Author: XinGPT

After watching many bloggers summarize Huang Jiaozhu's speech on GTC today, I feel that none of them hit the key points.

The key point is actually just one: Nvidia RTX Spark / N1X chip.

The biggest positive news is: $ARM

Why is this good for ARM? The core logic has three layers.

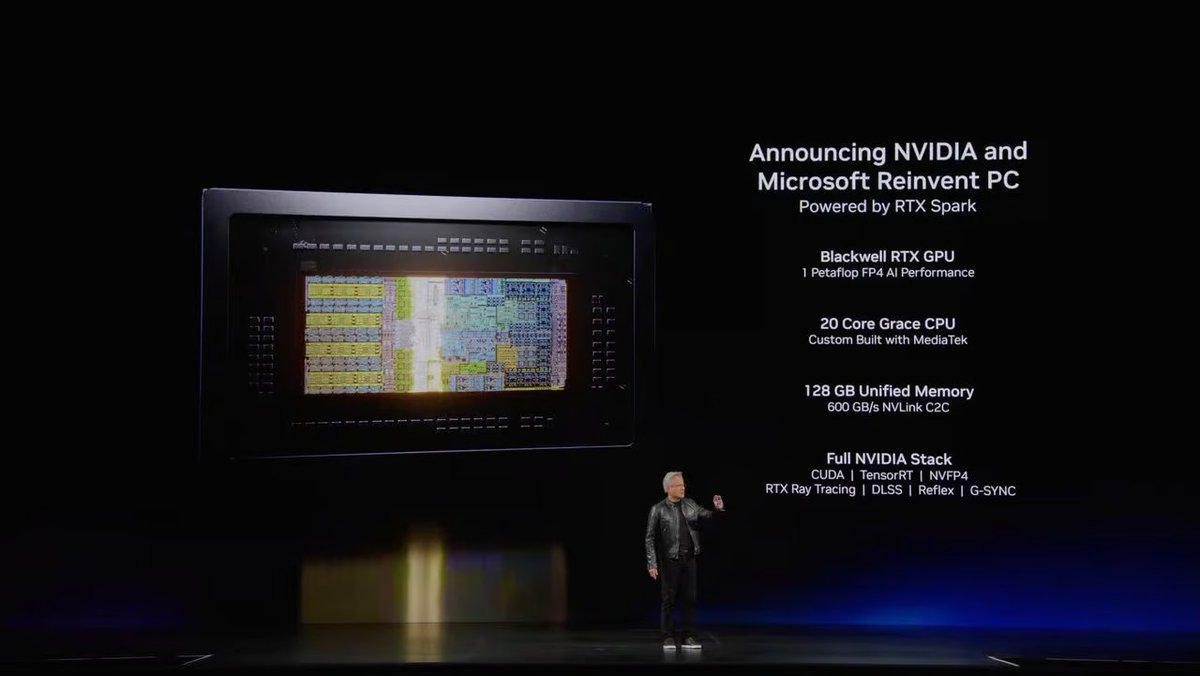

The first layer is the PC architecture narrative. In the past, the biggest issue with Windows on Arm was that it was driven solely by Qualcomm, making it difficult for the ecosystem to break out. Now, with Nvidia + Microsoft + MediaTek + multiple OEMs pushing together, "Arm PC" has been upgraded from a low-power office narrative to a "high-performance AI PC / Creator PC / local AI workstation" narrative.

The Verge pointed out that Nvidia, Microsoft, and Arm are synchronously warming up for "a new era of PC," suggesting that Qualcomm's de facto monopoly on Windows on Arm has been broken.

The second layer is royalty per chip. ARM's business model is license fee + royalty per chip. ARM itself stated in its FY26 Q3 investor material that royalty revenue grew by 27% year-on-year, driven by the adoption of higher royalty rate technologies per chip like Armv9, CSS, and the increased usage of ARM chips in data centers. This means that for ARM, Nvidia's high ASP, high core count, high-end AI PC SoC is more valuable than ordinary low-priced IoT/mobile chips.

The third layer is ecosystem endorsement. Nvidia entering the Windows PC main processor market essentially helps ARM validate a long-term bull case: the Arm architecture is not only suitable for smartphones and low-power devices, but can also enter high-performance PCs, local AI, AI workstations, and even further into data center CPUs. Reports from Reuters also mentioned that Nvidia's Vera CPU has been adopted by OpenAI, Anthropic, SpaceX, etc., and Jensen Huang emphasized that CPU/PC products are an important growth direction for the future.

In terms of competitive landscape, Qualcomm is the most directly pressured, as its differentiation in Windows on Arm has been taken by Nvidia; Intel/AMD will also be challenged, but in the short term, they still rely on the x86 software ecosystem and mainstream PC shipments to maintain their basic market share. For ARM, this means an additional heavyweight customer is helping it penetrate the PC market.

Of course, this is a short-term bullish catalyst, and whether it can translate into ARM's profits in the long term will depend on the actual shipment volume of AI PCs.

The market has already provided an answer, with ARM up 14% in pre-market, while Qualcomm fell 7%.

ARM's only problem is that it is too expensive: Analysts' expectations on Yahoo Finance show that ARM's FY2027 average revenue expectation is about $5.97 billion, and FY2028 is about $7.96 billion. Even considering the FY2028 expected revenue, a stock price of $400 still represents over 50 times P/S.

This indicates that the market no longer sees ARM as an ordinary IP licensing company, but is preemptively giving it a valuation as an AI CPU platform company. In other words, a stock price of $400 requires ARM to upgrade from a mobile IP royalty company to a comprehensive company of data center AI CPU, Arm PC, CSS, Armv9, and high-end customized computing platforms.

Of course, there is a cheaper option, which is to buy SoftBank: ARM's current market value is about $370 billion, and SoftBank holds about 86.72% of ARM, corresponding to an ARM holdings value of about $321 billion. The market value of the SoftBank group is about 48.8 trillion yen, about $306 billion. This means that SoftBank's current overall market value is slightly lower than the value of its ARM equity. Moreover, by buying SoftBank, one also gains access to other assets such as OpenAI, Vision Fund, PayPay, and SoftBank Corp.

However, there is a long-term issue with holding SoftBank, which is that Masayoshi Son has used it for financing, leading to net debt and asset financing, and its investment targets are not pure, plus SoftBank also has significant volatility risk from non-ARM assets.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。