Every Monday, Wednesday, and Friday, reviewing the market with data, grasping opportunities through trends, covering macroeconomics, US stocks, precious metals, crude oil, and cryptocurrency assets, providing insights into key changes in the global market, produced by PANews.

Macro Market

The US-Iran ceasefire memorandum has been implemented, and crude oil has once again become the only asset subjected to concentrated selling. Trump authorized the "free opening" of the Strait of Hormuz and lifted the naval blockade, with a formal signing ceremony scheduled for June 19 in Switzerland. Iranian Deputy Foreign Minister Karibabadi stated that "the achievements far exceed the commitments," with 60 days of nuclear negotiations to begin after the US fulfills its obligations.

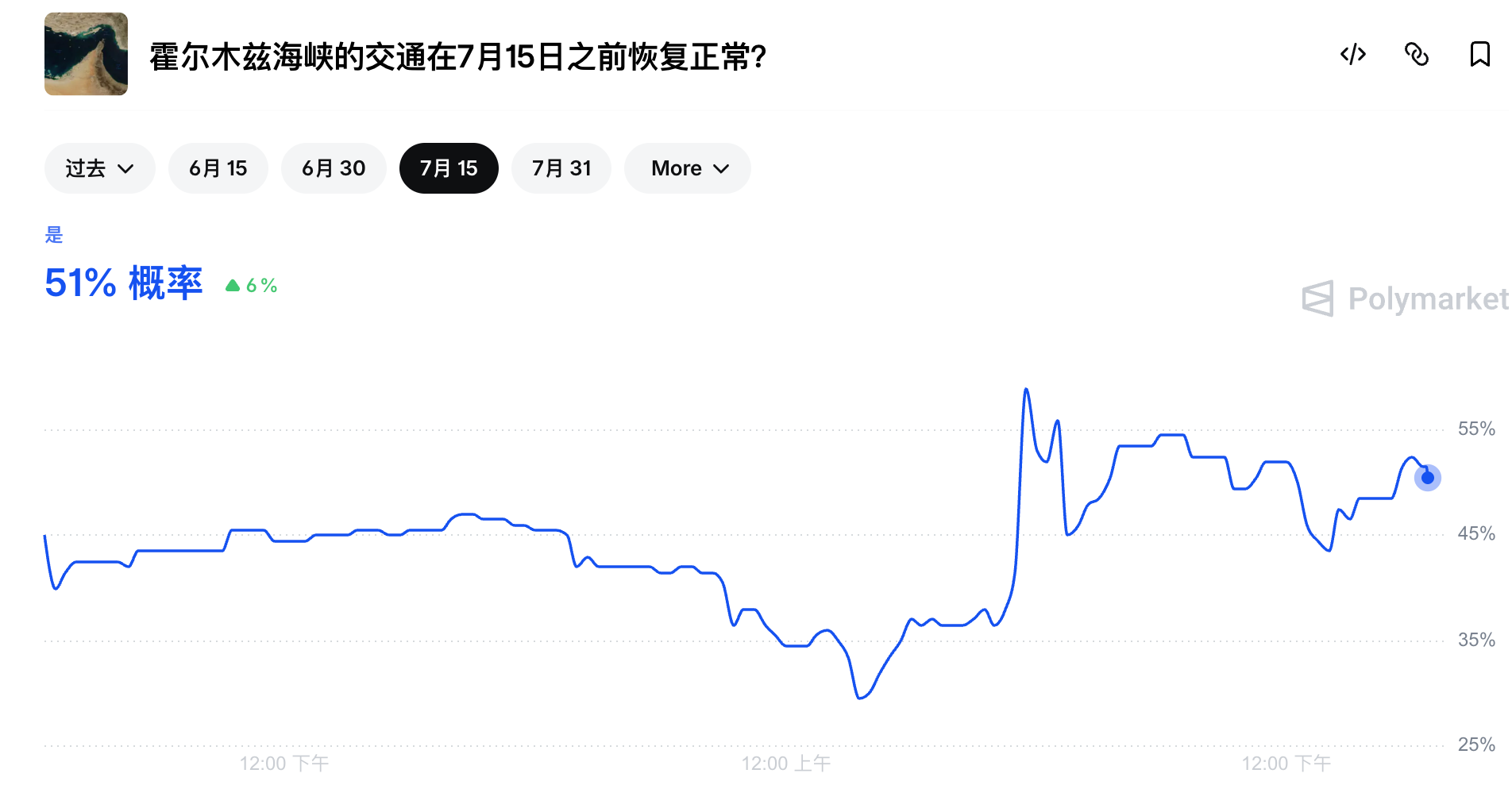

Since the end of February, the geopolitical premium that has enveloped the market has suddenly disappeared, with WTI crude oil prices plummeting 4.7% to around $80, and Brent crude oil following suit as the market bets that the restoration of supply chains will ease inflationary pressures. Analysts pointed out that the decline in oil prices directly undermines the foundation of the "re-inflation trade," and the future path of the Federal Reserve has also been repriced. Jefferies analyst David Zervos proclaimed that oil prices would naturally fall below $60, and GasBuddy also expects that by July 4, the nationwide average gas price will drop below $3.75, even though Polymarket data shows the probability of the Strait returning to normal navigation before July 15 is only 51%.

The spot gold maintained high-level fluctuations after breaking $4300, and spot silver forcefully broke through the $70 barrier, reaching a new high for this phase. The interest rates and exchange rates also responded quickly; the US dollar index weakened, and US Treasury yields fell, with the 10-year US Treasury yield dropping 5 basis points to around 4.42%. Some institutions believe this change means that "inflation risk premiums are systematically being removed."

Next, we need to focus on:

Recovery pace of Middle Eastern energy exports: If the recovery speed is lower than expected, it may once again push up inflation and energy price volatility.

June 15-17: The 52nd G7 summit will be held in France, focusing on the joint statement by the US and Europe regarding mine clearance in the Gulf and subsequent sanctions lifting.

June 18, 02:00: The Federal Reserve's FOMC interest rate resolution and the debut of the new chairman Kevin Warsh will directly determine the latest monetary path after the current decline in inflation expectations.

June 19: The US-Iran peace agreement will be formally signed in Switzerland, confirming the details of Iran verifying the US's fulfillment of obligations and launching 60 days of nuclear negotiations. If successfully implemented, it will confirm the systematic decline of geopolitical risk premiums and directly suppress the central price of crude oil.

