This report is written by Tiger Research. In the field of decentralized finance lending, the discourse power is gradually shifting from project protocol parties to professional operators holding risk control decision-making power. The essence of entering the industry has become a choice: to borrow others' judgment abilities, to externally output judgment abilities, or to build and control judgment abilities independently.

Key Points

- The field of decentralized finance is giving rise to a new role in asset management, marking the end of an era where the industry is fully dominated by protocols and community governance.

- The sector is still in its early stage, but capital flows and channel resources have quickly concentrated towards leading risk management teams, and their past practical performance is becoming the core reference standard for institutional entry.

- There are currently three major entry paths in the industry: channel distribution (operating teams providing backend support), asset supply (on-chain conversion of offline assets), and autonomous operation (self-built teams becoming risk operators).

- The entry path directly determines the discourse power of the entity, the core capabilities required, and the potential risks it must bear.

- The core decision in the industry is not whether to enter decentralized finance, but how to delineate responsibilities: which risk control decision powers are delegated externally, and which core authorities are retained in-house.

1. Risk Operators: Professional On-Chain Asset Management Service Providers

Traditional finance has long separated decision-making judgment from execution, and as the crypto market matures, various specialized functions have formed dedicated professional operating entities.

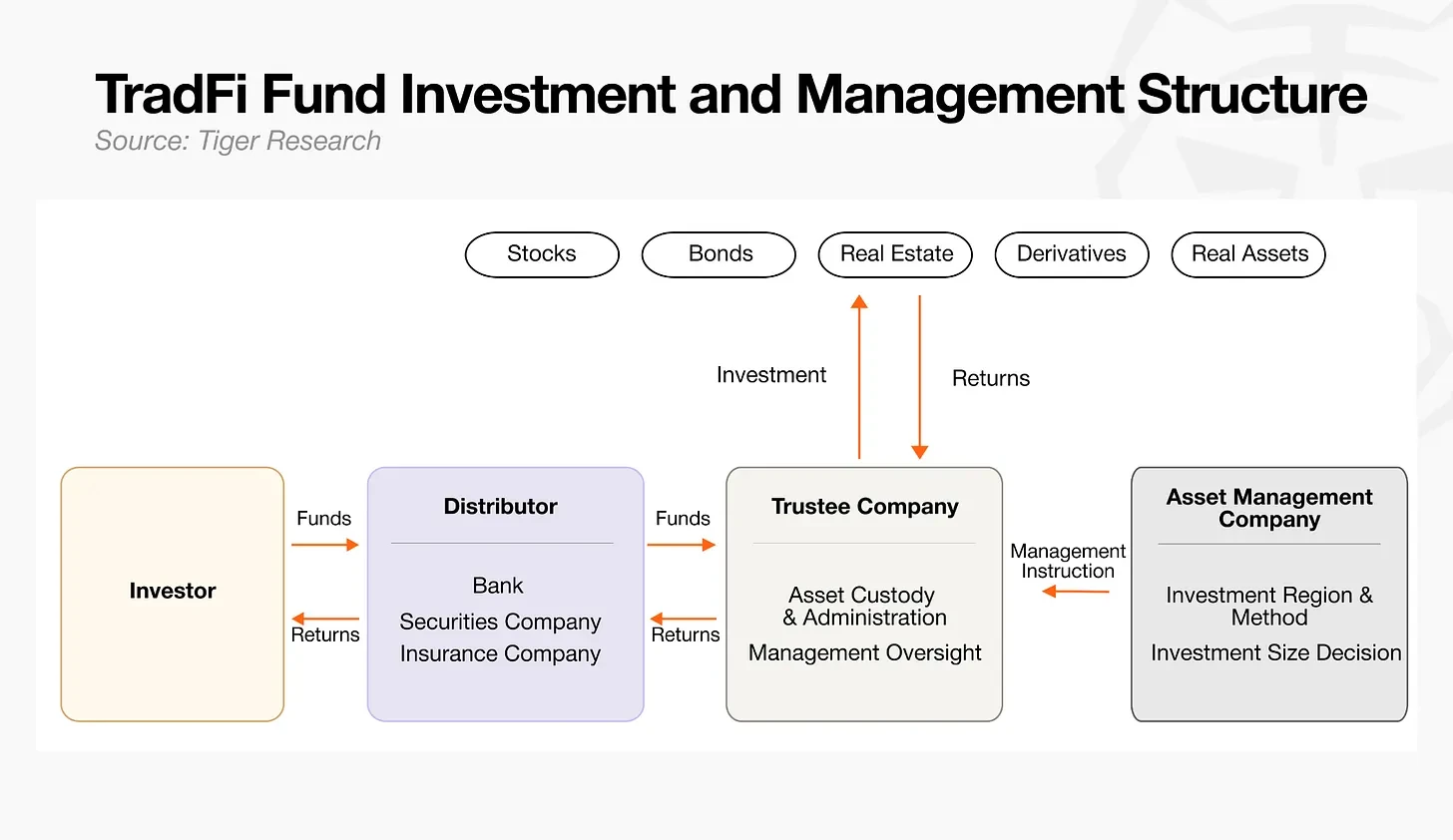

Functional Division in Traditional Finance

- Asset Managers: The core decision-making center for capital operations, formulating overall investment strategies and issuing specific execution instructions to custodians.

- Custodians: Responsible for the safekeeping of assets, strictly following the instructions of the managers to execute investment operations and overseeing asset security throughout the process.

- Channel Distributors: Sell fund products to investors, completing market fundraising and capital aggregation.

The crypto industry has evolved a corresponding functional system. Early decentralized finance relied entirely on smart contracts, but market practice has proven that relying solely on code cannot comprehensively prevent various potential on-chain risks. To ensure the smooth operation of on-chain lending, a group of professionals specializing in complex risk assessment and overall allocation have emerged, known as risk operators, who formally take on the role of asset managers within the on-chain ecosystem.

