Author: Prathik Desai

Article compiled by: Block unicorn

Over the past year, we have spent a significant amount of time reporting on perpetual contract (perps) trading platforms. Their rapid rise is hard to ignore. Perpetual futures allow participants to price in events shortly after they occur, providing around-the-clock high leverage and ample liquidity. Existing exchanges have never offered this service due to trading time and day restrictions. A team of 11 members, driven by the concept of 24/7 trading, has transformed Hyperliquid into the fastest-growing cryptocurrency exchange, with annual revenue nearing $1 billion.

Throughout 2025, the trading volume of perpetual contracts was, on average, seven times that of spot trading. This seems to be a reliable way to build a sustainable business. Thus, the inevitable happened: others followed suit.

Last week, the two major prediction markets, Polymarket and Kalshi, announced the launch of perpetual futures and cryptocurrency trading within just a few hours. Just a few months ago, Hyperliquid also announced plans to launch event contracts. The integration of perpetual contracts and prediction market platforms seems to be a natural progression. Everyone wants to become a comprehensive exchange, providing one-stop services that integrate attention, capital, and leverage.

Three weeks ago, Saurabh wrote in a report on X that Hyperliquid's entry into the prediction market would help the exchange dominate the financial space. But does this also hold true in reverse? Can the moves by Polymarket and Kalshi also yield similar returns?

Today, I will tell you all about it.

Why Perpetual Contracts Are Important for Prediction Markets

Prediction markets have a stickiness problem. They tend to be cyclical, and volume reaches historical highs when major events are available for betting, as we see during the U.S. presidential election, Super Bowl season, or Federal Open Market Committee meetings.

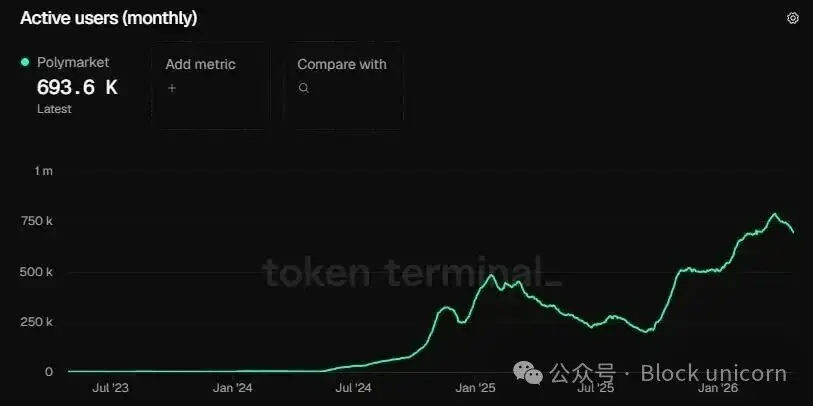

During the U.S. presidential election in November 2024, Polymarket's monthly active users peaked at 321,500. Three weeks later, this number fell by 25% to 245,000.

However, the monthly user count fluctuates up and down due to seasonal factors.

In January 2025, Polymarket's user count peaked at 500,000 and then fell below 200,000 in September. This reflects Polymarket's user retention.

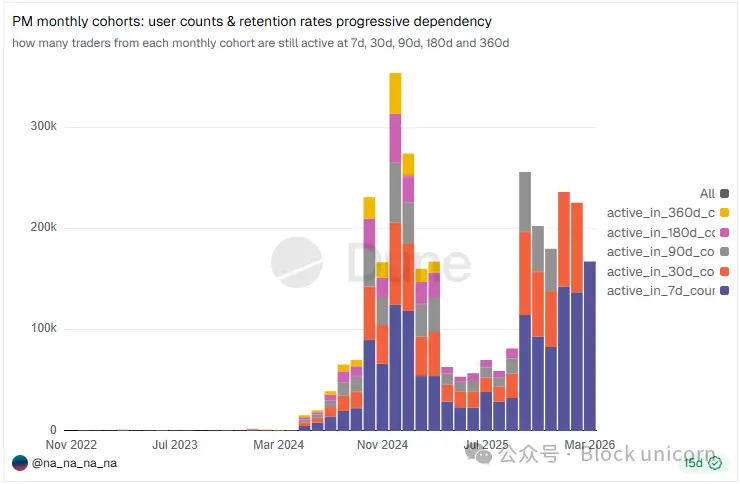

Dune's user population data shows that since 2024, only 8% to 11% of users in the monthly user base are still trading a year after joining. About 75% of users drop off within 90 days. Users may return to participate in events, but do not necessarily find the platform sticky.

