Author: Jae, PANews

When the night sky of Tehran was torn apart by flames, Wall Street traders were still asleep.

On the first weekend of March, most people's mobile phones were buzzed with the same news: the United States launched an attack across Iran, and its supreme leader Khamenei was killed.

For traditional financial markets, this was the worst timing: Sunday, the market was closed, and trading was impossible.

The impact of the war, even if delayed until Monday's opening, still triggered severe turbulence. Crude oil futures at the Chicago Mercantile Exchange (CME) triggered a circuit breaker at the moment of opening, resulting in a trading delay. Brent crude and WTI crude both surged over 10% on the day.

However, war does not take a holiday.

While global capital was anxiously waiting in a "pricing blind spot" due to trading hour restrictions, the decentralized trading platform Hyperliquid completed the early pricing of this crisis with 24-hour uninterrupted candlestick charts, and its protocol token HYPE rose against the current by 25% during this severe downturn of the crypto market.

This was not a coincidence but a battle over the "pricing power" of "who calls the shots."

Traditional markets unable to cope with the "weekend black swan," pricing power shifted on-chain

On the morning of March 1, a military operation codenamed "Epic Fury" and "Roaring Lion" ripped apart the calm in the Middle East.

Explosions were heard in strategic strongholds in Iran like Tehran. Local media subsequently confirmed: Iran's supreme leader Khamenei was killed in the airstrike. The Revolutionary Guard immediately entered a wartime state and issued a warning capable of shaking the global energy market: if Iran's oil facilities were damaged, the energy infrastructure of the entire oil-producing region in the Middle East would be turned to ruins.

The Strait of Hormuz, which carries 20% of global oil transport, also fell into paralysis, with the speed of tankers in the waters dropping to nearly zero, and shipping traffic almost stagnant.

However, it was Sunday. The doors of the exchanges in New York, London, and Hong Kong were tightly closed.

Investors could only watch helplessly as risks continued to accumulate, unable to hedge or exit. This meant that, despite the global digesting of the profound impacts of the attack on Iran, the market price anchor was inoperative.

Faced with the smoke over Tehran, investors could not hedge risks in traditional markets. This interruption in pricing not only led to the accumulation of risks but also resulted in huge price gaps when the market opened on Monday, forcing many investors to exit at extreme prices.

For a long time, the pricing power of global assets has been in the hands of traditional exchanges, but the Iranian crisis exposed the most fatal weakness of this system: it cannot cope with "weekend black swans."

At the same time, another system was operating smoothly.

Within the first 24 hours of the escalation of the Iranian situation, Hyperliquid’s order book had completed several rounds of price discovery for oil perpetual contracts, reflecting the market's expectations for the blockade of the Strait of Hormuz first.

Former Credit Suisse CIO Iggy Ioppe pointed out that the on-chain market bore nearly 100% of the public price discovery function over the weekend, and usually, when the futures market reopens, the prices tend to align with the trends of the on-chain market.

While Wall Street was still calculating profits and losses, on-chain traders had already priced the blockade of the Strait of Hormuz with real money.

The price discovery mechanism is undergoing a structural shift: from a time-limited traditional market to a 24/7 uninterrupted on-chain protocol.

This is not a theoretical deduction, but a result of capital voting with its feet.

According to CoinGecko statistics, the trading volume of Perp DEX (decentralized perpetual contract exchanges) surged 346% year-on-year to $6.7 trillion in 2025. Perp DEX's open interest soared 229.6%, while the open interest of CEX (centralized exchanges) significantly dropped by 20.8% during the same period.

PANews believes that this migration of capital is driven not only by the pursuit of asset ownership but also by a rational choice for pricing efficiency.

Blockworks researcher Shaunda Devens once pointed out that Hyperliquid achieved the best liquidity for buy-sell quotes in the crypto market. This depth means that when macro shocks occur, the signals on Hyperliquid will be transmitted faster than those on CEX.

According to PANews observations, although the 24-hour trading volume of gold and silver on the HIP-3 market still lags behind Binance, its trading depth and transaction prices are already comparable to Binance.

It is worth noting that although Hyperliquid sent out price signals over the weekend, its holding scale is still not on the same level as traditional exchanges.

Only in the absence of CME could Hyperliquid take on the role of the price discovery center, more acting as a stopgap. It can be said that the road to the takeover of pricing power by Perp DEX is an unexpected start, just beginning.

The reverse market rise logic of HYPE token, "wealth seeks danger"

While most crypto assets were in wide fluctuations due to war panic, HYPE followed a completely different trajectory, rising over 25% within just three days.

