Translation: Block unicorn

Introduction

Hello everyone in the Year of the Horse, last week, two highly watched emerging financial companies released their financial reports within 48 hours. Neither company's revenue met expectations. Both companies were quickly placed into the same narrative framework: the cryptocurrency market is sluggish, trading volume is weak, and good times are over.

But this viewpoint completely misses the point.

Coinbase and Robinhood's stock price trends may be closely related to Bitcoin (BTC) prices, but their future trajectories are not determined by BTC's performance in the fourth quarter. They are gradually shaking off the narrow definition that "the fate of the company is closely linked to the cryptocurrency cycle."

Both companies are undergoing significant transformations—if you know where to look, you can see this from their financial data—but if you only look at the complex data from the last quarter, you might completely overlook these changes.

But things are not as murky as they appear. Just take a look at the data from the past few quarters and compare it with the series of product announcements both companies have made over the past 12 months, and the picture becomes clear.

The long-term development trends of both companies tell us their respective directions, their bets on the future of finance, and crucially, when their development paths began to converge.

In today's analysis, I will dissect their stories individually, then explain their commonalities and what this reveals about the broader competitive landscape they are in.

Part One: Coinbase - A Bet on Infrastructure

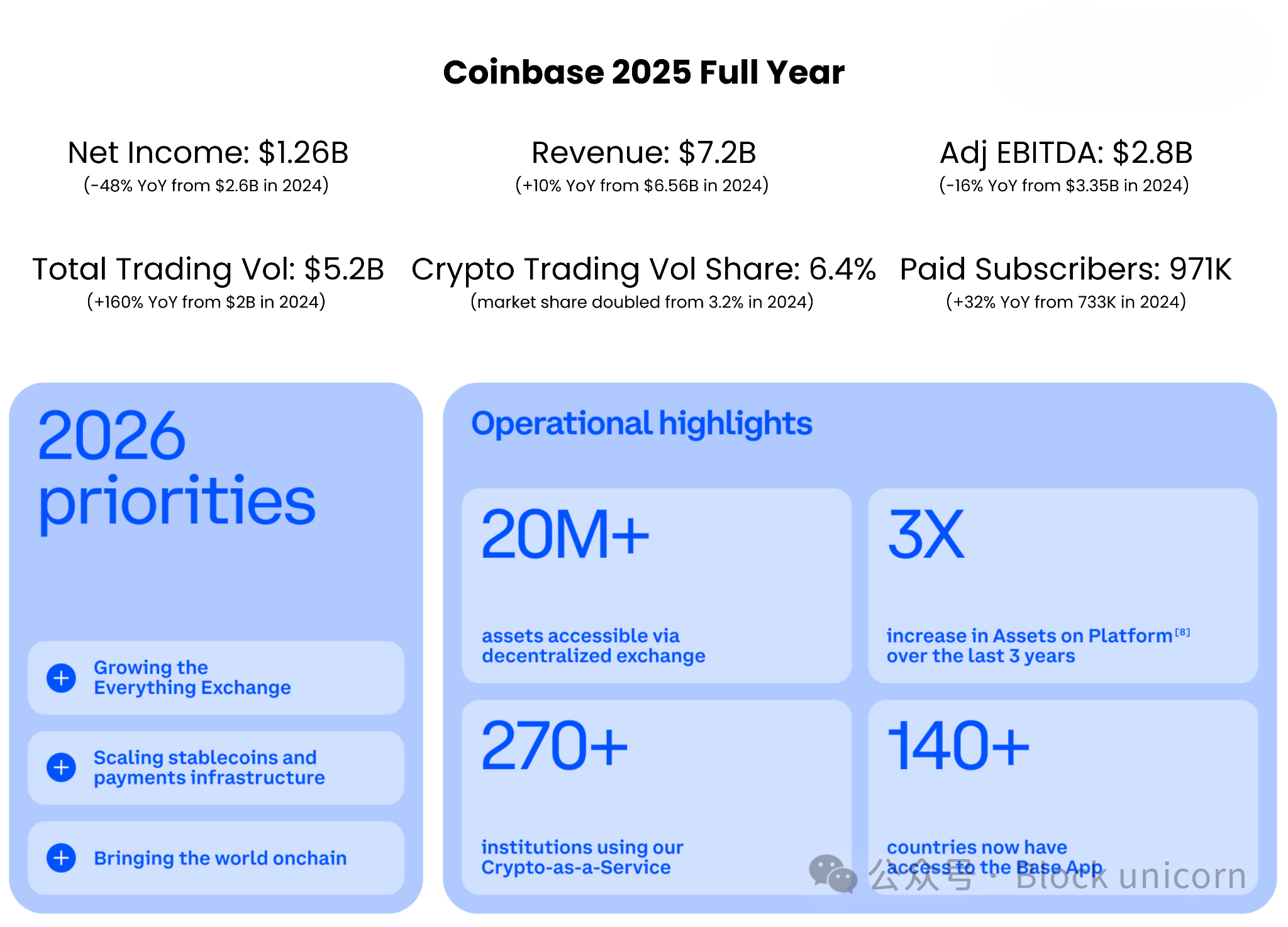

Coinbase recorded a net loss of $666 million in the fourth quarter of 2025, which might make this quarter feel disappointing. But the numbers need to be interpreted in context. During that quarter, Coinbase also experienced an unrealized loss of $718 million on its cryptocurrency holdings, and it recorded an impairment loss of $395 million on its investment in Circle. Excluding these non-cash accounting losses, Coinbase still maintained adjusted profitability for 12 consecutive quarters.

The report indicates that adjusted profit was $178 million, and adjusted EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) was $566 million.

While this may be reassuring, there is something else I find even more noteworthy.

