Author: Chloe, ChainCatcher

On April 8, 2026, Morgan Stanley's spot Bitcoin ETF (code: MSBT) officially began trading on the NYSE Arca, becoming the first spot Bitcoin ETF issued directly by a major bank in the United States, with an annual fee rate of 0.14%, setting a new record for the lowest market fee.

This move is not just a simple product launch; it symbolizes that liquidity in the cryptocurrency market is undergoing a restructuring. As major giants like BlackRock and Fidelity join forces to carve up the trillion-dollar ETF market, the power of Wall Street and compliance endorsements are fully engaged, creating real survival pressure not on Bitcoin holders, but on native crypto exchanges that are losing liquidity pricing power.

What is the competitive logic behind these five giants? Is Morgan Stanley's low-price strategy sufficient to change the overall landscape? And how can perpetual contracts become the last fortress for native crypto exchanges in this war of attrition?

Trillion-Dollar Market: Cryptocurrency ETFs are Developing Toward High Concentration

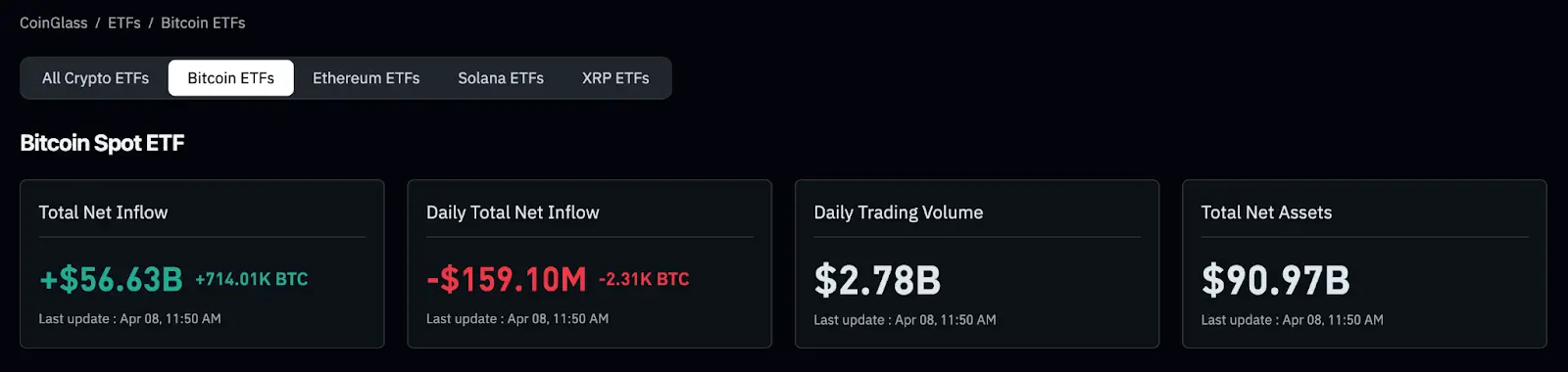

As of 2026, approximately 25 asset management companies in the United States are directly involved in cryptocurrency products (including ETFs, trusts, and funds), resulting in extremely high market concentration. The total assets under management (AUM) of the five major crypto asset management giants have exceeded the threshold of one hundred billion dollars, with the spot Bitcoin ETF exceeding 90 billion dollars. Compared to the initial stage of just 56 billion dollars in 2024, the growth rate over two years reached 1.6 times.