But that is just part of the problem.

Prediction markets can also freeze funds until the issue is resolved. In contrast, perpetual contracts (Perps) constantly update event prices every second, attracting attention for extended periods and fostering ongoing user engagement. This is also more beneficial for prediction markets because traders' trading volumes are larger, leading to higher fee revenues.

In 2025, the notional trading volume of malicious traders exceeded $60 trillion, while the notional trading volume of precious metals traders was $28 billion.

Thus, this expansion of adjacent areas for prediction markets (PM) becomes a natural evolution. Platforms that satisfy a certain speculative demand often extend their operations into other areas. They either develop relevant functions themselves or acquire other platforms that possess those functions. We have witnessed this numerous times: Robinhood expanded from the stock market to the options market, cryptocurrency market, and eventually entered the prediction markets (PM). Coinbase acquired Deribit for a record $2.9 billion to enter the derivatives trading domain. Binance also expanded from providing spot trading to futures trading, eventually creating its native blockchain.

We often see this in traditional fields as well. A company expands its range of services in hopes of cross-selling new products to the same batch of customers. This has two purposes: to increase average revenue per user (ARPU) and to diversify reliance on multiple revenue sources, thereby enhancing the company's ability to withstand market cycle fluctuations.

In the early 1970s, the Chicago Board of Trade’s (CBOT) commodity futures revenues consistently declined. So they utilized a previously 4,000 square foot smoking lounge of the parent company CBOT to establish the Chicago Options Exchange (now known as Cboe). Since both required a common infrastructure, they were able to operate synergistically: risk management, clearing, and a network of professionals familiar with derivatives pricing.

However, operating a perpetual contract trading platform presents a huge gap between wanting to run such a venture and having the real capability to implement it.