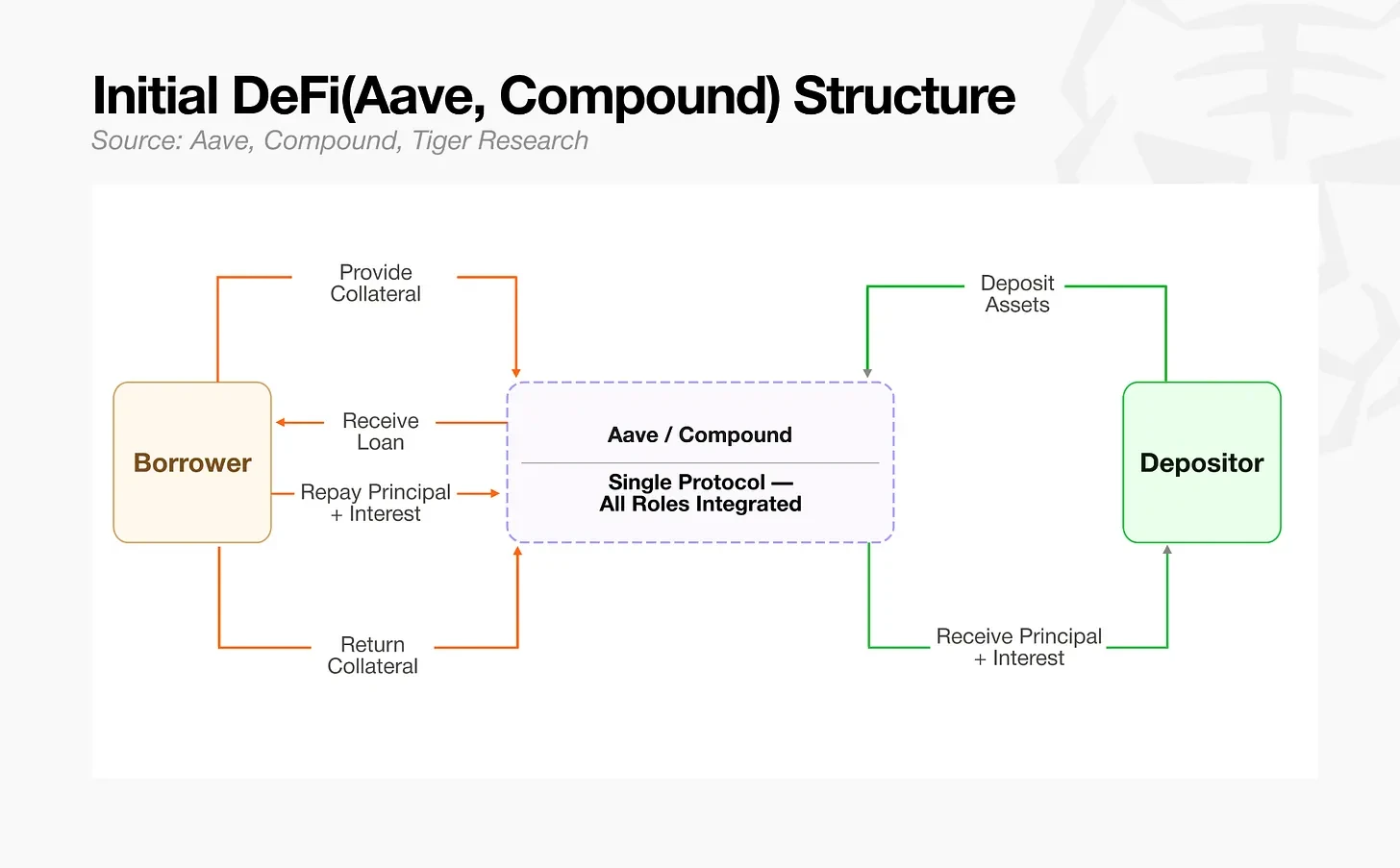

2. Early DeFi Lacking Professional Subdivided Risk Control Roles

First-generation decentralized lending protocols like Aave and Compound tightly integrate lending underlying facilities with risk control standards. At that time, although there were risk operators, all network assets were unified into a single capital pool, with operators only able to act as global risk control managers for the protocol, making minor adjustments to overall risk parameters. Once high-volatility assets flowed into the capital pool, the single pool structure could easily trigger risk transfer, and losses from a single poor-quality asset could rapidly spread throughout the ecosystem, highlighting the urgent need for dedicated personnel to manage such cascading risks.