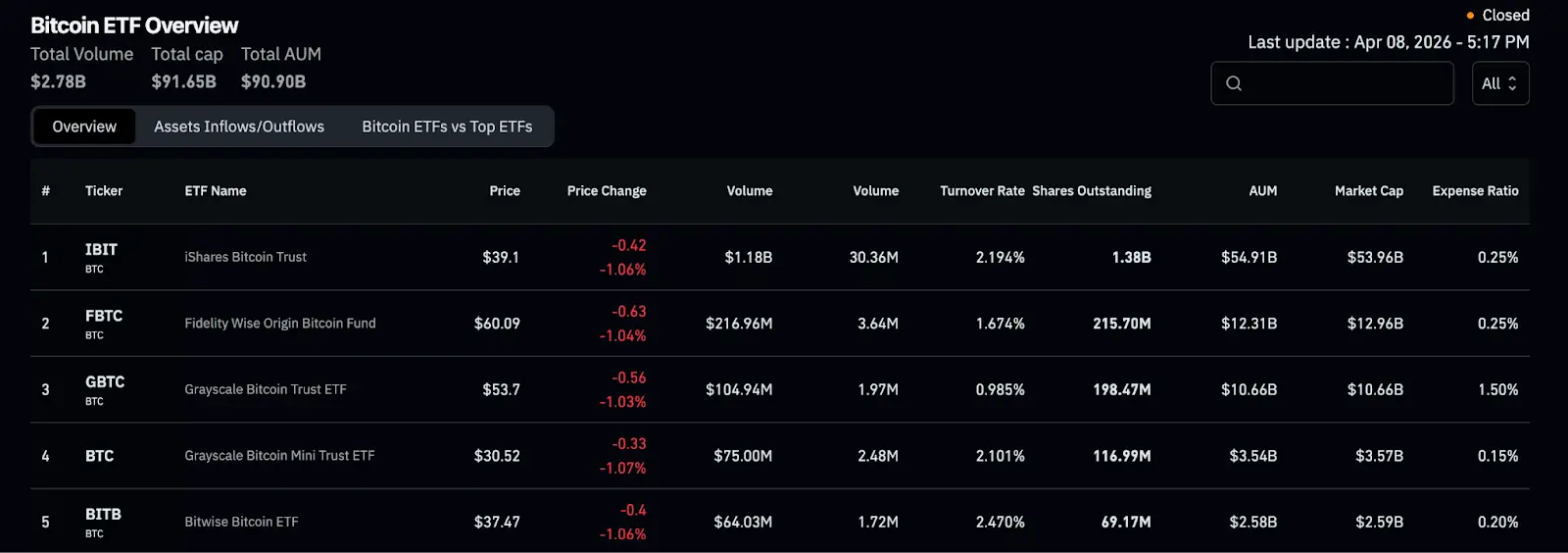

In the competitive landscape, BlackRock's iShares Bitcoin Trust (IBIT) has shown absolute dominance, for example, with IBIT (BlackRock) leading the pack with 54.9 billion dollars in AUM, attracting 8.4 billion dollars in net inflows in a single quarter, capturing 45% of the total market inflow; FBTC (Fidelity) follows in second place with 12.3 billion dollars, and GBTC (Grayscale) ranks third with 10.6 billion dollars.

From the above data, it is clear that when institutional capital decides to allocate Bitcoin exposure, BlackRock is almost the only choice. This is not simply the result of a rate war; it is the Matthew effect created by the combination of brand credibility, deep liquidity, and strong distribution channels. As the largest ETF issuer globally, BlackRock has created institutional-level average daily trading volumes and extremely narrow bid-ask spreads for IBIT. For latecomers, even if they offer concessions in fees, it is challenging to surpass this moat built by liquidity and trust in a short period.

Five Giants, Five Strategic Logics

On the surface, five major asset management companies are competing for the same pie, but upon closer examination of their competitive strategies, it reveals distinctly different battlefield divisions.

