Author: Wall Street Journal

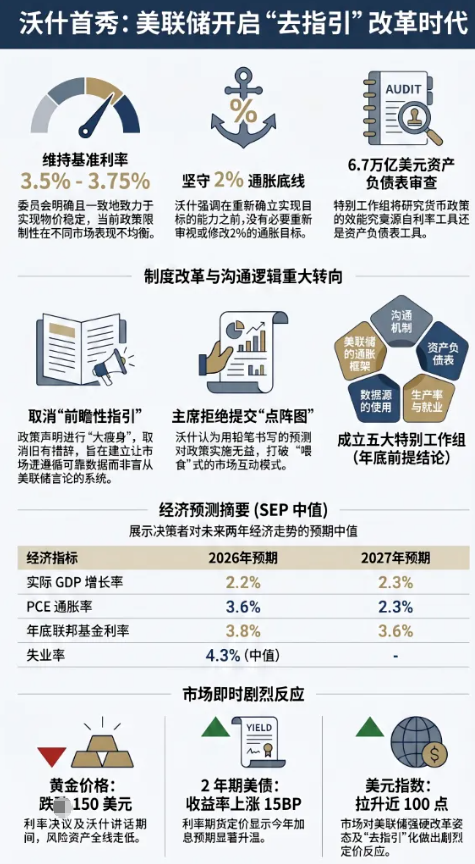

On Wednesday, June 17, Eastern Time, the Federal Reserve announced after the FOMC meeting that it would keep the target range for the federal funds rate unchanged at 3.50% to 3.75%.

On Wednesday, June 17, Eastern Time, the Federal Reserve announced after the FOMC meeting that it would keep the target range for the federal funds rate unchanged at 3.50% to 3.75%.

The post-meeting statement emphasized the commitment to price stability in reducing high inflation, with the dot plot reflecting a strong hawkish tendency among Fed decision-makers.

This was the first FOMC meeting chaired by Walsh. In the press conference, Walsh stated that the committee is clearly and unanimously committed to achieving price stability and a 2% inflation target.

From the interest rate decision, his new official fire was a substantial reduction in the decision text, including the interest rate guidance. At the same time, he is implementing reforms, and this statement abolishes the long-standing “forward guidance,” announcing the immediate establishment of five special task forces (on communication mechanisms, the balance sheet, the use of data sources, productivity and employment, and the Fed’s inflation framework) to propose improvements by the end of the year.

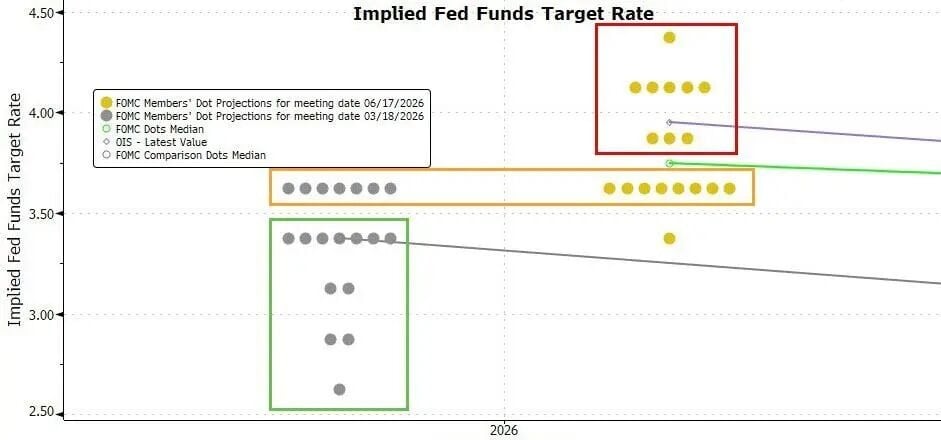

The new statement shows that in the dual mission of employment and inflation, the Fed only emphasizes the inflation aspect, maintaining the previous consistent assessments on inflation and other economic areas, reasserting that inflation remains high, and pointing out that the conflicts in the Middle East introduce significant uncertainty to the economy. Compared to the statement, the subsequently released dot plot reflects a more pronounced hawkish tendency: half of the Fed decision-makers providing interest rate forecasts expect at least one rate hike within this year.

It is worth mentioning that there were supposed to be 19 individuals providing interest rate forecasts at this FOMC meeting, but the dot plot shows that only 18 provided forecasts, and as Fed Chair, Walsh broke with the norm by explicitly refusing to submit his economic projections summary (SEP) and dot plot.

He explained this by saying, “I reviewed the dot plot, and when I saw what was submitted, I noticed that all submissions were written in pencil, you know, the kind with big rubber erasers... For me, this does not help in policy implementation.”

Based on Walsh's stance against providing interest rate guidance, it has led to speculation that this may be the Fed’s last time providing the dot plot.

Nick Timiraos, a veteran Fed reporter known as the “new Federal Reserve correspondent,” commented that this is a “very hawkish” dot plot. He stated in the title that the Fed is keeping interest rates unchanged, but more officials expect that the next step will be a rate hike.

