Written by: Rita

Guide to Trends

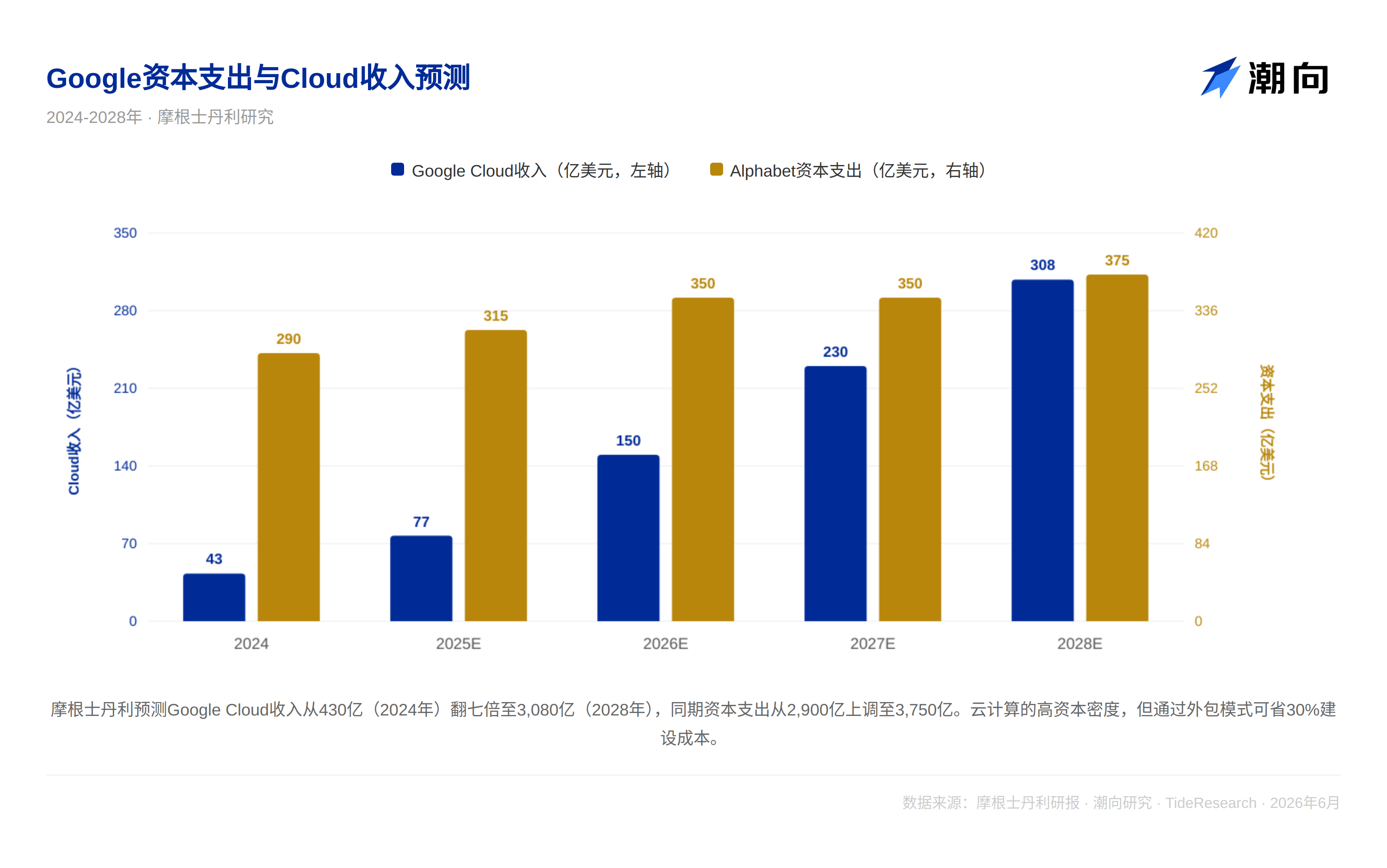

Morgan Stanley raised Alphabet's target price from $375 to $415. The real driving force is TPU, not search or YouTube. Through deducing data from chip shipments, it is expected that Google Cloud's revenue will increase sevenfold to $308 billion by 2028, while EBIT's share of the entire company skyrockets from 2% to 46%. This indicates a fundamental transformation of the business model: from an advertising company to an AI computing power operator.

