Circle Financial Report Detailed Interpretation — Looking Through Phenomena to See Essence, Is CRCL Worth Buying?

First of all, I am not bearish on $CRCL. I have also mentioned multiple times that CRCL is on my purchase list; I just do not plan to buy CRCL at 80+ dollars. Recently, I have been considering starting to gradually rebuild my position; this is the premise.

Many friends have already looked at Circle's financial report, and the answers given for the fourth quarter are quite good. Some friends even said that Circle's performance during the interest rate reduction cycle is already impressive. Although this is not incorrect, it is not entirely true either.

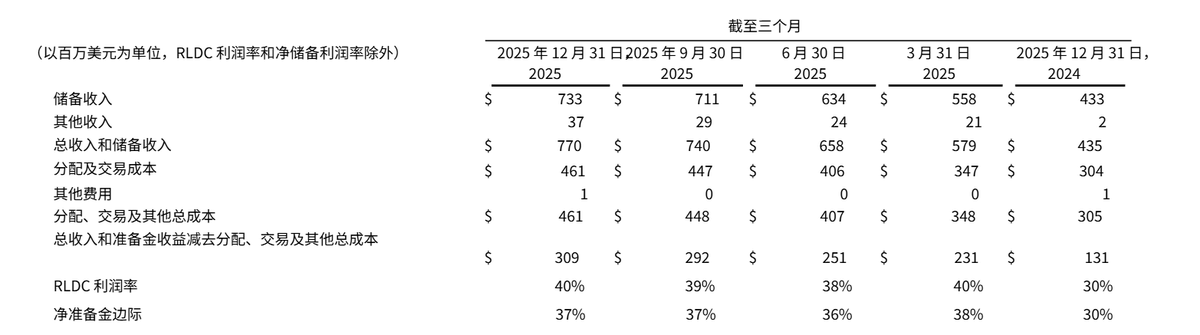

Indeed, Circle's fourth quarter financial report for 2025 shows a 77% increase in total revenue compared to the same period in 2024, reaching 770 million dollars, and earnings per share (EPS) reached 0.43 dollars, significantly exceeding market expectations, with net profit at approximately 133 million dollars, which is undoubtedly good news.

However, looking at the detailed data, Circle's achievement is not due to its business revenue or fee increase, but rather due to increased interest, which comes from the rise in USDC issuance.

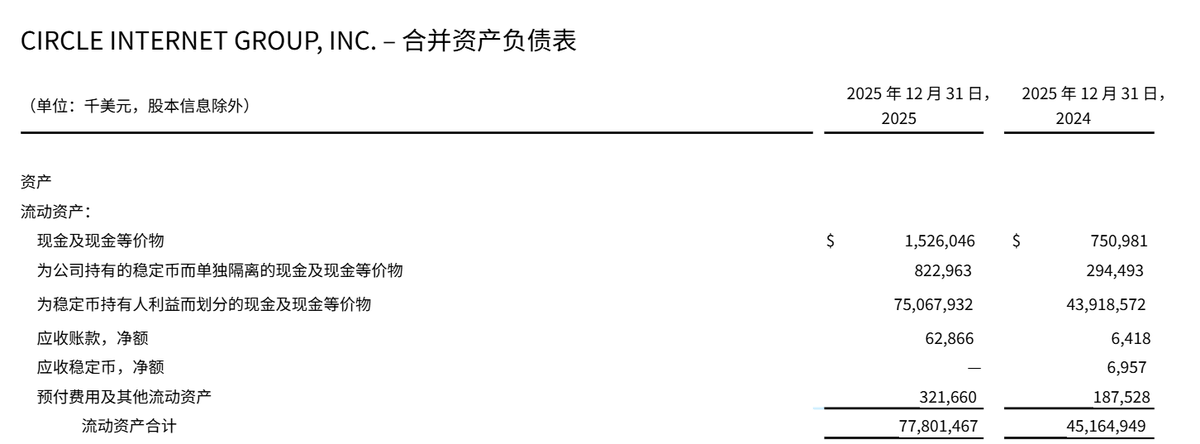

As of December 2024, Circle's total USDC issuance is 43.92 billion dollars.

By December 2025, the total issuance of USDC has reached 75.49 billion dollars, an increase of 71.88%.

Therefore, the main increase in $CRCL's revenue comes from the significant rise in USDC issuance, leading to higher interest income.

The financial report also clearly states that the main source of income is derived from reserve income, while other reserve income is also increasing. However, even by December 2025, other income is only about 37 million dollars, which is merely 1/20 of reserve income. As we all know, even Circle itself has admitted that a decrease in federal fund rates will directly impact the income structure.

So, in the face of a declining interest rate cycle, if other revenues cannot surge, Circle will have to continue issuing large amounts of USDC to maintain good revenue expectations.

