Written by: Lin Wanwan

The money is already embedded in the code.

Six months ago, AI payment was just a PowerPoint presentation at a launch event. Today's AI is becoming the "cash register."

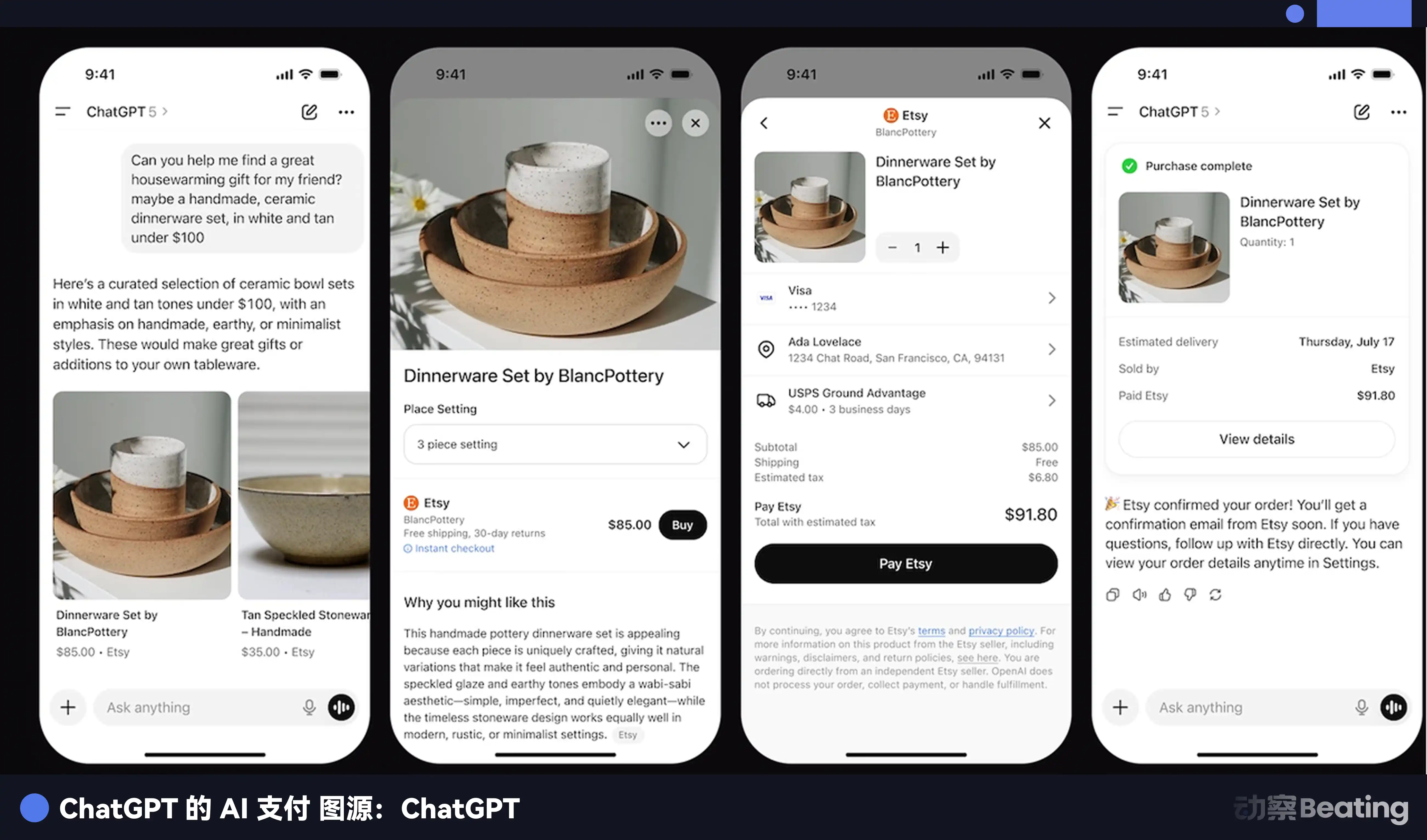

Now, when you open ChatGPT and search for any product, you will see a blue "Buy" button. Fill in the address, make the payment, and the goods are shipped. The entire process is seamless, without jumping to any webpages.

Last week, Google caught up and integrated products from Etsy and Wayfair into its search and Gemini, allowing direct checkout in conversations. Microsoft's Copilot also simultaneously launched shopping checkout features. Meta's Zuckerberg just announced a full pivot to AI-enabled commerce.

However, a more covert commercial narrative is quietly unfolding; the toll battle for AI payments will begin with two major AI payment camps in the fall of 2025.

On September 16, Google gathered over 60 companies to release an "AI Agent Payment Agreement."

The list consisted entirely of traditional financial giants: Mastercard, PayPal, American Express, along with a few allies from the tech sector.