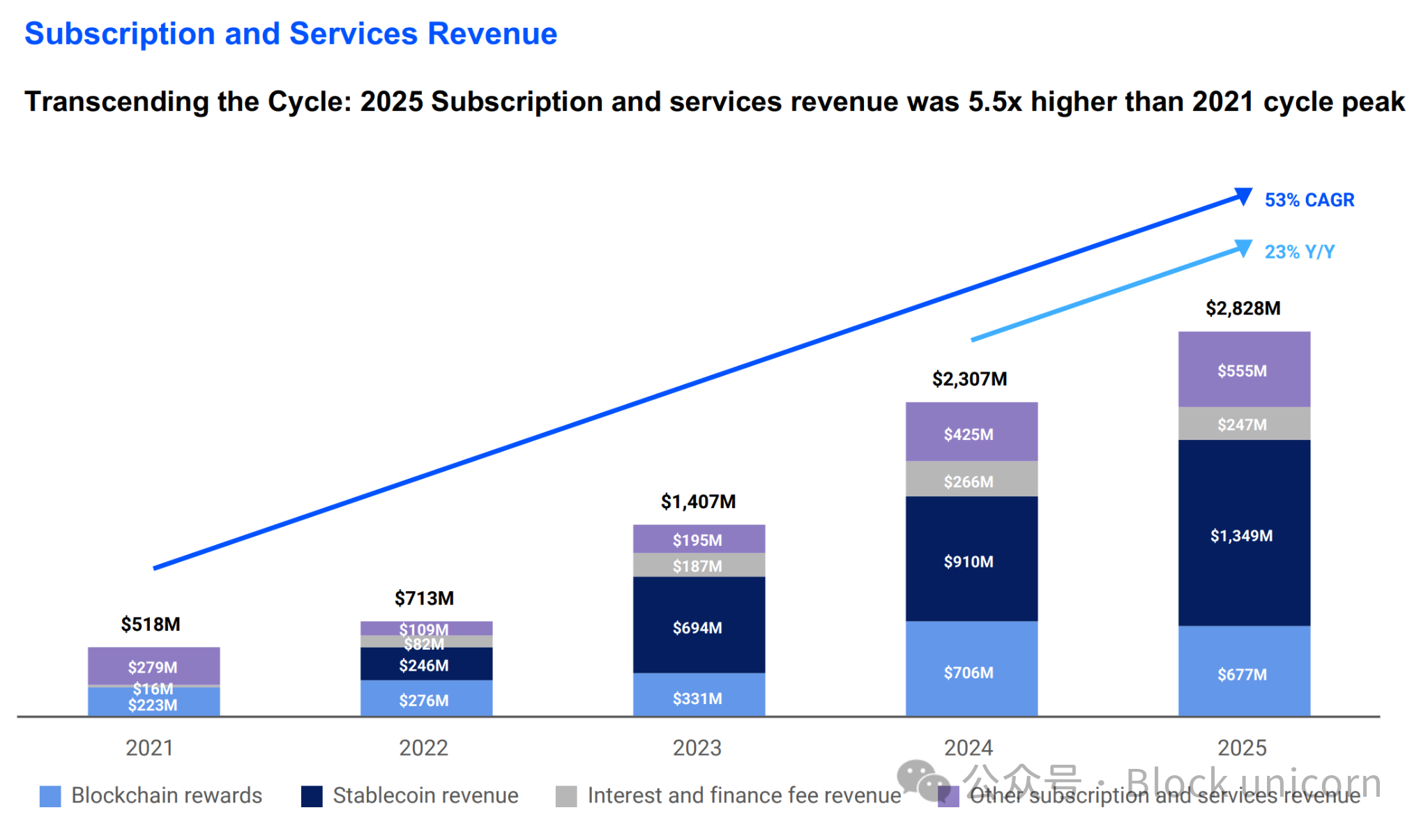

Coinbase's subscription and services (S&S) revenue reached $2.8 billion in 2025, a 5.5-fold increase from the peak of the 2021 cycle, and double that of 2023. This indicates that Coinbase's revenue base is constantly expanding, covering areas like stablecoins, custody, and blockchain rewards. In the fourth quarter, the amount of USDC held in Coinbase products reached an all-time high of $17.8 billion, an 18% quarter-over-quarter increase. Currently, Coinbase holds more cryptocurrency than any other company worldwide, accounting for 12% of the global cryptocurrency holdings.

However, this revenue is highly sensitive to interest rate changes. When interest rates and cryptocurrency prices fall, the yields on stablecoins, staking rewards, and custodial balance interest income decrease. This is evident from the company's guidance for the first quarter of 2026, which expects revenue from stablecoins and custody business to drop from $727 million in the fourth quarter to between $550 million and $630 million.

