Previously, MSX has released a preview overview titled “Oil Prices Rise, Interest Rates Hard to Drop, Seven Sisters at a Standstill: Which Main Lines Should Be Considered for Q2 Excess Returns in US Stocks?”, systematically organizing the overall market main lines for Q2. Following this framework, it becomes clear that the AI market in US stocks in Q1 is no longer as simple as just “whether the leading chip companies are rising”.

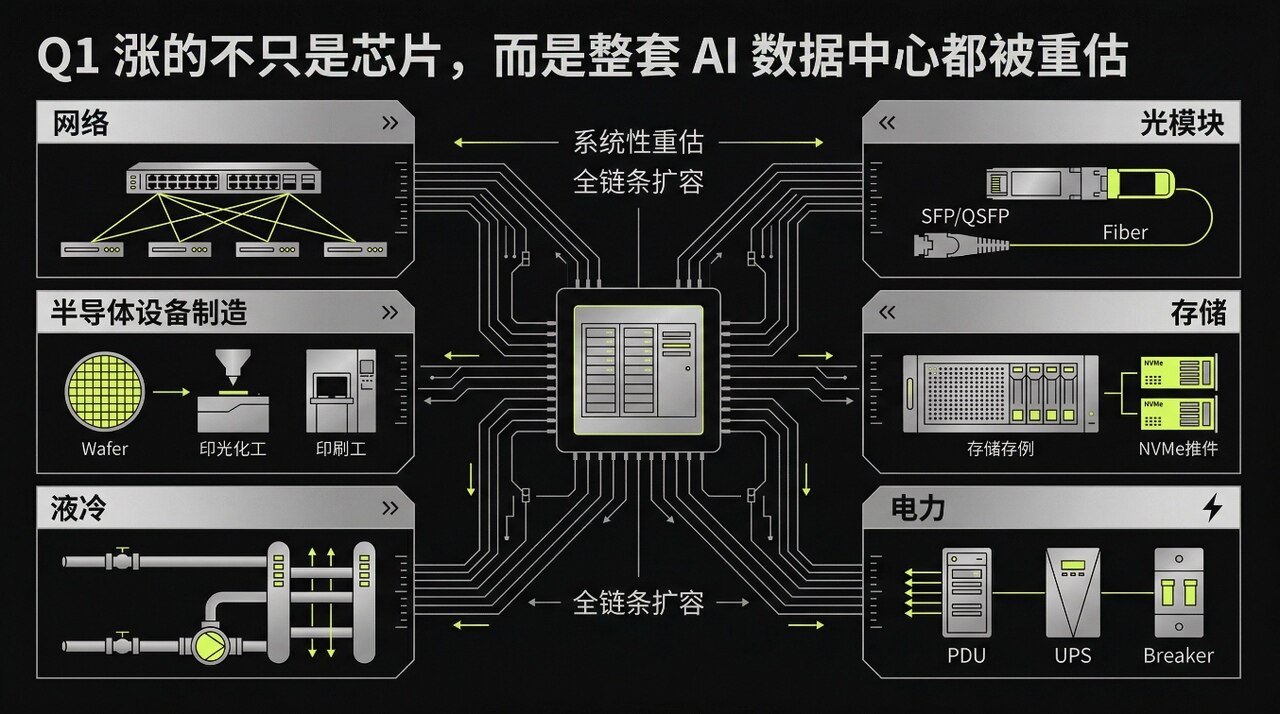

According to MSX Research Institute, the increase is not limited to a few GPU-related companies, but rather the entire data center ecosystem: there is a need to expand the machine room, increase bandwidth, supplement power supply, adopt liquid cooling, and push forward production capacity.

