As the rise of the US stock market this year has been heavily concentrated on a few AI-weighted stocks, there are concerns about breadth, and the dual risk of NVIDIA's earnings report has significantly amplified.

Written by: Zhang Yaqi

Source: Wall Street News

NVIDIA will release its quarterly report after the market closes on May 20 (Wednesday) Eastern Time, marking a key stress test in the current AI bull market cycle. The semiconductor sector is technically severely overbought, and option positions are heavily skewed towards bullish, coupled with a rare signal of "stock prices and implied volatility rising simultaneously," which increases the dual risks associated with this earnings window compared to previous instances.

Goldman Sachs' TMT chief expert Peter Callahan released a briefing titled "Yellow Light" on Monday, noting that the Nasdaq 100 Index (NDX) and the Philadelphia Semiconductor Index (SOX) recorded their first weekly decline of this quarter last week; the yield on the 10-year US Treasury rose to about 4.60%, marking the largest weekly increase in over a year; oil prices rebounded to about $109 per barrel; and the VIX rose in tandem. He pointed out that the core contradiction currently faced by the AI and semiconductor themes is that the fundamentals remain strong, while the technical pressures continue to accumulate.

The options analytics firm SpotGamma indicated in a recent report that the market is exhibiting a rare pattern of "rising stock prices and climbing volatility" simultaneously—usually, these two should have an inverse relationship. This signal suggests that traders are paying for protection premium against large fluctuations while chasing prices upwards. The implied volatility for NVIDIA's earnings report has now reached 6%, with market attention highly focused on this time point.

The earnings results and forward guidance will directly test the market's predictions regarding the AI computing supercycle. Given NVIDIA's high correlation with the semiconductor and broader technology sectors, its earnings performance, whether positive or negative, will trigger widespread links at the market level.

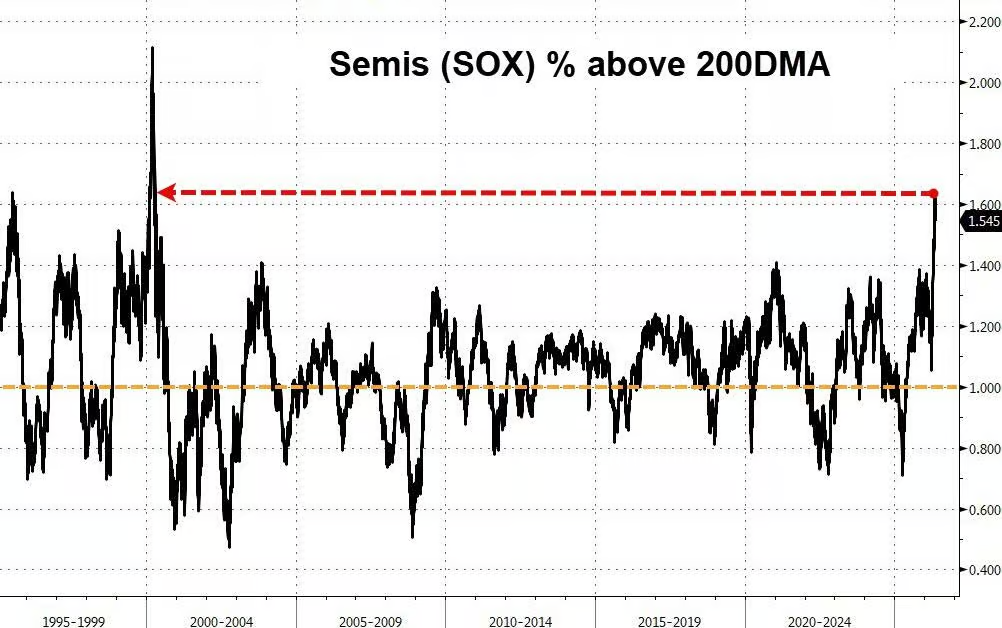

The Technicals Issue the Most Extreme Warning Since 1999/2000

The scale and speed of the current semiconductor rally have pushed the technical aspects to historically overbought levels.

