"The price of Bitcoin may reach an all-time high in the first half of 2026."

Author: Grayscale

Translation: Deep Tide TechFlow

Key Points

We anticipate that 2026 will accelerate structural changes in the digital asset investment space, driven primarily by two key trends: an increasing macro demand for alternative value storage tools and enhanced regulatory clarity. The combination of these two trends is expected to attract more capital inflows, expand the adoption of digital assets (especially among wealth management and institutional investors), and further integrate public blockchains into mainstream financial infrastructure.

Therefore, we expect to see an increase in digital asset valuations in 2026, and the theory of the "cryptocurrency four-year cycle" (i.e., the crypto market follows a cycle every four years) will be declared over. We believe that the price of Bitcoin may reach an all-time high in the first half of 2026.

Grayscale expects bipartisan-supported legislation on crypto market structure to become law in the United States in 2026. This will further promote the deep integration of public blockchains with traditional finance, facilitate compliant trading of digital asset securities, and potentially allow startups and established companies to issue securities on-chain.

The outlook for fiat currency is increasingly uncertain; in contrast, we can be highly confident that the 20 millionth Bitcoin will be mined in March 2026. Due to the rising risks associated with fiat currency, we believe that digital currency systems like Bitcoin and Ethereum, due to their transparency, programmability, and ultimate scarcity, will increasingly be favored by market demand.

We expect that more crypto assets will be offered through exchange-traded products (ETPs) in 2026. These investment tools have already achieved initial success, but many platforms are still conducting due diligence and working to incorporate crypto assets into their asset allocation processes. As this process matures, we anticipate that more slow-moving institutional capital will enter the market in 2026.

Additionally, we have outlined the top ten themes for crypto investment in 2026, reflecting the wide range of use cases emerging from public blockchain technology. For each theme, we include the related crypto assets. Specifically:

The risk of dollar depreciation drives demand for currency alternatives

Regulatory clarity supports the adoption of digital assets

The influence of stablecoins will grow with the push of the GENIUS Act

Asset tokenization reaches a turning point

Blockchain technology goes mainstream, with privacy solutions urgently needed

AI centralization spurs demand for blockchain solutions

DeFi accelerates, with lending leading the way

Mainstream adoption requires next-generation infrastructure support

Focus on sustainable revenue models

Investors default to seeking staking yields

Finally, we believe that the following two topics will have limited impact on the crypto market in 2026:

Quantum Computing: While research and preparations for post-quantum cryptography continue, we believe this issue will not significantly affect market valuations in the coming year.

Digital Asset Trusts (DATs): Despite widespread media attention, we believe DATs will not become a major factor influencing the digital asset market in 2026.