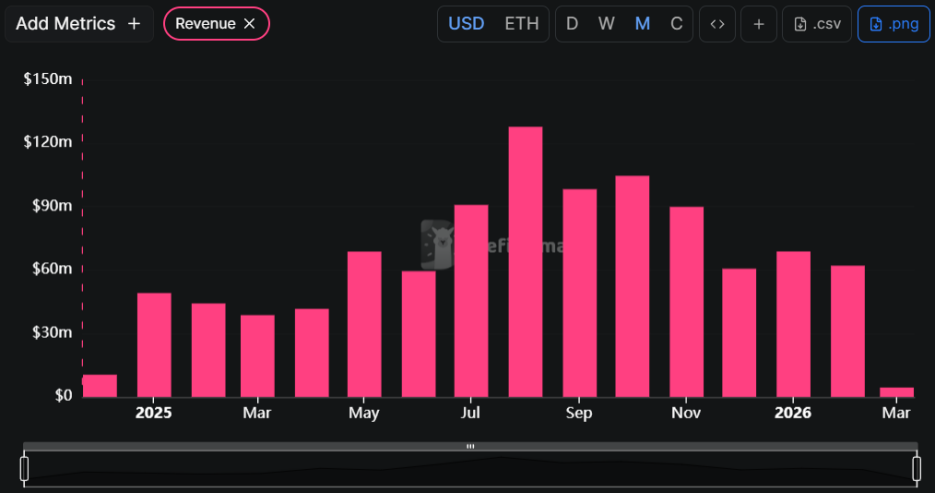

The intrinsic value of HYPE is highly tied to its protocol revenues. DeFiLlama data shows that Hyperliquid's revenue reached $62 million in February, averaging over $2.2 million per day.

According to the tokenomics design, 99% of the protocol income will be used for secondary market buybacks and destruction of HYPE. It can be said that the continuous deflationary pressure on the supply side comes from real trading demand.

During the weekend of the Iranian crisis, a significant amount of risk-averse funds rushed into Hyperliquid to hedge risks in oil, gold, and various assets. The protocol's daily revenue broke $2.4 million during the most volatile 24 hours.

For HYPE holders, this formed a positive feedback mechanism: the more chaotic the situation, the more frequent the transactions, the greater the buyback strength of the protocol, and the scarcer the tokens become.

PANews believes that this "anti-fragile" property allows HYPE to evolve into a wartime asset similar to "volatility call options" under the macro context.

HYPE is no longer just a carnival for retail investors; its strong revenue-generating ability under "black swan" conditions has boosted the confidence of large investors. According to Onchain Lens monitoring, a giant whale has cumulatively increased its holdings by over 540,000 HYPE in the past 18 days, worth up to $15 million; another whale spent 3.69 million USDC to buy over 110,000 HYPE.

What is even more noteworthy is that compared to the serious conflict that broke out between the U.S. and Iran on June 13 last year, at the moment when Israel and Iran fired missiles at each other, the instinctive reaction of investors was to deleverage, resulting in a severe withdrawal of positions in most perpetual contract protocols, and the price of HYPE also plummeted more than 20% accordingly.

Just nine months later, under the same scenario, Hyperliquid delivered an unexpected answer.

Through HIP-3, Hyperliquid has transformed itself into a "decentralized pricing engine for global assets." When commodities are no longer traded solely at CME but are priced 24 hours on a Perp DEX, HYPE, as the fuel of the engine, has evolved from "DeFi protocol" to "digital macro asset."

PANews believes that the recent rise of HYPE is essentially a process of partial crypto assets becoming "macrocized."

However, the high income brought by sudden macro events is also temporary. If the stalemate in the conflict continues, the market's long-term liquidity may dry up, and fee income will sharply decrease, leading to the failure of the deflationary narrative.

What else did Hyperliquid do right to run ahead of the "war concept" targets?

In the face of geopolitical crises, capital's choices are often the most rational.