Perpetual Stacking

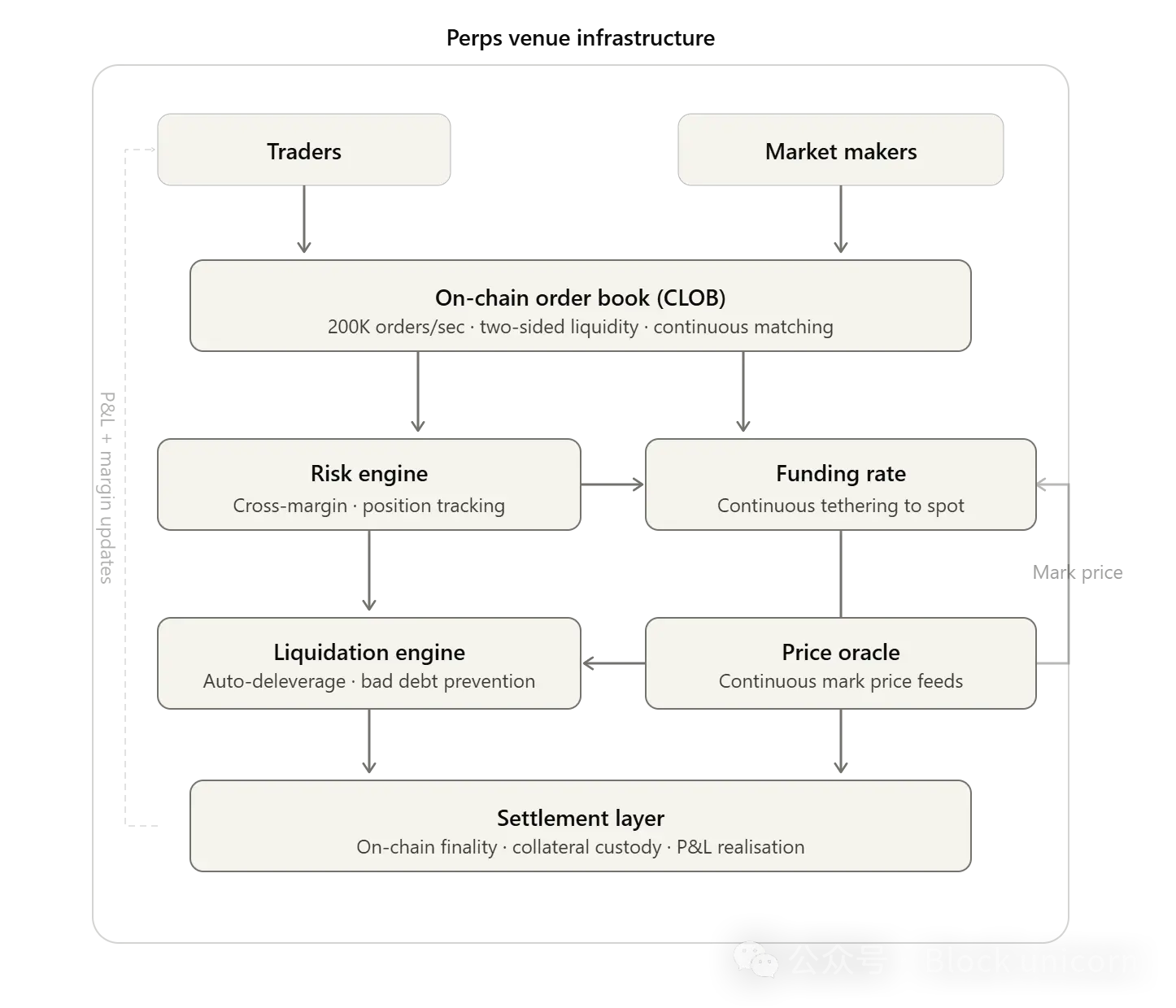

Running a perpetual trading platform involves too many components. Let's start with liquidity.

The Hyperliquid platform processes over 200,000 orders per second through a fully on-chain order book. This trading venue settles daily trading volumes exceeding $6-7 billion, employing a bilateral market-making model. Insufficient liquidity can lead to extreme volatility, excessive bid-ask spreads, and high slippage, making it easier for whales to manipulate prices.

Next is the risk engine—the core of any derivatives platform. It tracks every transaction and checks the margin requirements for each order. In October 2025, when the cryptocurrency market evaporated $19 billion, the Hyperliquid platform handled billions in settlements without interrupting services.

Additionally, there is a funding rate mechanism that ties traders' prices to the spot price of the underlying asset. This mechanism continuously operates by settling small amounts between long and short positions every few hours.

Building the entire tech stack is not the primary issue; I believe the prediction markets can achieve this. The greater challenge lies in stress testing this tech stack.

Hyperliquid built all these systems and stress tested them in real scenarios, such as a 10/10 cryptocurrency liquidation event and the U.S.-Iran war. After everything was ready, they launched event contracts through HIP-4. Kalshi and Polymarket, on the other hand, are trying to do the opposite. They operate successful prediction markets that do not require any of the aforementioned systems. Now, they not only have to compete with the very successful Hyperliquid but also with an untested system that cannot cope with the high-frequency activity of perpetual trading, vying for market share.

For prediction markets, there are many unfavorable factors that make expansion to perpetual contracts more challenging than vice versa.

Hedging Synergy

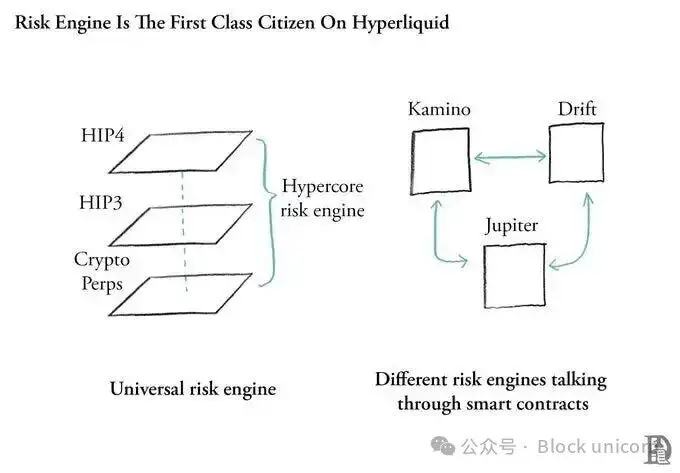

On the Hyperliquid platform, the risk engine monitors all your positions across all trading pairs, spot markets, and upcoming event contracts. Saurabh explained this in his HIP-4 report.