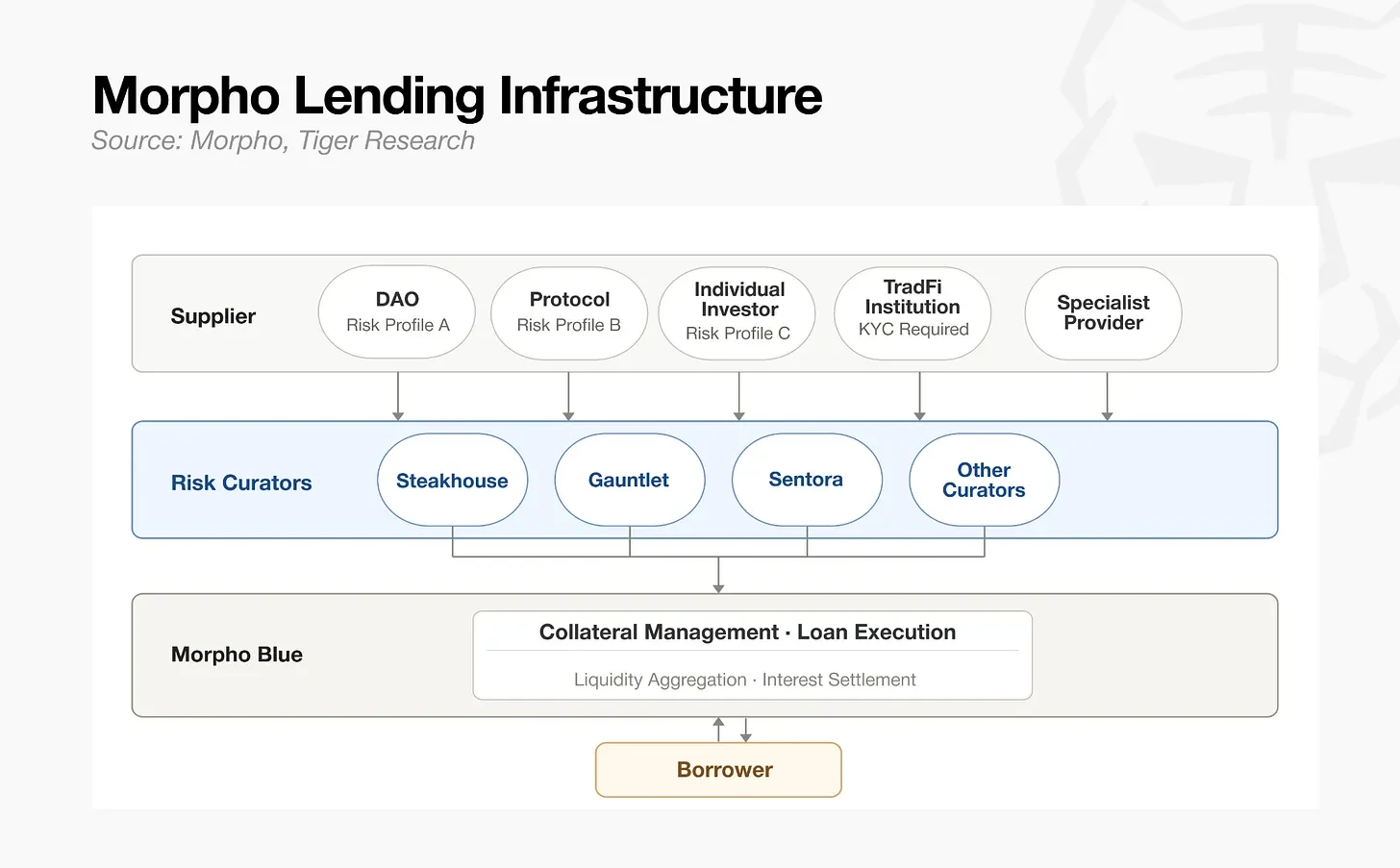

It was not until the advent of Morpho that the industry landscape was completely rewritten. This project splits collateral asset classes and loan durations into independently traded markets, replacing the traditional single capital pool with a modular multi-custody structure, fundamentally reconstructing the asset operation model, and the functions of risk operators have correspondingly transformed. Operators are no longer confined to passive risk control within a fixed protocol framework; external professional teams can independently formulate risk control rules, and build and operate dedicated lending vaults. With the complete separation of underlying infrastructure and risk assessment authority, risk operators transitioned from protocol-wide risk control managers to professional asset operators in the crypto market, independently managing multiple funding vaults.

3. Current Landscape of Leading Industry Players

As of May 2026, the global risk management sector manages assets totaling approximately $7 billion, with the top three teams accounting for 70% of the market share. The sector only officially entered its explosive growth phase in 2025, and capital has quickly concentrated towards strong teams, with investors highly favoring operational entities with mature practical performance.

The three leading teams have different entry paths:

