Every Monday, Wednesday, and Friday, we review the market with data, grasp opportunities with trends, covering macroeconomics, US stocks, precious metals, crude oil, and crypto assets, gaining insights into key global market changes, produced by PANews.

Macroeconomic Market

Overnight, the market narrative switched from "war escalation" to "peace agreement." Trump suddenly announced during US stock trading that he would cancel military strike plans against Iran and stated that the US-Iran agreement has entered the final drafting stage, expected to be signed in Europe as early as this weekend. Risk appetite quickly returned, global stock markets, bonds, gold, and crypto assets rebounded simultaneously, while crude oil became the only asset to be sold off.

On the macroeconomic data front, inflation pressures have not dissipated. The US PPI rose 6.5% year-on-year in May, the largest increase since 2022, while core PPI slowed to 4.9%, still far above the Federal Reserve's target range. The World Bank has also downgraded its forecast for global economic growth to 2.5% for 2026, warning that if Middle Eastern energy supplies are further disrupted, global growth could drop to 1.3%. Former Federal Reserve Chair and former US Treasury Secretary Janet Yellen warned that the risk of US sovereign debt is severely underestimated by the market, while recent reasons for interest rate cuts have largely disappeared.

The situation in the Middle East remains central to market pricing. Trump claimed that Iran's supreme leader agreed to the agreement, stating that the Strait of Hormuz is expected to reopen, but both Iranian officials and Israel denied that an agreement had been reached. The market seems less concerned about whether the agreement is signed and more focused on whether the probability of war escalation is declining, with WTI crude oil and Brent crude both retreating by over 5.9% to around $85 and $87, respectively. Buffalo Bayou's strategy director Frank Monkam believes that Trump's ever-changing messages are undermining oil traders' willingness to take risks.

After extreme fluctuations, precious metals surged violently, with spot gold soaring 3.4% to recover strongly to $4212.26, while silver skyrocketed 6.2% back above $67. As the CME announced plans to launch 24/7 gold futures trading on July 26, the market is betting that volatility in precious metals will further increase.

Regarding the recent phenomenon of "central banks increasing holdings against the trend while gold prices temporarily weakened," a report from the European Central Bank earlier this month indicated that by the end of 2025, gold's share in global official reserves will rise to 27%, surpassing US Treasury bonds. Experts point out that the main reason for recent gold price fluctuations is that the consecutive surges in gold prices from 2024 to 2025 have created correction pressure, while the spike in energy prices due to Middle Eastern geopolitical conflicts has raised inflation expectations, and the market anticipates the Federal Reserve may raise interest rates, thus suppressing gold price upward momentum.

Economist Thorsten Polliet optimistically states that the recent pullback is a natural correction after rapid increases, rather than the end of a bull market. Even if gold prices fall to $3900-$4000, it still presents an extremely attractive buying opportunity for long-term investors with a five-year horizon. However, FX Empire analyst Christopher Lewis warns that $4000 for gold and $60 for silver are key support levels in the current market, and if gold effectively loses $4000, the downward space could expand to $3500; while if silver falls below $60, it could drop to the $50 range.

The yield on the 10-year US Treasury plummeted 10 basis points to 4.45%, and the dollar index fell nearly 0.8% from the day's high. Mischler Financial's managing director Tony Farren noted that core inflation, excluding energy shocks, was lower than expected, temporarily changing the mood in the bond market.

In Europe, similar hawkish signals were released. The European Central Bank raised interest rates for the first time in three years, increasing the deposit rate from 2.0% to 2.25% and the main refinancing rate to 2.4%, reflecting a renewed rise in European inflation amid energy price shocks.

Next, attention needs to be paid to:

Whether the US-Iran agreement will materialize from June 13 to 14, which will directly affect crude oil, gold, and global risk assets.

The Federal Reserve's interest rate meeting on June 18, where the market currently expects a 98.5% probability of maintaining interest rates unchanged. This decision and Powell's speech will directly determine the market's pricing on the interest rate cut path for the second half of the year; if hawkish signals are released, it may trigger a stock market correction.