On the 29th of the same month, Stripe and OpenAI released another set of agreements called the Agentic Commerce Protocol, abbreviated as ACP. Stripe also announced that it was testing ACP-based commerce solutions with AI players like Microsoft Copilot, Anthropic, and Perplexity.

The two lists have very few overlaps. Coinbase appears in both Google’s AP2 ecosystem and is also a long-term partner of Stripe.

What these two camps are competing over is a seemingly mundane yet trillion-dollar question: When AI spends money on behalf of humans, whose pipe does the money flow through?

You might think this doesn’t concern you. But consider this: you currently have ChatGPT help you book flights, an AI assistant comparing prices for products, or an Agent automatically purchasing office supplies. These scenarios are visibly becoming a reality. Every transaction requires a pipe to transport money from your pocket to the merchant.

Whoever builds this pipe can charge a toll on every transaction.

This is the essence of this battle.

A Round Table Changed in 12 Months

The story begins with a dinner meeting.

In the summer of 2024, Stripe hosted then-Deputy Secretary of the Treasury Wally Adeyemo in its San Francisco headquarters for a fintech roundtable.

A group of payment company executives gathered to chat, among them were two individuals who had never met before: Stripe's CEO Patrick Collison and a young man named Zach Abrams.

Abrams has quite the background. He and his partner Sean Yu are serial entrepreneurs, having sold their first company, Evenly (which handled P2P transfers, similar to the US version of Venmo), to Square (now known as Block) in 2013.

Later, Abrams joined Coinbase as the head of consumer products and also served as the Chief Product Officer at Brex; Yu has worked as an engineer at DoorDash and Airbnb. In 2022, the two teamed up again to establish Bridge, facilitating stablecoin payments for enterprises, with clients including Coinbase and SpaceX.

The topic at that roundtable was initially broad, but Abrams later recalled feeling overwhelmed: over 90% of the time was spent discussing stablecoins, even though he was the only representative from a stablecoin company present.

Prior to that, Bridge had been pursuing Stripe as a client, hoping to integrate its technology into Stripe's payment system. However, after that roundtable, the direction shifted. Collison began to frequently meet with Abrams, not to discuss collaboration, but to discuss acquisition.

In October 2024, Stripe announced it would acquire Bridge for $1.1 billion. Bridge had just closed a $40 million Series A funding round in March 2024, with a valuation of $200 million.

The acquisition price was 5.5 times the valuation; by revenue multiples, it could exceed 100 times. Sequoia Capital stated in their post-investment remarks that they believed Bridge would join the ranks of Instagram, YouTube, PayPal, and WhatsApp as a company that realized its full potential after being acquired.

By February 2025, the transaction was officially completed. Bridge's 60-person team moved into Stripe's San Francisco headquarters and participated in Stripe's new employee training camp held every two weeks.

This was just the first step.

Things progressed rapidly thereafter. In May 2025, Stripe launched stablecoin financial accounts, allowing businesses in 101 countries to hold stablecoin balances and make payments globally with stablecoins.

In the same month, ChatGPT unveiled a shopping recommendation feature, enabling users to search for products in the chat window, compare options, and then jump to the merchant's website to place orders.

In June, Stripe acquired wallet company Privy.

Privy’s function is straightforward: it enables any app to integrate a digital wallet, allowing users to make on-chain payments without needing to download any additional cryptocurrency wallet software. At that time, over 75 million accounts were already using it.

Patrick Collison tweeted a very straightforward statement: "Money has to reside somewhere, and Privy builds the world's best programmable vaults."

In September, together with crypto investment giant Paradigm, they incubated Tempo Chain, a new blockchain specifically designed for payments. Paradigm's co-founder Matt Huang (who is also a board member at Stripe) personally led the team.

The list of companies joining the Tempo design camp reads like an all-star lineup from the payments industry: OpenAI, Anthropic, Deutsche Bank, Visa, Shopify, Standard Chartered, Brazil's largest digital bank Nubank, DoorDash, Revolut, and South Korea's e-commerce giant Coupang.

Stripe CEO Patrick Collison stated that Tempo would be able to process tens of thousands of transactions per second with sub-second confirmations and charge fees of less than 0.1 cents per transaction, with transaction costs quoted in US dollar stablecoins, eliminating the need to hold highly volatile native tokens.

In the same month, Stripe and OpenAI officially released the ACP agreement, launching the Instant Checkout feature for ChatGPT — users can see recommended products in the chat window and can place orders and pay instantly without switching sites or swiping cards.

The first batch of supported merchants included Etsy, followed by millions of Shopify merchants.