Google Cloud's annual growth is equivalent to three AWS

Morgan Stanley on June 29 raised Alphabet's target price from $375 to $415, maintaining an "overweight" rating. The real drive comes from TPU, not from search, YouTube, or Gemini. The report used a bottom-up computational framework. By reversing the chip shipment data from Broadcom and MediaTek, it deduced the pace of Google's computational expansion, calculating figures that Google itself has not disclosed. Morgan Stanley's semiconductor team, starting from Broadcom's public guidance of 10 GW for 2027, combined with $12/W ASIC revenue calculations, established a framework estimating total shipments of 14 GW in 2028, with about 60% of TPU share attributed to Google.

Specifically, Google will add about 9 GW of local computing capacity by 2028. Of this, 7 GW will come from self-developed TPU (Broadcom supplying about 5 GW for internal use, 4 GW for external sales; MediaTek contributing about 1.5 GW), with another 2 GW coming from Nvidia GPUs.

This deduction is based on actual shipment data and pricing from chip manufacturers, not conceptual speculation.

Structural changes in revenue breakdown

The most critical change lies in the monetization logic. Morgan Stanley breaks Google Cloud into two revenue lines.

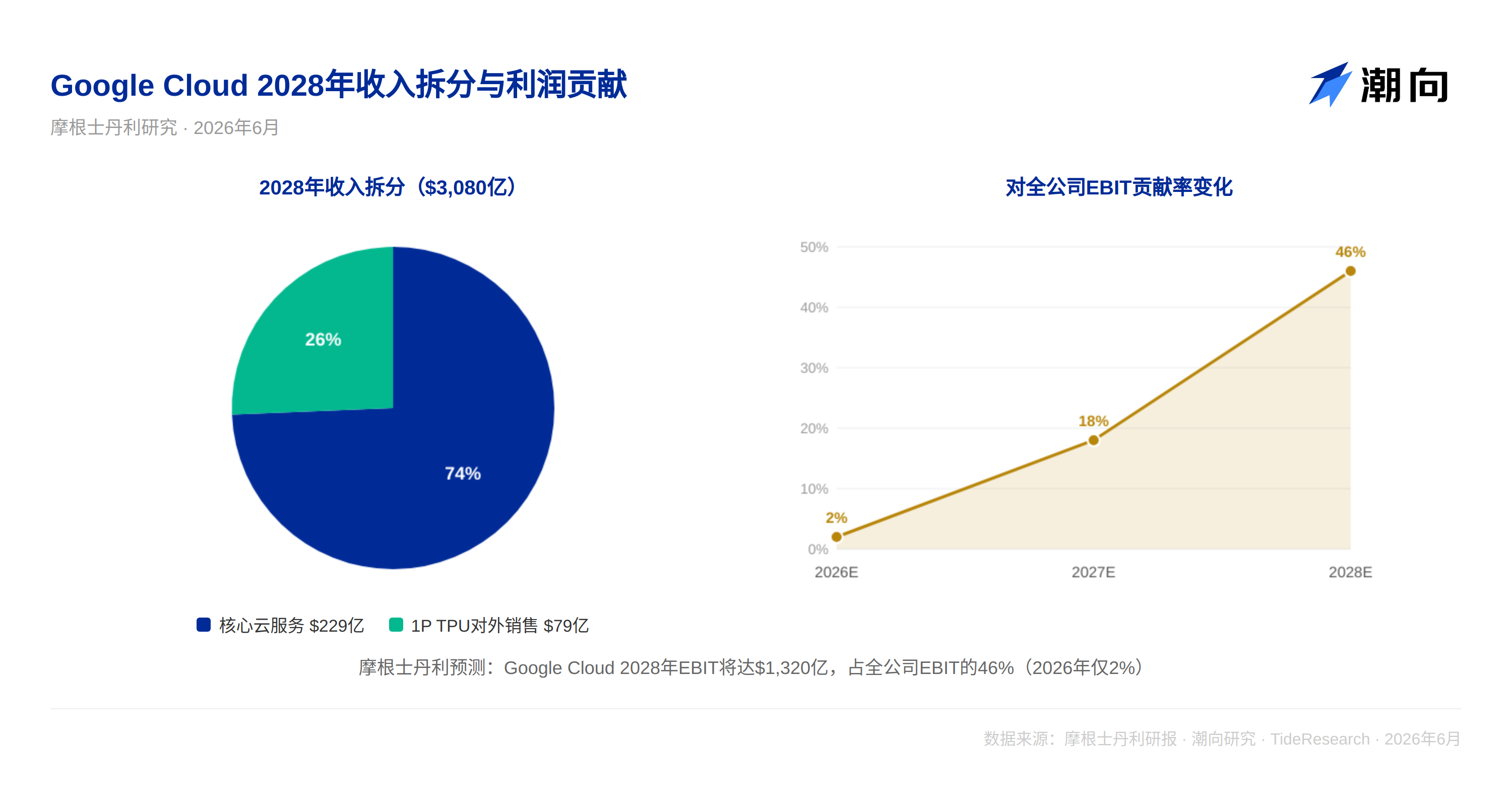

The first line is core cloud services, monetizing at $18 per watt, expected to contribute $229 billion by 2028. This is the traditional way of generating income in cloud computing.

The second line is first-party TPU external sales. Google plans to sell 4 GW of TPU computing capacity externally, estimated to generate $79 billion in incremental revenue at $200 million per GW. Morgan Stanley estimates that the gross margin for the first-party TPU system is only 20%, much lower than that of core cloud services. Google’s strategic intent is to build ecological moats by integrating more AI data centers with TPU architecture, rather than focusing on this business for gross profit.

Combined, Google Cloud's revenue will reach $308 billion by 2028. This is seven times the $43 billion expected in 2024.

Reorganization of profit structure

Morgan Stanley forecasts that Google Cloud's EBIT will reach $132 billion by 2028, accounting for 46% of the entire company's EBIT.

Two years ago, this ratio was only 2%. Google’s profit engine is switching from the advertising business to cloud computing and AI infrastructure. The valuation framework also needs to change; the current multiple of 18 times 2028 EPS appears conservative.

Capital expenditures and cost optimization

However, the cost is significant, with capital expenditures raised from $300 billion in 2027 to $350 billion, and further to $375 billion in 2028.