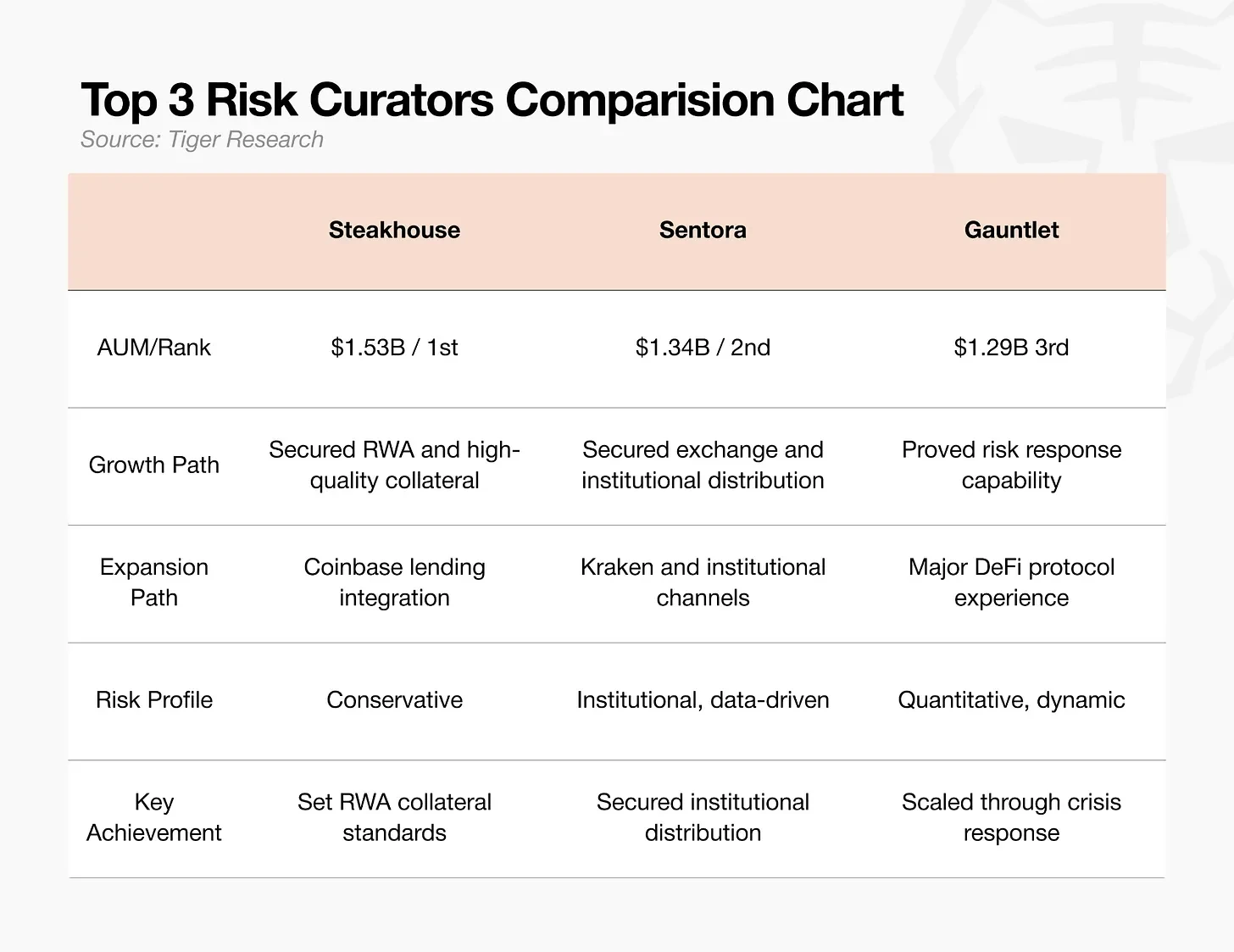

- Steakhouse: A prudently managed risk operating institution that pioneered the compliant on-chain mortgage of high-quality real-world assets like U.S. Treasuries. As the exclusive backend risk control partner for Coinbase’s lending business, it holds top-tier traffic channels, managing assets totaling $1.53 billion as of February 2026, ranking first in the industry while also leading the delineation of compliance standards for real assets that can be included as collateral within the DeFi ecosystem.

- Sentora: Built on an artificial intelligence risk control model and an institutional-level data system, deeply integrated with Kraken Exchange as a backend service provider, it solidifies the capital inflow channel for institutional funds, managing assets totaling $1.34 billion and ranking second, focusing on connecting trading platforms with institutional clients' capital flow links.

- Gauntlet: A veteran on-chain quantitative risk modeling institution, focusing on simulating various market risk control parameters. In October 2025, it undertook a $775 million influx of capital in business, completing abnormal annual yield recovery in just 10 days, demonstrating exceptional large capital risk control and crisis management capabilities recognized by the industry, currently managing assets totaling $1.29 billion, regarded as a benchmark for large capital inflow risk stabilization.

At this stage, competition in the sector has already moved beyond simple asset size comparisons; the core competitive focus has shifted to three major barriers: collateral admission standards, capital distribution channels, and emergency response capabilities for unexpected risks.