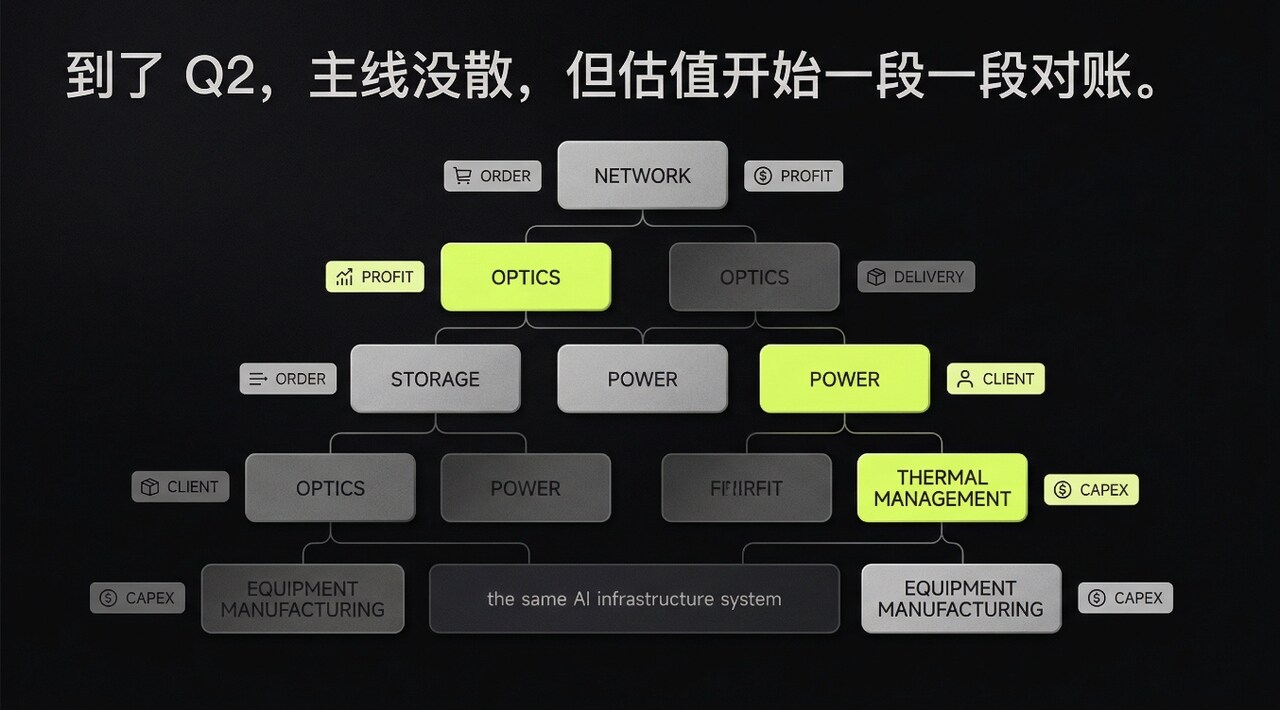

Thus, by Q2, the main lines have not changed, but the market rhythm will.

The sectors of networking, optics, storage, electricity, and equipment manufacturing are still within the main line, but the follow-up trends will not simply see an overall rise in valuations along the entire chain of “AI infrastructure”, but rather will focus more on orders, deliveries, profits, and whether capex can meet expectations.

From the performance range since Q2, the strongest elasticity has been seen in AEHR.M and AAOI.M; on a year-to-date basis, AAOI.M, SNDK.M, AEHR.M, and LITE.M have shown higher gains, clearly indicating a noticeable differentiation within the AI infrastructure chain.

1. What Was Bought in Q1 Was Not Just a Company, But an Entire Data Center Expansion

The most obvious point from the market trend in Q1 is that after securing funds, investors are no longer fixated on individual chips. Chips are indeed still the gateway, but the real capital expenditure is within the entire data center. As long as hyperscalers continue to increase capex, funds will follow down the path of “what is still needed for AI implementation”.

Looking at the asset pool on the MSX platform, this main line already has a clear trading mapping.