US Stock Dynamics

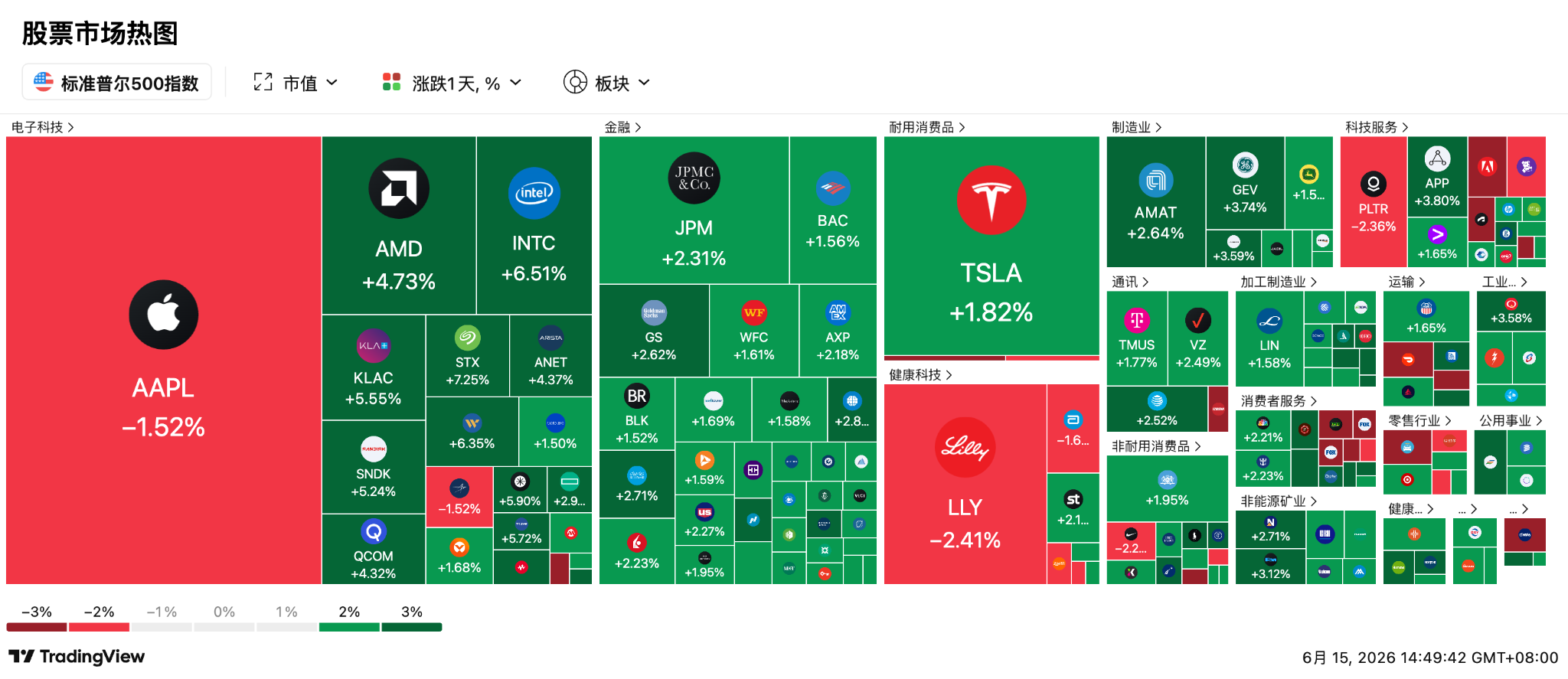

US stocks continued to rise under expectations of easing geopolitical risks, US stock futures collectively strengthened before the market opened, with the Dow Jones up about 0.98%, the S&P 500 up 1.23%, and the Nasdaq 100 leading with a rise of 1.92%.

On Friday, SpaceX's first trading day saw a surge of 19%, with a market capitalization exceeding $2.1 trillion, becoming the sixth largest company in the US stock market, with a single-day trading volume reaching $80 billion, further strengthening the narrative of "AI + aerospace capitalization." Cathie Wood even went so far as to liquidate her holdings in AMD and Tesla, heavily investing $440 million in SpaceX.

The semiconductor sector collectively strengthened, with ARM rising over 11%, Intel, AMD, and Qualcomm up 6.51%, 4.73%, and 4.32% respectively, while Adobe fell 6.7%, becoming a typical divergence target under the pressure of AI revaluation. Streaming media and consumer technology also performed actively, with Roku soaring 20% in a single day, reaching a new high for this phase.

At the institutional level, some strategists pointed out that the current rise in US stocks is driven more by "reduced interest rate expectations + easing geopolitical risks" rather than earnings upgrades, and volatility may be amplified again after the FOMC.

Next, we need to focus on:

June 16: SpaceX options contracts will be officially listed for trading on CBOE and Nasdaq, and the massive engagement of derivatives will trigger severe price fluctuations for this giant.

June 17: The Amazon "Leo Europe 3" constellation launch mission will become a catalyst to validate the continuous monetization ability of the commercial aerospace industry chain.