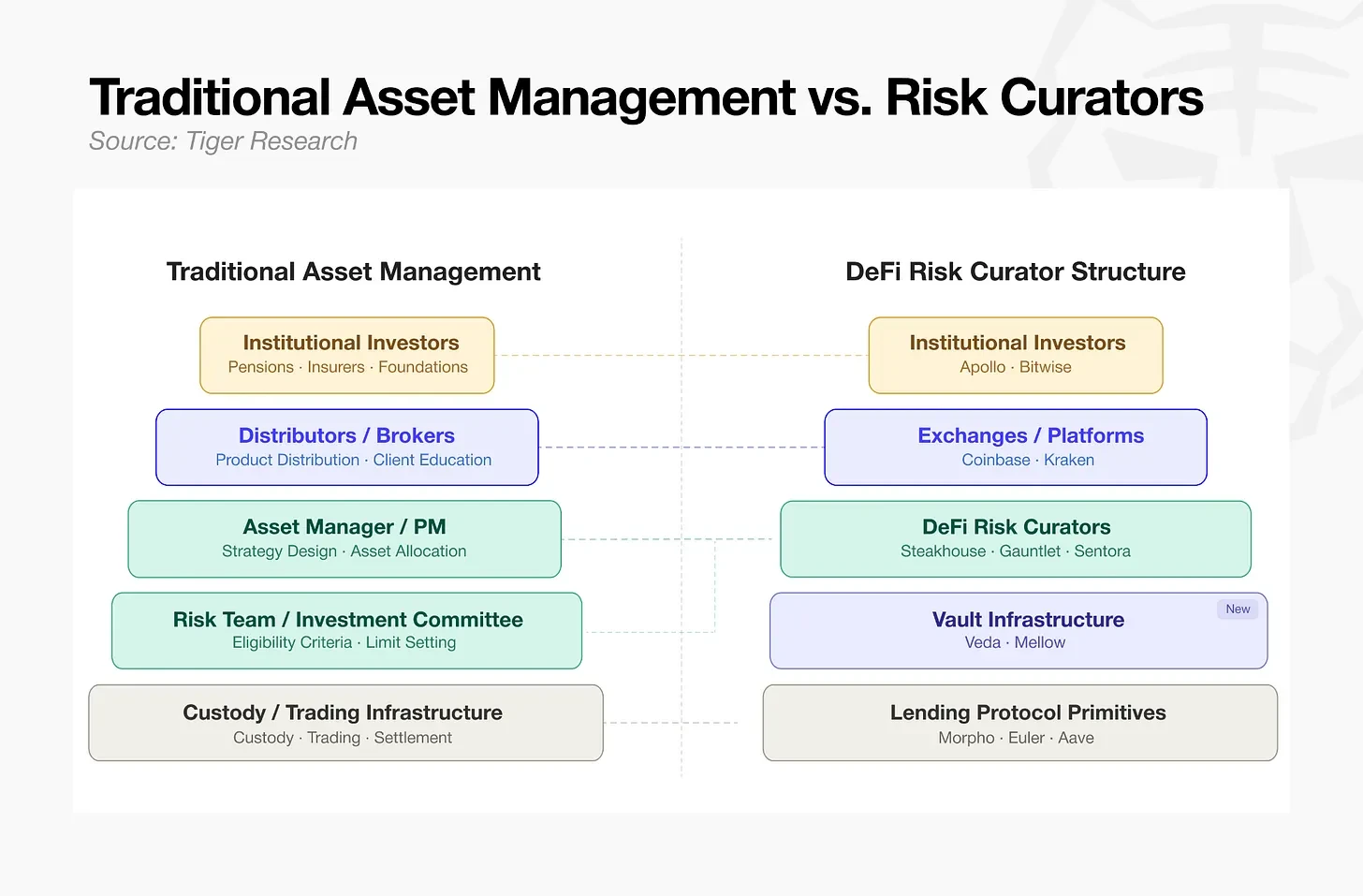

4. Traditional Asset Management Model vs DeFi Risk Operating System

With Morpho completing market modularization, different types of collateral assets now require specialized teams for independent judgment and control, leading professional risk control teams like Steakhouse to enter as exclusive risk operators for DeFi, gradually aligning decentralized finance operation models with traditional mature asset management processes.

From top to bottom, it can be clearly seen that the current DeFi underlying architecture has completely replicated the full functional division system of traditional finance:

- Top-level capital fundraising and distribution: Institutional investors serve as the core source of capital, with massive funds flowing into on-chain ecosystems through mainstream centralized exchanges and comprehensive service platforms, corresponding to traditional financial brokerage and capital distribution channel functions.

- Middle-level strategy formulation and risk control: DeFi risk operators coordinate and plan capital operation models, paralleling traditional asset management portfolio fund managers and risk control committees, establishing asset admission thresholds, position limits, and building comprehensive capital operation strategies.

- Bottom-level product construction and asset custody: Relying on capital vaults to translate operating strategies into investable on-chain financial products; the foundational lending protocols are responsible for asset storage and on-chain settlement execution, assuming the functions of traditional finance asset custody and trade clearing infrastructure.

From capital fundraising, strategic operation to asset custody and clearing, the entire operation process has thoroughly benchmarked the mature traditional financial system. For traditional financial institutions, on-chain lending is no longer a foreign emerging sector but a logically clear and well-structured standardized market, significantly lowering the entry barriers for institutions.

5. Benchmarking Traditional Asset Management: Distribution of Opportunities in the Sector

After on-chain lending has completed the functional split akin to traditional asset management, it opens the doors for various institutions to enter, but there are significant differences in entry barriers across different levels of the sector:

- Channel distribution level: Facing the end-user market, leading crypto institutions have completed market monopolization, making direct competition with traditional financial institutions extremely low in cost-effectiveness.

- Strategy management level: The core competition lies in financial professional judgment capabilities and professional talent reserves; asset risk assessment, control, and product packaging are all core main businesses of traditional asset management. There is no need to self-develop complex underlying technical systems; relying on mature modular infrastructure to implement self-built risk control systems can quickly establish a stable profit-making business model, making it the optimal entry path.

- Asset custody and underlying facilities level: Focused on blockchain technology development and implementation, this is a technology-intensive field, requiring high capabilities in underlying public chain development, making it extremely challenging for traditional financial institutions to autonomously build systems to enter.

Compared to other sectors relying on traffic resources and underlying technologies, the strategy management and risk control layer has the lowest entry barrier; traditional financial institutions can quickly capture dominant positions in the industry with their well-established risk control systems accumulated over many years.