It looks at all your positions without distinction. Ultimately, the leverage you use and the margin you keep as cross-collateral determine when you will be liquidated. The combination of positions in spot, futures, prediction markets, or any other markets determines how much margin you need to maintain.

But Saurabh, aren't other blockchains like Ethereum or Solana also composable? Of course they are. On a general-purpose chain, each application runs its own risk engine in its respective smart contract. They cannot atomically view each other's states. Therefore, Kamino cannot know what is happening on Pacifica. Aave cannot know what is happening on Lighter. All applications are smart contracts on their respective chains. Each application or smart contract has its own independent risk engine; making them aware of one another, that is, creating a universal risk engine, requires massive collaboration.

This universal risk engine solves a core funding issue by optimizing the same capital across multiple trades made by traders in the trading venue.

Let's say a trader on the Hyperliquid platform goes long on ETH with 5x leverage. She is concerned about the Federal Reserve's interest rate decision next week, so she buys an event contract at a price of $0.65 for the outcome of "Federal Reserve Keeps Rates Unchanged". Since both positions are stored in the same margin account due to using the same risk engine, if the Fed unexpectedly cuts rates and ETH prices rise, her long position profits, while the loss on the outcome contract is only her principal invested. If the Fed keeps rates unchanged, the outcome contract pays off, partially offsetting the loss on her long position.

This is why a prediction market platform or a hedging trading venue cannot just be an added feature. This hedging possibility is precisely what gives HIP-4 value on the Hyperliquid platform. Ordinary traders on the platform view the prediction market as insurance against reversals in their existing hedged positions.

Currently, collateral on the Polymarket and Kalshi platforms will be locked until the event is resolved. Therefore, unless they provide a unified risk engine between their real money trading and prediction market trades, they will lose a key factor that keeps traders on the platform. Neither of these platforms has announced the implementation of a cross-margin system between their prediction market trading and real money trading venues.

The categorization of prediction markets and the average trader profile further raise concerns about their ability to replicate successful performance in real-money trading.

Over 80% of Kalshi's monthly total trading volume comes from sports-related trades. This percentage for Polymarket also exceeded 40% in 2025. So, how do you build a sustainable pricing mechanism for a paid trading platform around these sporting events? This would exclude a large portion of traders from participating in paid trading.

Moreover, Kalshi's ordinary traders are retail investors who have never interacted with cryptocurrencies, funding their prediction market accounts through ACH transfers from their bank accounts. Therefore, even if we assume the theoretical possibility of cross-margining on the Kalshi platform, I doubt these traders have the expertise required to double down on the platform and use perpetual contracts as a hedging strategy.

What Methods Might Work for Prediction Markets?

If Kalshi and Polymarket announce cross-margining, I think there is a situation in which these bets would work. Their relationships with major brokers and clearing companies could facilitate high-value, high-frequency trading activities for event contracts and perpetual futures.

This would enable institutional trading departments to view prediction markets as part of a broader risk management toolkit.

Both Kalshi and Polymarket have partnerships that enable them to access institutional clients.

Kalshi's collaborations with FIS and Tradeweb data, along with Polymarket's trades with the Intercontinental Exchange (ICE), could help retain institutional clients who value the use of perpetual contracts to hedge their prediction market positions on the same platform.

This remains an elusive goal, requiring many factors for prediction markets to develop favorably. They need to establish stress-tested infrastructure, form partnerships, and prove to clients that their platform can help optimize capital allocation.

But this is a necessary condition for their survival in fierce competition. With distribution channels occupied by Hyperliquid, they have no choice but to seek maximum opportunities elsewhere.

That concludes today; see you in the next article.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。