Western Securities believes that the ceasefire agreement contains many terms unfavorable to the United States and fails to substantively constrain the Iranian nuclear issue. The fundamental contradictions of geopolitical risks in the Middle East have not been eliminated. A deeper impact is that the foundation of the "petrodollar" system is weakening, the cracks in dollar credit are rapidly expanding, and gold is expected to initiate its fourth major wave.

Written by: Bu Shuqing

Source: Wall Street Insights

Trump announced a U.S.-Iran ceasefire, and global risk assets surged in response, but the unusual signal of rising gold prices simultaneously is hinting to investors that this "TACO market" is different from previous ones, and the hidden cost behind it may be the accelerated expansion of the cracks in dollar credit.

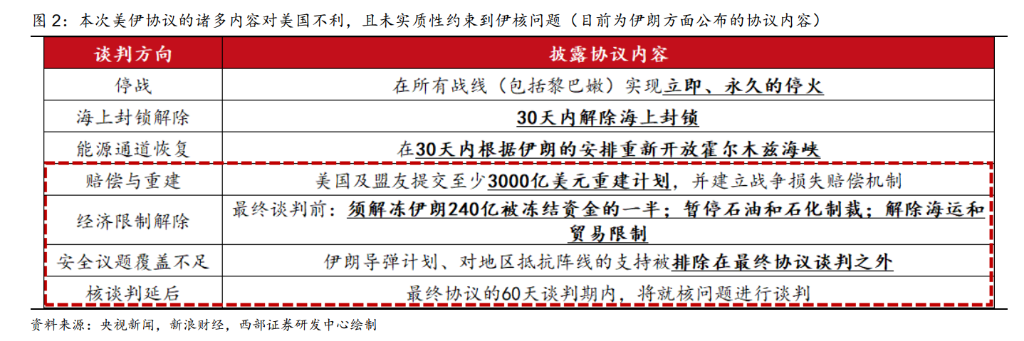

On June 14, Trump announced that the U.S. and Iran had reached a ceasefire agreement, and the next day, global risk assets broadly rose. The strategy team at Western Securities pointed out that the recent U.S. 10-year Treasury yield surged again, breaking through 4.5% at one point, prompting liquidity risks that "forced" Trump to seek a ceasefire urgently. However, unlike the situation last May when Trump paused tariff wars, this ceasefire agreement contains many unfavorable terms for the U.S. and fails to substantively constrain the Iranian nuclear issue; the fundamental contradictions of geopolitical risks in the Middle East have not been eliminated.

What is more concerning is that the gold price rose concurrently with this surge in risk assets, indicating a "resonance" signal that is significantly divergent from the market performance when the tariff war was paused in May 2025. Western Securities believes that Trump's eagerness to disengage from the U.S.-Iran conflict instead conveys a key signal to the market: the U.S. may no longer be able to maintain order in the Middle East through unilateral means, the foundation of the "petrodollar" system is shaking, and the cracks in dollar credit may accelerate, leading to the initiation of the fourth wave of gold's "main rise."

Two TACO Events, Different Contexts

Understanding the limitations of this ceasefire market requires a comparison with the tariff war TACO in May 2025.

In mid-May last year, U.S. Treasury yields broke through 4.5% and quickly surged, and liquidity risks forced Trump to announce a delay in the global tariff war. At that time, the dominance over the decision to impose global tariffs completely rested with Trump; once he chose TACO, the risks of the tariff war could be temporarily relieved, and U.S. Treasury yields would quickly fall, causing global risk assets to achieve a "coordinated surge."

This time, the situation is entirely different.

The report points out that in the U.S.-Iran ceasefire agreement, as reported by Iran's Mehr News Agency, the U.S. and its allies must provide no less than $300 billion for Iran's national economic recovery plan, the so-called "war reparations," which adds considerable uncertainty to subsequent negotiations. According to Xinhua News Agency, Trump stated on Tuesday that the U.S. will not invest any funds in Iran.

More importantly, the resolution of geopolitical risks in the Middle East does not depend on the will of the Trump side—U.S. constraints on whether Israel escalates the Middle Eastern situation remain to be observed, while the main authority on whether the Strait of Hormuz can return to its pre-war free passage status lies with Iran.

U.S. Treasury Yields "Easy to Rise, Hard to Fall," Ceasefire Fails to Resolve Fundamental Contradictions

Western Securities had indicated in previous reports that unless the U.S. can quickly quell the U.S.-Iran conflict, U.S. Treasury yields may be "easy to rise but hard to fall." Currently, this judgment remains valid.

