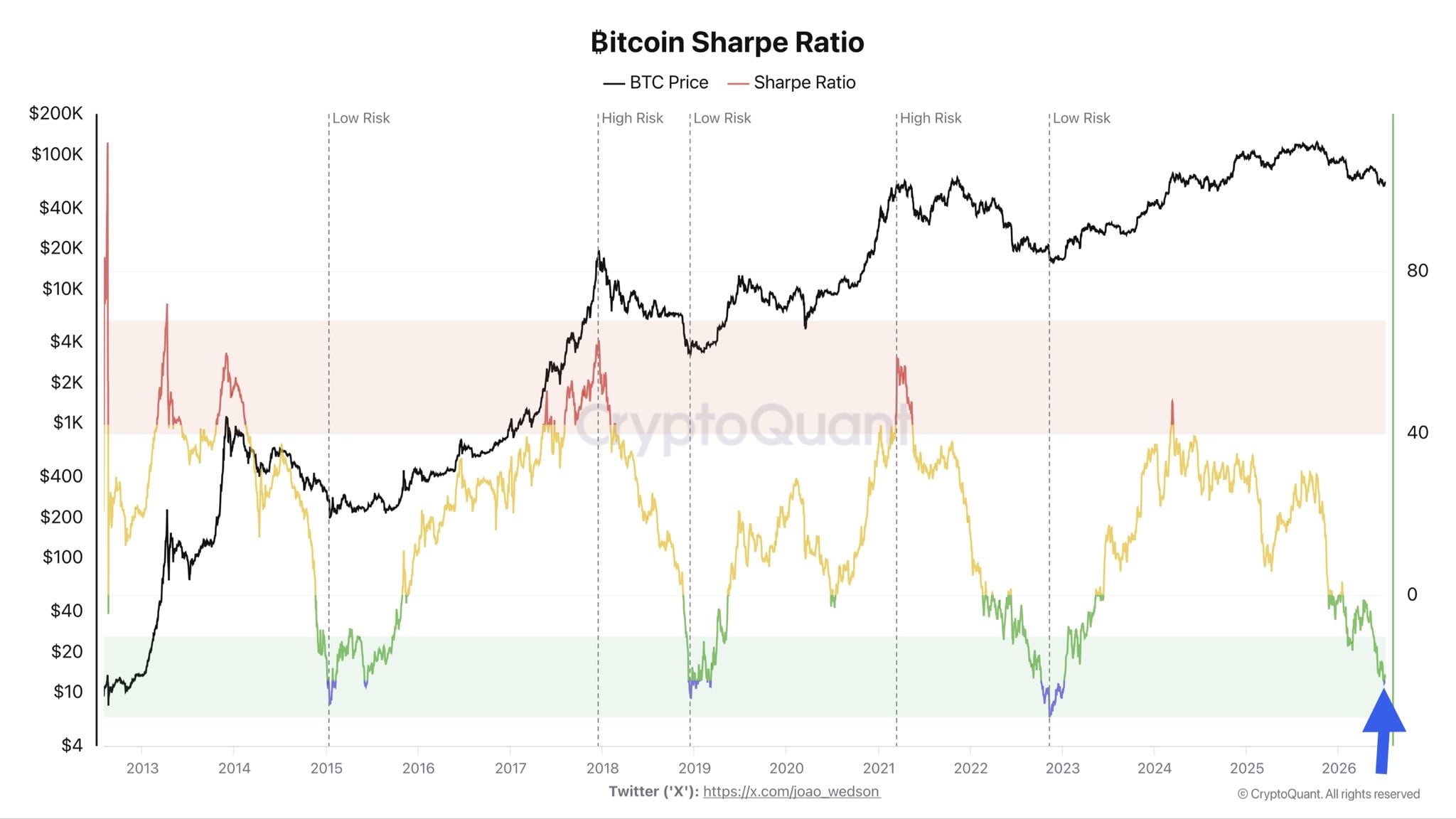

On-chain risk-return indicators also reflect that investor sentiment is still low. CryptoQuant analyst Darkfost states that Bitcoin's Sharpe Ratio has recently fallen below -20 again; although it has slightly rebounded afterward, historical experience shows that this level typically occurs only during extremely pessimistic market periods. The Sharpe Ratio is used to measure the return performance relative to risk, with negative values indicating that the risks taken by investors have exceeded the returns obtained. Similar periods of extreme pessimism often last for weeks or even months, accompanied by the market repeatedly finding a bottom.