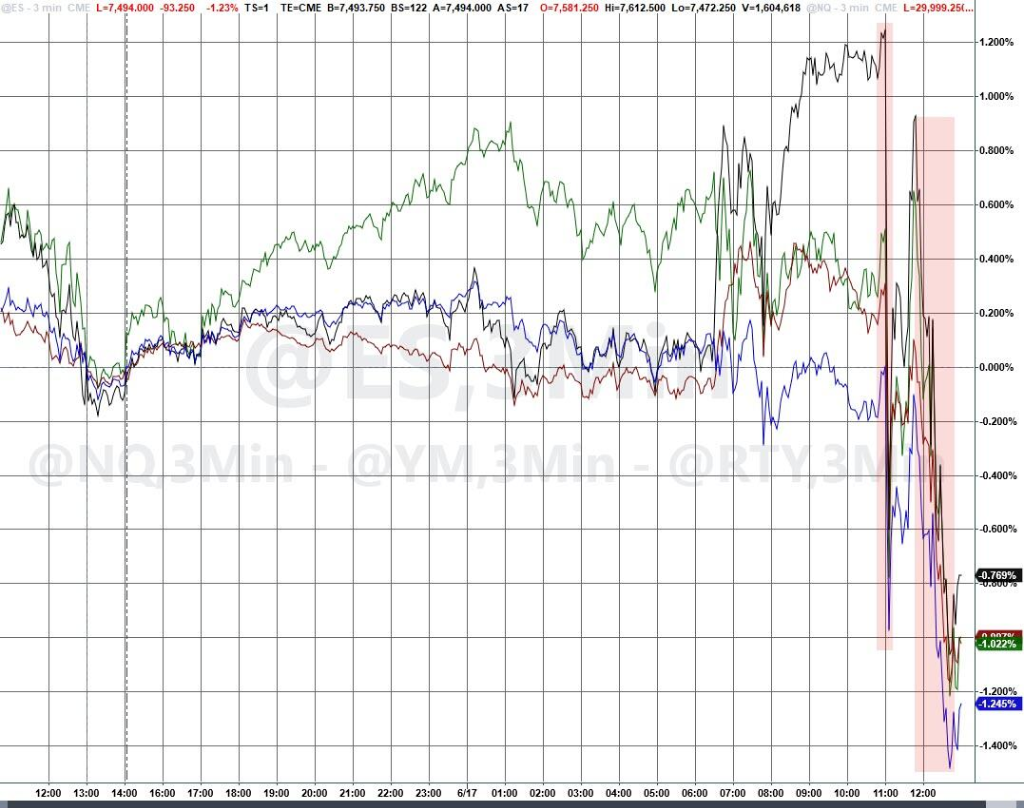

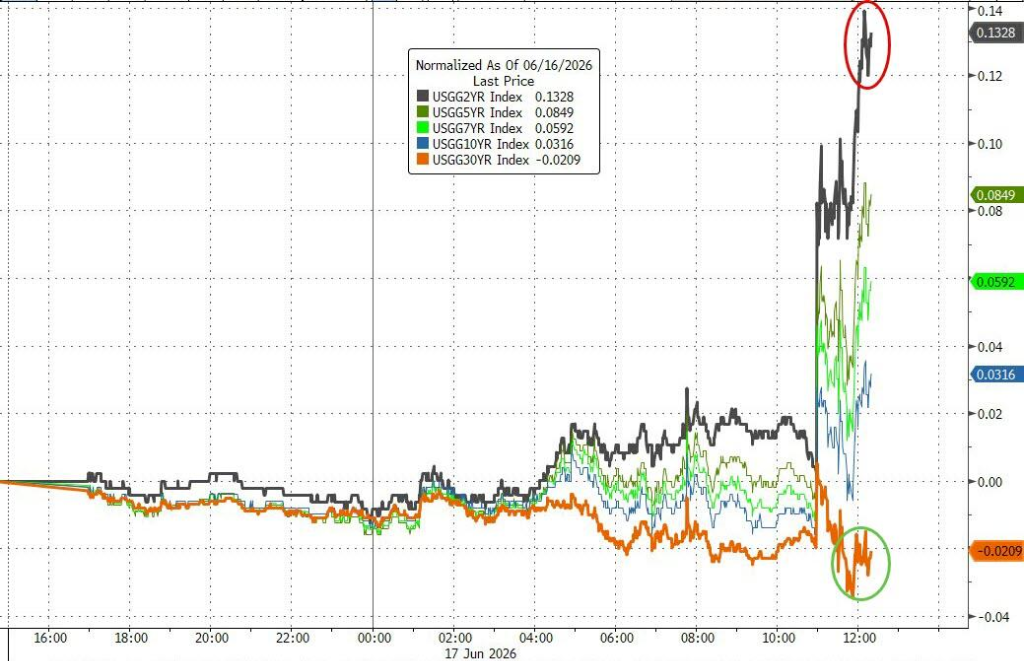

The strong hawkish tendency caught the market off guard. All three major U.S. stock indices closed down on Wednesday: the S&P 500 index fell about 1.2%, the Nasdaq dropped about 1.3%, and the Dow Jones dipped about 1%. The VIX fear index rose above 18 again.  The yield on the 2-year U.S. Treasury, sensitive to interest rates, rose by 16 basis points, while the 10-year saw an increase of over 8 basis points. The U.S. dollar index surged by 0.86%, reaching a two-month high.

The yield on the 2-year U.S. Treasury, sensitive to interest rates, rose by 16 basis points, while the 10-year saw an increase of over 8 basis points. The U.S. dollar index surged by 0.86%, reaching a two-month high.  Spot gold prices fell more than 2.5%, erasing all gains accumulated this week due to expectations for peace talks.

Spot gold prices fell more than 2.5%, erasing all gains accumulated this week due to expectations for peace talks.