US Stock Dynamics

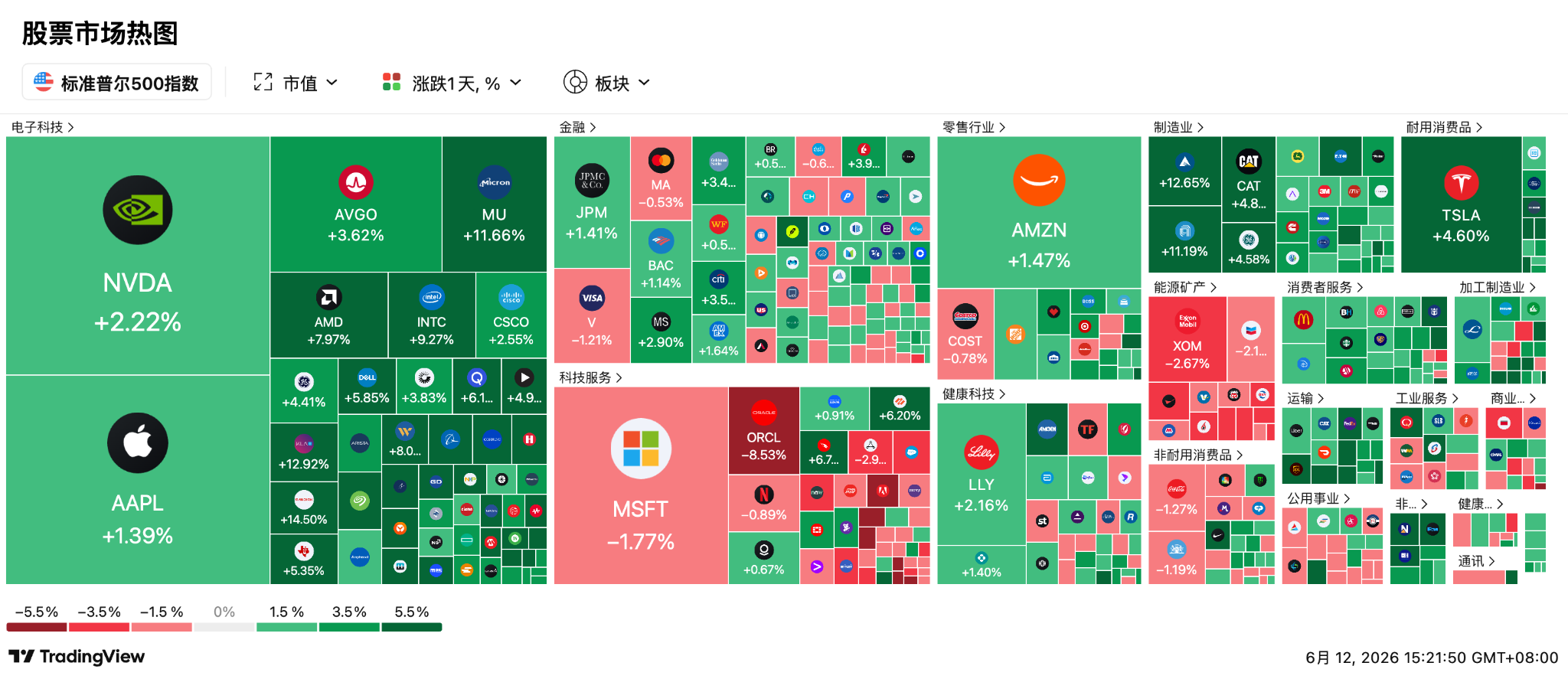

After Trump released signals of peace, the three major US stock indices soared collectively, with the Dow Jones Industrial Average gaining 929.97 points to 50848.75 points, an increase of 1.86%; the S&P 500 index rose 1.75% to 7394.30 points; the Nasdaq index increased 2.54% to 25809.66 points. The Nasdaq 100 index surged nearly 3.5%, achieving the best single-day performance in over a year.

The core storyline in the market remains AI. Although the Nasdaq 100 index lost $2.7 trillion in market value over seven trading days prior, funds have not left the tech sector and are waiting for new narrative catalysts. As oil prices fell and yields declined, the valuation pressure on growth stocks quickly alleviated.

The Philadelphia Semiconductor Index surged 7.91%, marking the largest single-day gain since April 2025. Intel rose over 9%, Micron Technology gained over 11%, ASML increased over 9%, Arm surged over 11%, and AMD rose nearly 8%. The momentum driving the market includes not only the recovery in risk appetite but also Bank of America upgrading Intel's rating from "underperform" to "buy," with a target price of $135.

