Written by: Jacob Zhao @IOSG

In previous research reports of the Crypto AI series, we have consistently emphasized the point that the most practical application scenarios in the current crypto space are concentrated in stablecoin payments and DeFi, and the agent is the key interface of the AI industry facing users. Therefore, in the trend of the integration of Crypto and AI, the two most valuable paths are: in the short term, AgentFi based on existing mature DeFi protocols (basic strategies such as lending, liquidity mining, etc., and advanced strategies such as Swap, Pendle PT, and funding rate arbitrage), and in the medium to long term, Agent Payment centered around stablecoin settlement, relying on protocols such as ACP/AP2/x402/ERC-8004.

The prediction market has become an industry trend that cannot be ignored by 2025, with its annual total trading volume soaring from about $9 billion in 2024 to more than $40 billion in 2025, achieving over 400% year-on-year growth. This significant growth is driven by multiple factors: uncertain demand due to macro political events, maturity of infrastructure and trading models, and a thawing regulatory environment (Kalshi's legal victory and Polymarket's return to the US). The early forms of prediction market agents are expected to emerge in early 2026 and potentially become an emerging product form in the field of agents within the next year.

Prediction Market: From Betting Tools to "Global Truth Layer"

The prediction market is a financial mechanism that trades based on the outcomes of future events, where contract prices essentially reflect the market's collective judgment on the probability of an event occurring. Its effectiveness comes from the combination of collective intelligence and economic incentives: in an anonymous environment of betting real money, decentralized information is quickly integrated into price signals weighted by capital willingness, significantly reducing noise and false judgments.

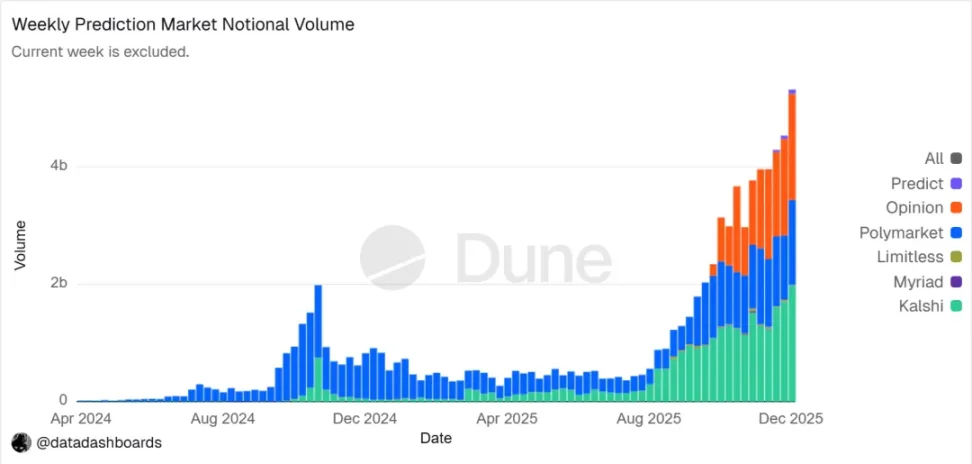

▲ Trend chart of nominal trading volume in prediction markets Data source: Dune Analytics (Query ID: 5753743)

By the end of 2025, the prediction market has essentially formed a duopoly structure dominated by Polymarket and Kalshi. According to Forbes statistics, the total trading volume in 2025 is expected to reach around $44 billion, with Polymarket contributing about $21.5 billion and Kalshi approximately $17.1 billion. In February 2026, Kalshi's trading volume ($25.9B) surpassed Polymarket's ($18.3B), approaching a 50% market share. Kalshi has achieved rapid expansion due to its previous legal success in election contracts, its compliance first-mover advantage in the US sports prediction market, and relatively clear regulatory expectations. Currently, the development paths of the two have shown clear differentiation:

Polymarket adopts a mixed CLOB structure of "off-chain matching, on-chain settlement" and a decentralized settlement mechanism, creating a global, non-custodial, high liquidity market. After returning to compliance in the US, it forms a "onshore + offshore" dual-track operation structure;

Kalshi integrates into the traditional financial system, attracting participation from Wall Street market makers in macro and data-based contract trading through API connections with mainstream retail brokers, with products constrained by traditional regulatory processes, resulting in relatively lagging long-tail demand and unexpected events.