Goldman Sachs data shows that the SOX index has cumulatively risen about 70% since the low at the end of March, adding over $5 trillion in market capitalization along the way. Factors driving this include a temporary alleviation of geopolitical tensions, unexpectedly strong corporate earnings—such as AMAT raising its full-year performance guidance beyond expectations, and CSCO achieving a year-on-year growth of 35% in product orders—as well as increased investor confidence in the demand for AI computing power; semiconductor industry profit expectations have been raised by over 25% since the beginning of the year.

However, Peter Callahan specifically pointed out that the SOX index is currently about 60% above its 200-day moving average, a deviation that has not been seen since the peak of the Internet bubble in 1999/2000. He also noted that Goldman Sachs' high momentum factor portfolio has experienced single-day fluctuations of ±5% or more on 12 trading days this year, accounting for nearly 15% of the trading days for the year; the rapid expansion of leveraged ETFs and options products has further amplified this dual elasticity.

"As we conclude this week’s earnings season (NVIDIA on May 20) and head into the summer trading, it's worthwhile to keep these tactical dynamics in mind," Callahan wrote. Goldman Sachs' trading desk still holds a mid-term constructive stance on the AI and semiconductor themes but tactically advises investors to remain cautious regarding the technical challenges.

NVIDIA’s Earnings Report: Forward Guidance May Be More Critical Than Current Performance

The market remains optimistic about NVIDIA’s fundamental prospects, but the recent stock price movement has somewhat priced in expectations.

According to Goldman Sachs' NVIDIA earnings preview report, analysts broadly expect NVIDIA’s revenue this quarter to exceed market predictions by about $2 billion—historically, this company’s exceedance has typically been between 2% to 3%. The market is more focused on the forward guidance for the next quarter, with current analyst consensus at about $8.6 billion, representing a quarter-on-quarter increase of about 9%. Other focal points include whether NVIDIA's cumulative revenue guidance for data centers of about $1 trillion has further upside potential and the narrative of accelerated demand for Agentic AI inference—especially its pure CPU rack products expected to start shipping in the second half of 2026.

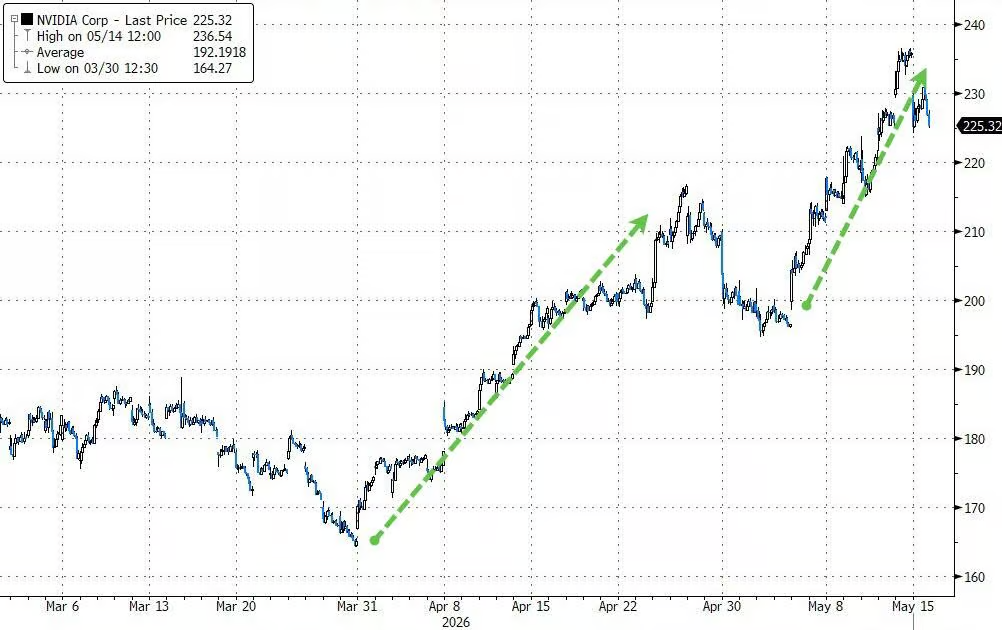

Looking at the recent price movements, NVIDIA has risen for 7 consecutive trading days, with a total increase of 20%, marking the longest consecutive rise in nearly two years; since the low at the end of March, it has added a market capitalization of about $1.7 trillion. However, Goldman Sachs data also shows that in the past 5 earnings report announcements, NVIDIA has seen declines in 4 instances on the following trading day (T+1), and there has not been a significant single-day rise triggered by earnings reports since May 2022.

