Recently, the Hong Kong Special Administrative Region ("Hong Kong") Inland Revenue Department updated its Frequently Asked Questions (FAQs), clarifying how to determine the tax residency status of individuals who may simultaneously be considered residents in both the Mainland and Hong Kong according to the rules of the Comprehensive Avoidance of Double Taxation Agreement between the Mainland and Hong Kong ("Comprehensive Arrangement").

As the economic interactions between the two regions become increasingly close, cross-border work and living between the two places have become the norm, with many people living a "working in Hong Kong, living in the Mainland" lifestyle. When individuals meet the residency criteria in both places, the tax system's application relies heavily on the tie-breaker rules.

Click here to read the original text

Overview of Tax Arrangements between Mainland China and Hong Kong

Mainland Side:

A Mainland tax resident individual refers to a person who has a domicile in China, or a person who does not have a domicile in China but has resided in China for a cumulative total of more than 183 days in a tax year. Here, "domicile" is defined as a place where a person habitually resides in China due to household registration, family, or economic interest. In practice, the Mainland uses habitual residence as the core standard, and retaining a Mainland household registration may likely be presumed to indicate an intention of habitual residence, thus being recognized as a Mainland tax resident.

Hong Kong Side:

A Hong Kong tax resident individual refers to a person who usually resides in Hong Kong, or a person who stays in Hong Kong for more than 180 days during the relevant tax year or stays in Hong Kong for more than 300 days during two consecutive tax years. Compared to the Mainland, Hong Kong's determination of tax resident individuals focuses more on factual residency status and the degree of economic connection, rather than legal permanent residency status or household registration.

Given the objective existence of differences in tax systems regarding residency identification and tax year calculations, cross-border workers may simultaneously meet the residency standards of both regions, facing the issue of tax conflicts arising from dual residency. On August 21, 2006, the Mainland and Hong Kong formally signed the "Comprehensive Arrangement" to avoid double taxation and prevent tax evasion, and thereafter, both sides successively signed multiple protocols to update the content to reflect the development of international tax rules and promote economic and investment exchanges between the two regions.

Tax Residency Determination Logic: Tie-breaker Rule

To resolve tax jurisdiction conflicts, the "Comprehensive Arrangement" introduced the tie-breaker rule, which is widely used in the international tax field as a significant rule for resolving conflicts of dual tax residency caused by differences in the laws of various tax jurisdictions.

According to the tie-breaker rule under the "Comprehensive Arrangement," for individuals who meet the tax residency standards of both the Mainland and Hong Kong, their tax residency status is determined in the following order:

1. Where they have a permanent home;

2. The party with which they have a closer personal and economic relationship;

3. Where they have habitual residence;

4. Decided by mutual agreement between the competent authorities of both parties.

It is particularly noted that these criteria are arranged in order of priority, and the subsequent criterion is only used if the preceding criterion cannot resolve the issue.