In addition to Polymarket and Kalshi, other competitive players in the prediction market are mainly developing along two paths:

- One is the compliance distribution path, embedding event contracts into the existing account and clearing systems of brokers or large platforms, relying on channel coverage, compliance qualifications, and institutional trust to establish advantages (e.g., Interactive Brokers × ForecastEx's ForecastTrader, FanDuel × CME Group's FanDuel Predicts), with significant compliance and resource advantages, but still at an early stage in terms of products and user scale.

- The second is the crypto-native on-chain path, represented by Opinion.trade, Limitless, Myriad, which rapidly expands volume through points mining, short-cycle contracts, and media distribution, emphasizing performance and capital efficiency, but its long-term sustainability and risk control robustness are still to be validated.

The traditional financial compliance entry and the crypto-native performance advantages of these two paths together constitute a multi-competitive pattern in the ecosystem of prediction markets.

On the surface, the prediction market resembles gambling; its essence is a zero-sum game, but the core difference between the two lies in the presence of positive externalities: aggregating decentralized information through real-money trading to publicly price real-world events, forming a valuable signal layer. Its trend is shifting from betting to a "Global Truth Layer" — as institutions like CME and Bloomberg get involved, event probabilities have become decision metadata that can be directly invoked by financial and corporate systems, providing more timely and quantifiable market truths.

From the global regulatory landscape, the compliance paths of prediction markets are highly differentiated. The U.S. is the only major economy that explicitly includes prediction markets in its financial derivatives regulatory framework, while markets in Europe, the UK, Australia, and Singapore generally regard them as gambling and tend to tighten regulation. Countries like China and India completely prohibit them, meaning the future global expansion of prediction markets still depends on the regulatory framework of various countries.

Architectural Design of Prediction Market Agents

Currently, prediction market agents are entering an early stage of practice, and their value lies not in "AI predictions being more accurate," but in amplifying the information processing and execution efficiency within the prediction market. The prediction market is essentially an information aggregation mechanism, and prices reflect the collective judgment of event probabilities; inefficiencies in real markets stem from information asymmetry, liquidity constraints, and attention constraints. The reasonable positioning of prediction market agents is executable probabilistic portfolio management: transforming news, rules texts, and on-chain data into verifiable pricing deviations, executing strategies in a faster, more disciplined, and lower-cost manner, and capturing structural opportunities through cross-platform arbitrage and portfolio risk control.

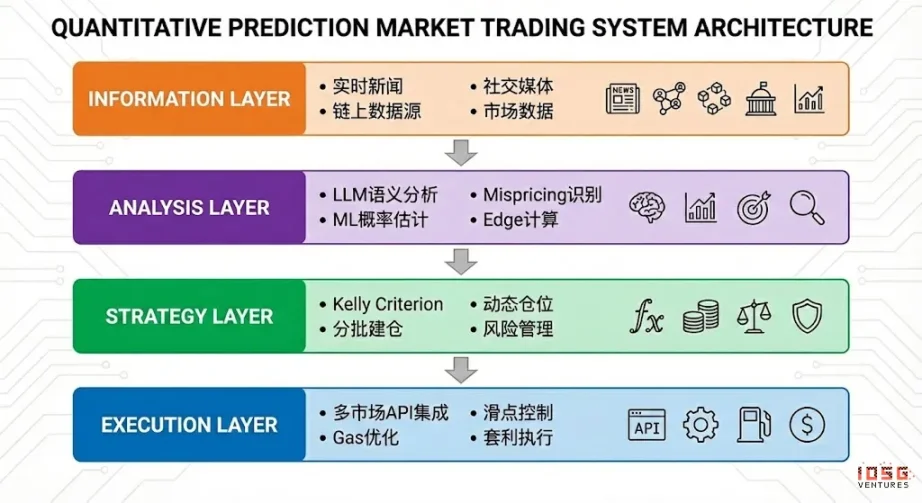

An ideal prediction market agent can be abstracted into a four-layer architecture:

- The information layer gathers news, social, on-chain, and official data;

- The analysis layer identifies mispricings and calculates Edge using LLM and ML;

- The strategy layer converts Edge into positions through the Kelly formula, batch building, and risk control;

- The execution layer completes multi-market orders, slippage and Gas optimization, and arbitrage execution, forming an efficient automated feedback loop.