Half of the decision-makers expect a rate hike this year; Chair rejects the dot plot unprecedentedly

The median value of interest rate forecasts from Fed officials published after this Wednesday's meeting shows that Fed officials have raised their rate expectations for the next two to three years: the federal funds rate is expected to be 3.8% by the end of 2026, up from 3.4% previously, 3.6% by the end of 2027, and 3.4% by the end of 2028, with March expectations at 3.1%, and the longer-term federal funds rate remains unchanged at 3.1%.  Different from the dot plot released in March, this time’s dot plot clearly does not hint at any easing bias. Among the 18 Fed officials providing interest rate predictions, nine expect at least one 25 basis points hike before the end of this year. In other words, half of the Fed officials predicting expect at least one rate hike this year. In contrast, the previous median interest rate forecast indicated that the Fed overall expected one rate cut this year. Meanwhile, the camp supporting rate cuts this year has significantly shrunk, with only one individual predicting that there would be rate cuts this year.

Different from the dot plot released in March, this time’s dot plot clearly does not hint at any easing bias. Among the 18 Fed officials providing interest rate predictions, nine expect at least one 25 basis points hike before the end of this year. In other words, half of the Fed officials predicting expect at least one rate hike this year. In contrast, the previous median interest rate forecast indicated that the Fed overall expected one rate cut this year. Meanwhile, the camp supporting rate cuts this year has significantly shrunk, with only one individual predicting that there would be rate cuts this year.

The interest rate resolution receives unanimous support for the first time in nine months, deleting interest rate guidance

Compared to previous meetings, the resolution statement released after this meeting was completely rewritten.

In terms of length, compared to the previous resolution statement at the end of April, the full text of this statement has been reduced by nearly two-thirds. At the same time, the narrative structure of the statement has changed, deleting the previously reiterated so-called interest rate guidance, no longer stating that the FOMC will evaluate the stance of monetary policy based on the impact of future data on the economic outlook, and removing the following sentence:

“If there are risks that might impede the (FOMC) committee from achieving its goals, the committee is prepared to adjust its monetary policy stance when appropriate.”

The first paragraph of the statement no longer introduces recent employment, inflation, and other economic conditions but straightforwardly announces that all twelve FOMC committee members voted in favor of the decision to maintain interest rates unchanged. This is the first time in almost nine months that the Fed’s interest rate resolution has received unanimous support from the FOMC voting members, partly due to the exit of the most dovish Fed Governor Miran (Stephen Miran) in May.

No longer reiterating close attention to risks in both employment and inflation

The second paragraph of this statement reads, in support of the Fed's dual mission of full employment and price stability, the FOMC has decided to keep the policy rate unchanged.

In terms of dual missions, this statement no longer reiterates that the FOMC is committed to achieving full employment and a 2% inflation target in the long term, nor does it reaffirm that the FOMC is closely monitoring risks in both employment and inflation, but instead adds a sentence at the end of the introduction of economic conditions, stating that “the (FOMC) committee will be committed to achieving price stability,” thereby emphasizing the mission regarding inflation.

Although the length has significantly reduced, compared to the last resolution statement, the evaluation of the economy remains largely unchanged, maintaining references to the impact of the Middle East conflict, reiterating that inflation remains high, and stating that unemployment rate changes are minimal.

Lowering GDP growth expectations for this year, raising inflation expectations

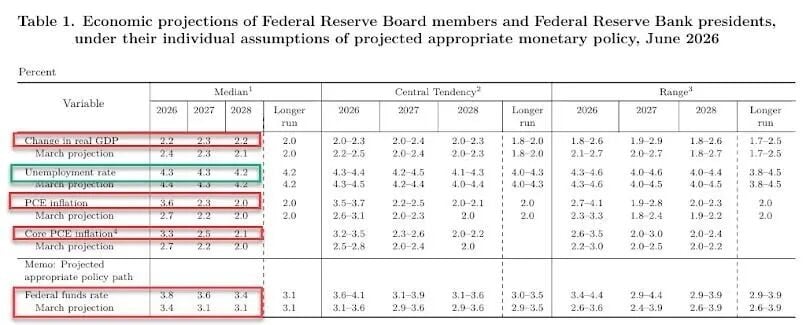

The economic outlook released after the meeting shows that Fed officials expect economic growth to further slow this year, with a slight improvement in the unemployment situation, but inflation is clearly rising.

Fed officials have lowered their GDP growth expectations for this year and the following year, with a downward revision of this year's unemployment rate expectations.  Compared to the inflation outlook released in March, this time the expectations for PCE inflation and core PCE inflation for this year and the next have been raised, with the difference being that this time the expectations for core PCE inflation for the following year have also been increased.

Compared to the inflation outlook released in March, this time the expectations for PCE inflation and core PCE inflation for this year and the next have been raised, with the difference being that this time the expectations for core PCE inflation for the following year have also been increased.

This year's PCE inflation expectation has increased the most, rising by 90 basis points to 3.6%, with this year's core PCE inflation expectation at 3.3%.

Here is the complete translation of Walsh's first press Q&A:

Walsh

Good afternoon. It is an honor, truly an honor, to return to the Federal Reserve and take on this role at such a pivotal moment. I am especially encouraged by the warm welcomes from old friends and new colleagues. I have also seriously listened to the opinions of my FOMC colleagues and absorbed many new ideas, new thoughts, and the sincere will to push the Fed forward.

