整理:Macro_Lin

Recently, I read a special report published by the Bank of Korea (BoK) titled "Review of the Sustainability of the Global Semiconductor Boom." This report is quite special.

South Korea is a major exporter of memory chips, and the financial reports of Samsung and SK Hynix are, in a sense, the national economic reports of the BoK. When this central bank personally involves itself in seriously discussing how far this AI-driven semiconductor supercycle can go, the attitude itself is worth savoring. Sell-side research reports have their positions, and short reports have their emotions, but the tone throughout the BoK's report is that of a restrained central bank, with a much higher density of argument than emotional density.

Core Viewpoints

The Bank of Korea believes that the extent and duration of the supply-demand imbalance in the current storage cycle clearly exceed the historical three cycles, with expansion continuing uncertain until at least the first half of 2026. However, starting in 2027, five variables will together determine when the reversal will occur, with two of the most concerning signals already having appeared.

1. How This Cycle Differs from the Past Three

The BoK divides the semiconductor cycles since 2010 into four phases: the smartphone proliferation (2013 to 2015), cloud expansion (2017 to 2018), post-pandemic contactless (2020 to 2021), and the current AI diffusion (2024 to present).

The scripts of the past three cycles are the same. New technologies drive up demand, supply lags behind, after concentrated capacity expansion, supply exceeds demand, inventory accumulates, prices decline, and the cycle reverses. After 2017, this reversal point highly coincides with the inflection point of CAPEX from large American tech companies.

This cycle has three key differences.

First, demand growth is the fastest in history. With the explosive loading of AI accelerators, HBM is being driven by inference demand, leading to a synchronized expansion across all categories of DRAM.

Second, supply elasticity is the worst in history. HBM processes are complex and the capacity expansion cycle is long. Storage manufacturers have gone through the intense period from 2022 to 2023, becoming conservative in capacity expansion. General DRAM production lines are cut to produce more HBM, further exacerbating tension on general goods.

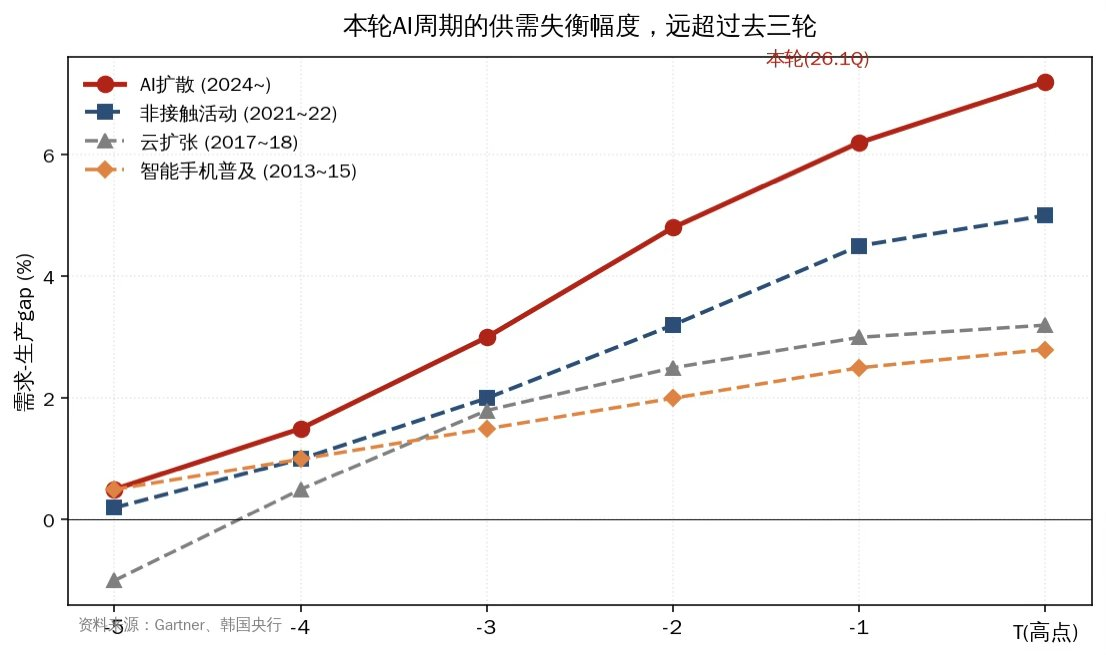

The third point is the outcome. The BoK created a crucial chart comparing the demand-production gap of the four cycles on one coordinate, showing that the imbalance in this cycle clearly exceeds that of the past three cycles. Both the inventory levels on the manufacturing side and the demand side for DRAM are decreasing, with no signs of accumulation.