Strategy Framework for Prediction Market Agents

Unlike traditional trading environments, prediction markets have significant differences in settlement mechanisms, liquidity, and information distribution, and not all markets and strategies are suitable for automated execution. The core of prediction market agents lies in whether they are deployed in clearly defined, codable scenes that align with their structural advantages. The following analysis will focus on three levels: target selection, position management, and strategy structure.

Target Selection in Prediction Markets

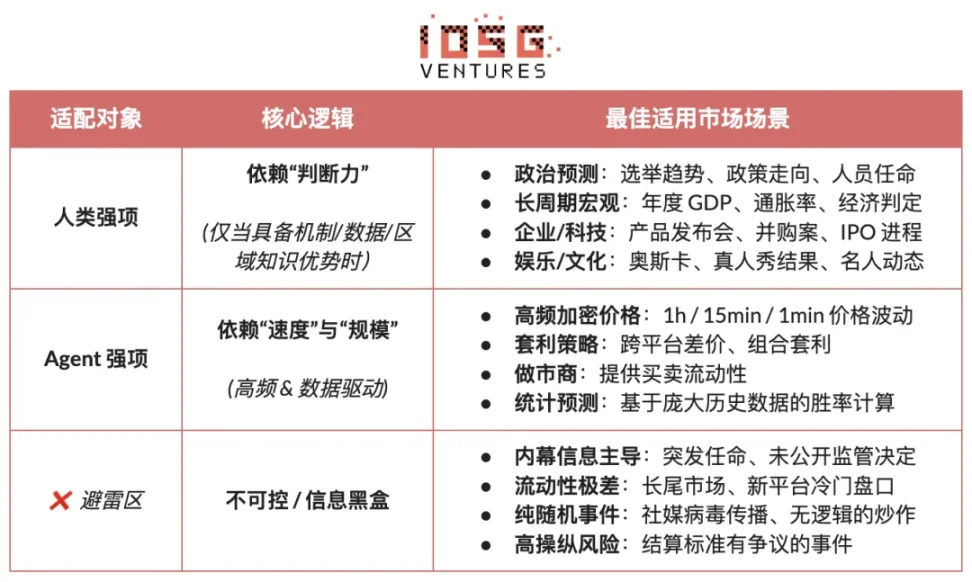

Not all prediction markets have tradeable value; their participation value depends on: clarity of settlement (whether rules are clear, whether data sources are unique), quality of liquidity (market depth, spreads, and trading volume), insider risk (degree of information asymmetry), time structure (expiration time and event rhythm), and the trader's own information advantages and professional background. Only when most dimensions meet basic requirements does a prediction market have the foundational participation; participants should match based on their own advantages and market characteristics:

- Core human advantages: markets that rely on professional knowledge, judgment, and integration of fuzzy information, with relatively loose time windows (measured in days/weeks). Typical examples include political elections, macro trends, and corporate milestones.

- Core advantages of AI agents: markets that rely on data processing, pattern recognition, and rapid execution, with extremely short decision windows (measured in seconds/minutes). Typical examples include high-frequency crypto prices, cross-market arbitrage, and automated market making.

- Incompatible fields: markets dominated by insider information or purely random/high-manipulative markets provide no advantage to any participant.

Position Management in Prediction Markets

The Kelly Criterion is the most representative capital management theory in repeated game scenarios, aiming not to maximize single profit, but to maximize the long-term compounding growth rate of capital. This method estimates the optimal position ratio based on win probability and odds, enhancing capital growth efficiency under conditions of positive expectation, widely used in quantitative investment, professional gambling, poker, and asset management.