Walsh

This week’s FOMC meeting fully embodies the Fed’s best traditions: rigorous debate, an open mindset, commitment to mission, and a sense of responsibility and accountability for performance. In this field, all these ultimately boil down to one point: setting the right monetary policy or getting as close as possible to it—that is our North Star.

Walsh

My colleagues and I are here to fulfill our statutory responsibilities, as you have previously heard us say: price stability and maximum employment. These goals guided our work in the meeting that has just concluded.

Walsh

As you saw a few minutes ago, the committee decided to keep the target range for the federal funds rate at 3.5% to 3.75%. To support the Fed's dual mission, the committee also reaffirmed the policy of maintaining ample reserves in the banking system. Despite heightened uncertainty due to factors such as conflicts in the Middle East, economic activity continues to expand at a robust pace. Productivity growth and capital investment are both strong, job growth is keeping pace with labor growth, and the unemployment rate is relatively stable. We recognize that the inflation rate has been well above the Fed's long-stated 2% inflation target. This has been the case for more than five years. Persistently high prices are a burden for the American people, but past experiences may not necessarily repeat.

Walsh

I am pleased to report that FOMC members are clear and unanimous that this committee will achieve price stability. In any organization, leadership transitions are a natural and timely opportunity to reaffirm its mission, review current practices, and consider whether those practices best align with our goals. My Fed colleagues and I will work closely together to explore what changes might help improve the implementation of monetary policy.

Walsh

On this point, you may have noticed a difference in today’s policy statement. It is shorter, more concise, and omits some old phrases. This statement simply aims to present facts to you as accurately as possible based on our judgments. The so-called “forward guidance” is no longer included, as we unanimously believe it is not appropriate for the current policy mix.

Walsh

This afternoon, you will also receive the routine economic projections summary (SEP). The committee's longstanding practice allows participants to submit these projections, and I encourage my colleagues to continue doing so. However, I personally did not provide any projections, consistent with my views on the SEP (at least in its current structure). The median projection for this year’s real GDP growth is 2.2% and 2.3% for next year; the overall PCE inflation rate for this year is 3.6%, and for next year, it is 2.3%; the unemployment rate is approximately 4.3%. The median forecast for the federal funds rate by participants is expected to be 3.8% by the end of this year and 3.6% by the end of next year.

Walsh

Now, please allow me to say a few words about a key initiative we announced today. I will appoint a special task force for each of five areas that are crucial for the broad implementation of monetary policy. First, communication of the Federal Reserve; second, the Fed's balance sheet; third, our use and reliance on existing data sources; fourth, productivity and employment during the transformation period; lastly, the Fed’s inflation framework.

Walsh

These topics are timely and important, and in my opinion, deserving of a re-examination. My colleagues and I have engaged in lively and purposeful discussions about them over the past few days. For each independent task force, I am recruiting some of the best talent, including individuals from both academia and other fields. They will be supported by subject matter experts from our excellent Fed staff and will have a clear assignment.

Walsh

Starting from first principles, pose sharp questions, examine current practices, consider alternatives, and ultimately propose further actions for policymakers. Since last summer, my colleagues have discussed possible ways to improve the format and function of Fed communication. This new task force will continue that work, and I expect it to propose some well-considered recommendations, including suggestions regarding the SEP I just mentioned. The second task force, the one on balance sheet policy, will review the current ample reserves system and assess the benefits and risks of the Fed's balance sheet composition. They will evaluate alternative frameworks for implementing and conducting monetary policy.

Walsh

The third task force, the data working group, will assess new information sources and consider methodological changes for improving data collection, aiming to provide policymakers with more accurate, relevant, timely, and perhaps most importantly, actionable information about our economic conditions.

Walsh

The fourth, the productivity and employment working group, will examine the pace, scope, and economic impacts of new general technologies, including artificial intelligence, and explore their potential impacts on the Fed's pursuit of its employment and inflation missions.

Walsh

The last task force, the inflation framework working group, will study the driving factors of inflation. Fundamentally, it will explore various concepts for achieving price stability in a changing economy. In the coming weeks, you will hear more information about these task forces and this overall initiative. For now, I can make a simple statement: each task force will serve everyone in the system, serving the goals shared with everyone who sat around the table with me in the past few days—a Federal Reserve that has a clear understanding of its mission, aligned with its goals, and looking to the future. Thank you all for your attention, and I am happy to answer your questions.

Speaker 2

Hello, Chair Walsh. It’s great to see you again, welcome back. You’re launching so many initiatives so quickly; what is the timeline for each of the task forces you envision?

Walsh

I think it depends on the individual task forces. It also depends on the extent to which we urgently need clear answers. My expectation—I am still in the process of recruiting and finalizing members—is that the task forces will begin their work in the coming weeks.

We expect to start receiving more information from them by the end of summer to understand how they frame the issues. Hopefully, most (if not all) will reach conclusions by the end of the year.

Speaker 2

Specifically regarding the inflation framework, you mentioned first principles. Does this include a review of the 2% target itself? You’ve mentioned that the numbers to the right of the decimal point are not as important. Does this mean you believe that starting from “2% as a point target is too strict” is a premise you may consider?

Walsh

Let me break it into two parts. First, regarding the inflation framework review, its role is: what are the driving factors of inflation? To what extent does the Fed bear responsibility for inflation? How do we measure inflation? But that may overlap with my data working group.