Figure 1: Comparison of demand-production gaps in historical semiconductor cycles, with the current AI cycle significantly surpassing the past

2. Five Variables That Determine How Far the Cycle Can Go

The BoK provided a clear framework of five factors, three from the demand side and two from the supply side. I will discuss them in order of importance.

① Timing of profitability verification for AI investments. Currently, OpenAI and Anthropic are both operating at a loss, with market expectations for future dominance supporting valuations and investments. The BoK’s judgment is nuanced, the market’s focus will shift from securing territory to whether it can be profitable starting next year. Coupled with risks such as data center power bottlenecks, accelerated GPU depreciation, and underutilization, it will be challenging to maintain the current CAPEX growth rate.

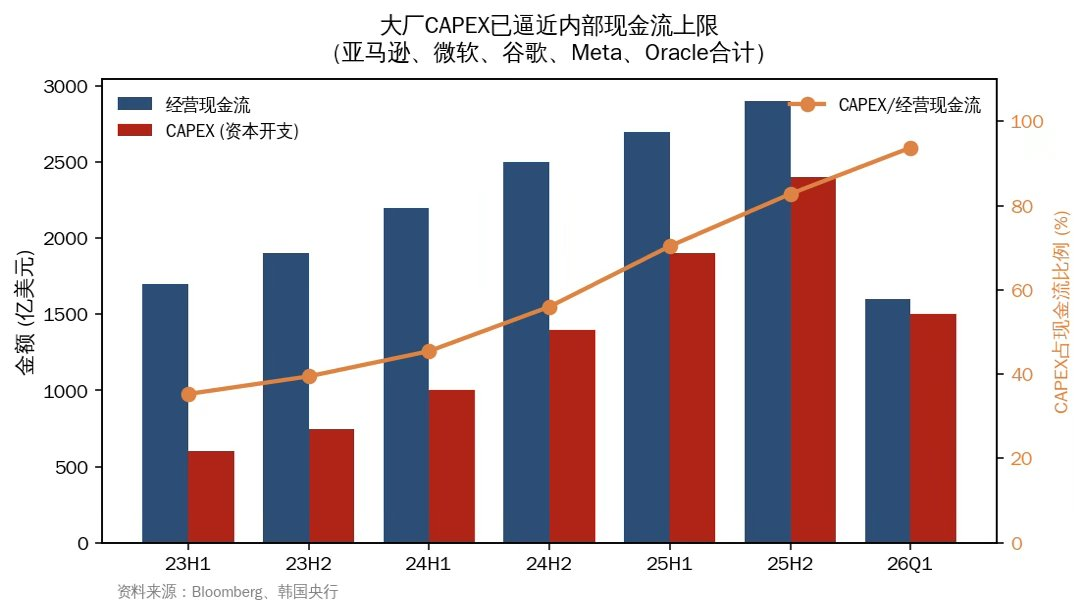

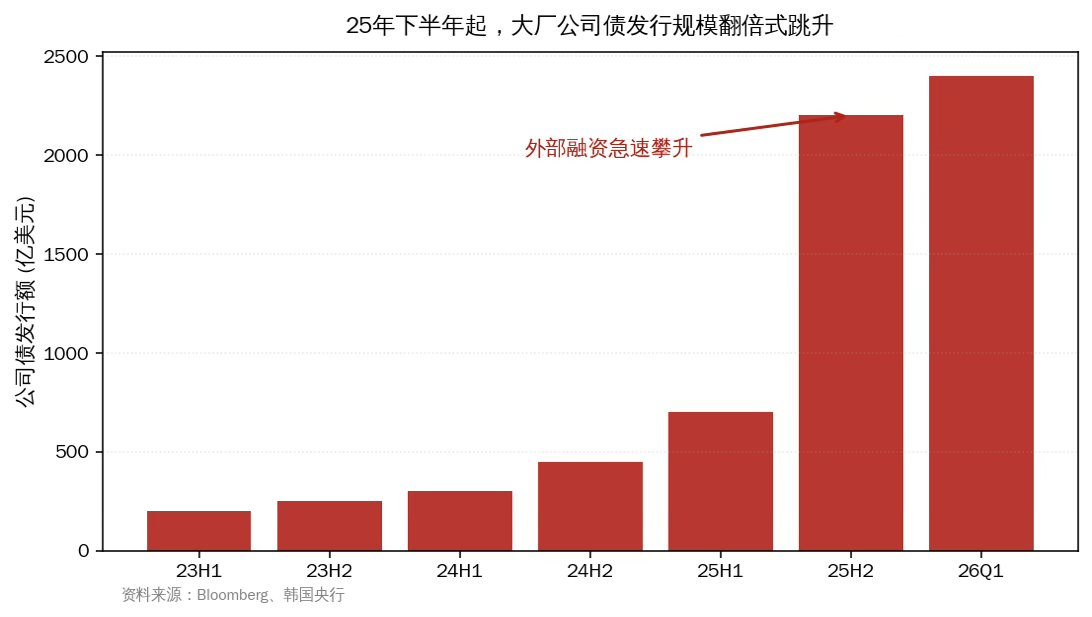

② Whether large companies can continue to raise funds. This section contains the most informative details of the entire report. The BoK explicitly compares the current situation to the telecom bubble of the late 1990s and points out a deteriorating fact, the internal cash flows of large companies can no longer support this level of CAPEX. Since the second half of last year, major companies have reduced buybacks and significantly issued corporate bonds, with some companies' CDS spreads widening.

Figure 2: Corporate operating cash flows are unable to cover CAPEX, with the ratio soaring from 25% to nearly 100%

Figure 3: The scale of corporate bond issuance surged from the second half of 2025, with external financing becoming a major supplement

