On Friday night, the US stock market and CME futures closed one after another, and information that could affect the market continued to pour in.

A trader stared at the screen, with three layers of judgment in his mind: he felt that there would be news of war brewing over the weekend, the probability of BTC going down first and then up was underestimated; he thought that the results of the next Federal Reserve decision had not been priced in; he also wanted to buy a weekend gap insurance for his crude oil or precious metals positions.

The trouble is, these three things often need to be done in three different places. Betting on long and short positions at the contract exchange, betting on events at prediction markets, and completing hedges at the options exchange, with margins also split into three parts. Cognition is clearly a whole, but positions are fragmented.

Hyperliquid's new market framework HIP-4 solves this fragmentation.

What is HIP-4?

HIP-4 turns the "outcome" itself into a tradeable standardized asset, allowing judgments such as "will a certain event happen" and "will a certain price reach a certain position at a certain time" to enter Hyperliquid's trading system in the form of standardized assets. It launched the Hyperliquid testnet on February 2.

A community member recently reverse-engineered the core contract of HIP-4 based on the contracts already deployed on the testnet, allowing us to preview its structure before the mainnet launch.

The simulated HIP-4 frontend based on the testnet contract by the community

HIP-4 adopts a dual-layer structure. Transactions occur in HyperCore, while fund custody, prize pool management, and partial settlement take place in HyperEVM. The former is responsible for high-frequency matching, while the latter handles the more complex contract logic of prediction markets, with clear divisions of labor.

Through HIP-4, abstract "events" can be "transposed" into real tradable assets.

For example, if someone opens a market for "who will win the 100-meter sprint," with event ID 9 and outcome 0 representing "Hypurr wins," then this outcome will be mapped to the "#90" token on HyperCore, traded on the order book. Traders buy and sell it just like trading a spot asset.

For markets like "Will BTC touch a certain price within 15 minutes," which are similar to options, settlement will occur directly in HyperCore based on real-time price data at expiration, without the need for external oracles.

The settlement rules for event contracts like "who will win the 100-meter sprint" are not yet clear.

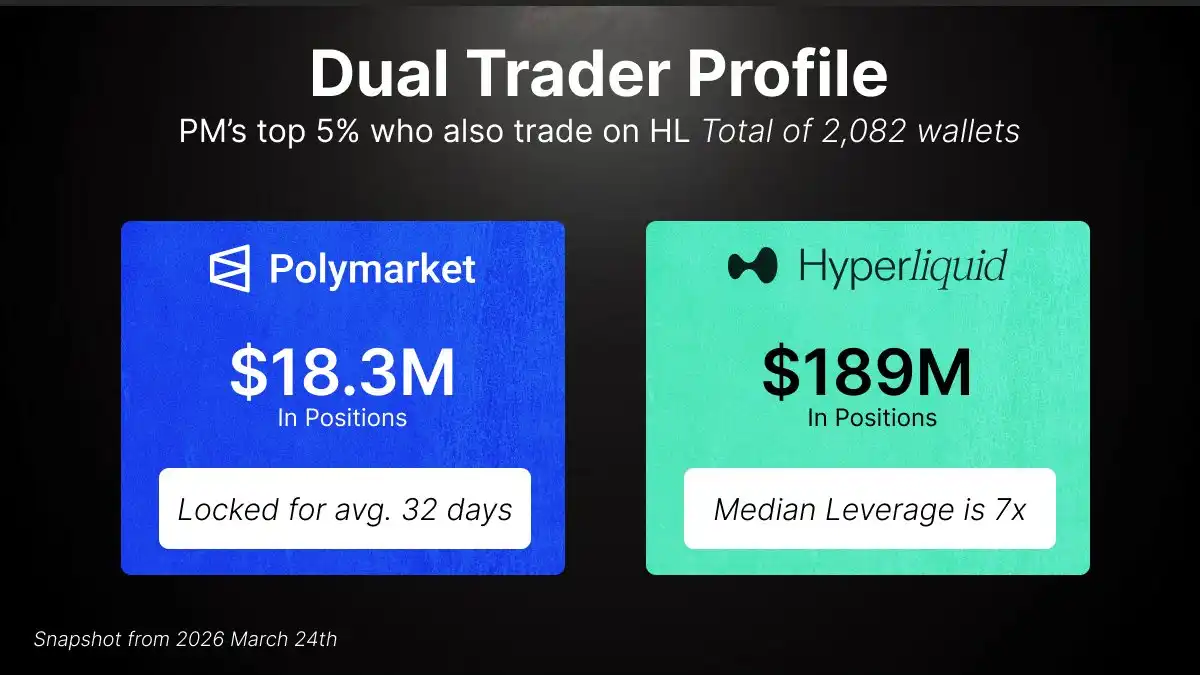

User Profile Overlapping with Polymarket

A study reviewed nearly 15,000 active Polymarket addresses and found that among top traders, there is a group of people who are already active on Hyperliquid as well.

This overlapping group of users contributed approximately $1.43 billion in trading volume on Polymarket, while managing roughly $189 million in contract positions on Hyperliquid, with about $29 million in margin usage. The balance of their Hyperliquid accounts is nearly evenly distributed between long and short positions, mainly trading mainstream assets like BTC and ETH; on Polymarket, they tend to hold positions in long-term events such as elections and Federal Reserve decisions. This indicates that this is a group of typical mature traders.

Today, these two positions are still lying in two isolated systems. Approximately $18.3 million in prediction market holdings cannot enter the contract margin system. Based on these overlapping users’ average leverage of about 7 times on Hyperliquid, it theoretically corresponds to over $120 million in additional trading capacity.

Aiming at the Weakness of TradFi, New Imagination Space for On-Chain Finance

HIP-4's greater imagination lies in its composability.

The community has outlined several potential new products:

Weekend gap options: Traditional markets have a long void period between Friday’s close and Sunday’s open; HIP-4 can turn this void into a weekend gap option. Traders holding positions related to crude oil, silver, or stocks in HIP-3, worried about a sudden gap before Monday's market opens, can buy an option that hedges based on the difference between Friday’s closing price and Sunday’s opening price.

Internal and external pricing deviations: Compensation for the maximum deviation between the internal pricing of HIP-3 exchange and the external oracle price, hedging against liquidation risks.

Funding rate options: Allowing traders to hedge negative funding rates.

These structured tools are precisely what sets HIP-4 apart from traditional prediction markets. The latter often lacks natural opposing orders, with markets primarily led by insider traders, and insider information continuously extracting profits from uninformed retail investors and market makers.

In contrast, HIP-4’s structured products have inherent hedging needs, not just carrying a betting function. The pricing logic, liquidity quality, and market depth of market makers will elevate to another level.

Cognition has never been linear, and positions should not be either.

The same set of accounts, the same set of margins, and the same settlement system—HIP-4 brings Hyperliquid one step closer to the vision of being the "House of All Finance".

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。