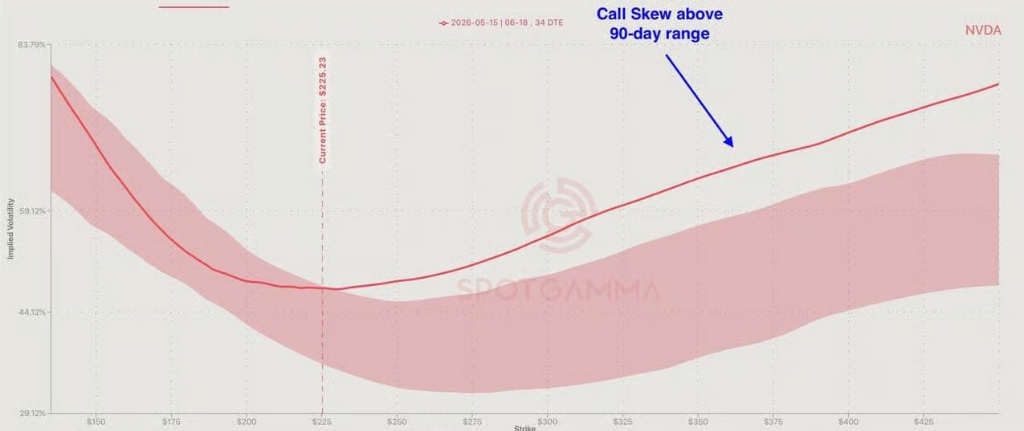

Options Market: Extreme Bullish Bets and Tail Risk Hedging Align

The options position structure exhibits a set of contradictory signals.

According to SpotGamma data, overall positioning remains extremely bullish, with traders continuously rolling NVIDIA call options to higher strike prices, maintaining call skew at the upper end of the 90-day historical range, while demand for downside protection is very limited. According to data cited by 22V Research, last Friday, the nominal trading volume of S&P 500 call options hit a historical record of $2.6 trillion, with call options accounting for as much as 60% of all options trading volume; the RSI of the Philadelphia semiconductor index also rose to its highest level since March 2000.

Meanwhile, hedging arrangements against downside risks have also quietly emerged. SpotGamma points out that there has been a significant increase in large put option structures and buying behaviors around the S&P 500 (SPY), semiconductor ETF (SMH), and DRAM-related assets, concentrated in deep out-of-the-money strike price ranges, indicating that their function is more aligned with tail risk hedging than merely directional bets. "Market participants are not bearish on NVIDIA, but their preparations for downside scenarios are not insignificant," SpotGamma wrote in its report, "any directional shift is likely to quickly impact the broader market."

SpotGamma further added that NVIDIA has cumulatively risen over 35% since the low in March, and the current scale of call option positions suggests that if the earnings report disappoints the market or triggers significant profit-taking, it could lead to a considerable directional reversal.

Breadth Risk in the Market: The Rally Is Supported by a Few Stocks

Under the strong performance of semiconductors and large tech stocks, the overall lack of participation in the US stock market is creating structural concerns.

Peter Callahan pointed out in the report that although the S&P 500 has risen about 8% since the beginning of the year, only about 52% of component stocks have recorded positive returns. The significantly lagging sectors this year include residential real estate, medical devices, construction engineering with exposure to government business, federal IT services, software and services, independent power producers, restaurant chains, commercial real estate brokerage, and insurance brokerage among many others.

Callahan candidly stated that examining the charts of these sectors makes him question whether the current market performance reflects overall "health," or merely the "funding source" effect of investors being forced to concentrate their funds in a few large-cap AI stocks. The Oppenheimer equity derivatives team also pointed out that only about one-fifth of S&P 500 component stocks have outperformed the index in the past month, with the dispersion index rising to its highest level in over a year, while the implied correlation is close to its lowest since the beginning of the year. Goldman Sachs' prime brokerage department's latest data also indicates that the technology sector has recently shown clear signs of "risk withdrawal."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。