What is even more concerning is the nature of the financing itself. Companies like Neocloud (for example, CoreWeave) are much smaller than the big companies but need to continually purchase GPUs and build AI data centers, with NVIDIA providing them with credit support to leverage sales of its GPUs. This structure is highly similar to the vendor financing provided by Cisco and Lucent to emerging telecom companies back then.

Another layer is off-balance-sheet financing. Meta's Hyperion Data Center uses SPVs and private credit to achieve $29.5 billion in liabilities that do not appear on Meta's balance sheet. Oracle's Stargate, with a scale of $66 billion, and xAI's Colossus, with $20 billion, both use similar structures. The BoK mentions a detail that in February to March 2026, institutions like Blue Owl, BlackRock, Morgan Stanley, and Cliffwater suspended redemptions of some private credit funds due to concerns over AI disruption. This is a crack.

③ Efficiency advancements of AI models. After DeepSeek, techniques like quantization, MoE, Mamba, NVIDIA CMX, and Google TurboQuant have rapidly emerged to save memory. The BoK admits that the bidirectional influence is uncertain. Enhancements in technical efficiency could either lower unit demand or, due to the Jevons Paradox, expand total demand. This section in the BoK's summary chart shows a bidirectional arrow, the only one of the five factors that cannot be directed.

④ The expansion speed of major storage manufacturers. This year, Samsung's P4 and SK Hynix's M15X have exhausted their existing cleanroom space, but it is still insufficient. The actual supply release window is in the second half of 2027. SK Hynix's Yongin and Micron's new plants will start production in H2 2027, and Samsung's P5 will start production in 2028. This is a hard constraint on supply that can be marked in the calendar.