Currently, active Bitcoin investors are still generally in a losing position. Darkfost analyzes that the AVIV (Active Value/Investor Value) ratio is currently hovering around 0.8, indicating that all active Bitcoin investors are averaging a floating loss of about 20%. Compared to the extreme levels of 0.5 to 0.6 seen at previous bear market bottoms (corresponding to losses of 40%-50% for investors), the current overall loss level of investors has not yet reached extreme bear market levels. This indicates that, although the market has entered a value range, there remains a certain gap from a typical bear market bottom. However, he also emphasizes that Bitcoin still follows its cyclical rules, and there is no need to wait for all indicators to fall to historical extremes for a rebound to occur in the short term, but the current situation of widespread losses among holders must be acknowledged.

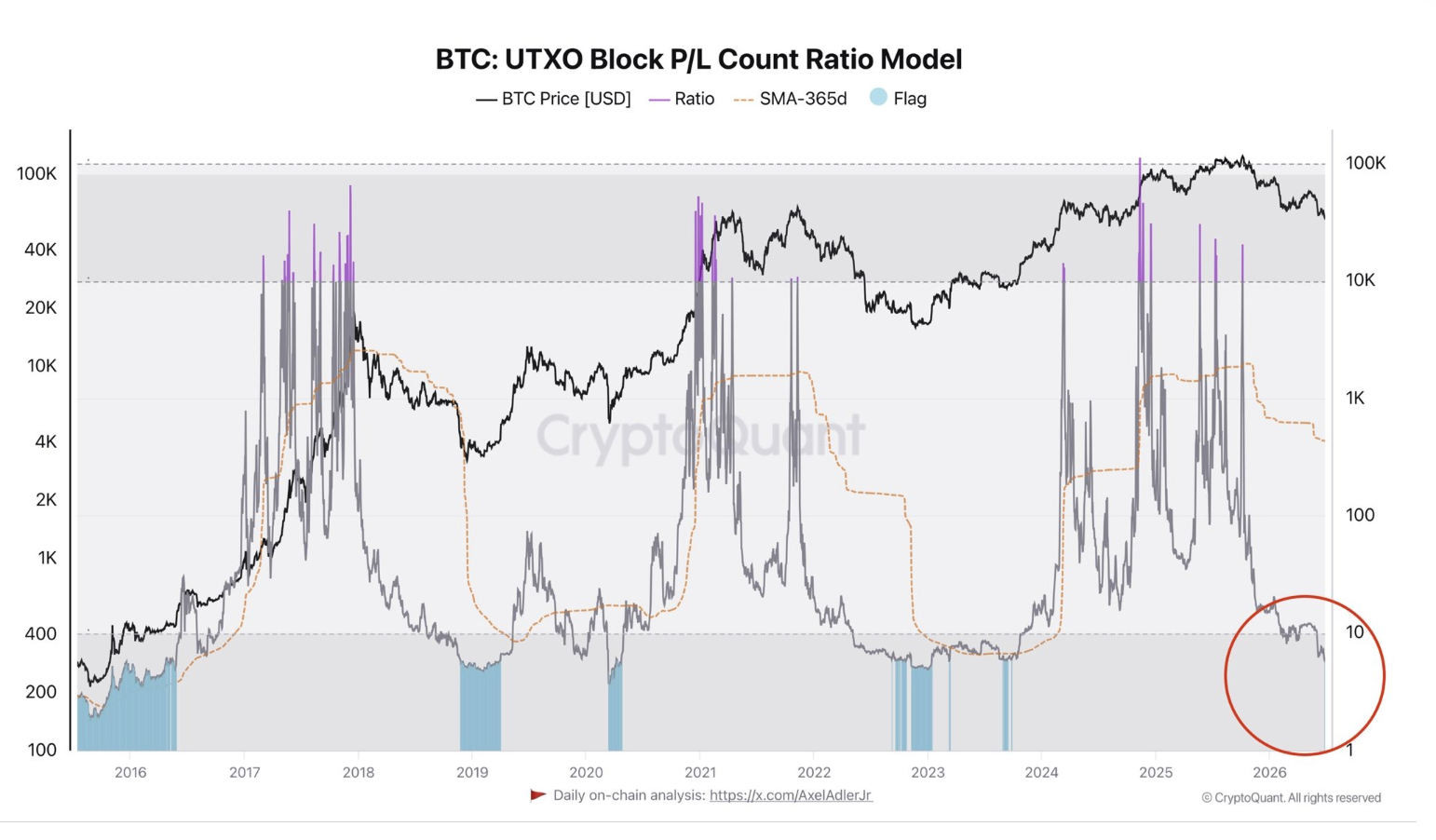

Meanwhile, on-chain data indicates that the market has clearly entered a "surrender" phase. Darkfost further points out that the UTXO profit and loss ratio has prompted the first "surrender" signal of this bear market. Currently, the proportion of on-chain losing trades has dropped to the lowest level of this bear market compared to the proportion of profitable trades. Historically, this indicator has appeared multiple times in market bottom regions. The last time it dropped to a similar level was during the mid-2023 bear market bottom, when Bitcoin's price briefly fell to about $26,000.