First to strengthen is networking. AI clusters are not about racing single-machine computing power; they compete on interconnectivity, bandwidth, and latency. ANET.M, as a leading switch manufacturer, naturally stands at the forefront, while CRDO.M and MRVL.M focus on the critical aspects around interconnectivity and accelerators. Names like AVGO.M which control both chip and connectivity capabilities will be pushed up by the market. Though CIEN.M is more oriented towards the outskirts of network infrastructure, as long as cross-room transmission and data transportation continue to increase, it cannot be completely overlooked. Once clusters grow larger, networking is no longer a supporting role but becomes a proper expenditure item.

Next comes optics. As AI training and reasoning move towards higher densities, optical modules and related devices become more prominently highlighted. LITE.M, COHR.M, AAOI.M, FN.M were repeatedly grouped together in Q1, with a direct logic: bandwidth needs to increase, interconnects need updates, and specifications need to elevate. In the previous phase, the market wasn't eager to differentiate winners and losers but instead raised valuations for the “upward specification” trend. Who is at 800G, who is at 1.6T, and who can handle more advanced deliveries were set aside for the time being.

Storage also got reclassified. MU.M, WDC.M, STX.M, SNDK.M were previously viewed more as cyclical stocks, but in Q1, funds began pushing them towards the “AI infrastructure chain”. The reason is easy to understand; as models grow larger, data increases, and training becomes more frequent, memory and storage are no longer limited to the outdated logic of PCs and smartphones. At least at the trading level, the market is willing to reassess such companies within the framework of “data center expansion”.

Further on is electricity and thermal management. VRT.M, as a typical beneficiary of “power supply + cabinets + support”, GEV.M, a name more oriented towards power equipment and grids, might not always be in the hottest positions in Q1, yet they were still lifted by funds. After all, while computing power can be crammed into the machine room, where the electricity comes from, how heat is dissipated, and whether deliveries can keep up must all be accounted for. Once the data center density increases, these questions cannot be escaped.

Equipment manufacturing did not fall behind either. LRCX.M, KLAC.M, AMAT.M, MKSI.M, TER.M, TSEM.M, AEHR.M in this line, have thus far captured expectations of “production expansion will continue to transmit”. Advanced processes, storage, packaging, yield management, production line automation, and testing and validation phases, once incorporated by the market into the framework of “AI production expansion”, will see valuations moving upwards.

So the trend of increase in Q1 was not led by one or two companies, but rather the entire chain was lifted together. The market first recognized one thing: data centers need to expand. The subsequent sectors of networking, optics, storage, electricity, thermal management, and equipment manufacturing have all been placed on the table.

2. By Q2, the Main Line Is Still Intact, But Valuations Will Start to Reconcile Segment by Segment

The issue in Q2 is not that the AI narrative suddenly vanished, but that the first round of “all segments together raised valuations” has already passed. There will still be increases, but they won’t be as orderly as before.

The networking and optical chains in Q1 were based on high bandwidth, interconnect upgrades, and cluster expansions. By Q2, these expectations will not disappear but will be broken down for analysis. Names like ANET.M with clearer customer bases and steadier product rhythms will be watched for the sustainability of order intensity; CRDO.M, MRVL.M, AVGO.M, which are positioned at key places around interconnectivity and computing power, will see the market start asking about customer structures, shipping rhythms, and revenue recognition; names like CIEN.M, leaning more towards network infrastructure, will look more at new orders, delivery cycles, and project advancements in Q2, making it unlikely to continue eating the premium along with the entire chain.

The optical chain is likely to widen the gap. Even though specifications upgrades are discussed, the underlying customers, capacities, yield rates, and price pressures vary significantly. LITE.M, COHR.M, AAOI.M, and FN.M could rise together in the previous stage, but by Q2, the market will start to analyze each on a case-by-case basis: who has more stable customers, who has smoother shipments, and who can retain profits. The prior phase relied on “everyone buying together as the optical chain”, while the latter phase focuses on who can solidify their accounts.