Regarding the 2% inflation target, that is the Fed's long-held 2% target. You have heard me say before that I tend to focus on the numbers to the left of the decimal point. Well, 2 is now the number to the left of the decimal point, and zero is to its right. I believe that until we reaffirm our commitment and ability to achieve the 2% inflation target, there is no need to revisit it. So that is not within the scope of our current work.

Speaker 3

Kobe, thank you very much. I am Kobe Smith from The New York Times. You’ve previously stated that inflation is a choice. In the policy statement, it included the commitment to achieving price stability that you reiterated today. But looking at the SEP, most of your colleagues expect core PCE to be around 3.3% by the end of this year, while the 2% target is not expected to be reached until 2028.

So I really want to know how much patience the Fed can have in waiting for a one-off surge in inflation to pass while waiting for inflation to cool after several years of high inflation? Under what circumstances would you support the Fed taking action and raising rates?

Walsh

Okay, there are a lot of questions here. Let me try to break it down. First, we have the capacity and commitment to achieve the 2% price stability target. That is exactly what we are to do. In the Fed’s review of its strategy over the past several years (including in January)—a strategy we are still bound by—the Fed's statement indicated that inflation is primarily determined by monetary policy. Indeed, that is the case.

I have long said that inflation is a choice. It certainly is.

Today, I announce that this committee is clear and unanimous in deciding that we will achieve this goal. The rest of your question sounds like you are encouraging me to give forward guidance. We have abandoned forward guidance. Some members of the committee, I suspect, have abandoned it, as I feel that offering forward guidance at the current moment is inappropriate based on our discussions in the past few days.

Others have different views, believing that as a general proposition, forward guidance is not the business we should be in. But that will be handled by the communication task force and my policy-making colleagues.

We will seriously listen to expert opinions and then make our own decisions. But I cannot provide any forward guidance about our next actions. The good news is, we will have another meeting in six weeks.

Speaker 3

So, I want to follow up on current policy setting. Given the data flows we have observed and forecasted, how restrictive do you think current policy is?

Walsh

I have heard various descriptions from both inside and outside the Fed. Let me share my view: it is uneven. If I look at the real estate market as an example, the Fed's policy is not the only factor determining the state of the real estate market. But overall, I do think that there seems to be a certain level of restriction in Fed policy in that area. If I were to describe what is happening in financial markets, it would be hard to apply the term “restrictive” in any other context.

So I would say it is uneven. This may reflect the different transmission mechanisms of monetary policy, whether coming from our interest rate tools or balance sheet tools. The good news is, we also have a working group on this matter, the balance sheet task force will delve deeper into it.

Speaker 4

You said you don’t like forward guidance; it was removed from the statement this time. However, the dot plot shows that nine members indicate they want to raise rates before the end of this year, which the market interprets as forward guidance. So what does this mean for how you guide the market and for the future of the dot plot?

Walsh

I have to give you the same answer I gave Ms. Smith. We have a task force addressing this issue. I will say a bit more. I reviewed the dot plot, and when I saw the submissions, I noticed that all submissions were written in pencil, you know, the kind with big erasers.

This means that I think colleagues present here understand that the world changes quickly, and they don’t feel bound by what might happen six weeks or six days from now. In case the situation changes... I would also like to point out a few other points. What I have heard from them is that when they submit model predictions—just to clarify, this does not mean that this is more likely than other possibilities, it simply means this is more probable than other scenarios.

So I haven’t heard great confidence. What I've heard is a humility that I believe we should have. I did not submit a dot. For me, this does not help with policy implementation. I suspect, as I mentioned in my opening remarks, that by the end of the year, all aspects of communication—news conferences, dot plots, meetings, transcripts, minutes—will be reviewed. This will be part of it.

I don’t want to predict outcomes, but I am quite open to potential results. In the past few days, frankly, in the past three weeks, my colleagues have shown an openness to changes and risk-laden easy changes which has impressed me greatly.

But our foremost goal is to set monetary policy correctly. The way to set monetary policy correctly is to fulfill the responsibilities assigned to us by Congress to achieve price stability, on which there is no divergence.

Speaker 4

You might get the same answer about the task force... Regarding communication, what are your thoughts on these news conferences? Do you think you will continue holding them after every meeting? Do you find them useful? What is the future of Kevin Walsh's communication style?

Walsh

Well, we might have 15 to 20 minutes left, so I don’t want to predict outcomes. News conferences can be a very useful way to communicate with households, businesses, and broadly through media outlets like yours. I had a great late mentor, George Shultz, whose motto was that news conferences are useful, but when you hold one, make sure you have something important to say.

Today, I think we have something important to say: our commitment to achieving price stability, our commitment to rethinking practices to advance the Fed. To ensure you and the American people feel these are not fantasies, but tangible ideas, we will seek out the best talent—whether it is the best minds within the Fed or those I know in business, economics, academia, technology, and more—to share their perspectives.

This is what we will do here, pursue the truth. I believe we will present some new and interesting ideas. We made some changes today. I expect there will be more changes, some of which might warrant a news conference.

Speaker 5

Hello, I am Chris Rugaber from the Associated Press. Thank you for answering our questions. Could you talk about your long-term views on inflation? I know you might not comment on short-term fluctuations, but is it primarily driven by energy prices and the war in Iran? Or do you have any concerns about potential inflation pressures in the economy? Thank you.

Walsh

I cannot put it better than what the committee just did, so let me reiterate. Inflation remains elevated relative to the committee's 2% target, partly reflecting supply shocks that have driven up prices in certain sectors, including energy. The next part makes it clear, however, that the Fed is committed to achieving price stability. My own judgment is that the committee has spent considerable time discussing this issue, not just over these two days but for several weeks.

