The market lacks confidence in a strong opening surge, but the potential for future growth is worth looking forward to.

Written by: Eric, Foresight News

After a six-month wait, the highly anticipated "high-performance L2" MegaETH's token MEGA will officially launch and open for trading. On-chain trading will open on April 30th at 6 PM Beijing time, while off-chain trading (on exchanges) will open at 7 PM.

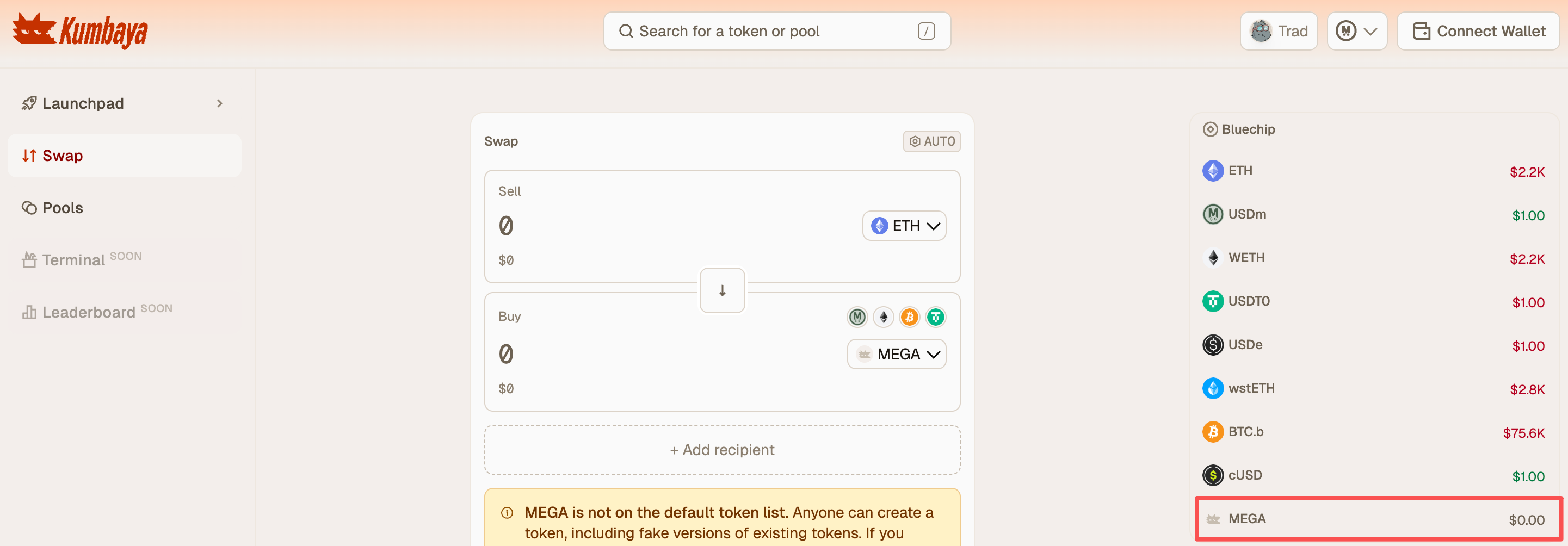

As the native token on MegaETH, MEGA's on-chain trading will initially be conducted on the DEX of MegaETH. Currently, the largest DEX on MegaETH, Kumbaya, has already listed MEGA. Investors eager to get in on the first wave can prepare USDC in advance and convert it 1:1 into the native stablecoin USDM on MegaETH through the official cross-chain bridge, or transfer assets like ETH via cross-chain bridges such as LI.FI, Stargate, and Across.

On the centralized exchange side, the two major Korean exchanges, Upbit and Bithumb, have confirmed they will list the MEGA KRW trading pair, and Bitget as well as Coinbase have also confirmed they will list MEGA.

MegaETH will allocate at least 500 million (5% of total supply) tokens to holders of The Fluffle NFT. Holders can claim 50% at the TGE, with the remaining portion unlocked in batches. Additionally, MegaETH will airdrop 2.5% of the total token supply, but this airdrop aims to incentivize the use of the mainnet and is not a broad-based airdrop activity.

Currently, MegaETH has launched the Terminal Points System, which will run from April 28th to June 23rd, for a total of 8 weeks. Users can interact on the mainnet to earn airdrops, including but not limited to cross-chain activities, participating in DEX trading or providing liquidity, and engaging with gaming applications. The official statement indicates that rewards will be distributed based on users' points and activity quality, which means behaviors focused solely on farming airdrops may be excluded.

The next big question is, how will the market price MegaETH?