Institutional funds also remain cautious. According to Coinglass data, the Coinbase Bitcoin premium index has maintained negative values for 48 consecutive days since May 19, setting a record for the longest continuous negative premium since the launch of this index, exceeding the approximately 30 days of continuous negative premium during the "10·11 crash". The Coinbase premium index is mainly used to assess the demand for Bitcoin from professionals and institutions. Historically, sustained negative premiums tend to coincide with the exit of institutional funds from the U.S., warranting caution about short-term pullback pressures.

However, from the Bitcoin bottom-buying index AHR999, this indicator has currently dropped to 0.32, nearing historically low ranges. Over the past decade, this indicator has only fallen below 0.3 in extreme market conditions, including early 2011, the bear market bottom of 2018, the "312 flash crash" triggered by the pandemic in 2020, and during the FTX collapse in 2022. Although it has not yet fallen below 0.3, it is already at a historically rare level.

In addition to investors, miners are also under increasing pressure. On-chain analyst @gaah_im points out that the Bitcoin miner cyclical pressure composite index has fallen to its lowest level since 2026, re-entering a historically undervalued range. This index combines the Puell Multiple and the reverse miner surrender index, reflecting changes in miner income and selling pressure. Historical data shows that this indicator has signaled at several crucial market bottoms in 2015, 2018, 2020, 2022, and near 2024. Notably, during the market surrender period in 2015, this composite index reached zero for the only time, when the price of Bitcoin briefly dropped from about $300 to $160. If this indicator exhibits similar behavior again in 2026, it will mark that miner pressure has reached historically rare levels again.

Still in a repair market, $70,000 may become a key reversal level

Currently, this round of increase is more inclined to be a corrective rebound after the previous excessive decline.

Crypto analyst Murphy also points out that during Bitcoin's rebound process, the relative trading volume of the spot market has quickly declined. In the absence of spot demand driving the market, such increases often struggle to evolve into trend reversals and are typically just emotional recovery markets, with subsequent focus needed on the sustainability of the rebound.

However, Murphy notes that there have been some positive changes regarding capital. On a positive note, the USDC/USDT exchange rate has fallen from 1.001 to 1.0006, indicating that market exit willingness has weakened and trading willingness is recovering; meanwhile, although mainstream stablecoins within trading platforms are still in a net outflow state, the outflow rate has continued to narrow, suggesting that the marginal improvement in capital pressures provides some support for the continuation of the rebound. However, the weakened spot driving force implies that the weight of derivatives has relatively increased. The 7-day average of perpetual contract long premiums has continued to rise to $160,000/hour, indicating that Taker buying is continuously pushing perpetual contract prices above spot prices; despite a decrease in current open interest, it still remains significantly above the levels from February of this year. The current long premium is still within a relatively normal range, but as the rebound continues, the risk of long squeezing will continue to accumulate, and if open interest rebounds again, intense long and short battles will lead to sharper and faster fluctuations, which is worth paying close attention to.

For the potential rebound space, Murphy has segmented the target range into three nodes: $64,000, $68,000, and $70,000. Among them, $64,000 and $68,000 correspond to the short-term cost accumulation zones for Bitcoin (positions held for less than 1 month and less than 3 months); while $70,000 corresponds to the short-term holder realized price (STH-RP), which is typically seen as the dividing line for bull and bear sentiment, with historical trend reversals often beginning when the price effectively breaks through this critical level, thus $70,000 is regarded as the ceiling for this rebound in the bear market.