Cryptocurrency

Macroeconomic positives have driven Bitcoin upwards, approaching a breakthrough of $66,000, with a daily increase of over 2%. Market data shows that $64,000 has become a key support level held firmly by bulls, while the $67,200 to $68,500 range has gathered a large amount of bearish liquidity and options pressure. Notable trader Killa warned that if Bitcoin fails to stabilize in the core area of $65,000 to $66,000 after the 14th, the latter half of the month may face a severe depth correction. Some strategies suggest that if it falls below $64,000, it could trigger liquidity withdrawals to below $60,000, while breaking through $68,000 to $70,000 could open a new round of short squeezes.

The potential rate hike by the Bank of Japan is viewed as a short-term risk event by several traders, with historical data showing that similar cycles have led to Bitcoin retracements of 20% to 30%. Analyst Kaz warned that with the Bank of Japan about to raise interest rates, tightening global liquidity could push BTC up to $70,000 in the short term, after which it may sharply retreat to $50,000.

Additionally, today marks the fixed dividend date of the perpetual preferred stock STRC under MicroStrategy, occurring on the 15th of each month. Due to the US stock market being closed over the weekend, some pent-up buying demand may be released today. According to historical data, Bitcoin has seen significant increases in March, April, and May around mid-month, which may be related to the STRC dividend date effect. However, affected by previous concerns over MicroStrategy's sale of 32 BTC, STRC is currently trading at a discount of $94.80, raising doubts among investors about its dividend ability.

Key points for today:

Lido: Swellchain will cease operations on June 15, users need to withdraw wstETH assets in advance

Kelp: Starting from June 15, 20 chains will no longer support rsETH cross-chain bridging

Arbitrum (ARB) will unlock about 92.65 million tokens on June 16, worth approximately $7.8 million

Upbit 24-hour trading volume ranking: BTC, WLD, XRP, ETH, ZKC

Bitcoin spot ETF: $316 million net outflow last week, with a net outflow for 5 consecutive weeks

Ethereum spot ETF: $14.9072 million net outflow last week, with a net outflow for 5 consecutive weeks

HYPE spot ETF: $5.8662 million net inflow last week

Today's largest gain among the top 100 cryptocurrencies: ZEC up 17%, WLD up 14%, NEAR up 12%, JUP up 9%, HYPE up 8%.

Asia-Pacific Market

The Nikkei 225 index skyrocketed 5% under the influence of arbitrage capital, reaching a historic high of 69,600 points. The market showed extreme excitement over the communication vacuum created by the absence due to illness of Bank of Japan Governor Ueda, with a high probability of an interest rate hike expected this week at 88%. SoftBank Group rose 11% as foreign capital increasingly views Japanese assets as a safe haven against global geopolitical fluctuations and imported inflation.

At the same time, the South Korean market also displayed a frenzied surge, with the KOSPI index opening high and jumping 5.42% to 8,563 points, triggering a circuit breaker. The benefits of the AI hardware cycle are being realized, with SK Hynix rising over 7% due to the early shipment of HBM4E samples, and Samsung Electronics also rising 5%. This phenomenon is not only rooted in a fundamental reversal but also in foreign capital's gamble that the South Korean stock market will be included in the developed market watch list by MSCI by the end of June.

A-shares and Hong Kong stocks began to counterattack under external liquidity overflow, with the Shanghai Composite Index up 1.39%, the Shenzhen Component Index up 3.52%, and the ChiNext and STAR Market indices skyrocketing 4.95% and 4.6% respectively.

The US export ban on Anthropic's large model has sparked speculation about domestic alternatives, with AI concept stocks like Zhizhu AI skyrocketing 27%, while SMIC and Hua Hong Semiconductor rose 6% and 13% respectively. Moreover, supply chain capacity anxiety regarding NVIDIA has transmitted upstream to materials, with more than 20 PCB concept stocks like Shengyi Technology collectively hitting trading limit due to extreme shortages of HVLP4 copper foil.

Next, we need to focus on:

June 16: The Bank of Japan's interest rate decision and Deputy Governor Ueda's post-meeting statement will determine the next direction of yen arbitrage capital and whether the rally in Japanese stocks can continue.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。