In the past six months, the hottest topic in the Bitcoin mining circle is no longer "how much has it risen," but "how much longer can it last." The price of Bitcoin is hovering around $60,000, while the cost line is firmly pressed above $80,000 — this accounts for a loss no matter how you look at it.

A large-scale "exodus" has begun, but the direction is surprising: it is not to exit the market, but to turn around and dive into the AI computing power track.

1. Losing $20,000 per Coin, Miners Shut Down Collectively

● First, let’s look at a heart-wrenching set of numbers. In February 2026, the average production cost of one Bitcoin across the network had risen to $87,000, while the price was only about $64,000. This means that miners incur a loss of nearly $20,000 on each block mined. This is not just a matter of thin profit margins; it is a situation where each production incurs a loss.

● Analysts at Rosenblatt Securities put it more bluntly: mining revenues have dropped to less than 3 cents per terahash. Except for the most efficient mining machines, the rest are all losing money. The hash price, a core indicator of miners' ability to earn, has fallen by about 30% over the past three months to only $28/PH/day, approaching a historical low.

● As a result, large-scale shutdowns occurred. On February 9, the Bitcoin network triggered an 11.16% decrease in mining difficulty — the largest reduction in nearly four and a half years since the 2021 ban in China. The difficulty adjustment is a system’s automatic protection mechanism to make it easier for miners who remain in the market to mine coins, but the problem is that an 11% "burden reduction" is just a drop in the bucket against a 45% cost-price inverted rate.

● There is an "miner profit sustainability index" within the industry, where 100 is the healthy line, and the current number is 21. In plain terms: except for a very few top players with electricity costs below $0.05/kWh and using only the latest models, the rest are all experiencing cash flow losses.

2. The Faithful Liquidation: From "Holding Coins" to "Holding Cash"

● A more alarming signal came from industry giants. In late February, Bitdeer, a Nasdaq mining company led by Wu Jihan, made a shocking move: it liquidated all Bitcoin holdings. They not only sold all 189.8 BTC mined that week, but also reduced the 943.1 BTC in reserves to zero, cashing out approximately $63 million.

● This company recently became the largest publicly traded self-operated mining company in the world with a capacity of 63.2 EH/s, yet chose to leave not a single coin behind. This was unimaginable in the past — "mining equals hoarding coins" used to be the golden rule in the mining circle. But now, this belief has been shattered.

● Bitdeer's explanation is very realistic: at a time when hash prices are below $30, holding Bitcoin represents a huge opportunity cost. Each coin held means less cash flow available for debt repayment, equipment upgrades, or transformation. They issued $325 million in convertible bonds, explicitly stating the funds' use: repaying old debts, hedging dilution risks, and the remainder — directed towards AI infrastructure.

● Cango also liquidated its holdings. This company sold 4,451 Bitcoins in early February, cashing out $305 million, with the funds used to pay off loans and layout AI computing. Once a "famous company in the mining circle," Bitfarms simply announced a complete exit from Bitcoin mining and will focus entirely on AI in the future.

3. On the Other Side, the Madness: AI's "Power Thirst"

While miners run away, on the other side, some people are rushing in with cash. Who? AI companies.

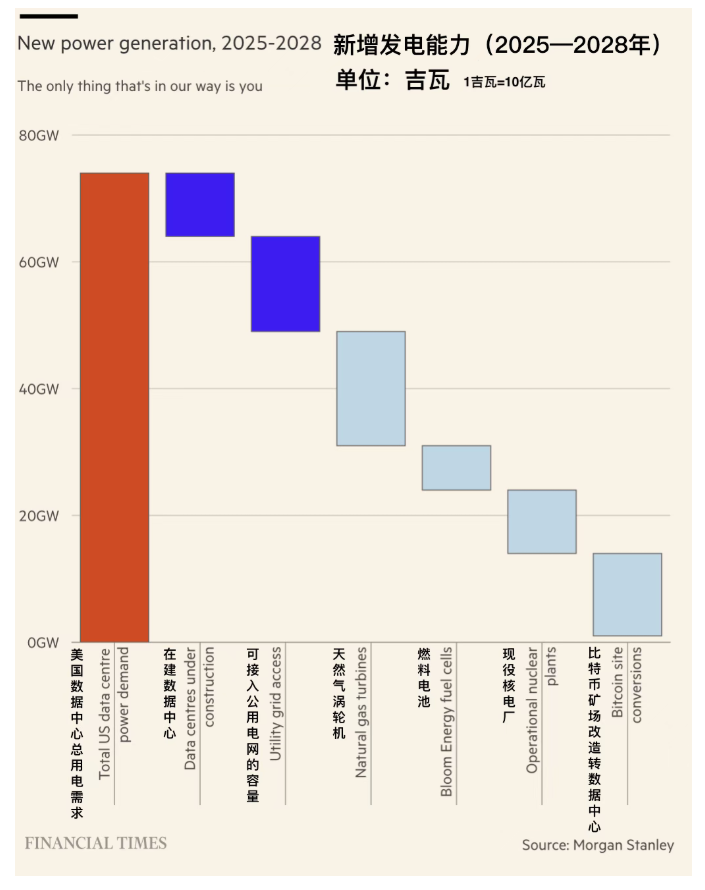

● Morgan Stanley recently calculated a figure: from 2025 to 2028, the electricity demand of data centers in the U.S. will increase by 74 GW (1 GW = 1 billion watts). But what about supply? The new infrastructure being built only adds 10 GW, and the usable capacity that the grid can squeeze out is about 15 GW, totaling 25 GW, with a gap of 49 GW.