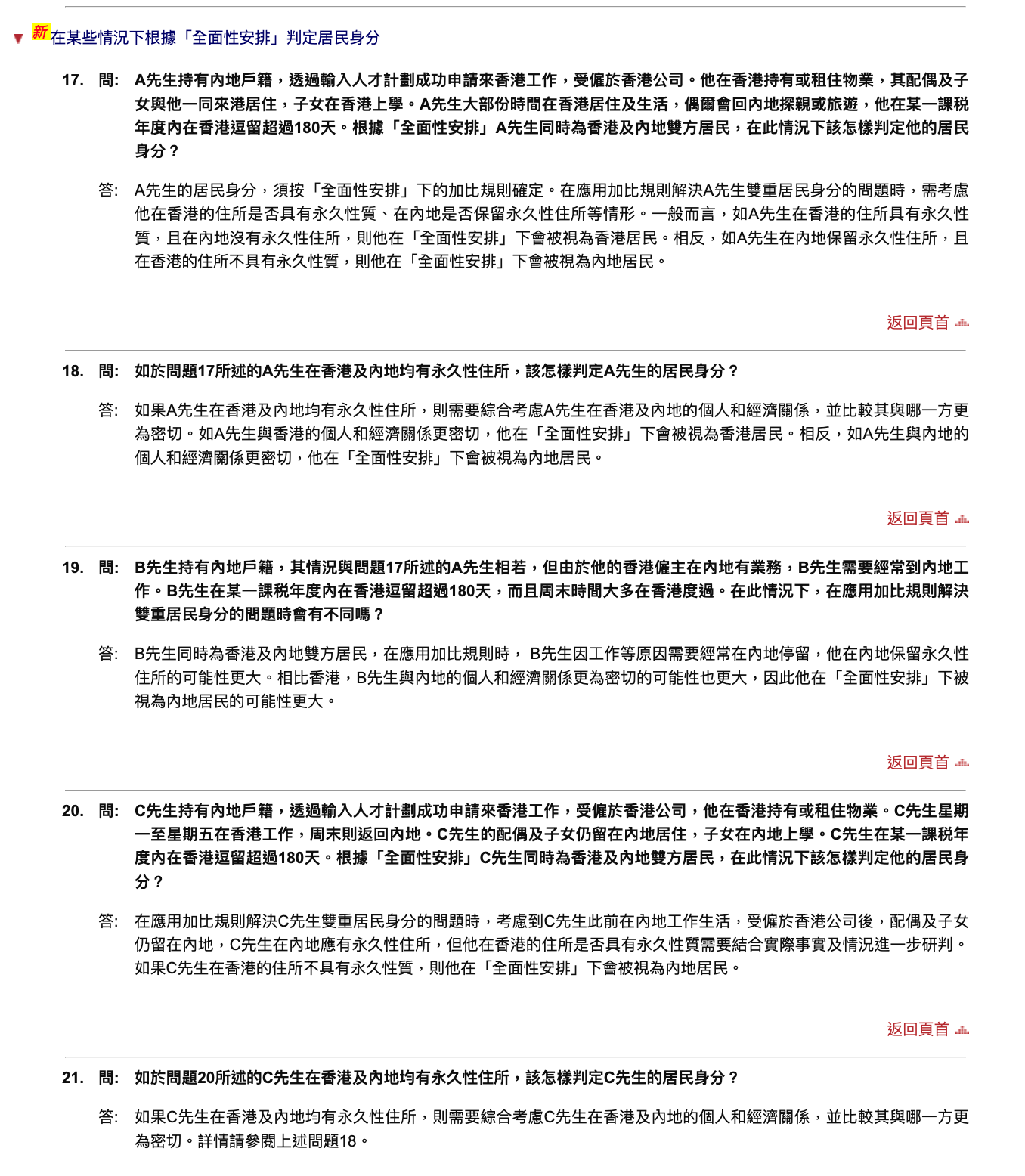

FAQ Update: How the Tie-breaker Rule is Applied in Real Scenarios

The significant importance of this FAQ update lies in the use of more realistic scenarios (Q17-Q21) to demonstrate how to determine individual tax residency status based on the tie-breaker rule in common situations, such as the "Talent Scheme" and "Dual City Living."

For various scenarios, the Hong Kong Inland Revenue Department has not provided absolute answers on tax residency identification, but has listed factors that may be considered when determining residency status, including: individual household registration in the Mainland; long-term residence, work, and study locations of core family members such as spouses and children; held business equity; the location of salary payments and social security contributions, etc. These factors constitute strong evidence of "close economic connections."

Thus, possessing a household registration in the Mainland and whether an individual stays in Hong Kong for more than 180 days in a tax year, among other singular factors, is not a decisive factor under the tie-breaker rule for determining residency status; under the "Comprehensive Arrangement," they may still be regarded as a Hong Kong resident. This does not imply that "length of stay" and other core criteria are unimportant, but rather that the tie-breaker rule assesses a combination of various factors comprehensively.

Conclusion

Overall, the recent update to the FAQs by the Hong Kong Inland Revenue Department does not represent a significant adjustment at the institutional level, but rather serves as a vivid practical guide—further clarifying the rules for determining tax residency status for frequently cross-border individuals. With the enhancement of tax regulatory capacities and increased transparency of tax-related information, tax authorities in both regions are expected to make more precise determinations regarding individuals' economic interests, and cross-border tax management is developing toward a more refined direction.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。