This is what we are prepared to say about inflation. But our commitment to achieving that goal is firm, consistent, and clear. I think this has been an important message that we have missed over the past five years, and we will correct that.

Speaker 5

Okay. Additionally, about your data working group and other aspects, I mean, generally, it seems people feel the Fed has considered all data. Certainly, that's the feeling prior. Is there any data you feel has not been given enough attention?

I mean, you've previously mentioned the trend of “mean reversion,” but similarly, this is well known to most Fed members. So what is this working group looking at? What are the potential outcomes? I know you don’t want to predict outcomes, but are there examples of data you expect to see receive more focus? Thank you.

Walsh

So, you're asking me my question. Let me say, I don’t want to predict outcomes. I also don’t want to elaborate too much on what they will do, because I still need to make a couple of calls before I finalize the leadership. I am very interested in external experts' views on this matter.

I would say this: generally, a lot of the data consumed by U.S. central bankers and other government officials comes from old-fashioned survey methods, based on national accounts... The portrayal of the U.S. economy seems quite different from the U.S. economy in 2026. The response rates of the survey methods do not meet our needs, and the questions asked may have been very relevant a generation ago, but may not be applicable now.

Thus, even within the official statistics, if the task force and our best thought propose suggestions on how to use new analytical methods to elevate these official statistics to meet our contemporary standards, I would remain open-minded. Additionally, almost every CEO running their private business is using real-time information that does not go through extensive revisions and can tell them what just happened at that moment.

As you know, implementing monetary policy has a normal, long, and changing lag. What we genuinely care about is what is happening now. We are less interested in historical echoes. You can hear from my responses that some data we receive, like the monthly payroll index we await every first Friday of the month or other statistics, might be mere historical echoes, though still quite useful by the time of its third revision.

We need to reduce those error margins because we must make tough decisions in real-time. I am very confident that we can learn a lot from the private sector, reforms from the official sector, and new analytical techniques that are far more refined than simply asking whether something is core or non-core.

Speaker 6

Thank you. Welcome, Chair. I am from Fox Business Channel. So, if you're not providing a lot of continuous forward guidance, will the market experience more volatility? Shouldn't Americans know more about your future thoughts?

Walsh

I believe financial markets perform best when reacting to incoming data. I think when financial markets are asking, “How will the Fed respond to incoming information?” they are less efficient. The more markets are focused on what is happening in the real economy, judging what is good data and what is bad data, the better financial markets can price in the most likely occurrences and tail risks.

Market prices might be the most important information source guiding central bankers. However, when what the markets do simply reflects what we are saying, then we are taking away the most important source of information and turning a blind eye to it. I want us to establish a system that removes those blindfolds and allows the markets to follow the data they find reliable; they will focus on the data, and we will too.

They will deliver better information through market prices, enabling us to make more informed decisions. But ultimately, the target I set at the beginning—to achieve the price stability goal that Congress has mandated us—is our imperative.

Speaker 6

If I could bring you back to the meeting for a moment. This is your first meeting. The board members seem quite hawkish. When you listen to their remarks overall, was there any discussion of future rate cuts?

Walsh

Today? There was only one proposal on the table. There was no discussion of any other proposals. Regarding that proposal, I would say the discussion was quite limited. Everyone was clear and unanimous on this. The practice of this central bank and other central banks is to have a range of alternatives.

Today, we only had one. I believe further discussions deepened understanding and clarified what we need to do and how to accomplish it. I don’t want to predict what will happen in the future, but for us, there was only one important issue. We accepted it. We engaged in a solid internal debate over a few days about it, and in the end, I think we are in a better position.

Speaker 7

Thank you very much, I am Claire Jones from the Financial Times. You know, as we read this very brief, and I think all of us appreciate, statement, one might wonder, given what you've said here about the risks of U.S. inflation and your responsibilities, why are you not raising rates today?

I want to ask, why not? What do you need to see to take action to raise rates? Secondly, regarding your task forces, will you consider borrowing any best practices from other central banks? Thank you.

Walsh

I’m glad they are accustomed to you asking two questions because my answer to your first question will be very brief: I have nothing to say other than the statement itself.

Regarding the responses I received earlier, the market's reactions to our unfiltered comments, I think are more helpful than going off-script after the statement is released. As for best practices regarding task forces, those are topics I have thought about. I’ve also been involved in one or two task forces in my lifetime.

Best practices are: find the smartest people; ensure the task forces have personnel with diverse backgrounds and leanings so they can engage in some internal debate; ensure that when you establish task forces, the teams that are receiving the information feel they have a stake in it.

This is why we are looking for—yet to finalize a list—some of the most important talents in our building and across the Reserve Banks, with individuals from every field, and in some sense, seconding them to this small group for a few months. This way the task force leaders can understand how the world’s most analytical central banks view this and can reflect that in the final best practices.

We are not outsourcing decision-making to anyone.

The management and past Reserve Bank have selected the 19 individuals at the table. These will be our decisions. We can agree on some suggestions, disagree on others, and engage in good internal debates on these. But their outputs, I hope and believe, will make our internal discussions better, stronger, and more dialectical, so we can ultimately achieve our price stability goal.

Speaker 7

Quickly following up on your mention of market perspective. If you look at the two-year Treasury yields, they actually indicate that the market believes more tightening is needed. Is this also your interpretation of the message conveyed by the two-year yield?