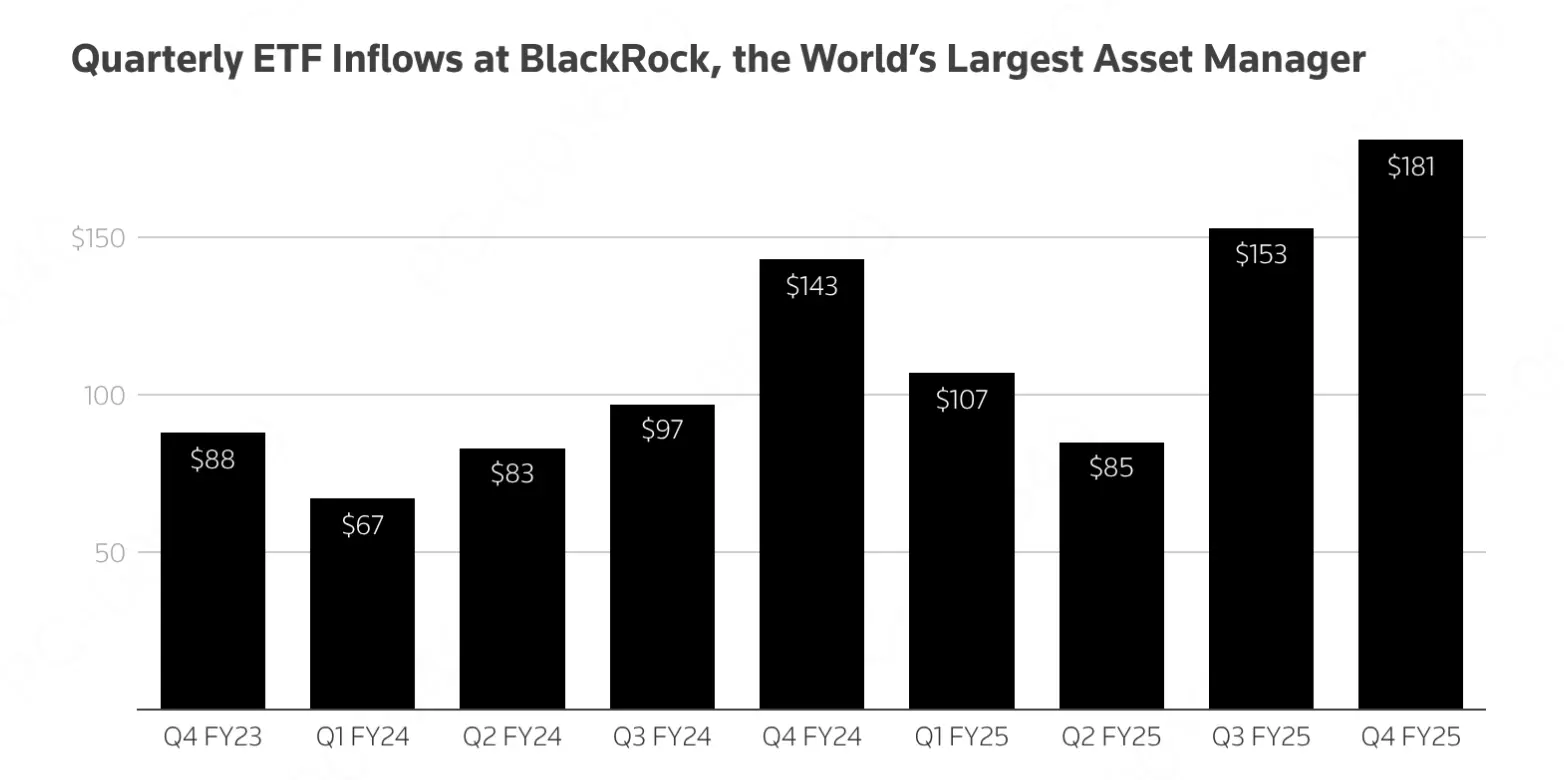

BlackRock's logic is the most straightforward: scale equals moat. With 14 trillion dollars in global AUM and deep distribution agreements with major brokerage platforms, IBIT naturally occupies the "preferred list" of institutional investors. Before the fee war began, BlackRock had already locked in the largest liquidity pool in the market, giving it an exclusive advantage that no native cryptocurrency competitors could replicate.

Fidelity takes a different route: institutional self-custody. Although its fee rate is 0.25%, the same as IBIT, FBTC is directly managed by Fidelity Digital Assets for Bitcoin custody. Compared to the third-party model led by Coinbase, this "full-stack" architecture eliminates reliance on third-party cryptocurrency exchanges, providing strong trust for insurance companies or pension funds that prioritize compliance and asset security. Additionally, to further enhance security, Fidelity introduced BitGo as a co-custodian in February 2026 to implement multiple backups.

Grayscale's advantage lies in its historical depth. Since its inception in 2013 with the Bitcoin Trust, Grayscale has accumulated a watchlist of over 36 crypto assets and an extensive network of institutional relationships. Although GBTC faced massive fund outflows during the early stages of its ETF transition, with net outflows reaching 1.2 billion dollars in the first quarter of 2026, this has significantly narrowed compared to the peak in 2024. Grayscale's market value is based on breadth rather than depth: it is currently the only traditional asset management company that can provide diversified cryptocurrency products such as Ethereum, Solana, and DeFi themes.

Bitwise focuses on differentiated advantages; its Solana staking ETF (BSOL) accumulated 500 million dollars in AUM within just 18 days. Using staking yield mechanisms as a weapon, it precisely targets institutional clients seeking alternatives to Bitcoin exposure, which is not merely asset replication but rather packaging on-chain native yield logic into compliant and distributable traditional financial products. To date, Bitwise controls about 70% of Solana ETF's total assets under management, accounting for 545 million dollars of the total scale of 775 million dollars.

Galaxy Digital has chosen to partner with State Street to launch actively managed ETFs, providing comprehensive institutional services beyond passive index products. This strategy targets institutions that need portfolio advice and risk hedging designs rather than simply exposure needs.

In summary, the competitive landscape has expanded from a focus on fees to multiple dimensions including asset breadth, custodial asset security, and the returns of investment targets, and it is now a multi-dimensional competitive environment.