● This is why mining sites have suddenly become in demand. What do miners have? Wires, land, and grid connection licenses — what AI companies need most is not chips, but "electricity," or more specifically, "the speed of electrification.” How quickly you can connect power and get the facility running determines how quickly you can grab a share of the computing power market.

● Morgan Stanley has calculated: even if all the electricity available from Bitcoin mining sites in the U.S. and Europe were used for data centers, there would still be a shortage. However, transforming mining sites can shorten the gap by 10 to 15 GW, making it an optimal solution for "quickly filling the void."

● Therefore, the story flows smoothly: mining sites are essentially ready-made large-scale, low-latency data centers with electrical capacity, cooling systems, and rack space. In the bear market of Bitcoin, these are cost burdens, but in an era of tight AI computing power, they are scarce assets that can generate rental income.

4. Transformation in Progress: Who Runs Fast, Who Gets Valuation

● On February 26, one of the largest mining companies in the U.S., MARA Holdings, announced a partnership with Starwood Capital to convert some Bitcoin mining facilities into AI data centers. The initial plan is for a 1 GW capacity, which can be expanded to 2.5 GW. Starwood is responsible for design, leasing, construction, and operation, while MARA provides the land, and both parties jointly own the project. Upon the announcement, MARA's stock price surged by 17% in after-hours trading.

● Interestingly, Morgan Stanley has set a target price of only $8 for MARA, which is 3% lower than its closing price at the time. The reason: Mara is not "thorough" enough; it still wants to juggle — both mining coins and working on AI. The market prefers stories of "decisive transformation."

● What does decisive mean? TeraWulf is one example. This company just secured financing for a joint project for a 168 MW AI data center, with FluidStack as the partner, backed by payment assurances from Google. Analysts set a target price of $37 for TeraWulf, implying an upside of about 159%. All 13 analysts rated it as a buy.

● Bitfarms has an even more specific plan: it aims to fully transform an 18 MW Bitcoin mining site in Washington State to support Nvidia GB300 GPUs, using liquid cooling technology, and expects completion by the end of 2026. They calculated that this site, accounting for less than 1% of the total, when converted to GPU as a service, could generate net operating income exceeding all profits made from mining in the company’s history.

● The logic of valuation has completely changed. Previously, mining companies’ stock prices fluctuated with Bitcoin prices and hash rates, like a roller coaster. But if they sign long-term leases, with reliable payment counterparts (like Google), cash flow becomes "monthly rental income,” and the market will treat you like an infrastructure company for valuation — comparable to data center REITs like Equinix and Digital Realty, rather than other mining companies. Morgan Stanley calls this logic the "REIT endgame."

5. Computing Power Landscape: Who Takes Over, and Who is in an Awkward Position

● According to Hashrate Index, U.S. miners currently account for about 37.5% of the global market share, while Russia holds 16.4%, and China 11.7%. If U.S. mining facilities reduce Bitcoin operations for AI, the network's hash power will become more concentrated in places like Russia and China. This is somewhat awkward for a government that once promised to "make the U.S. the global cryptocurrency capital."

● However, political matters are hard to predict. There might be another route: selling to allies. For instance, Canaan Technology recently spent nearly $40 million to acquire a 49% stake in three mining sites from Cipher Mining in Texas. These sites have a total installed capacity of 120 MW, with electricity costs below $0.03/kWh and also feature wind power. Capital is flowing, and the computing power landscape is still being restructured.

This round of "mine to AI" essentially exchanges two mathematical problems: on the Bitcoin side, the halving cuts the block reward to 225 coins per day, while transaction fees can’t keep up; on the AI side, 74 GW of new demand presses against a 49 GW gap. The electricity, land, and grid connection permissions that mining sites hold have transformed from "mining costs" into "computing power hard currency."

In the short term, miner shutdowns and transformations will continue. In the long term, those who can shift from "mining volatility" to "rental cash flow" will survive as the next-generation infrastructure companies. This industry has never believed in sentiments, only in shutdown prices.

Join our community, let’s discuss and grow stronger together!

Official Telegram community: https://t.me/aicoincn

AiCoin Chinese Twitter: https://x.com/AiCoinzh

OKX benefits group: https://aicoin.com/link/chat?cid=l61eM4owQ

Binance benefits group: https://aicoin.com/link/chat?cid=ynr7d1P6Z

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。