Walsh

Hmm? We were in a very good state. I suppose that is why we don’t answer the third question. I don’t intend to comment on the market reactions over the past 30 or 60 minutes. What we’re providing to the market is a new chapter for the central bank, some new thinking. What we are giving to the market, households, and businesses is, I believe, a commitment to challenge ourselves so that we can deliver on the promises we made in the past.

That’s a lot for financial markets to digest. I am not particularly interested in their initial few minutes or even days of reactions. I think it's most important that financial markets—and at least equally important that households and businesses—know that this central bank will achieve price stability.

Speaker 8

Hello, Chair Walsh. I am Brian Chung from NBC News. Thank you for answering our questions. So when you say we have given up forward guidance, to the average person, it might sound like the Fed will say less, or provide less insight into the direction of its borrowing costs.

So for those whom you might encounter in the grocery store, where price tags are rising faster than their wages, how would you explain this? I don’t know, maybe the “task forces” are the answer. But how will you communicate this era, this chapter of the Fed?

Walsh

If I told someone in front of a milk shelf that I have a task force to handle this, I think that would be very poorly done. So I appreciate your question. If I met someone in the grocery store, I would say: we cannot exert a significant influence on specific prices, like today’s oil prices or even the price of a dozen eggs. This does not have a primary effect on what we do.

But we have a very important task to ensure that these changes in oil, beef, eggs, or milk do not spill over into the economy, do not generate second and third-round effects. That is our job, our commitment, our capability, and we will achieve it.

Speaker 8

Is the relationship between the Fed and the Treasury also under review? There is typically a breakfast meeting with the Treasury Secretary. Do you plan to continue this? Since you were sworn in, have you had any conversations with the President?

Walsh

Regarding the President, I have nothing to tell you. About the Treasury Secretary, he’s been releasing pictures of breakfasts. So I can’t deny the long tradition of weekly meetings between the central bank chair and the Treasury Secretary. I think we have had three so far.

I believe he is overseas this week, so it would be an exception this week. I think those discussions are very useful. The goals of the central bank, as well as our roles and responsibilities, have quite clear distinctions from the fiscal authorities. In my view, monetary policy is independent of what we do.

But that doesn’t mean we are not interested. Whatever happens to fiscal authorities, my way of thinking is this central bank needs to have a broad horizon but focused responsibilities. We need to be quite interested in what is happening in the world. I won’t allude to the fact that we are very interested in what is happening in the Middle East. That certainly has some impact on our daily work.

This doesn’t mean it’s our responsibility, but I think we will maintain a broad perspective. So far, my meetings with Secretary Bessent have helped to broaden this perspective. Hence, we can be aware of things that might impact our daily work even if that’s not our direct responsibility.

Speaker 9

Steve Liesman, CNBC. Mr. Chair, thank you. Thank you for answering my questions. You mentioned before you became Chair that you believed productivity would be one reason to lower rates. Do you still feel this way now?

Walsh

The committee discussed productivity today. AI was mentioned. My view on this, as well as in relation to social interchange, is that artificial intelligence, the latest generation of general technology, could be the most significant change the economy, businesses, and households experience in my adult life. It is filled with tremendous opportunities and risks. I value both. You may have heard me say that AI is shorthand for American creativity.

This does not mean it will be easy. Of course, it doesn’t mean it won’t be disruptive. But in the long run, my belief—which I heard considerable support for today within the committee—is that America is a winner, and as we proceed down this path, America will ultimately get better. Now, returning to policy implementation, the timing, scale, speed, and the impacts on output and employment, this is one of the things we are setting up task forces to address.

Speaker 9

If you don’t mind following up from a different angle, when you see strong job growth, elevated inflation, GDP seemingly performing well, and the stock market soaring, how do you assess this economy? Do you feel the federal funds rate is restrictive?

Walsh

So that’s your second question. I will give the same answer as before. I say when I think of policy implementation, it’s important to focus on the effects of the policy, not what we said, but what is happening. The best way I can describe it is uneven. I do see some restrictions in areas like the real estate market. But it’s hard to apply the same description elsewhere. I’d add this on.

You mentioned one of our dual mandates regarding employment. I don’t think we face brutal choices. I disagree with the view expressed generations ago that the Fed Chair stands at a podium like this and says, you have to choose; you have to decide whether you are willing to tolerate higher inflation to get more people employed.

I don’t believe that. What I believe is that if we do our job well, we can achieve strong growth, low prices, and robust employment in harmony. Therefore, what you hear from the committee today is that we still have work to do on price stability.

Speaker 10

Thank you, I am Nick Timiraos from The Wall Street Journal. Chair Walsh, you’ve said multiple times that credibility is earned through delivery. If credibility needs to be earned through delivery, then action should be tightening or at least threatening to tighten. Now, you did not do that today. Why?

Walsh

The judgment you expressed has not been stated by any of the 19 people seated here. We will meet in six weeks and will discuss this again.

Speaker 10

If I could ask about AI. The infrastructure building is generating substantial demand. Capital expenditures, data centers, electricity, the returns on productivity may be more distant. So in your judgment today, does AI increase demand more or supply?

Walsh

This is a good question for central bankers and economists. We spend much of our time calculating demand. It’s easier; we can see it, we can calculate it, we can check it, we can revise it. But what we need to do is infer supply.

You will notice that in the second paragraph of what your colleague described as a very brief statement, we have one sentence about the demand side and one of equal length about the supply side. Both are important, and just because we can calculate one better doesn't mean we would favor it over the other.