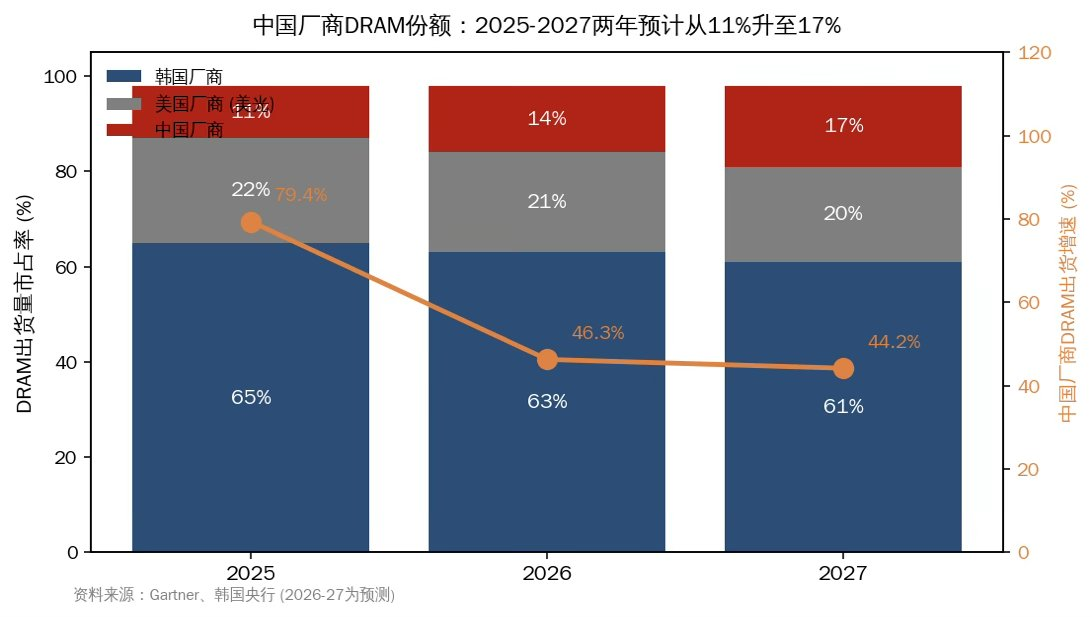

⑤ The pace of catch-up by Chinese manufacturers. The BoK assesses the technological gap between China and South Korea to be about four years, with both HBM and general DRAM lagging. Thus, the high-end pattern is unlikely to shake in the short term. However, one number worth noting is that the DRAM shipment share of Chinese manufacturers may rise from 10.5% in 2025 to 17% in 2027, with the growth rate in the next two years more than three times that of the major storage manufacturers. This share will press on general DRAM prices and accelerate the alleviation of the imbalance.

Figure 4: The share of Chinese manufacturers' DRAM rises from 11% to 17%, with shipment growth rates far exceeding those of major storage manufacturers

3. Regarding the Middle East War, the BoK's judgment is calmer than expected

Currently, there are no signs of delayed construction of data centers or a slowdown in storage supply. The AI investment cycle is led by large American companies, with 74% of data centers under construction located in the Americas, and the correlation between the global economy and semiconductors has significantly weakened over the past two years.

However, the BoK listed several potential transmission chains. Rising oil prices increase data center operating costs, tightening financial conditions elevate the financing difficulty for large companies, and disruptions in the supply of raw materials and equipment (bromine, helium) in the Middle East would affect storage if Taiwan's energy issues impact system chip production. The most direct backlash is on the consumer side, as Gartner has already predicted that in 2026, due to rising storage prices, PC shipments will decline by 10.4% year-on-year, and smartphone shipments will decline by 8.4%.

4. Putting Together the Timeline

The BoK concludes with a colored matrix visualizing the intensity of the impact of the five factors across the years 2026, 2027, and 2028. I will translate the essence of this table into a narrative timeline.

In 2026, the demand-dominant, supply-constrained pattern continues. This is the most certain year.

In 2027, contradictions begin to accumulate. Pressure on large companies’ financing rises, Chinese production accelerates, new plants have yet to be put into production, but the weaknesses in the financing are already exposed.

In 2028, Samsung's P5, SK Hynix's Yongin, and Micron's new plants will release significant supply, thereby substantially amplifying risks on the supply side.

A Bit of Extension

The truly interesting aspect of this report lies in its narrative style. A central bank rooted in storage does not overly praise its domestic industry; it dedicates much space to discussing the fragility of financing structures, the bidirectional uncertainties of technological efficiency, and the nuanced inflection point in 2027 on the timeline. This restraint itself speaks to an attitude.

The comparison with the telecom bubble is a part of the report I read several times. The script back then was, robust early demand alongside competitive capacity expansion, together with a technology innovation that exceeded expectations (WDM wave division multiplexing), ultimately catapulting the industry into rapid oversupply. In today’s AI industry, all three conditions are present; the only difference is that the critical technology akin to WDM has yet to appear.

When domestic investors focus on the storage industry chain, their attention habitually falls on supply-side matters like HBM yield and CXMT progress. The BoK’s report brings the focus back to the demand side, more specifically, the sustainability of financing in the AI industry. Vendor financing from Neocloud, off-balance-sheet leverage from SPVs, and redemption interruptions for private credit funds—these signals should be monitored more closely than any expansion timeline.

At least until the first half of 2026, the story continues. What happens after that will depend on how the five variables above play out.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。