Storage, on the other hand, will be trickier. In Q1, the market was willing to assign more “AI-related” valuations to MU.M, WDC.M, STX.M, and SNDK.M, but by Q2, questions like: how firm is this demand, can profit recovery keep up, or is it just another cyclical rebound with a new facade will arise. As long as prices, units shipped, and profits can synchronize upwards, funds will continue to provide valuations; however, if reports don’t hold firm enough, retractions will be direct. The biggest fear for storage companies is being bought as AI infrastructure only to turn back into cyclical stocks.

For electricity, thermal management, and equipment manufacturing, Q2 may actually allow for a clearer view of the fundamentals. They may not always be at the hottest discussions, but at reconciliation points, delivery, expansion, order visibility, and how gross profits trend will be more evident. VRT.M's order and delivery rhythms, and GEV.M's positioning in the broader power equipment cycle will be compared to hyperscalers’ expansion plans. On the equipment manufacturing side, LRCX.M, KLAC.M, AMAT.M, MKSI.M, TER.M, TSEM.M, AEHR.M will also be closely monitored by the market: can AI production expansion continue to propagate downstream, and can testing, verification, production line rhythms, and final deliveries keep up, or will it be limited to just a few upstream investments.

Previously, investments were made collectively by sector; now, evaluations must be done company by company. The main line remains, but valuations will no longer move together.