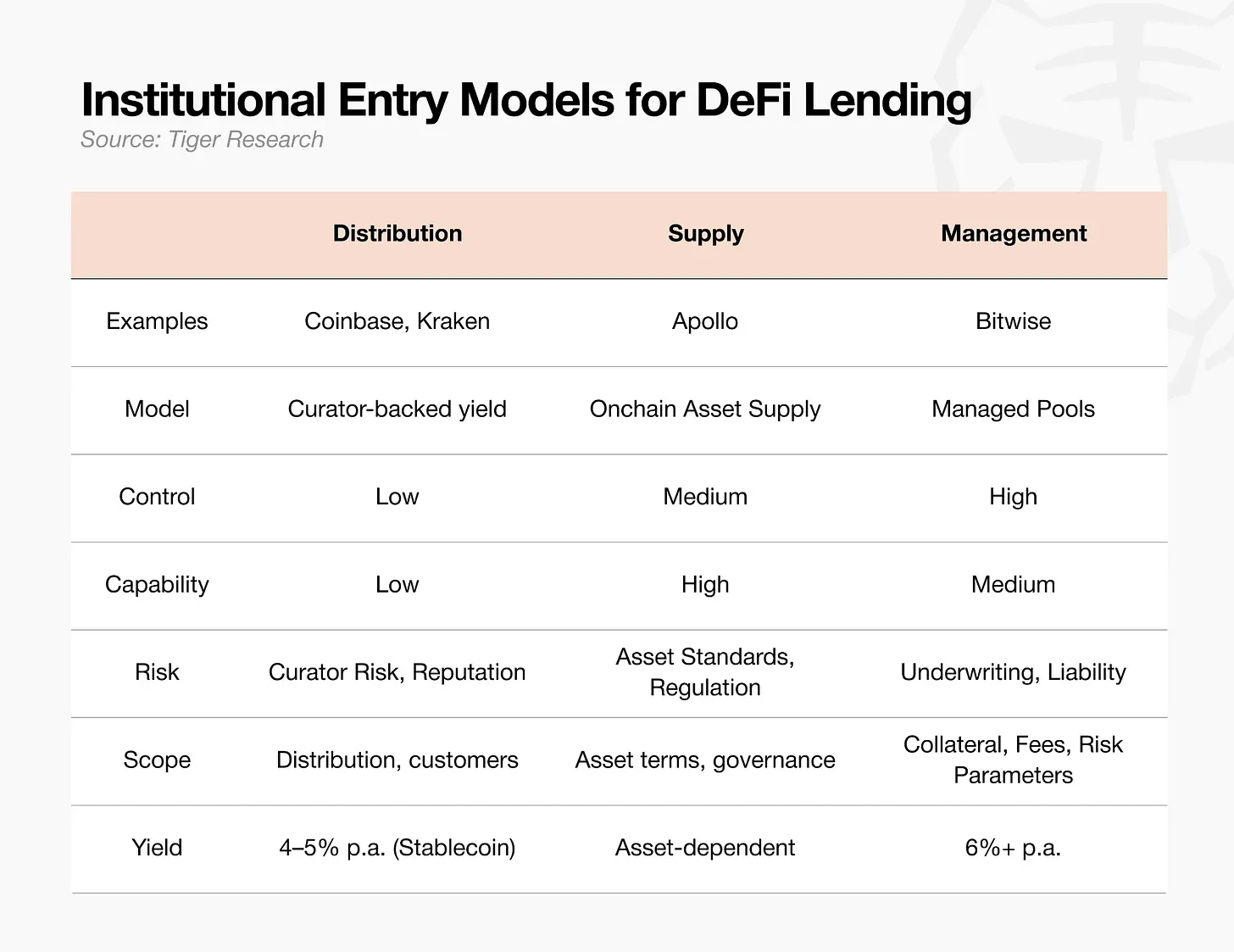

Currently, institutional entry into DeFi mainstream can be divided into three major models, regardless of the chosen path, the core competitiveness of the sector always hinges on the professional risk management judgment capabilities of the risk operating teams.

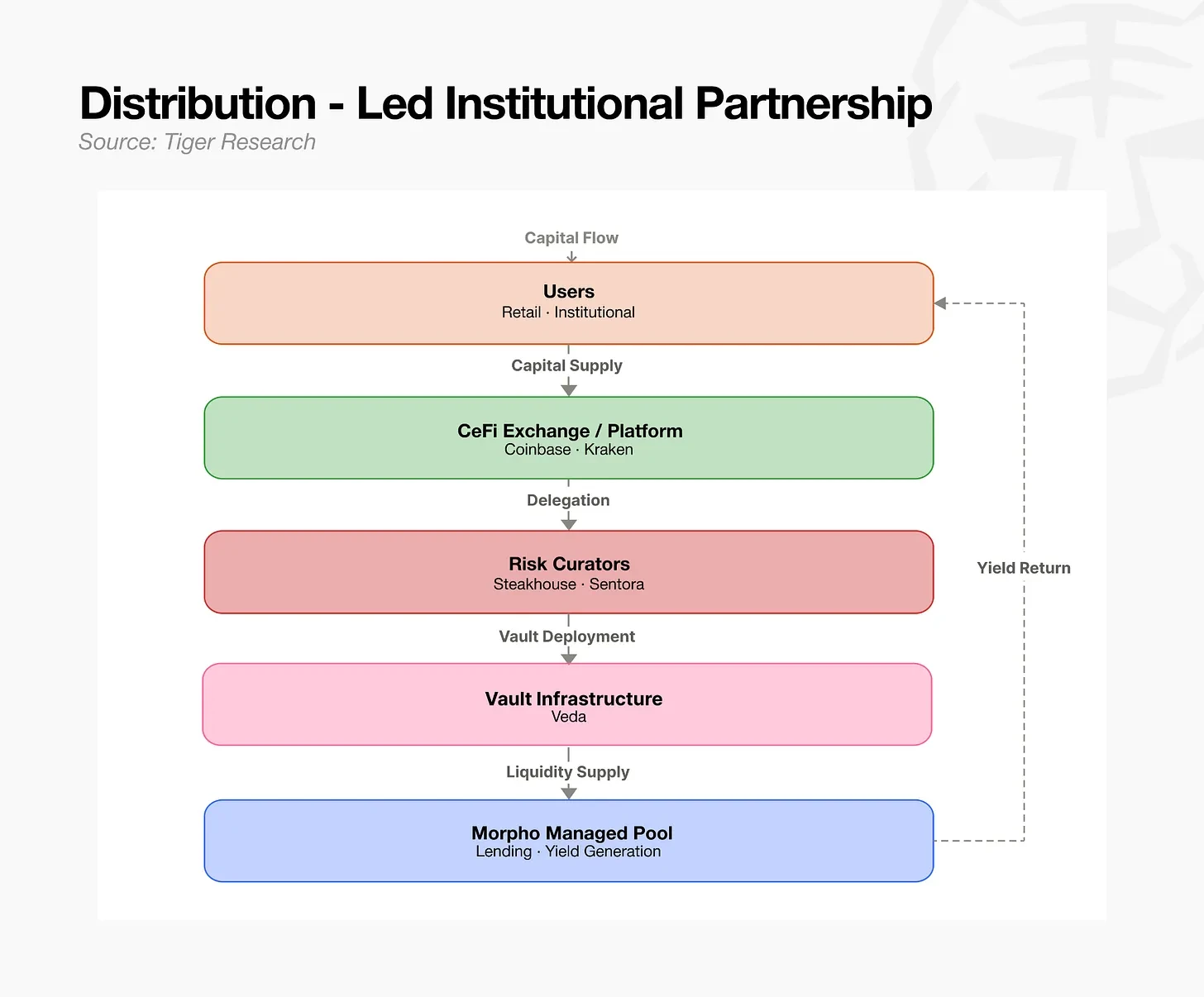

5.1 Channel Distribution Model: Leveraging Professional Teams for Backend

Harnessing a mature external risk operating team as a backend service to rapidly seize market share. This suits exchanges and fintech platforms that have massive user traffic but lack independent on-chain risk control operation capabilities. In this model, investment strategies are fully outsourced, but the risks associated with brand reputation and business responsibilities that come from the partnering team are still borne by the institution. Centralized exchanges with terminal traffic that do not wish to independently delve into complex on-chain lending risk control typically adopt this model: they connect with authoritative compliant external risk control teams as business backends, launching lending financial services. The platform is responsible for leveraging its own traffic to complete large capital inflows, while collateral review and full-process risk control are entirely the responsibility of the partnering risk operating team.