- The classic form is: f^* = (bp - q) / b

- Where, f∗ is the optimal bet proportion, b is the net odds, p is the probability of winning, q=1−p

- The prediction market can be simplified as: f^* = (p - market_price) / (1 - market_price)

- Where, p is the subjective real probability, market_price is the market's implied probability

The theoretical effectiveness of the Kelly Criterion highly relies on accurate estimation of true probabilities and odds. In reality, traders struggle to maintain accurate knowledge of true probabilities consistently. In actual operations, professional gamblers and prediction market participants tend to adopt more executable and less probability estimation-dependent rule-based strategies:

- Unit System: This method divides capital into fixed units (such as 1%), investing different unit numbers based on confidence levels, with an automatic limitation on single-risk through unit cap, making it the most common practical method.

- Flat Betting: Every bet uses a fixed proportion of capital, emphasizing discipline and stability, suitable for risk-averse or low-confidence environments.

- Confidence Tiers: Pre-setting discrete position tiers with absolute upper limits to reduce decision complexity and avoid the pseudo-precision issues of the Kelly model.

- Inverted Risk Approach: Starting from the maximum bearable loss, this approach deduces the position size from risk constraints rather than return expectations, forming a stable risk boundary.

For prediction market agents, strategy design should prioritize executability and stability rather than pursuing theoretical optimality. The key lies in having clear rules, simple parameters, and fault tolerance for judgment errors. Under this constraint, the confidence tiers method combined with fixed position limits is the most suitable universal position management scheme for PM Agents. This method does not depend on precise probability estimates but categorizes opportunities into limited tiers based on signal strength, corresponding to fixed positions; even in high-confidence scenarios, it sets clear limits to control risk.

Strategy Selection in Prediction Markets

In terms of strategy structure, prediction markets can mainly be divided into two major categories: deterministic arbitrage strategies (Arbitrage) characterized by clear rules and codability, and speculative directional strategies (Speculative) relying on information interpretation and directional judgment; in addition, there are also market-making and hedging strategies dominated by professional institutions, demanding high capital and infrastructure requirements.

Deterministic Arbitrage Strategies (Arbitrage)

- Settlement Arbitrage: Settlement arbitrage occurs when event outcomes are basically determined, but the market has not yet fully priced this stage. Profits mainly come from information synchronization and execution speed. This strategy has clear rules, lower risks, and can be fully encoded, making it the most suitable core strategy for agents in prediction markets.

- Probability Conservation Arbitrage (Dutch Book Arbitrage): Dutch Book arbitrage exploits structural imbalances formed by the sum of prices of mutually exclusive and complete event sets deviating from probability conservation constraints (∑P≠1), locking in directionless risk returns through combination building. This strategy relies solely on rules and price relationships, has low risk, and is highly regulatable, making it a typical deterministic arbitrage form suitable for agent automation.

- Cross-Platform Arbitrage: Cross-platform arbitrage profits by capturing pricing deviations of the same event across different markets, posing low risks but requiring high demands for latency and parallel monitoring. This strategy is suitable for agents with infrastructure advantages, but increased competition leads to declining marginal returns.

- Bundle Arbitrage: This form of arbitrage utilizes pricing inconsistencies between related contracts for trading, characterized by clear logic but limited opportunities. This strategy can be executed by agents but requires certain engineering requirements for rule parsing and combination constraints, with an intermediate adaptability for agents.

Speculative Directional Strategies (Speculative)

- Structured Information Driven Strategies (Information Trading): These strategies revolve around clear events or structured information, such as official data releases, announcements, or ruling windows. As long as the information sources are clear and the trigger conditions definable, agents can leverage speed and discipline advantages at monitoring and execution levels; however, when the information turns into semantic judgments or situational interpretations, human intervention is still required.

- Signal Following Strategies: This strategy gains profits by following the actions of accounts or funds that historically perform well, with relatively simple and automatable rules. Its core risks lie in signal degradation and being reversed, hence filtering mechanisms and strict position management are required. It is suitable as a complementary strategy for agents.

- Unstructured and High Noise Strategies (Unstructured / Noise-driven): These strategies highly depend on emotions, randomness, or participant behaviors, lacking stable reproducible edges, and long-term expected values are unstable. Due to the difficulty in modeling and high risk, they are unsuitable for systematic execution by agents and are not recommended as long-term strategies.

High-frequency pricing and liquidity strategies (Market Microstructure): These strategies rely on extremely short decision windows, continuous quoting, or high-frequency trading, demanding high latency, models, and capital. Although theoretically suitable for agents, they are often restricted by liquidity and competition intensity in prediction markets, suitable only for a few participants with significant infrastructure advantages.