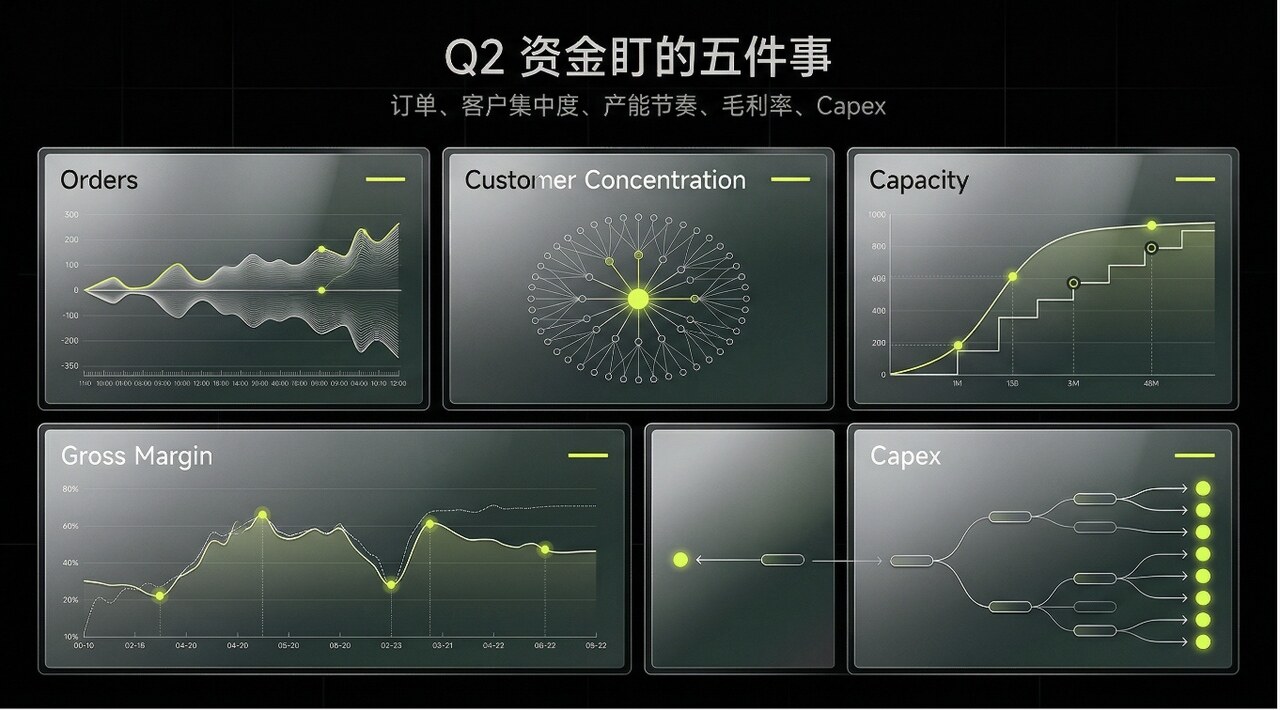

3. In Q2, Five Key Aspects of Focus Are to Pin High Expectations to Financial Reports

First, focus on orders. The networking chain typically is the first to be reconciled: are orders still piling up, are deliveries still accelerating, and has customer procurement shifted from trial orders to regular ones? A typical beneficiary like ANET.M will be repeatedly monitored for the sustainability of order strength; CRDO.M, MRVL.M, and AVGO.M, which are positioned around interconnectivity and computing power, will also be under watch for more visible projects and clearer shipment guidance.

Next, check on customer concentration. The optical chain especially cannot escape this issue. More concentrated customers lead to quicker increases in Q1; by Q2, if one major customer slows down, stock prices often react ahead of financial reports. For the group of LITE.M, COHR.M, AAOI.M, and FN.M, the market will care more about who the customers are, their proportion, and how the rhythm goes, rather than using one phrase “bandwidth upgrade” to smooth all fluctuations.

The third point is to look at production rhythms. Many companies talked about “strong demand” in Q1, but in Q2, investors are more concerned about “can you actually produce it, can you deliver it”. The optical chain looks at the ramp-up, while electricity and thermal management focus on delivery, and equipment manufacturing observes the rhythm of orders turning into shipments. Deliverable-focused names like VRT.M will often be revalued by the market at this stage: as long as delivery is steady, expectations will not easily dissipate. LRCX.M, KLAC.M, AMAT.M, MKSI.M, TER.M, TSEM.M, AEHR.M in this line will also be the same, demand must genuinely pass down, and ultimately must land atop the production line, testing, and deliveries.

The fourth aspect looks at gross margins. In Q1, when valuations were raised, the market was willing to set aside the profit statements; by Q2, it will begin to scrutinize. MU.M, WDC.M, STX.M, SNDK.M are the most typical examples: a rise in demand is one thing, but can profits keep up is another matter. Prices are up, but costs are also rising, or competition compresses profits back down, leading to an initial drop in valuations. The same goes for the optical and networking chains; an upgrade in specifications does not automatically equate to a rise in profits. Those who can convert higher-end shipments into higher gross margins will be more stable.

Finally, attention returns to the capital expenditures of hyperscalers. In Q1, the market defaults to “big companies will continue to invest”, while Q2 will heed more to “where they are investing, what they are prioritizing, and whether budgets have shifted”. As long as capex remains high, this chain still has potential; but should the structure of capex change, the order of beneficiaries will follow suit, leading to rapid differentiation. Training shifts towards reasoning, the rhythms of networking and optics will change; once the machine room expansion rhythm shifts, the ordering of electricity, thermal management, and equipment manufacturing will also adjust.

Overall, when capturing these sector rotation opportunities, the core is not in predictions, but in the ability to swiftly capitalize when signals emerge. Currently, the market is focusing on the aerospace sector, and MSX is running a Commercial Aerospace Trading Week, providing a solid entry point. For traders interested in participating in the 10,000 USDT reward pool and the sector, it also offers a practical opportunity to lower friction costs.

Conclusion

The rise in Q1 was led by the entire chain, while by Q2, the market will begin reconciling segment by segment. Networking, optics, storage, electricity, and equipment manufacturing will not move together anymore; whoever's orders land first, deliveries follow suit, and profits materialize first will have a better chance of solidifying valuations.

Reflecting on the tradable targets on the MSX platform, this main line already has a relatively complete observation framework, and MSX will continue to track the evolution of this main line and the rhythm of related targets.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。