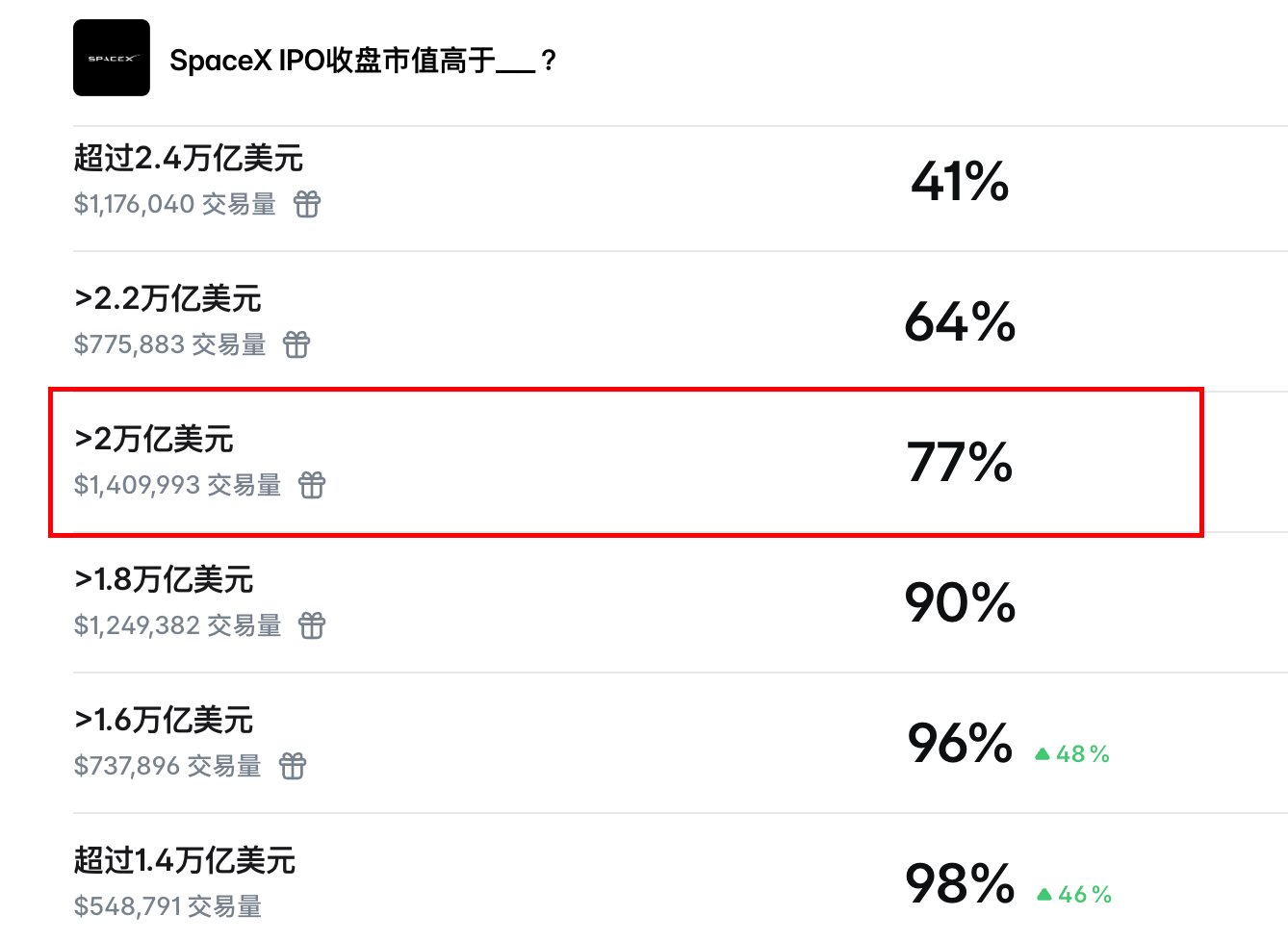

Tonight, the focus of the global market is undoubtedly the SpaceX IPO. The company raised $75 billion at an issuance price of $135, corresponding to a valuation of $1.77 trillion, becoming the largest IPO in history. The market subscription exceeds two times, with a probability of 77% on Polymarket for “first-day market capitalization exceeding $2 trillion.”

However, well-known short-seller James Chanos believes that the current valuation reflects investors' enthusiasm for Elon Musk and AI rather than fundamentals. But Oppenheimer analyst Timothy Horan stated that SpaceX is the "only vertically integrated AI company," initially setting an investment rating of "outperform" with a target price of $190, suggesting that SpaceX is expected to surge about 40% compared to IPO pricing once listed, increasing its market value to $2.5 trillion.

As a super unicorn, the funding support on the first day of opening will directly determine the risk appetite of the US stock summer market. If it breaks below the issue price, it will cause a devastating psychological blow to the overall AI sector.