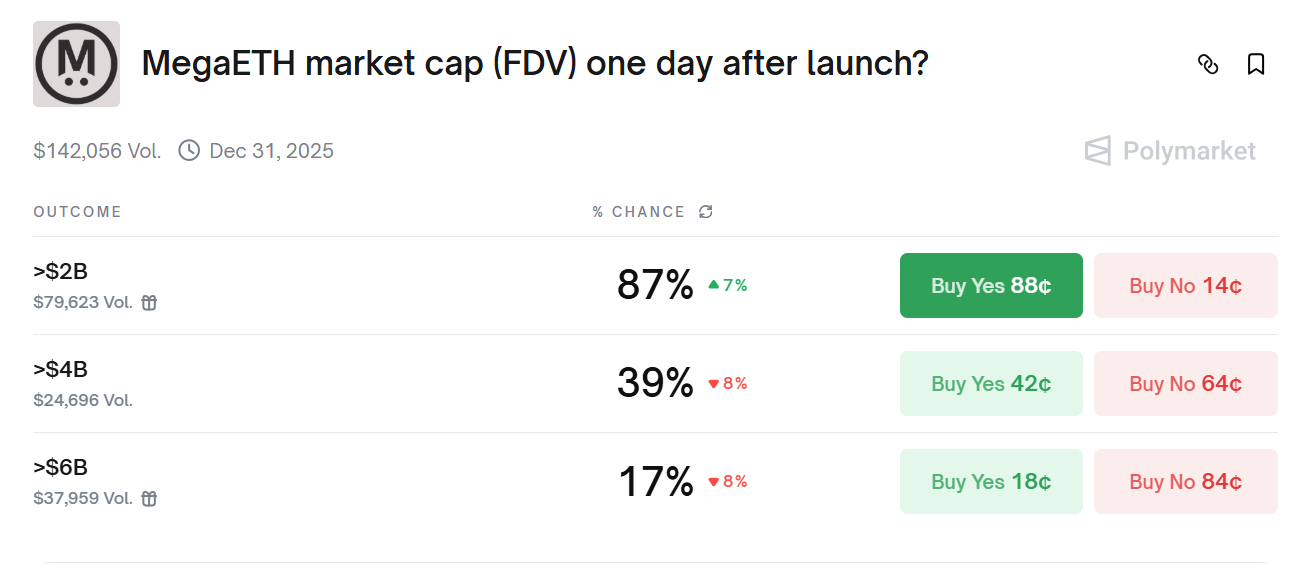

During MegaETH's public offering at the end of October 2025, the subscription amount reached an astonishing $1.39 billion, which is 27.8 times the hard cap of $49.95 million. The final valuation for the public offering also hit nearly $1 billion. Prior to the public offering, the FDV forecast for MegaETH on Polymarket was very aggressive, with predictions on October 23rd suggesting an FDV of $2 billion and $4 billion one day after the token launch, with probabilities reaching 87% and 39%, respectively, while the following day, the probability of exceeding $4 billion briefly surpassed 50%.