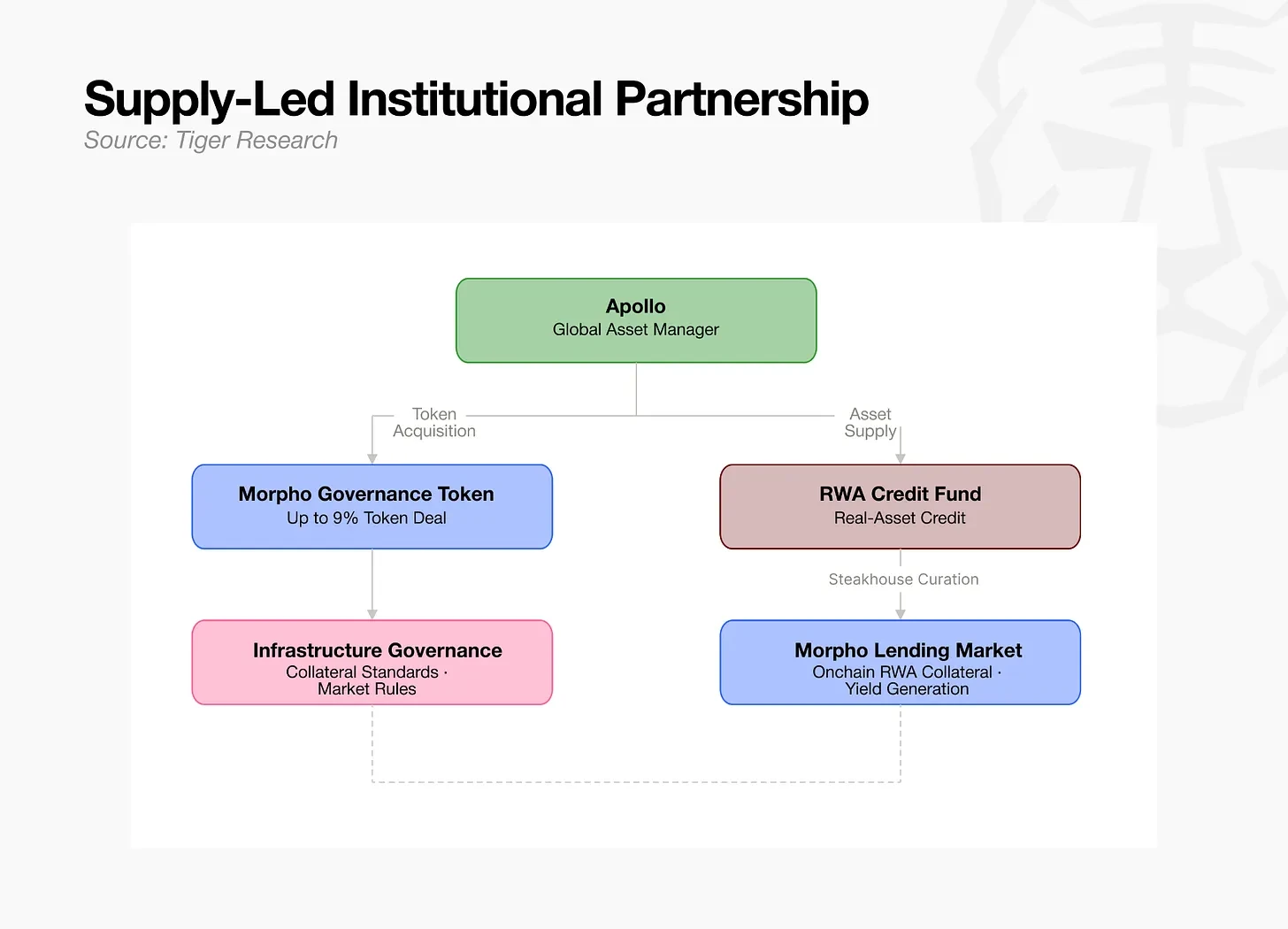

5.2 Asset Supply Model: Compliance of Quality Offline Assets On-Chain

Asset management institutions with real-world assets and high-quality underlying credit assets directly transfer their existing assets to the on-chain market. For instance, Apollo, while completing the supply of assets on-chain, also engages in governance tokens for lending protocols, deeply participating in establishing industry collateral admission rules suitable for their own assets. The core challenge of this model lies in completing the standardization and compliance of assets while building a comprehensive regulatory matching system. Large private equity institutions and holders of offline tangible assets can connect their quality existing assets directly to on-chain financial channels. Apollo goes beyond mere asset supply, increasing holdings of governance tokens in leading lending protocols, actively participating in rule-making processes, and pushing for their offline assets to become officially recognized compliant collateral in the on-chain market, with greater risk control priority. However, asset suppliers cannot haphazardly include any asset as collateral; the market requires professional third-party verification of the authentic safety of the assets to ensure they can be quickly liquidated in on-chain settlement scenarios. This phase relies heavily on the rigorous qualification review and credit endorsement from the risk operating team. Ultimately, the long-term realization of the asset supply model still relies on the asset management institution's professional strength in risk control verification.