Risk management and hedging strategies (Risk Control & Hedging): These strategies do not directly pursue profits but aim to reduce overall risk exposure. They have clear rules and defined goals, operating long-term as underlying risk control modules.

Overall, strategies suitable for agents in prediction markets focus on clear rules, codability, and weak subjective judgment, where deterministic arbitrage should be the core source of returns, structured information and signal following strategies as supplements, while high noise and emotional trading should be systematically excluded. The long-term advantage of agents lies in their execution speed and risk control capabilities.

Business Models and Product Forms of Prediction Market Agents

The ideal business model design for prediction market agents explores different directional opportunities at various levels:

- Infrastructure level, providing multi-source real-time data aggregation, Smart Money address libraries, unified prediction market execution engines, and backtesting tools, charging B2B fees to obtain stable income unrelated to prediction accuracy;

- Strategy level, introducing community and third-party strategies, constructing a reusable and assessable strategy ecosystem, and realizing value capture through invocation, weighting, or execution shares, thereby reducing reliance on a single Alpha.

- Agent/Vault level, agents directly participate in real trading execution in a trust management manner, relying on on-chain transparency and strict risk control systems, collecting management fees and performance fees for realized capabilities.

Different business models correspond to product forms, which can also be divided into:

- Entertainment/Game-like mode: Lowering participation barriers through intuitive interactions similar to Tinder, having the strongest user growth and market education capacity, is an ideal entry point for breaking circles, but must be transitioned to subscription or execution-type product monetization.

- Strategy subscription/signal mode: Not involving fund custody, regulatory friendly, with clear accountability, a relatively stable SaaS revenue structure, representing the most viable commercialization path at the current stage. Its limitation lies in the strategies being easily replicated, execution having losses, with a long-term revenue ceiling being limited. The experience and retention can be significantly improved through a "signal + one-click execution" semi-automated form.

- Vault custody model: Having scale effects and execution efficiency advantages, the form is similar to asset management products, but faces multiple structural constraints such as asset management licenses, trust barriers, and centralized technical risks, with the business model highly dependent on market environment and sustained profitability. Unless there are long-term performances and institutional endorsements, it is not suitable as the main path.

Overall, a diversified income structure of "infrastructure monetization + strategy ecosystem expansion + performance participation" helps to reduce reliance on the single hypothesis that "AI continues to outperform the market." Even as Alpha converges with market maturity, underlying capabilities such as execution, risk control, and settlement still possess long-term value, thereby building a more sustainable business loop.

Case Studies of Prediction Market Agents

Currently, prediction market agents are still in the early exploration stage. Although the market has seen diverse attempts from underlying frameworks to upper-layer tools, it has yet to form a standardized product that is mature, replicable, and accomplished in strategy generation, execution efficiency, risk control systems, and business closure.

We divide the current ecological landscape into three levels: infrastructure level, autonomous trading agents, and prediction market tools.

Infrastructure Level

Polymarket Agents Framework

Polymarket Agents is the developer framework officially launched by Polymarket, aiming to solve the engineering standardization problem of "connection and interaction." This framework encapsulates market data acquisition, order building, and basic LLM calling interfaces. It addresses the question of "how to place an order with code," but leaves blank the core trading capabilities—such as strategy generation, probability calibration, dynamic position management, and backtesting systems. It is more like an officially recognized "access standard," rather than a finished product with Alpha returns. Commercial-level agents still need to build a complete investment research and risk control core based on this.

Gnosis Prediction Market Tools

Gnosis Prediction Market Agent Tooling (PMAT) provides complete read-write support for Omen/AIOmen and Manifold but only opens read-only permissions for Polymarket, revealing clear ecological barriers. It is suitable as a foundational development base for agents within the Gnosis system, but has limited practicality for developers mainly operating in Polymarket.

Polymarket and Gnosis are currently the prediction market ecosystems that explicitly productize "agent development" into official frameworks. Other prediction markets like Kalshi mostly remain at the API and Python SDK level, requiring developers to independently fill in critical system capabilities such as strategies, risk control, operation, and monitoring.