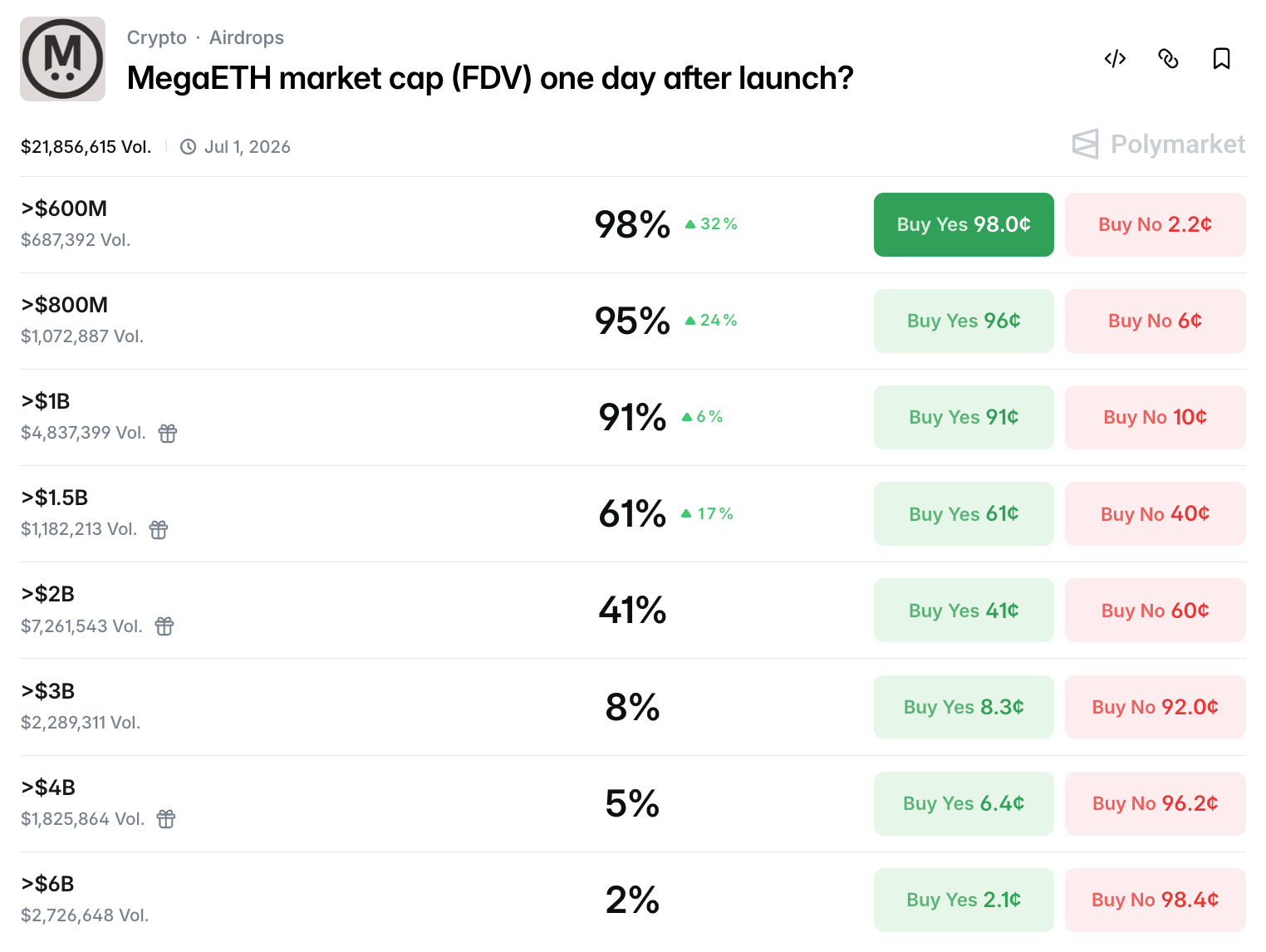

However, at that time, the market's trading volume was only 140,000, which inevitably distorts the data. After 6 months of negotiation, the trading volume of this prediction market has now reached nearly $22 million, and market sentiment has clearly calmed down significantly.

From the data, there is a fair amount of confidence that breakeven (FDV greater than $1 billion) is feasible. Still, the probabilities of FDV exceeding $1.5 billion and $2 billion are much lower than earlier optimistic expectations. The highest probabilities for exceeding $600 million and $800 million indicate participants in the public offering may even incur losses. Investors looking to get in on the first wave may need to pay more attention to real-time market changes.

In the current market conditions, the reason MegaETH still has such a high valuation partly stems from the project's team's "eccentricity." Earlier, MegaETH publicly stated it would cancel the public offering allocation for investors looking to hedge; amidst frequent pressure from participants urging for token issuance, they insisted on launching the token only after achieving certain KPIs for the ecosystem.

MegaETH focuses on "high performance," with block confirmation times as short as 10 milliseconds, and introduced a mechanism for MEGA-priced auctioning with priority access, millisecond-level trading queue privileges, and high-frequency trading teams and market makers needing to bid continuously for MEGA to obtain priority packaging rights. Thus, MegaETH is likely to be more favorable for high-frequency trading and almost disproved applications like gaming, while also creating active demand for the MEGA token.

DeFi Research mentioned two days ago that due to MegaETH's strict locking mechanism, the actual circulating volume of MEGA at the initial opening is less than 4% of the total supply, leading to potentially extreme volatility. However, if the rigid demand logic for MEGA tokens is confirmed later, and there are no extreme unforeseen circumstances in the overall market, MEGA is believed to have certain upward potential.

A similar logic is reflected in Canton. In the early days of the CC token launch, the market was not optimistic, but as many of the major financial giants in the U.S. began using Canton for asset trading and settlement, its daily network transaction fees surged to the top of the entire network, and the CC token rose against the trend during a downturn in the broader market. For prudent investors, it is entirely reasonable to wait for the volatility to decrease and seize the opportunity to enter based on the actual development of the network ecosystem.

MegaETH has chosen a relatively pragmatic path, rather than treating the issuance of tokens as a sort of "finish line." However, this also further tests the team's ability to control the rhythm. For investors, this serious operational model is worth observing as a case study. If MegaETH can gain more attention in the future, it may increase the market's focus on projects that prioritize actual income and profitability.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。