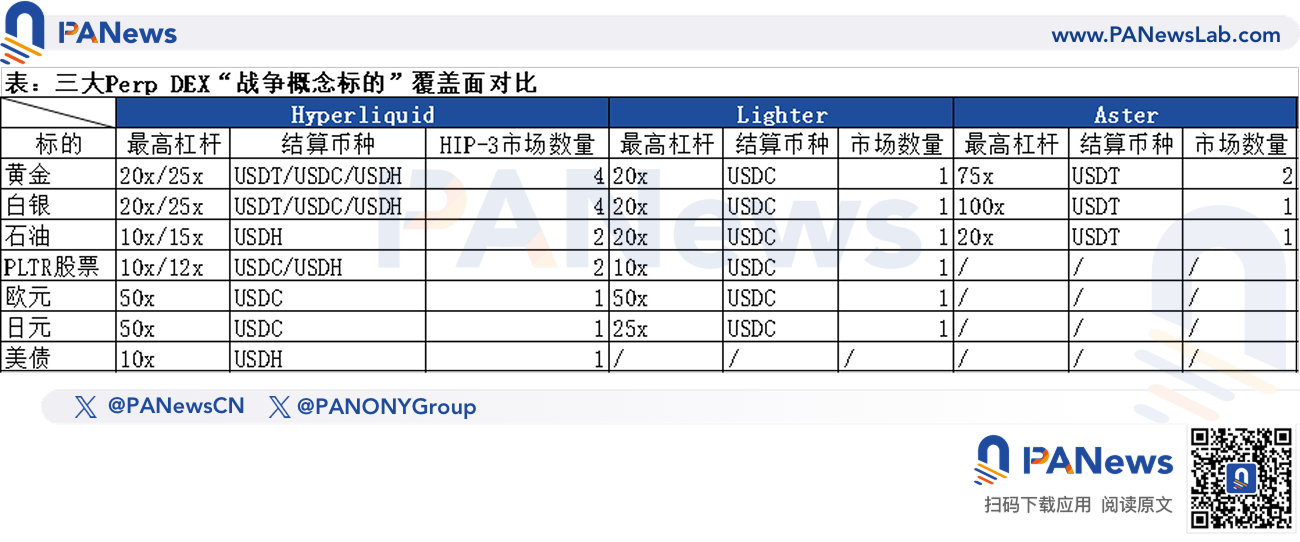

Although protocols like Lighter and Aster have come up with various tricks in the battle of Perp DEX, Hyperliquid has shown greater dominance in the face of systemic risks caused by the Iranian situation.

Artemis data shows that the Vol/OI (volume/open interest) ratio of Lighter and Aster is relatively high, reaching 3.3 and 2.1 respectively. This means that every dollar of real funds on these two platforms usually requires higher transaction frequency to generate $2-3 of trading volume.

Although the TGE airdrop of Lighter has long ended and the trading mining incentive phase of Aster has receded, their super-low or even zero fee strategies for retail users have made these two platforms still the top tools for day traders without incentives.

Since these traders rarely hold positions overnight, open interest (OI) is diluted while trading volume (Vol) remains exceptionally active, which directly raises the Vol/OI ratio.

While this "short-term" liquidity can create a prosperous appearance during stable phases, it may lead to severe slippage when facing geopolitical storms due to a lack of real depth.

In contrast, Hyperliquid's Vol/OI ratio has long remained stable at around 1.5, indicating a higher organic trading percentage. The protocol's open interest occupies over 60% of market share, with a total nearing $9 billion.

Among them, the open interest of the HIP-3 market is about $1.1 billion, and the 24-hour trading volume has reached $1.49 billion.

In contrast, Lighter and Aster show significant gaps compared to Hyperliquid. The open interest of TradFi targets on Lighter exceeds $45 million, while the 24-hour trading volume is about $68 million; Aster's open interest on commodity targets is less than $12 million, and the 24-hour trading volume is $100 million.

During the weekend of the Iranian crisis, when traders needed to establish hedge positions, only Hyperliquid's depth could bear large-scale selling pressure without causing a catastrophic slippage.

PANews believes that Hyperliquid's broad coverage of target categories is also one of the reasons for its逆势增长. It was observed that there were seven traditional target categories related to this Iranian war, with a corresponding number of HIP-3 markets reaching as high as 15. In terms of target coverage and the number of trading markets, Hyperliquid is significantly higher than Lighter and Aster.

From the perspective of maximum leverage multiples and settlement currencies, although Aster's leverage multiples are the most aggressive, each HIP-3 market offers different levels of leverage limits and richer settlement currencies, allowing users to participate in corresponding HIP-3 markets based on their risk preferences and settlement currencies, resulting in overall higher freedom of choice.

What is even more noteworthy is that users can conduct funding rate arbitrage on the Hyperliquid single platform. Taking silver and Palantir stocks as an example, the funding rates of various HIP-3 markets usually have both positive and negative values, allowing traders to earn the price differences in funding rates by establishing hedge positions in different markets, without the need for cross-platform arbitrage, resulting in a more user-friendly experience.

However, during CME's off-market period, the quotes in the HIP-3 market are heavily dependent on the protocol's own order book. If price manipulation occurs on specific targets (such as precious metals, crude oil, etc.), Perp DEX lacks the "circuit breaker" mechanism like traditional exchanges to protect investors.

Furthermore, large-scale provision of tokenized stocks and commodity trading may hit global regulatory red lines.

Nevertheless, in an increasingly turbulent macro environment, the financial system still needs a set of financial ledgers that do not rely on centralized credit and run continuously.

For investors, last year's "12-day war" was a warning, while the crisis in 2026 serves as confirmation. Perp DEX is becoming a macro tool for global risk hedging.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。