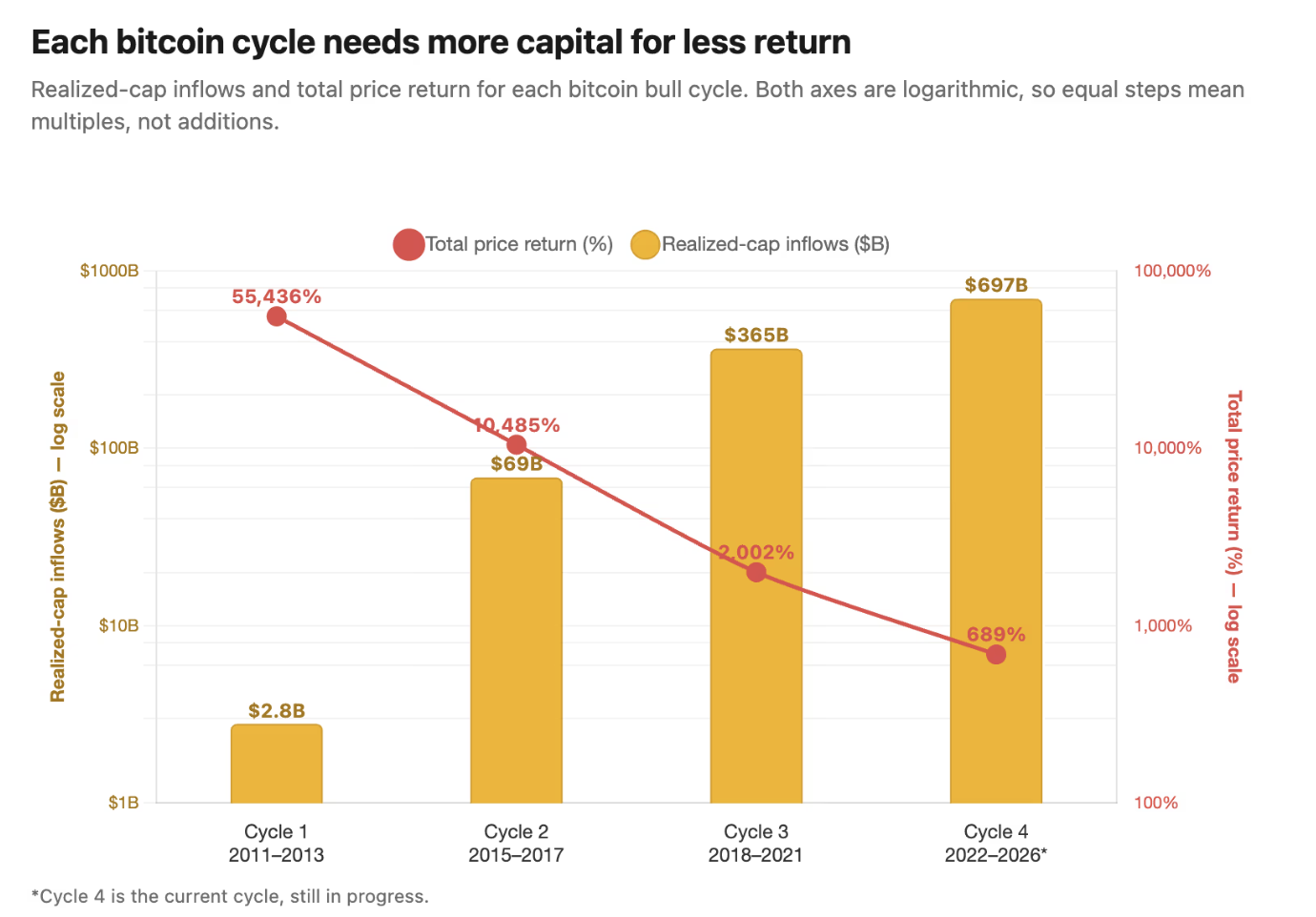

If we extend the time dimension further, the challenges facing Bitcoin's bull market become even more apparent. CryptoQuant founder Ki Young Ju believes that for Bitcoin to initiate the next parabolic bull market, it needs to truly grow into a globally core macro asset, rather than primarily relying on retail sentiment and ETF fund drives. He estimates that the next bull market may need to attract over $1 trillion in new funds, significantly higher than the current scale of institutional fund allocation. Historical data shows that the capital efficiency of Bitcoin bull markets is continually declining. The net inflow of about $2.8 billion during the 2011 cycle propelled prices up by approximately 550 times; about $69 billion brought nearly 100 times gains in 2015; approximately $365 billion drove around 20 times gains in 2018; while this round since 2022, approximately $697 billion in new funds has corresponded to only about a 689% increase. This means that as Bitcoin's market capitalization continues to expand, future needs for larger incremental funds to drive prices for similar magnitude increases will arise. However, this long-term logic still faces real challenges. Recently, the US spot Bitcoin ETF has experienced consecutive net outflows, retail funds continue to withdraw, while institutional funds have not formed a sufficient increment to flow in, leaving the market still some distance from the next round of comprehensive bull market.

Meanwhile, the altcoin market still shows no significant improvement. CryptoQuant analyst IT Tech indicates that the altcoin market, excluding Bitcoin and Ethereum, continues to face pressure. Data shows that the cumulative trading volume difference of altcoins in June has reached near five-year extreme lows and is still further declining, reflecting that the spot market continues to be dominated by net selling. Since the peak in early 2025, selling pressure has not shown significant relief, and the market has yet to show clear signs of stabilization.

Despite the short-term market still facing pressure, several seasoned investors believe that Bitcoin's price is gradually nearing the bottom range of previous cycles. For instance, early investor Bruno Ver anticipates that Bitcoin may still fall to around $50,000; CryptoQuant estimates Bitcoin's realized price to be around $53,400, which has historically served as an important reference for bear market bottoms; while multiple on-chain models from Glassnode place the potential bottom range between $37,000 and $60,000.

Overall, July has brought a much-awaited breathing opportunity for the crypto market, but a real trend reversal will still require more confirmation signals.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。