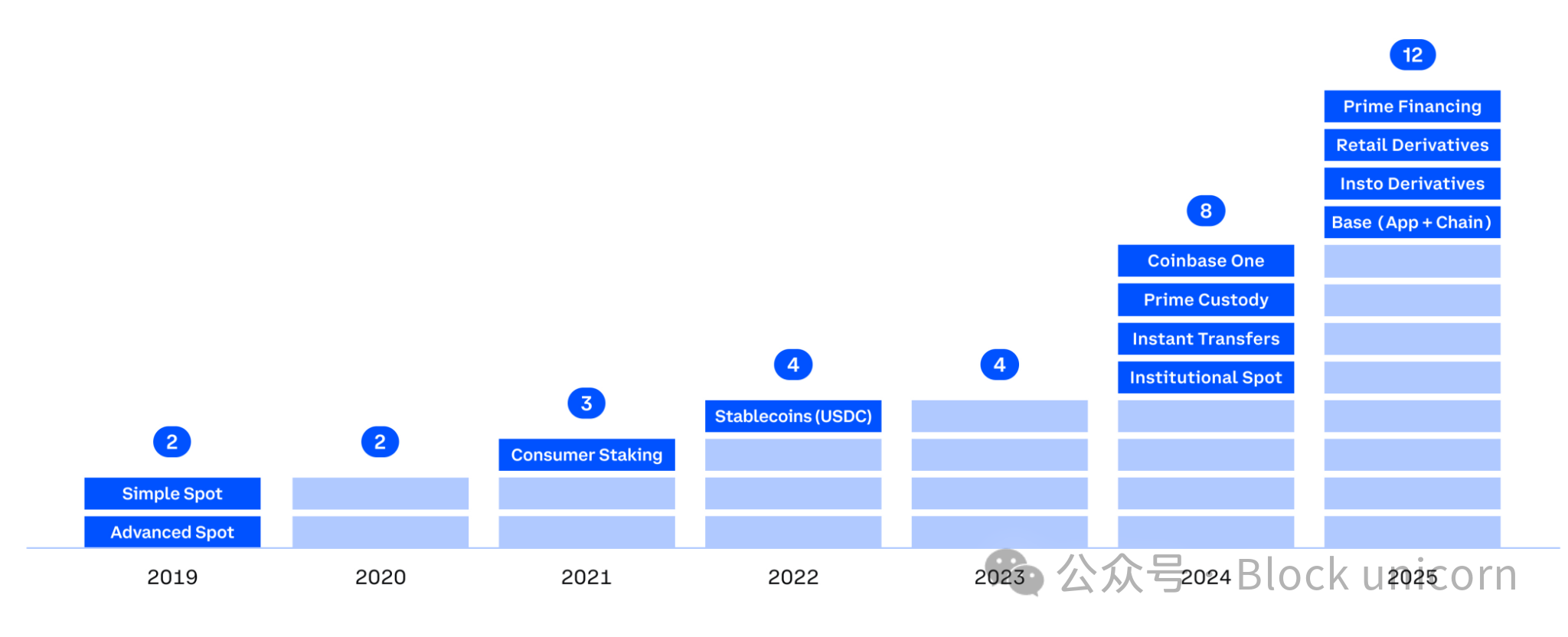

Coinbase is engaging in systematic diversification across multiple business areas, reducing its reliance on cryptocurrency cycles, which should enhance investor confidence. Currently, Coinbase has 12 business segments with annual revenues exceeding $100 million, six of which exceed $250 million, and two exceed $1 billion.

The acquisition of Deribit by Coinbase is the largest cryptocurrency transaction ever, enabling the company to capture high volume derivatives trading market, especially when the spot market is extremely volatile.

Coinbase's "Everything Exchange" vision is beginning to manifest in more areas beyond traditional finance. Earlier this week, Armstrong revealed on Twitter that the world's five largest globally systemically important banks (G-SIBs) are partnering with Coinbase.

JPMorgan has signed an agreement allowing clients to directly link their bank accounts to Coinbase. BlackRock's Bitcoin ETF custody service also operates through Coinbase's infrastructure. These attempts indicate that Coinbase's long-term goal is to become the settlement layer that large institutions can tap into during their financial onboarding process.

The recently launched forecasting markets by Coinbase also follow the same model aimed at retail customers. The forecasting markets went live two weeks ago, further expanding Coinbase's "everything can be traded" vision by introducing event-based trading. This creates an entirely new asset class, bringing new revenue sources to Coinbase and providing customers even more reasons to keep their assets on Coinbase instead of transferring them to other platforms.

Though the short-term performance of this new business line may not be large, its strategic intent is evident. How do I know? The forecasting market has become the fastest-growing business line for Robinhood, which is the best evidence.

Now, let’s take a look at the other side...

