Original author: Axis

Original translation: AididiaoJP, Foresight News

On March 15, South Korea's financial regulatory agency implemented a six-month suspension of part of the operations of the country's second-largest cryptocurrency exchange, Bithumb. English media reported this event as a routine compliance case involving anti-money laundering enforcement and regulatory adjustment. However, most of these reports overlooked more important underlying information.

In fact, this event is evolving into a market structure event occurring within one of the deepest liquidity pools supported by fiat currency in an on-chain financial system, with impacts far exceeding South Korea. Upbit and Bithumb collectively handle about 96% of the cryptocurrency trading volume in South Korea. The suspension of Bithumb is not only reshaping the operational landscape of the domestic market but also undermining the quality of signals that this market has conveyed to global traders for years.

Overall, cryptocurrency users in South Korea are active traders, but the system they are in is shaped by capital controls, high concentration of exchanges, and persistent language barriers. The combined effect of these three factors is that information related to prices often appears in South Korea before it is reflected in global markets, resulting in a temporary window of market desynchronization.

The reason global traders fail to receive information in a timely manner is structural rather than coincidental

South Korea is not an edge market but rather one of the most important markets globally for understanding where on-chain opportunities arise. The South Korean won is the second largest fiat currency by trading volume in global cryptocurrency trading, with a trading volume of about $663 billion year-to-date, accounting for nearly 30% of total global fiat-to-cryptocurrency trading. Nearly one-third of South Korean adults hold digital assets, a ratio that is double that of the United States.

The current South Korean government was elected in June 2025, and its campaign platform is one of the clearest in political history in supporting cryptocurrencies. Since taking office, nearly half of the best-performing 30 stocks in the South Korean composite stock price index have been related to digital assets. The stock market rapidly digested this signal, while the vast majority of the cryptocurrency community did not.

This is not a one-off market misalignment. Political and regulatory dynamics in South Korea often first appear in Korean-language media and local crypto Twitter, then influence the KRW trading pairs on Upbit and Bithumb, and are only reported by English media several hours to days later. The reverse process also exists: global macro changes originating from the English market often take a long time to be priced into local trading pairs. By the time the information is translated, the initial price reaction has usually already occurred.

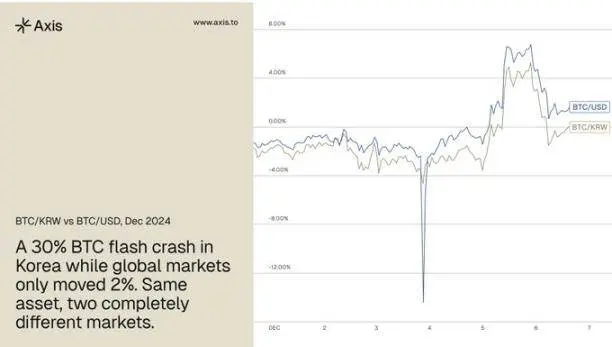

The clearest record occurred on December 3, 2024, when South Korean President Yoon Suk-yeol announced a state of emergency. Bitcoin's price in Korea fell by about 30% within the day, while the global price only dropped by about 2%, a difference of 28 percentage points, entirely caused by domestic political shocks. The total value of this sell-off was about $33.3 billion, and the South Korean market recorded the highest trading volume globally at one point, making this event a classic example of the typical misalignment of the South Korean market.

At that time, buying liquidity quickly shrank, and selling pressure continued to accumulate, with the sell-off pressure entirely concentrated on KRW trading pairs. Even stablecoins were de-pegged, with USDT trading at one point as low as $0.75 on Korean exchanges, while Bitcoin and altcoins were priced at a discount of 50% or more compared to global prices. Domestic users believed they were facing the last available liquidity to sell, thus they continued to sell at market prices despite the global price being almost unaffected. On-chain data showed that arbitrageurs sought to narrow the price spread through transfers of millions of USDT per transaction. The frontend systems of mainstream exchanges collapsed under the flow pressure, and retail users could not log in to buy discounted assets, only traders using APIs could execute trades during that window. From many standards, this was a significant and highly tradable event, but the window closed within hours.

The Bithumb suspension event follows the same pattern. This event has been fermenting in Korean information streams for weeks, but most English traders only learned of it now.

"Kimchi premium" is widely tracked but often misunderstood

For traders without Korean information sources, the kimchi premium has long been the most direct proxy indicator for understanding the dynamics of the Korean market. This premium measures the gap between the cryptocurrency prices quoted in KRW and the global prices quoted in USD. For this reason, experienced traders have long paid attention to KRW trading volumes. The Korean spot altcoin market is one of the highest trading volume markets globally and has historically been a reliable early indicator of broader market movements.

The problem is that most traders misinterpret this signal. The kimchi premium is commonly viewed as a measure of retail sentiment among Korean traders. While this is indeed part of it, the premium also reflects the intensity of structural capital pressures in a market where cross-border capital flows face regulatory friction. When this friction intensifies, price misalignments tend to expand.