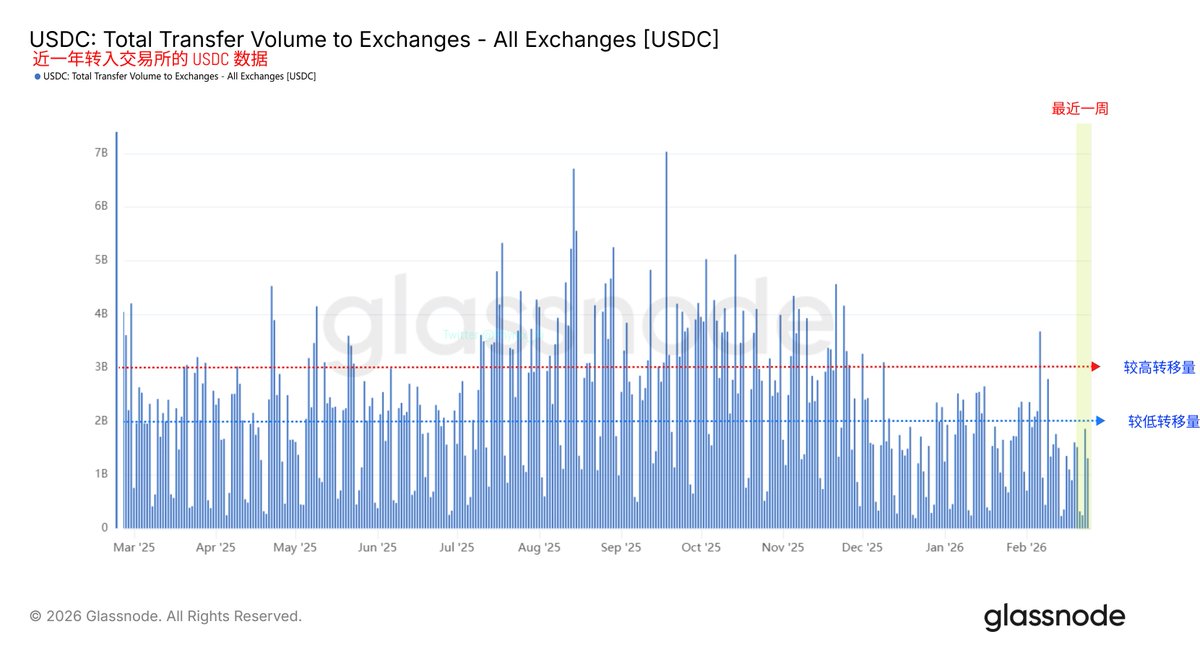

Recently, the market value of USDC has declined due to a slump in the cryptocurrency industry, but I believe that as the market warms up, USDC's market value will gradually rise. However, whether it can double again in about a month (during the first quarter 2026 financial report) is estimated to be very difficult. Moreover, once entering a substantial and rapid interest rate reduction cycle, the profitability per USDC will definitely be compressed.

Of course, the rebound in USDC's market value is also one of the reasons I am preparing to build my position; funds can often be seen as a leading indicator of the market. The continued rebound of USDC's market value is very likely due to investors preparing to bottom out, although this portion of funds has not yet shown a trend of moving to exchanges.

However, I believe that these newly issued USDC are either preparing to support trading or to support payments. No matter which, it is beneficial for the development of $CRCL. Of course, when this benefit will be realized is uncertain, so starting to build a small position now may not be a mistake.

Another point to note is that Circle's distribution costs are very, very high, especially the fees paid to Coinbase. The financial report shows that in the fourth quarter of 2025, CRCL’s "total distribution, transaction, and other costs were 461 million dollars, a year-on-year increase of 52%, due to increased distribution payments," and operational expenses also reached 254 million dollars, a year-on-year increase of 95%.

High channel costs and operational costs are also one of the reasons limiting CRCL.

Of course, CRCL also has good performance:

1. The Arc public test network has been launched, with over 100 participants from banks, capital markets, digital assets, payments, and technology fields. Based on data from the past 30 days as of February 20, 2026, the average daily transaction volume is 2.3 million transactions. Since the test network was launched, the total number of transactions has exceeded 166 million. Arc plans to launch the mainnet this year.

2. The Circle Payments Network (CPN) has expanded, with 55 financial institutions connected as of February 20, 2026, and another 74 are undergoing qualification review. The annualized transaction volume is 5.7 billion dollars.

3. The circulating EURC at the end of the year was 310 million euros, a year-on-year increase of 284%, and a quarter-on-quarter increase of 44%. The USYC assets at the end of the year amount to 1.5 billion dollars, a quarter-on-quarter increase of 111%.

4. Visa announced that card-issuing and acquiring banks in the U.S. can now use USDC for full settlement with Visa, achieving continuous settlement outside of traditional banking hours.

5. Intuit has launched a multi-year strategic partnership to integrate USDC and Circle's supporting infrastructure into its platform.

6. Established a partnership with Polymarket, the world’s largest prediction market, to promote the use of USDC as core collateral and settlement asset for its market.

7. The Bermuda government announced plans to become the world's first fully on-chain national economy, supported by Circle's digital asset infrastructure.

8. In December, Circle received conditional approval from the Office of the Currency Regulator to establish a national trust bank, further strengthening the USDC infrastructure.

That's basically it. Overall, $CRCL, as the first stock of U.S. stablecoins and currently the only one, still holds imaginative potential and a ceiling. This strong financial report mainly relies on the increase in USDC's market value, but maintaining this strength in the first quarter of 2026 financial report or even subsequent reports will be very difficult.

Gradually starting to build positions and buying on dips should be considered by those with ample funds. Additionally, because CRCL currently has lower other revenues, it is closely related to the overall rise and fall of the cryptocurrency market. If the overall cryptocurrency market is not doing well, CRCL may find it hard to rise independently.

@bitget VIP, lower fees, better benefits

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。