In October, Tempo completed its first funding round of $500 million, led by Greenoaks and Thrive Capital, with participation from Sequoia, Ribbit Capital, and SV Angel, reaching a valuation of $5 billion. A blockchain project established for less than two months was valued at $5 billion. Stripe and Paradigm did not participate in this round of funding.

In December, Tempo opened for public testing. UBS, Mastercard, and European buy-now-pay-later giant Klarna joined the partner list.

Zach Abrams from Bridge announced simultaneously that Bridge has applied for a national bank trust charter in the United States to comply with the requirements of the stablecoin regulatory act, the GENIUS Act, which takes effect in July 2025.

Looking at these events together: acquiring the ability to issue coins for $1.1 billion, creating stablecoin financial accounts, acquiring a wallet company, incubating a dedicated blockchain, applying for a bank charter.

From issuing coins to building the blockchain to creating wallets to making agreements to obtaining licenses, Stripe did it all.

In contrast, Google brings together over 60 alliances, an open agreement, and a code repository. Google has everything but its own chain, its own stablecoin, and its own wallet.

Alliances are the result of a group of people sitting down to hold meetings. What Stripe built is a system that can go live with a single decision.

In the month Google launched the AP2, Tempo was already in testing.

No Matter Who Wins, Circle Wins

In this war, there is one role that is smarter than Stripe.

It doesn't take sides, it doesn't fight, and it doesn't even say much. But regardless of who wins, it will always win.

This role is called Circle.

Circle issues a stablecoin called USDC, which is currently the most compliant digital dollar globally.

Another company, Tether, issues USDT, which is larger in scale but has faced scrutiny over whether its reserves are sufficient and whether its audits are reliable; regulators have debated this for years without conclusion. Retail investors may not care about these concerns, but in the AI world, there could be hundreds of thousands of automated transactions each day, each needing to withstand scrutiny. No reputable company would dare base its AI transactions on a stablecoin with questionable compliance.

As for Circle? A publicly traded company on the New York Stock Exchange. The SEC has reviewed its books, releasing quarterly financial reports showing the amount of US Treasury bonds and cash reserves—the entire world can see it.

This has resulted in an interesting situation: Stripe’s stablecoin financial accounts support USDC. OpenAI uses USDC through Stripe. Coinbase in Google's camp also accepts USDC.

Two camps are fiercely competing for "entry," striving to control the interface where AI spends money and the protocols involved. But regardless of who holds the entry, the money ultimately needs to convert into stablecoins to run on the chain. In the compliant stablecoin market, USDC virtually has no competition.

Two camps vie for entry, while Circle capitalizes on transaction volumes.

Here’s a piece of data. In 2024, the total value of global stablecoin transfers reached $15.6 trillion. What does this figure represent? It is comparable to the total transaction volume of Visa in a year.

In less than a decade, something has reached parity with a network built by Visa over sixty years.

And AI trading has only just begun. Consulting firm Edgar Dunn & Co. predicts that by 2030, AI-driven transactions will total $1.7 trillion. Each of these $1.7 trillion transactions will likely flow through stablecoin pipes.

US Treasury Secretary Scott Bessent publicly stated at a Senate hearing in June 2025 that a stablecoin market value of $2 trillion is a "very reasonable expectation."

Patrick Collison himself has said: the average interest rate on US bank deposits is only 0.40%, and $4 trillion of bank deposits are earning zero interest.

He thinks this consumer-unfriendly practice is a "loser strategy" and that young people will inevitably switch their money into higher-yielding stablecoins.

He is talking about a trend. And Circle just happens to be at the heart of that trend.

Epilogue

Finally, let’s zoom out a bit.

This battle over AI payment standards appears to be a turf war between two commercial camps. But it reflects a deeper issue: as AI begins to independently engage in economic activities, is the financial system designed for humans still adequate?

Patrick Collison envisions a future where AI Agents are the primary participants in economic activities. They compare prices, make purchases, handle payments, and settle transactions—entire processes without any human needing to press a button. This is the pinnacle of efficiency and the boundary of risk.

The Google and traditional finance alliance envisions another future: AI should be integrated into existing human financial infrastructure, constrained by current regulatory rules, operating within established trust frameworks.

Two futures, two logics, two camps.

However, regardless of which future comes to pass, one thing is certain: AI will spend money, and the money will need to move on the chain, with stablecoins required for settlement on the chain.

Thus, Circle continues to win. Stripe and Google continue to compete. Regulators continue to chase. Merchants continue to engage. Consumers remain unaware of which pipe their money flows through.

Until one day, something you bought with AI goes wrong, and you discover that neither anyone nor the AI knows whom to approach for a refund.

On that day, everyone will suddenly remember the questions that went unanswered today.

But by that day, the pipes will have been fixed, and tolls will have started to be collected.

History is always like this: first get on the bus, then buy the ticket.

Only this time, the bus is going too fast.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。