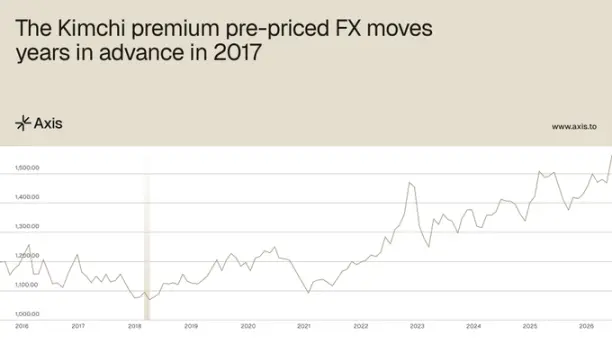

Historical records clearly illustrate this. As early as 2017, when the USD/KRW exchange rate was around 1060, the kimchi premium peaked at around 40%, which meant an effective USDT/KRW exchange rate of approximately 1480. Then, in December 2024, the actual USD/KRW exchange rate broke through 1480. The kimchi premium had priced in this forex change years earlier, and this information was encoded in publicly visible data; however, it needed to be interpreted in conjunction with Korean market information streams.

A persistent characteristic is that the kimchi premium does not naturally go to zero. Research indicates that as long as capital controls persist, the kimchi premium for Bitcoin will maintain a structural non-zero lower limit of about 1.24%. This means that when the premium compresses to that level, it often reflects changes in underlying capital pressures rather than simple normalization. In 2025, after periods when the premium was close to zero, Bitcoin recorded positive returns both over a week and a month: the average return over seven days was 1.7%, and the average return over thirty days was 6.2%. For traders, the important signal lies not in the absolute level of the kimchi premium but in its trend over time.

The Bithumb suspension event makes market misalignment in South Korea harder to anticipate, thus creating more asymmetry

The effectiveness of the kimchi premium as a signal depends on how price discovery occurs between various exchanges in South Korea. When multiple trading venues compete to price the same capital flows, the resulting price differentials often carry more information. As liquidity becomes more concentrated, this clarity starts to decline. Therefore, the suspension of Bithumb is removing the competitive price discovery mechanism that the premium relies upon.

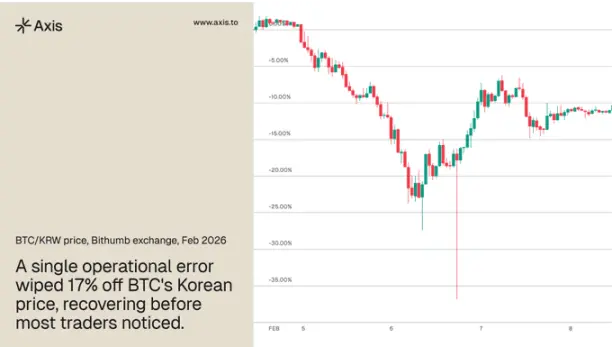

After the announcement was made, capital rapidly migrated to Upbit, further deepening the concentration. In February 2026, Bithumb experienced an operational error, mistakenly crediting users' accounts with 620,000 bitcoins, resulting in a 17% flash crash in the BTC/KRW trading pair, which was only later corrected. This event vividly illustrates what happens when price discovery relies on trading venues operating under single pressure.

The degradation of the premium does not mean that misalignment in the South Korean market ceases to occur; rather, it means that these misalignments become harder to predict before they appear, thus widening the information gap between participants who monitor the South Korean market directly and those who rely on English reporting.

At the same time, the underlying conditions that create these misalignments are becoming more severe. In 2025, under strict trading rules, $110 billion worth of cryptocurrencies flowed out of South Korea. Under the leadership of the new government, capital that had been structurally squeezed in the past is being reintroduced through new institutional channels, while the trading infrastructure relied upon by retail capital flows is being tightened simultaneously. Historically, this policy differentiation has been a precursor to the most severe and brief misalignments that the market has produced.

The structure of the South Korean market creates recurring information asymmetries for global traders

The kimchi premium is not a unique isolated phenomenon of the South Korean market. It is one of the most widely observed examples of a mechanism that operates to some extent in every capital-controlled market where cryptocurrency has evolved into parallel financial channels. The state of emergency in December 2024 and the Bithumb suspension event illustrate the same dynamics. Misalignments arise quickly in this market, rewarding participants with the right information sources, while disappearing before the rest of the market can catch up.

Traders who acted on December 3 did not do so because they were faster or smarter, but because they had been monitoring the correct signals and understood how South Korean political events mapped onto the price mechanisms at the exchange level, while the broader market was still unaware of what was happening.

As stablecoin infrastructure deepens globally, more markets will produce the type of capital pressure signals that South Korea has been releasing for the past decade. The challenge lies not in identifying the existence of these signals, but in establishing the infrastructure and discipline necessary to continuously capture them.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。