First, the Shiite "Resistance Arc" formed by Lebanon, Iran, and Yemen has not collapsed. One of the prerequisites for the U.S.-Iran ceasefire is to constrain Israel from attacking Lebanon again, but this does not seem easy to achieve at present.

Second, the traffic volume in the Strait of Hormuz is still at a low level, and restoring normal navigation will take time.

More critically, unless the U.S. can effectively control the Strait of Hormuz, even if the strait nominally achieves free passage, major countries around the world will still worry about Iran blocking it again, potentially leading to a large-scale replenishment of oil stocks. This means that the spiral of high oil prices - high inflation - high U.S. Treasury yields is unlikely to be broken in the short term, placing downward pressure on U.S. Treasury yields.

Expansion of Cracks in Dollar Credit, Fourth Wave of Gold May Start

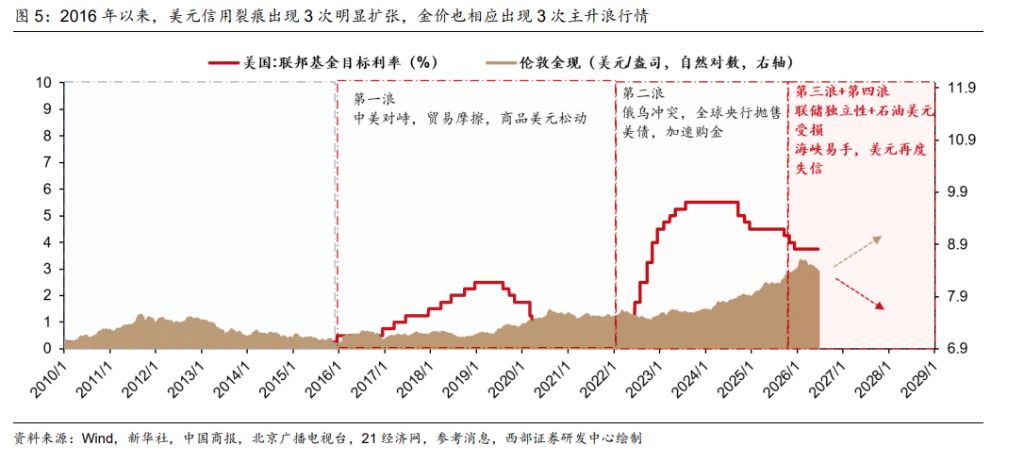

Western Securities believes the deep impact of this U.S.-Iran conflict lies in shaking the foundation of the "petrodollar" system, which is key to understanding the abnormal phenomenon of gold and risk assets rising simultaneously. The agency clearly states that the "fourth wave" of gold may thus be initiated.

The agency reviewed the three expansions of cracks in dollar credit since 2016:

- During the South China Sea issue between China and the U.S. in 2016, the U.S. attempted to suppress the internationalization of the RMB to strengthen dollar credit, which instead led to the loosening of the "commodity dollar" system, with gold prices rising against the trend during the Fed's rate hike cycle from 2016 to 2019;

- During the Russia-Ukraine conflict in 2022, the U.S. strengthened dollar credit by suppressing the economic integration of Russia and Europe, which actually accelerated global central banks' purchases of gold;

- Gold prices rose against the trend again during the rate hike cycle from 2022 to 2024.

In this U.S.-Iran conflict, the U.S. originally tried to strengthen the "petrodollar" by raising global oil prices, but substantive changes in control over the Strait of Hormuz instead undermined the geopolitical foundation of the "petrodollar." Western Securities points out that deindustrialization has led to a trend of weakening U.S. military capacity, which is the main reason for the continuous expansion of cracks in dollar credit; and every attempt the U.S. makes to repair dollar credit instead accelerates the widening of these cracks.

Trump's eagerness for TACO to withdraw from the U.S.-Iran conflict highlights the vulnerabilities of U.S. Treasuries, the dollar, and U.S. stock liquidity, and signals to the market that after the loosening of the "commodity dollar" system, the "petrodollar" system may also be on the verge of loosening.

Based on the above judgment, Western Securities suggests that asset allocation should continue to focus on the "AI + price increase" bull market barbell strategy.

On one hand, the monetary policy remains loose, AI has not yet formed a bubble, but it must accept the high volatility of AI computing hardware (communication equipment, semiconductors, storage, etc.); on the other hand, Fed QE may become an opportunity for domestic debt repair and balance sheet recovery, needing to grasp the PPI price increase chain (coal, oil, chemicals, new energy) while patiently awaiting the CPI price increase chain driven by balance sheet recovery in the second half of the year (real estate, liquor, etc.).

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。