Google is addressing this burden in new ways. First, by outsourcing data center power supply facilities and infrastructure to partners like Blackstone, saving about 30% of the construction costs for GW-level data centers. Second, MediaTek's TPU manufacturing costs are significantly lower than those of Broadcom. As MediaTek's share in Google's TPU orders increases, the unit cost of computing power continues to decline.

Trends Perspective

The biggest assumption in this report is the realization of revenue from external TPU sales. The report assumes that Google sells TPU systems externally at a 20% gross margin, generating $20 billion in revenue per GW. However, there are two issues to point out:

First, the report admits that "it cannot fully determine Google's gross margin pricing for the first-party TPU system." If Google aggressively lowers prices to establish the ecosystem, the $79 billion prediction for 1P TPU revenue in 2028 has significant downward revision risks. If this revenue falls short of expectations, the overall revenue target for Google Cloud will drop.

Second, Morgan Stanley has extensive investment banking relationships with Alphabet. It has provided investment banking services and received fees over the past 12 months and holds more than 1% of common stock in Alphabet. Individual analysts also own Alphabet stock. This does not affect the framework value and data depth of the report, but readers should independently assess whether the assumptions regarding the expansion of the TPU ecosystem in this report are overly optimistic.

The current Alphabet stock price is $353, corresponding to Morgan Stanley's 18 times 2028 EPS forecast, lower than the past long-term average of 21 times. However, this cheap valuation depends on two assumptions: that Google Cloud's revenue climbs as expected to $308 billion, and that the gross margin for the external sales of the TPU ecosystem can be maintained above 20%. If any part of this equation deviates, the price needs to be reevaluated.

Disclaimer

Fixed statement on research report content (brokerage views, not trend research views)

This article is a compilation and interpretation of third-party brokerage research reports by Trend Research. The ratings, target prices, profit forecasts, and relevant judgments quoted in the text are the views of those brokerage analysts, representing the positions of their respective institutions, and do not reflect the views of Trend Research, nor do they constitute any investment advice.

The market carries risks, and decisions should be made independently. This article should not serve as the basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。