Regarding AI and growth in data centers and related infrastructure, we see the demand side reflected in the GDP data without a doubt. However, when inferring the timing and extent of growth on the supply side, we are less certain. Intuitively, perhaps the supply side will expand but may take longer. I would describe it this way: there is a race between supply and demand.

Milton Friedman said that the only thing we know about economics is that there is a supply curve and a demand curve. They will eventually intersect. What does this mean for policy? The good news is that we have a task force to address this issue.

Speaker 11

Thank you, Mr. Chair. It sounds like regarding the data working group, you are considering a thorough reform of the national accounts system, which is how the government measures the economy. Is that your goal?

Walsh

Answering in one word: no. Answering in a few words: most of the data collection happens at other government agencies, and we have great respect and deference towards them.

But if along the way we propose suggestions—Fed staff have already begun developing such suggestions—about what they can do to help us as policymakers obtain the information, we will not hesitate. Again, I don’t want to define the scope of the data working group’s research. But I do believe there will be a review of the official statistics, and at least as importantly, there will be consideration to introduce best practices from the private sector and new analytical tools brought about by AI.

This way, we can integrate them to provide us with better real-time information. Thus, as I mentioned earlier, when we make decisions, we rely on true contemporaneous data, not what we call contemporaneous data, which is actually historical echoes.

Speaker 11

Okay, thank you. Another question I want to ask relates to the building renovation. Are you considering any changes to the renovation project? Given that they have somewhat become a political football over the past year.

Walsh

I have heard some things about that. I don’t think I am revealing anything, but my view is that when you enter a new institution, you should meet the inspector general; that’s just good practice. I want to continue this practice. I have already met with the inspector general once. He told me what I think everyone knows; he will release a report on the building and the project later this summer. I would be interested in reading that report.

From my perspective, looking ahead, from now until the project is completed, what can we do or should we do to be the best steward of taxpayer funds and ensure we deliver on the promises made. There is still work to be done. You might not be surprised, in my initial weeks, I have been a bit busy with other matters, but I commit to addressing the Fed's responsibilities comprehensively in the coming weeks.

Speaker 12

Victoria Gida, from Politico. I know you did not submit forecasts, but you are the person authorized to speak on behalf of the FOMC. So I want to know if you can tell us if the rise in inflation expectations in the SEP is all due to the war in Iran? What was the discussion regarding the rise in inflation expectations and potential growth slowdown?

Walsh

My interpretation of the meeting discussions is—I must admit, the SEP shows that half of the colleagues believe that given all developments, the policy rate should be at current levels or lower by the end of the year; the other half believes it should be higher. The 19th voter is me, and I did not submit. There are a range of views regarding first and second-round effects, with no consensus or firm opinions reached. But we will meet again in six weeks. I believe we will know more by then, and I think my colleagues will pay close attention to new developments from now until then.

Speaker 13

Could I quickly follow up on the SEP? You said you still encourage your committee colleagues to submit projections even if you do not. So what do you think the benefits are of them doing so (even if you do not)?

Walsh

This is a commitment made by the FOMC, and it is one I hope we will fulfill. Our commitment is to achieve price stability. I expect we will deliver on it by the end of this year. As I mentioned, if there are new communication frameworks, I wouldn’t be surprised. There will be some changes.

Regarding the SEP, that is a committee discussion, an intense discussion. I think we will have that discussion. I believe we will arrive at a better communication mix to fulfill our commitment. But I don’t want to predict what those will be.

But before that, I will continue expecting colleagues to submit their SEPs. Some of them, I believe, feel that the current structural practice is acceptable, but I have heard a lot of interest in truly reforming all these topics. You didn’t ask this, but I’ll answer anyway. The past few days have been very friendly, and the past few weeks have been quite warm. The institution wants to find out how we can do better.

The agency is returning to first principles. What encourages me is the changes we made in the statement, the reforms we are considering regarding the SEP; that instinct to open a new chapter is real. By the end of this year, I hope we can achieve some accomplishments in both form and substance.

Speaker 13

Could you please outline some principles that guide your own reaction function, and tell us some conditions under which you think the Fed should respond?

Walsh

This will be a very unsatisfactory final answer to the question. The Fed has many responsibilities, not just in monetary policy, but also in supervision and regulation, consumer affairs, and payments. My own view is that our credibility comes from delivering on what we say in everything we do. In my initial three weeks, I have spent more time on monetary policy than in all other areas combined.

However, the more we deliver on our commitment as good regulators and supervisors, the more benefits we will receive, and the more our credibility regarding monetary policy will increase. Look, when we achieve our price stability goal—we will—the American people will feel that the difficulties they have experienced over the past five years due to inflation are a thing of the past.

And that credibility will yield dividends in what we do. This institution will come to the press conference filled with the momentum of reform and the drive to do better. But we will achieve some accomplishments.

Speaker 14

How would you summarize the situation of the labor market across different regions?

Walsh

How do you characterize the labor market now? Do you think it is stable, or could it be a source of inflation? Thank you. Okay, yes. If I were to capture the committee's view, the committee believes the labor market is stable. Some members of the committee believe the trend is better than that. Trends are more important than data points. What happens in three or six months is more significant than any single data point or release.

I want to say employment data has been moving in the right direction. If I’ve heard another thing regarding this topic over the past few days, it’s that strong productivity driving growth is not something we fear, but something we embrace. Thank you all very much.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。