Part Two: Robinhood - Consumer Deep Gaming

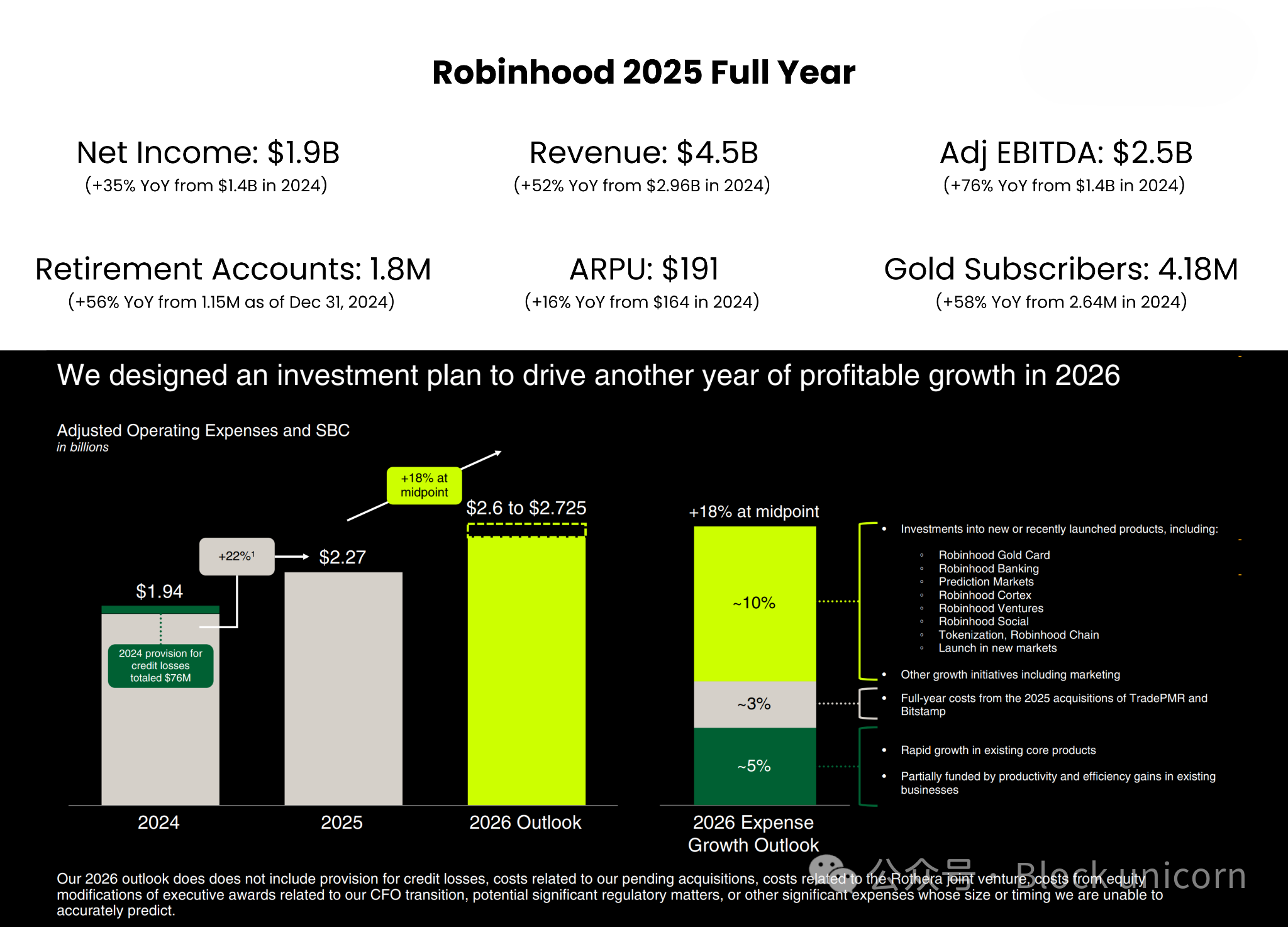

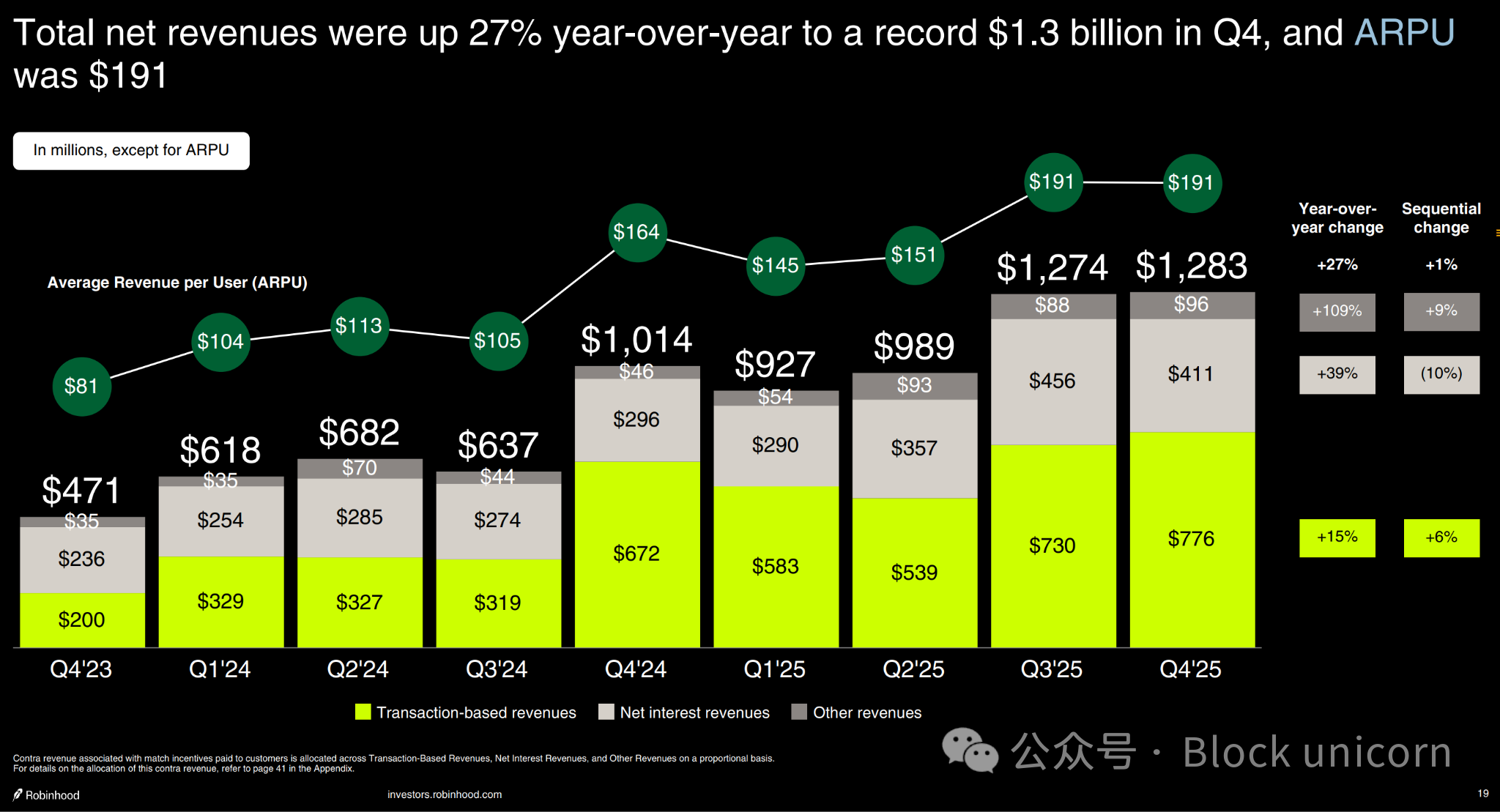

Robinhood's fourth quarter performance was actually quite good, but it was penalized for some inappropriate reasons. Due to the decline in cryptocurrency trading volume and the end of the football season, its revenue did not meet expectations, but for me, these are not the focus.

Most notably, its average revenue per user (ARPU) increased by 27% year-over-year to $191, while the number of paid users only grew by 7% during the same period. This indicates that Robinhood has earned more income from each customer without the need to rapidly expand its user base. Compared to its business model when it went public in 2021, this is a more diversified business model.

Where does the growth in ARPU come from? Partly from the rapidly growing "other trading revenue," which increased by 300% year-over-year to $147 million, primarily driven by forecasting markets. Some of the growth also came from options business, which grew by 41% to $314 million. Additionally, growth in net interest income and gold subscription business also contributed to revenue.

Despite cryptocurrency revenue based on trading growing over 40% year-over-year in 2025, still $8 out of every $10 in Robinhood's revenue comes from non-cryptocurrency business. This ensures that the company has a lower degree of reliance on cryptocurrency cycles.

$300 Million Business

The biggest indicator of the future development trajectory for Robinhood lies in the performance of its forecasting market. CEO Vlad Tenev described this product line, launched less than a year ago, as Robinhood's fastest-growing business in history, which speaks volumes about its importance. This product line achieved an annualized revenue of $300 million and $12 billion in contract trading volume in its first year, indicating a clear outlook for future development.

Robinhood has also increased its investment in forecasting markets by establishing a joint venture, Rothera LLC, with Susquehanna. Rothera LLC acquired MIAXdx in January 2026. This transaction gave Robinhood its own CFTC-licensed exchange and clearinghouse. This layer helps Robinhood build the infrastructure for its forecasting market, enabling it to control the pricing, contract selection, and economic models for these markets.