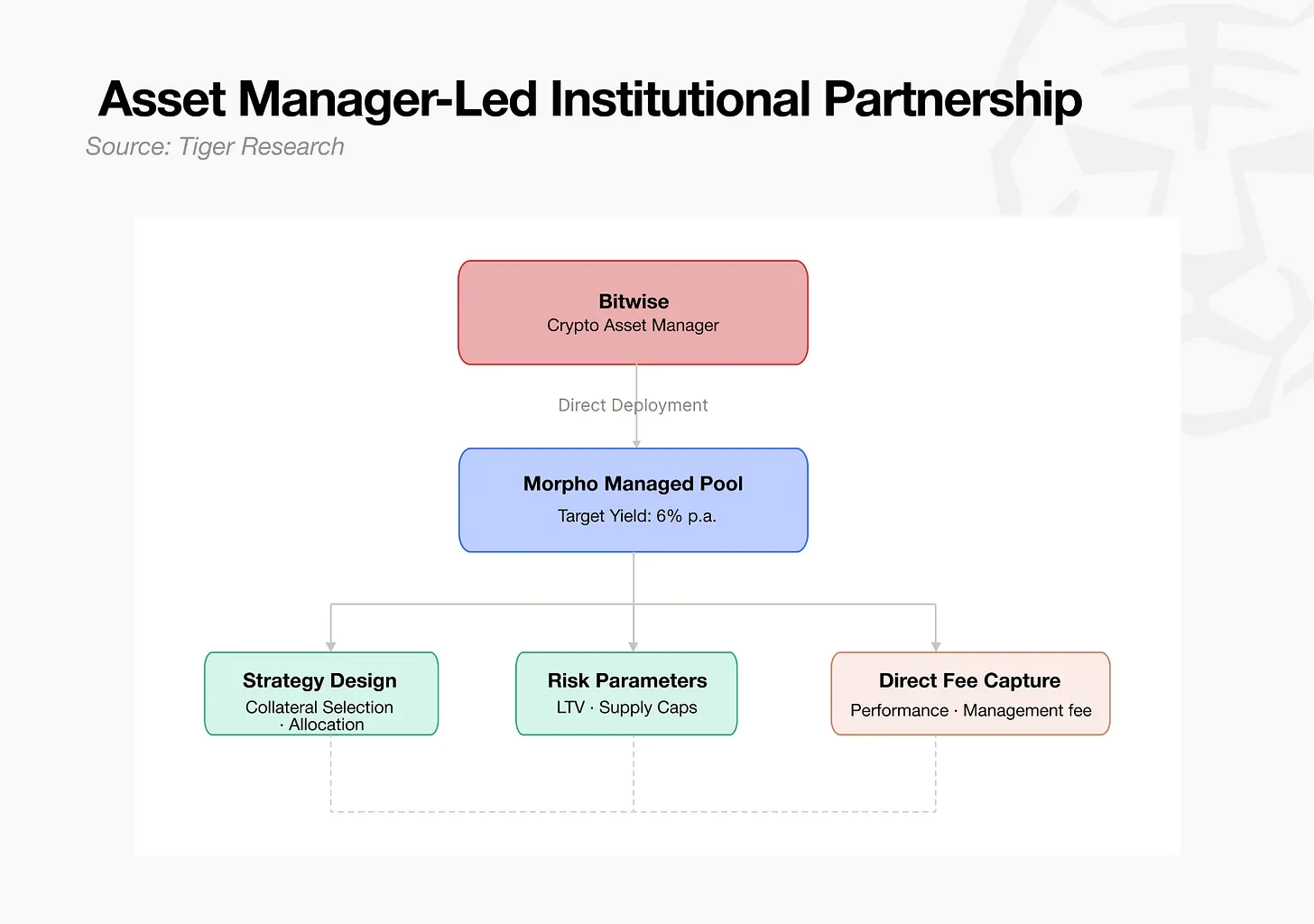

5.3 Autonomous Operation Model: Building a Team to Become Risk Operators (Representative Institution: Bitwise)

Asset management institutions independently develop investment strategies and autonomously build and operate exclusive on-chain capital vaults. Bitwise was the first to define on-chain capital vaults as 2.0 version exchange-traded funds, officially deeply entering the sector. This model has the highest degree of autonomy over fee pricing and collateral admission standards, but all risks and losses generated by business operations are borne by the institution itself, suitable for large asset management institutions capable of forming their own professional risk control teams. This model sees traditional asset management institutions move away from external platform dependencies, directly transforming into independent risk operators. Bitwise has established a system and risk control system based on its mature asset portfolio, independently designing and fully managing the operation model of on-chain vaults to directly obtain stable management returns on-chain.

6. Industry Landscape on the Eve of Massive Traditional Capital Entry

From the perspective of industry development trends, as the on-chain lending ecosystem continues to mature and improve, traditional large asset management institutions hold the strongest advantages for entry into the industry. After the DeFi ecosystem has completed functional modularization, the core market demands have shifted: the industry no longer lacks talent in smart contract development technology but is in dire need of professional financial capabilities accumulated over years in traditional finance, such as collateral due diligence audits and risk limit definitions. The practical risk control experience that traditional asset management institutions have accumulated over decades can seamlessly adapt to on-chain financial scenarios.

However, the current overall market scale of DeFi is still insufficient to accommodate the direct large-scale entry of global top-tier giant asset management institutions: the total scale of the global traditional asset management industry reaches up to $147 trillion, with BlackRock alone managing assets totaling $14 trillion; in contrast, the total size of all crypto DeFi sectors is only $80 billion, with the scale of the risk operating sub-sector being merely $7 billion, less than one two-thousandth of BlackRock’s management scale.

The stark difference in scale corroborates the massive growth potential of the sector in the future. Institutional capital traditionally adheres to a risk control-first principle, seeking to enter mature markets with well-established risk control systems. Once the risk operating teams establish a safe and stable on-chain capital circulation system, complemented by a well-formed industry regulatory framework, the industry will undergo qualitative changes. Even the smallest capital diversion from the $147 trillion traditional asset management market will quickly trigger explosive growth in the $80 billion DeFi market.

Many industry benefits only exist during the early development stage of the sector. Currently, there are only a handful of high-quality top-tier risk operating teams globally, and institutional mass entry urgently requires the establishment of mature operational rules. Teams that are the first to build a foundational operational system for the industry will firmly grasp the leading position in rule-making. Later entrants, while able to enjoy a more refined and regulated market environment, will only be able to participate in market competition following established industry rules, missing out on the core discourse power and first-mover advantages of early positioning.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。