Autonomous Trading Agents

Currently, many "prediction market AI agents" in the market are still in early stages, despite being labeled as "agents." Their actual capabilities are significantly distant from the automated closed-loop trading that can be delegated, generally lacking independent, systematic risk control layers, and failing to include position management, stop losses, hedging, and expected value constraints in the decision-making process. Overall, the product maturity level is low, and a mature system that can operate long-term has yet to form.

Olas Predict

Olas Predict is currently the prediction market agent ecosystem with the highest product maturity. Its core product Omenstrat is built on Omen within the Gnosis system, adopting FPMM and decentralized arbitration mechanisms at the underlying level, supporting small, high-frequency interactions but limited by insufficient market liquidity on Omen alone. Its "AI predictions" mainly rely on generic LLMs, lacking real-time data and systematic risk control, with historical win rates showing significant variation across categories. In February 2026, Olas launched Polystrat, extending agent capabilities to Polymarket—users can set strategies using natural language, and the agent automatically identifies probability deviations in markets settling within four days and executes trades. The system controls risk through local operations by Pearl, self-hosted Safe accounts, and hard-coded limits, marking the first consumer-facing autonomous trading agent aimed at Polymarket.

UnifAI Network Polymarket Strategy

Offers an automated trading agent for Polymarket, primarily focusing on tail risk-bearing strategies: scanning contracts nearing settlement with implied probabilities >95% and buying them, targeting a 3-5% price difference. On-chain data indicates a win rate close to 95%, but returns show marked variation across categories, with the strategy highly reliant on execution frequency and category selection.

NOYA.ai

NOYA.ai aims to integrate "research-judgment-execution-monitoring" into a closed-loop agent, covering intelligence, abstraction, and execution layers in its architecture. Currently, it has delivered Omnichain Vaults; the Prediction Market Agent is still in development, lacking a complete mainnet closed loop, and is in a vision validation stage overall.

Prediction Market Tools

Current prediction market analysis tools are still insufficient to constitute a complete "prediction market agent," with their value mainly lying in the information layer and analysis layer of the agent architecture, while transaction execution, position management, and risk control still need to be borne by the traders themselves. From the product form aspect, they are better suited as "strategy subscription/signal assistance/research enhancement" positioning and can be regarded as early prototypes of prediction market agents.

By systematically sorting and empirically screening projects recorded by Awesome-Prediction-Market-Tools, this report selects representative projects with initial product forms and usage scenarios as case studies. These focus mainly on four directions: analysis and signal layers, alert and whale tracking systems, arbitrage discovery tools, and trading terminals and aggregate execution.

Market Analysis Tools

- Polyseer: A research-style prediction market tool employing a multi-agent division of labor architecture (Planner / Researcher / Critic / Analyst / Reporter) for bilateral evidence gathering and Bayesian probability aggregation, producing structured research reports. Its advantages lie in transparent methodology, process engineering, and being open-source and auditable.

- Oddpool: Positioned as the "Bloomberg terminal of prediction markets," supplying cross-platform aggregation of Polymarket, Kalshi, CME, and real-time data dashboards.

- Polymarket Analytics: A global Polymarket data analysis platform, systematically presenting trader, market, position, and transaction data; it has a clear positioning and intuitive data, suitable as a basic data query and research reference.

- Hashdive: A data tool targeting traders, quantifying the selection of traders and markets through Smart Score and multi-dimensional Screeners, demonstrating practicality in "smart money identification" and follow-up decision making.

- Polyfactual: Focusing on AI market intelligence and sentiment/risk analysis, embedding analytical results into trading interfaces via a Chrome extension, likely targeting B2B and institutional user scenarios.

- Predly: An AI mispricing detection platform that identifies pricing deviations between market prices and AI-calculated probabilities for Polymarket and Kalshi, with the official claim of an alert accuracy rate of 89%, positioned for signal discovery and opportunity filtering.

- Polysights: Covers 30+ markets and on-chain indicators, utilizing Insider Finder to track new wallets and large one-directional bets, suitable for daily monitoring and signal discovery.

- PolyRadar: A multi-model parallel analysis platform offering real-time interpretations, timeline evolution, confidence scoring, and source transparency for a single event, emphasizing multi-AI cross-validation, positioned as an analysis tool.