Although the NFL season has ended, some short-term favorable factors make Robinhood's forecasting market more resilient. In January, NBA contracts traded on the platform surpassed NFL contracts. A government shutdown also led to a significant increase in trading volume in the same week the NFL season ended. Additionally, there will be the FIFA World Cup this summer, following the ongoing Winter Olympics. Besides, Robinhood is also building a brand new non-sports field.

Diversification Challenges

In addition to the forecasting market and Robinhood's current profit models (including options, margin, and gold subscriptions), there are some other factors that will enhance investor confidence. $HOOD is also building the next layer of distribution channels through private markets, family investments, and banking services.

Robinhood Banking officially launched a few months ago for its first customers. As of the end of January, it had 25,000 paying customers with total deposits of $400 million. More than half of the customers have activated direct deposit services, and Tenev considers this to be the most encouraging sign. This indicates that these customers are moving their financial lives into the Robinhood ecosystem, rather than just experimenting. However, compared to this platform's market value of $324 billion, $400 million in deposits is still trivial. Banking is a long-term developmental process, and Robinhood must be prepared to face the challenges in this area.

While the world is busy building forecasting markets, I believe the private market could become Robinhood's winning secret weapon, a field with few competitors involved. Tenev also believes that the potential scale of private markets may "surpass forecasting markets." Robinhood Ventures is Robinhood's registered fund aimed at providing retail investors the opportunity to invest in private companies, which has not yet officially launched. However, last year, European users experienced some through a stock token giveaway activity from OpenAI and SpaceX, which also sparked some controversy at the time. Robinhood Ventures will officially launch in the U.S. in 2026, with a huge potential market size. Tenev has repeatedly mentioned the ongoing $100 trillion intergenerational wealth transfer. If Robinhood can get a piece of that pie, even just as private assets shift from institutional investors to retail investors, it would dramatically change its income structure.

The bigger challenge lies in how to manage client expectations by clearly defining the boundary between tokenized equity and traditional equity.

The private market as a source of revenue may launch in 2026 but could gradually be realized over a longer period.

Same Destination, Different Timing

At first glance, the development paths of Coinbase and Robinhood seem entirely different. Indeed, they started from two extremes in the financial sector. However, they are now moving towards the same vision: to become a financial super app. Their recent development history confirms this.

Robinhood entered the financial sector in a traditional manner: offering commission-free stock trading, designed for users who found traditional broker fees too high and operations too complex. For five years, it has been building cryptocurrency-native infrastructure on top of traditional finance (TradFi). Now, it offers margin accounts, gold subscriptions, credit cards, banking products, derivatives exchanges, forecasting markets, and tokenization strategies.

Coinbase was born in the cryptocurrency field, providing the most trustworthy way to purchase, store, and trade digital assets when most companies on Wall Street avoided cryptocurrency. Over the past five years, Coinbase has gradually expanded from its cryptocurrency-native core business to existing consumer products in traditional finance, such as stocks, subscription services, credit cards, and now forecasting markets.

Both are rapidly converging towards the middle ground from opposite directions, where competition in retail finance will unfold over the next decade.

Forecasting markets currently serve as the stage where their direct confrontation can be clearly seen. Robinhood takes the lead in this regard, seizing the initiative over Coinbase, which was only launched two weeks ago. $HOOD also has its own exchange and clearinghouse, while $COIN has collaborated with Kalshi but has not signed an exclusive agreement.

Tokenization will be another area of competition that is more complex. Coinbase sees it as an infrastructure issue, enabling on-chain trading of bonds and securities by issuing tokenized stocks internally and establishing regulatory relationships. Meanwhile, Robinhood views it as a consumer access issue, enabling trading through open-tokenized stocks of private companies. Both have chosen different paths to address different aspects of the same problem.

The private market may become the third area where these two companies intersect. Coinbase has achieved on-chain capital formation through the acquisition of Echo, while Robinhood is taking its first steps to bring private company investments to retail users through its Ventures.

Both companies understand that the broader market will trust the financial service that can establish the deepest financial relationships and meet the growing needs of investors, which is typically one of the hardest areas for a market to accept. People do not easily change banks, brokers, or custodial institutions. If a platform enables users to manage their retirement accounts, bank card information, forecasting market positions, and ultimately manage their private equity portfolios, then it will be challenging for another platform to take customers away from a competitor.

The analysis concludes here, see you in our next article.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。