Traditional Large Bank Morgan Stanley Enters Bitcoin ETF

On April 8, 2026, Morgan Stanley's Bitcoin Trust (MSBT) began trading on the NYSE Arca, with an annual fee rate of only 0.14%, becoming the first large bank in the United States to issue a spot Bitcoin ETF in its own name, and also the current lowest fee Bitcoin ETF product on the market.

It is worth mentioning that the 0.14% fee is lower than Grayscale Bitcoin Mini Trust's 0.15% and significantly lower than BlackRock's IBIT at 0.25%, instantly making it the lowest fee spot Bitcoin ETF in the United States. For institutional investors holding long positions, the 11 basis point difference will translate into millions to hundreds of millions of dollars in cost savings annually under scale effects.

However, the fee rate is merely a surface issue; Morgan Stanley's true core weapon is its asymmetric advantage in its distribution network, possessing approximately 16,000 financial advisors managing over 6.2 trillion dollars in client assets. When these advisors actively recommend MSBT, the competitive logic is entirely different from other ETFs; it does not compete side by side with several products on brokerage platforms but reaches clients directly through high-sticking trust relationships.

Some analysts have pointed out that if clients of Morgan Stanley's wealth management platform allocate just 2% into Bitcoin, this could generate approximately 160 billion dollars in potential demand, a figure that exceeds the current total AUM of the entire spot Bitcoin ETF market.

On the other hand, MSBT is not acting in isolation, but is part of a series of initiatives. Morgan Stanley also plans to collaborate with E*Trade and Zerohash to launch retail direct trading services for Bitcoin, Ethereum, and Solana in the first half of 2026; in addition to the submitted application for a national trust bank subsidiary (Morgan Stanley Digital Trust), covering custodial, trading, and staking services — this complete layout of the financial infrastructure for crypto assets could pose a significant threat to the currently largest player, BlackRock.

The Dilemma of Exchanges and Their Last Differentiated Weapon

Furthermore, Wall Street's entry is exerting "customer dilution" pressure on native cryptocurrency exchanges. This is not merely an issue of a single competitor appearing, but rather the migration of the entire institutional entrance.

The rise of spot Bitcoin ETFs means institutional investors no longer need to open exchange accounts, manage private keys, or go through complex KYC processes; they can simply click to buy on existing traditional brokerage platforms. The fiat currency channels of Coinbase, Kraken, and Binance were once the only bridges for institutions to access cryptocurrency assets, but now this bridge has been completely bypassed by the ETF channels of BlackRock and Fidelity.

In this dilemma of stock competition, the only moat remaining for native exchanges that cannot be easily replicated is perpetual contracts, which are a unique financial innovation in the crypto market. They have no expiration date, maintain an anchor to spot prices through a funding rate mechanism, allow for high leverage bilateral trading, and the market never closes, operating 24/7.

According to Coinperps, derivatives dominate the structure of the entire cryptocurrency market, with perpetual contracts and futures accounting for as much as 77% of the total trading volume of 79 trillion dollars in the past year, indicating that the contribution of the spot business to native exchanges is waning.

The core advantage of perpetual contracts is the potential for large returns from small investments; for skilled traders, this is a trading density that no traditional ETF can provide. Institutions like BlackRock provide a sense of security for holding Bitcoin, whereas perpetual contracts from original cryptocurrency exchanges offer active traders a leveraged tool for profiting from cryptocurrency volatility. These are two entirely different demand markets, with the latter still being the absolute home ground for native exchanges.

An Ongoing Structural Restructuring

The essence of this competition is a slow but irreversible boundary redefining between traditional financial order and the native crypto ecosystem.

Wall Street brings credibility, distribution channels, and the scale effect of institutional capital, but it cannot reach leveraged traders, on-chain users, or those who view cryptocurrency trading as a lifestyle. The survival of native exchanges depends on deepening the ecological density of perpetual contracts, on-chain derivatives, and the next generation of financial infrastructures beyond the lost spot shares.

Jed Finn, head of Morgan Stanley's wealth management department, has openly stated that the direct crypto trading launched by E*Trade is "just the tip of the iceberg," with follow-up plans covering custody, wallets, and tokenized assets. Thus, it can be seen that when even the most conservative traditional financial institutions start using phrases like "the tip of the iceberg," it signifies that not only is a single bank's ambition at stake, but the ceiling for the entire sector is being redefined.

Today's listing of MSBT marks the latest symbolic node in this restructuring, as the influx of institutions is accelerating the embrace of cryptocurrency by traditional finance, but also diluting the liquidity of the native market. The real question is not which draws all the winnings, but how the future landscape of the cryptocurrency market will change once the boundaries disappear.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。