Cryptocurrency

After Trump released signals of easing, BTC rebounded from around $61,000 to above $63,500, but the market has not yet escaped the bear market structure. Currently, the key support and resistance levels that the market is focusing on are around $60,000 and $65,000.

BTC is still fluctuating in the $61,000 to $64,000 range, and we need to wait for a new directional choice. Only by breaking through the $64,000 area can the market have the opportunity to challenge $70,000 again.

It is worth noting that the $64,000-$66,000 area has a large number of low-leverage short positions. Binance's spot order book has a sell wall of about $37.7 million around $64,900, while the options market data shows that $2.23 billion of BTC options are expiring today, with the maximum pain point at $66,000.

Cointelegraph data shows that the market has begun to question BTC's function as a “safe-haven asset in the stock market,” and if risk assets are adjusted again, it is not impossible for Bitcoin to fall below $60,000. Analyst Killa believes that if it drops below $60,700, the logic of a short-term rebound will fail.

Today's highlights:

Binance will allow users to place limit orders for SPCX stocks starting from June 12 at 17:05

Binance will support planned upgrades for stock trading services on June 13

Upbit 24-hour trading volume rankings: WLD, XRP, BTC, ID, ETH

Bitcoin spot ETF: -$19.0265 million, continued net outflow for 5 days

Ethereum spot ETF: -$15.8894 million, continued net outflow for 3 days

Today's top gainers among the top 100 coins by market cap: VELVET up 86.6%, LAB up 35%, H up 34.2%, XMR up 16.3%, DEXE up 10.9%.

Asia-Pacific Market

The Japanese market has become an important beneficiary of the tech rebound. The Nikkei 225 index soared 4% at one point, and the Topix rose 1.4%. The market bets that easing tensions in the Middle East will alleviate energy cost pressures, while the US semiconductor sector surged nearly 8%, directly boosting Japanese tech stocks. However, the real risks have not disappeared, as the Bank of Japan will hold an interest rate meeting on June 16, with the market widely expecting a rate hike of 25 basis points to 1%. Due to Bank of Japan Governor Kazuo Ueda's absence due to illness, Deputy Governor Shinichi Uchida will host the press conference, and the market is concerned that his statements may trigger a new round of yen arbitrage trade unwinding.

The South Korean stock market experienced a violent surge, triggering a trading circuit breaker, with the KOSPI index rising 7% during trading. Samsung Electronics surged 10%, and SK Hynix jumped 9%, the latter causing a boom in the entire industry chain's outlook due to a rare increase in equipment procurement prices. Supporting the rally is not only the AI frenzy but also explosive export data from Korea: in the first ten days of June, exports increased by 85.9% year-on-year, with semiconductor exports surging 205.8%, accounting for nearly 40% of total exports.

The A-shares and Hong Kong stocks opened higher in sync, with the Shanghai Composite Index up 1.12%, the Shenzhen Component Index up 0.75%, the ChiNext Index up 0.5%, and the Sci-Tech Innovation Index up 2.58%. The semiconductor, commercial aerospace, and precious metals sectors led the gains.

Commercial aerospace became the strongest main line. The imminent listing of SpaceX stimulated sentiment, with Tongyi Aerospace hitting the 30% upper limit, Chengxi Aviation reaching the 20% upper limit, and stocks like AVIC High-Tech, Aerospace Development, and Tian'ao Electronics also closing up.

The semiconductor sector also exploded. Fuxin Technology, Shengkong Shares, and Blue Arrow Electronics hit the 20% upper limit, with Huahong Group, Lanqi Technology, and SMIC's Hong Kong stock chip shares generally rising over 7%.

The precious metals sector remained active. Shenglong Shares reached the upper limit, with Hunan Silver, Huaxi Nonferrous, and Zijin Mining following suit.

With the 2026 World Cup in North America set to kick off (Mexico 2-0 South Africa in the opening match, South Korea 2-1 Czech Republic), discussions regarding the "World Cup curse" have re-emerged in the A-share market. Historical data shows that since 1994, the Shanghai Composite Index has seen more declines than gains during the events, with a significant contraction in trading volume. In this regard, several brokers, including Guosen and Zheshang, stated that the "curse" is not a hard rule, and additionally, "event economy" themes directly catalyzed by the events, such as food and beverage, late-night teas, and hotel audiovisual rooms, may receive short-term speculative capital attraction during the performance vacuum period.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。