- Alphascope: An AI-driven prediction market intelligence engine providing real-time signals, research summaries, and monitoring of probability changes, still in early stages, biased towards research and signal support.

Alerts / Whale Tracking

- Stand: Clearly positioned for whale-following and high-confidence action alerts.

- Whale Tracker Livid: Productizing changes in whale positions.

Arbitrage Discovery Tools

- ArbBets: An AI-driven arbitrage discovery tool focusing on Polymarket, Kalshi, and sports betting markets, identifying cross-platform arbitrage and positive expectation (+EV) trading opportunities, positioned for high-frequency opportunity scanning.

- PolyScalping: A real-time arbitrage and scalp analysis platform for Polymarket, supporting full-market scans every 60 seconds, ROI calculations, and Telegram notifications, with opportunities filterable by liquidity, spreads, and volume, targeting proactive traders.

- Eventarb: A lightweight cross-platform arbitrage calculation and notification tool covering Polymarket, Kalshi, and Robinhood, with focused functionality available for free usage, suitable as a basic arbitrage assistance.

- Prediction Hunt: A cross-exchange prediction market aggregation and comparison tool providing real-time price comparisons and arbitrage identification for Polymarket, Kalshi, and PredictIt (approximately every 5 minutes refresh), positioned for information symmetry and market inefficiency discovery.

Trading Terminals / Aggregate Execution

- Verso: An institutional-level prediction market trading terminal backed by YC Fall 2024, offering a Bloomberg-style interface that tracks 15,000+ contracts in real-time for Polymarket and Kalshi, in-depth data analysis, and AI news intelligence, positioned for professional and institutional traders.

- Matchr: A cross-platform prediction market aggregation and execution tool covering over 1,500 markets, achieving optimal price matching via smart routing, planning automated yield strategies based on high-probability events, cross-arbitrage, and event-driven approaches, positioned for execution and capital efficiency.

- TradeFox: A professional prediction market aggregation and Prime Brokerage platform supported by Alliance DAO and CMT Digital, providing advanced order execution (limit orders, stop-loss, TWAP), self-custodied trading, and multi-platform smart routing, targeted at institutional-level traders, planning to expand to platforms like Kalshi, Limitless, and SxBet.

Conclusion and Outlook

Currently, prediction market agents (Prediction Market Agents) are in the early exploration stage of development.

- Market foundation and essence evolution: Polymarket and Kalshi have formed a duopoly structure, providing sufficient liquidity and scene foundations to build agents around. The core difference between prediction markets and gambling lies in positive externalities, aggregating decentralized information through real trades to publicly price real events, gradually evolving into a “global truth layer.”

- Core positioning: Prediction market agents should be positioned as executable probabilistic asset management tools, core tasks converting news, rules texts, and on-chain data into verifiable pricing deviations, executing strategies with higher discipline, lower cost, and cross-market capabilities. An ideal architecture can be abstracted into four layers: information, analysis, strategy, and execution, but its actual tradability highly depends on settlement clarity, quality of liquidity, and level of information structuring.

- Strategy selection and risk control logic: From a strategy perspective, deterministic arbitrage (including settlement arbitrage, probability conservation arbitrage, and cross-platform pricing trades) is best suited for automated execution by agents, while directional speculation should only serve as a supplement. In position management, executability and fault tolerance should be prioritized, with the tiers method coupled with fixed position limits being the most suitable.

- Business model and prospects: Commercialization primarily divides into three layers: infrastructure layer generates stable B2B income through data execution infrastructure, strategy layer monetizes through third-party strategy invocation or shared returns, and the Agent/Vault layer participates in practical applications under transparent risk control constraints on-chain, collecting management and performance fees. Corresponding forms include entertainment-style entry, strategy subscription/signals (currently the most feasible), and high-barrier vault custody, with "infrastructure + strategy ecosystem + performance participation" representing a more sustainable path.

Although a diversity of attempts from underlying frameworks to upper-layer tools has emerged in the ecosystem of prediction market agents (Prediction Market Agents), a mature, replicable standardized product has yet to surface across key dimensions such as strategy generation, execution efficiency, risk control, and business closure. We look forward to the iterations and evolution of prediction market agents in the future.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。