Authored by: Max.S

On February 28, 2026, a Saturday, air defense alarms in the Middle East shattered the tranquility of global geopolitics. The United States and Israel launched a meticulously planned large-scale airstrike on targets within Iran.

The timing of this military action resembled an extremely precise surgical operation, reflected not only in the physical coordinates of tactical strikes but also in the grasp of the "time coordinates" of global financial markets. Choosing to strike during the weekend when traditional Western financial markets were closed is significant: it maximally obstructed the immediate spread of panic in equities and forex markets, also granting various governments and central banks a full 48-hour buffer to intervene and guide market expectations.

However, during this deliberately created "trading vacuum," global capital did not sit idly by. As the gold and crude oil futures on the CME (Chicago Mercantile Exchange) were frozen at Friday's closing prices, and trading buttons for various ETFs were forcibly grayed out by the system, real undercurrents were surging in another ever-awake network. Cryptocurrency gold tokens like XAUT (Tether Gold) and PAXG (PAX Gold) experienced a trading surge on blockchain networks like Ethereum.

This was not just a geopolitical game but also a pressure test regarding "liquidity privilege." The airstrike event declared in an extremely extreme manner to all traditional finance practitioners: the traditional financial infrastructure based on T+1 or T+2 settlements, constrained by working days and fixed trading hours, is being abandoned by the times. The tokenization of real-world assets (RWA) and the ability to trade and settle digitally around the clock are no longer social experiments for geeks, but an inevitable trend for global capital vying for pricing power and trading Alpha.

From the perspectives of quantitative trading and hedge funds, the core of risk management lies in the accessibility of hedging tools. After the airstrike on February 28, the risk exposure of macro hedge funds surged instantly. By common logic, crude oil and gold are the preferred hedging targets. However, on that Saturday morning, thousands of financial institutions and professional traders became "liquidity prisoners."

The infrastructure of traditional financial markets is built upon the schedule of the industrial era. Although electronic trading has been common for decades, the underlying clearing and settlement systems (such as DTCC, Euroclear, and SWIFT networks) still rely heavily on centralized institutional batch processing and bank working hours. When black swan events unfold during non-trading hours, the reaction mechanism of traditional markets is completely frozen. Investors can only watch information flow spread at the speed of light while the capital flow is immobilized like insects trapped in amber.

This "deliberate avoidance of trading days" strike essentially compressed all market fluctuations and gap risks into the brief minutes during Monday’s opening. For quantitative market makers and high-frequency trading firms, this inability to hedge gap risks continuously is fatal. During the Monday opening phase characterized by extreme information asymmetry and drained liquidity, a chain reaction of long squeezes or short liquidations is easily triggered.

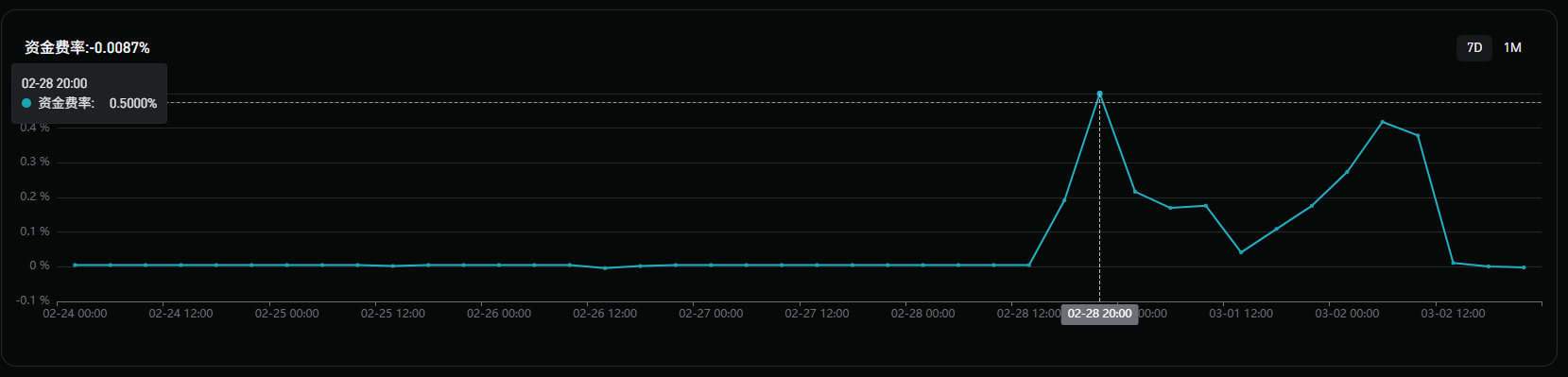

In contrast, the cryptocurrency market demonstrated resilience akin to a dimensional strike. Within minutes of the news of the attack on February 28, funds swiftly flowed into the liquidity pools of the crypto space. Trading pairs of XAUT and PAXG on major centralized crypto exchanges absorbed massive hedging demand. As shown in the funding rate chart (longs paying shorts), it reached 0.5% on February 28.

We can clearly see this smooth and steep value growth curve from on-chain data: no market closure, no circuit breakers, no blind boxes of opening gaps. The price of on-chain gold tokens continuously priced in milliseconds with each update from the front line battle report. By the time CME opened on Monday, the price of on-chain XAUT had completed thorough price discovery.

This brought about a profoundly disruptive financial phenomenon: the pricing power of traditional commodities has, for the first time in history during significant geopolitical crises, transferred to the digital asset market in stages.

When the Asian morning session began on March 2 (Monday), the traditional gold spot and futures markets experienced a surge at the opening. Over that weekend, XAUT transformed from being a shadow asset of GLD (SPDR Gold ETF) or COMEX futures gold into something else. Instead, the on-chain token became, in some sense, a "price oracle" for Wall Street’s Monday opening. Perceptive arbitrageurs took advantage of this 48-hour time differential to establish sufficient positions on-chain, and at the moment of the traditional market's opening on Monday, they eliminated the price disparity between the two worlds through high basis arbitrage, achieving perfect cash-out.

The trading frenzy in gold tokens over that weekend revealed the core value proposition of RWA assets: the expanding time dimension of liquidity.

In past narratives, people often focused on the advantages of RWA in lowering barriers, fragmenting ownership, or enhancing transparency. However, for professional financial practitioners, the greatest allure of RWA lies in the underlying logic of "settlement equals clearing" with T+0, as well as the 7x24x365 operation mechanism.

Imagine if what erupted over the weekend was not a Middle Eastern airstrike, but a sovereign debt default from a country, a major bank collapse, or an unexpectedly aggressive central bank rate cut. Traditional institutions would be left to passively bear enormous exposure risks before Monday’s opening. If US Treasuries, forex, or even core stock indices were deeply tokenized and sufficient liquidity pools established on the blockchain, institutional investors could immediately hedge against risks and swap assets via smart contracts at the moment a risk occurs.

In this event, not only gold but the exchange network between stablecoins and crypto-native assets served as a superhighway for capital refuge. The cross-border, cross-institutional fund transfers in the traditional financial system require complex confirmations from correspondent banks and multiple compliance reviews, often taking days. Meanwhile, on-chain, billions in hedging positions can undergo atomic swaps within a block time (12 seconds for Ethereum) without any counterparty default risk.

For Wall Street, the weekend at the end of February 2026 is a profound educational moment in investment research. Previously, many traditional institutions viewed the rise of RWA protocols like BlackRock's BUIDL (tokenized sovereign debt fund) and Ondo Finance with skepticism, believing they were merely gimmicks to attract stagnant capital from the crypto space. But the airstrike event proved that, in the face of extreme black swans, the liquidity premium provided by tokenized assets is a hardcore Alpha that no exceptional quantitative model can replace.

Quant funds will no longer be satisfied with trading interfaces provided by CME or NASDAQ; they will widely integrate APIs into on-chain DEXs and RWA trading pools with institutional-level compliance systems. To capture "asynchronous trading opportunities" during weekends and holidays, constructing cross-border arbitrage models spanning TradFi and DeFi will become standard for top hedge funds.

When brokers and market-making institutions realize that a massive amount of trading demand and fee profits are flowing into blockchain networks over the weekend, profit motives will compel them to actively become liquidity providers for on-chain assets. In the future, large market makers like Jane Street and Jump Trading will not only provide liquidity for ETFs on weekdays but will also inject liquidity into around-the-clock RWA asset pools during weekends.

Beginning with highly standardized commodities like gold and crude oil, the trend will gradually expand to short-term government bonds, high-quality corporate bonds, and even US stock indices. The carrier of financial assets will shift from the ledgers of trust companies and clearinghouses to distributed ledgers. There will be no more T+2 capital occupations, no more weekend anxieties over selling hedges on Friday afternoons, and global capital will truly achieve seamless circulation in both physical time and space.

"Money never sleeps" was once one of Wall Street's most famous slogans, but the reality is that traditional Wall Street not only needs to sleep but also requires weekends and statutory holidays. The artillery fire on February 28, 2026, brutally demonstrated that in the face of an increasingly complex and unpredictable global macro environment, broken trading times and locked liquidity are the greatest systemic risks themselves.

The price discovery process led by digital assets like XAUT over that weekend tolls the death knell for traditional clearing systems. RWA is not merely about moving real-world assets onto the blockchain; it is about reconstructing the temporal laws of financial operations with code. For quantitative analysts, traders, and financial engineers, the future battlefield will no longer be confined to a five-day workweek with eight-hour trading days. Whoever can first master the infrastructure for trading and settling around-the-clock digital assets will hold the throats of global markets during the next unexpected black swan night.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。