2026 Digital Asset Outlook: The Dawn of the Institutional Era

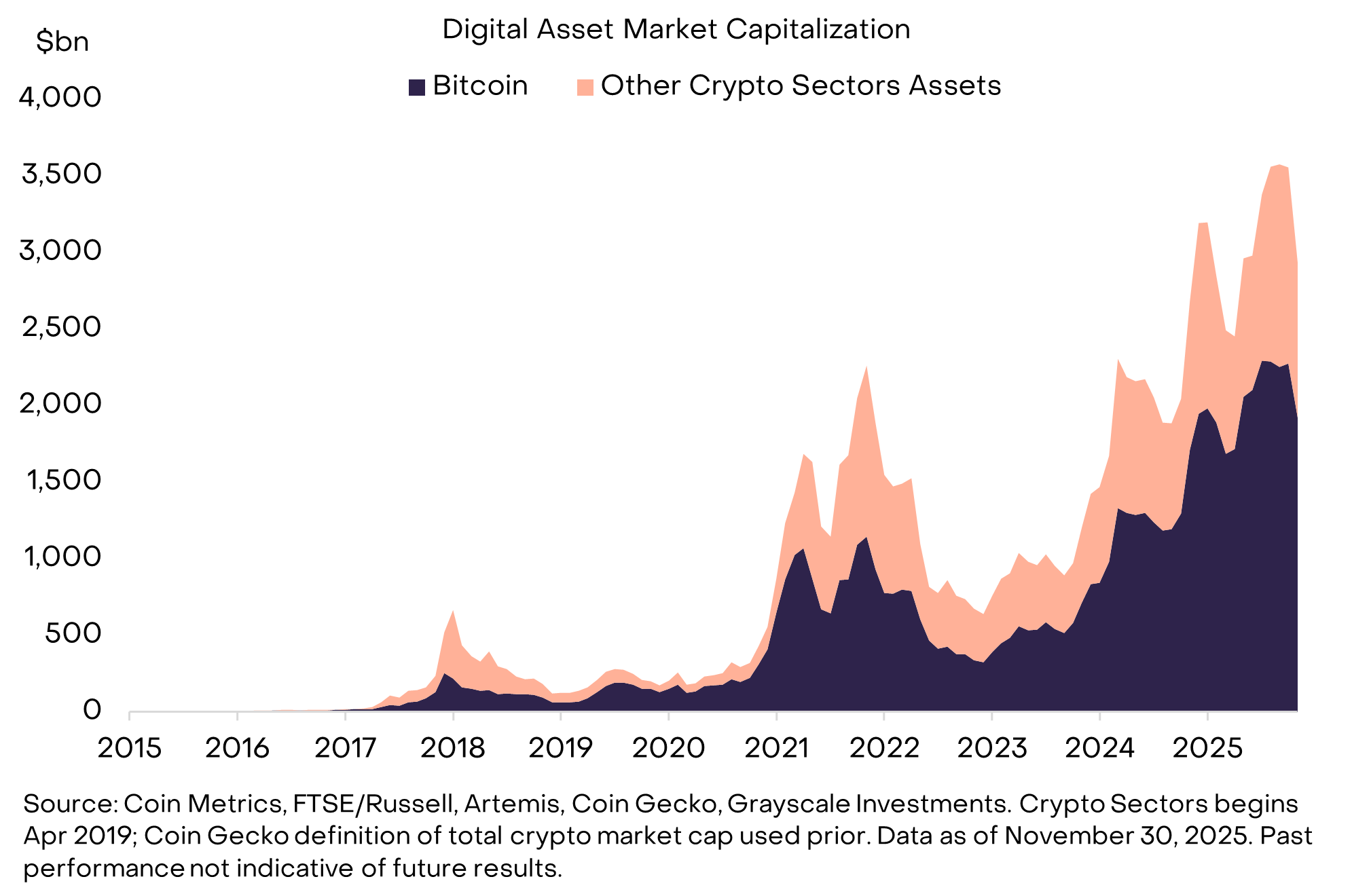

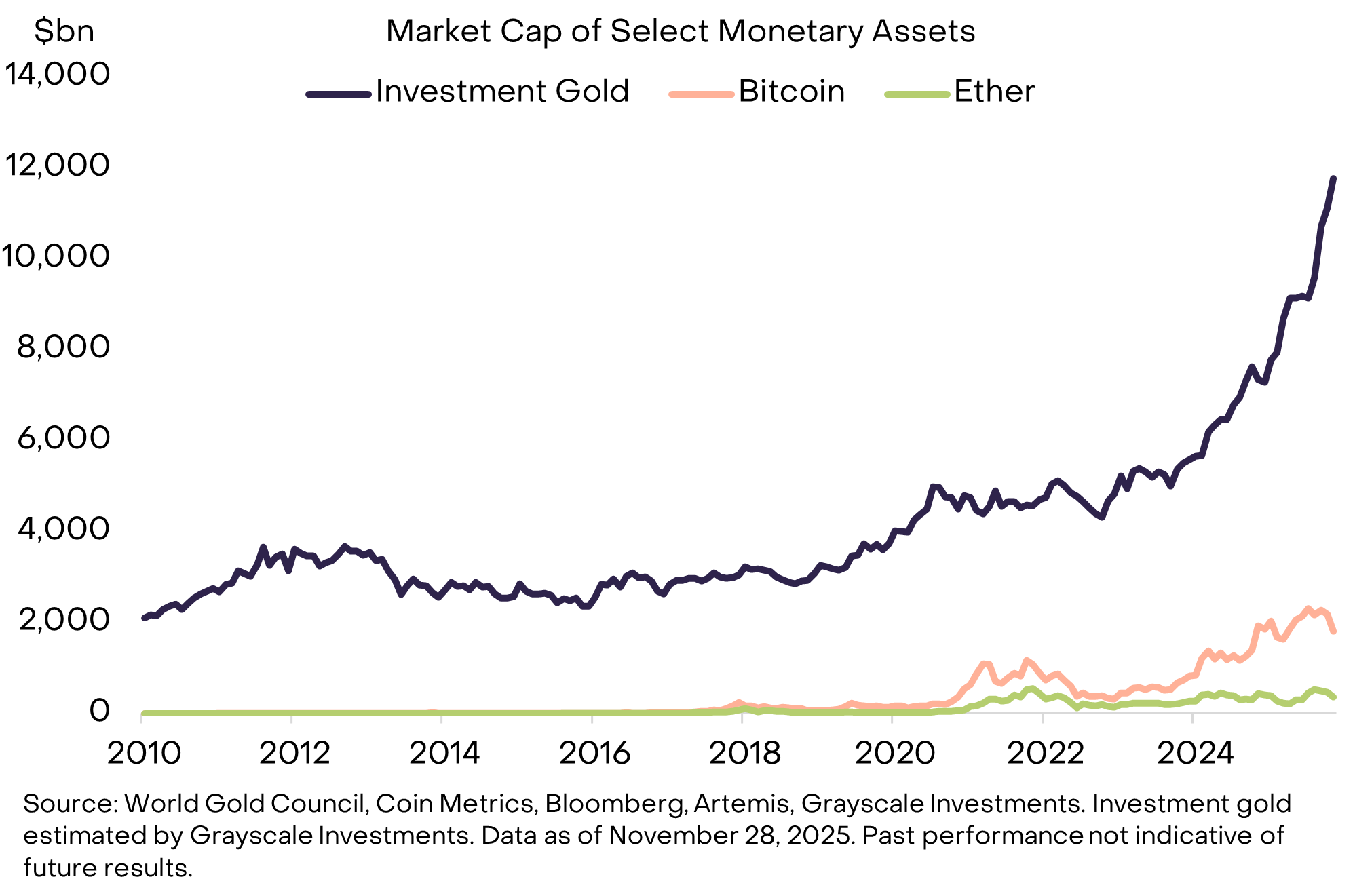

Fifteen years ago, cryptocurrency was just an experiment: there was only one asset (Bitcoin), with a market cap of about $1 million. Today, cryptocurrency has become an emerging industry and a medium-sized alternative asset class, encompassing millions of tokens with a total market cap of about $3 trillion (see Figure 1). Currently, the increasingly sophisticated regulatory frameworks in major economies are driving the deep integration of public blockchains with traditional finance, bringing long-term capital inflows to the market.

Figure 1: Cryptocurrency has now become a medium-sized alternative asset class

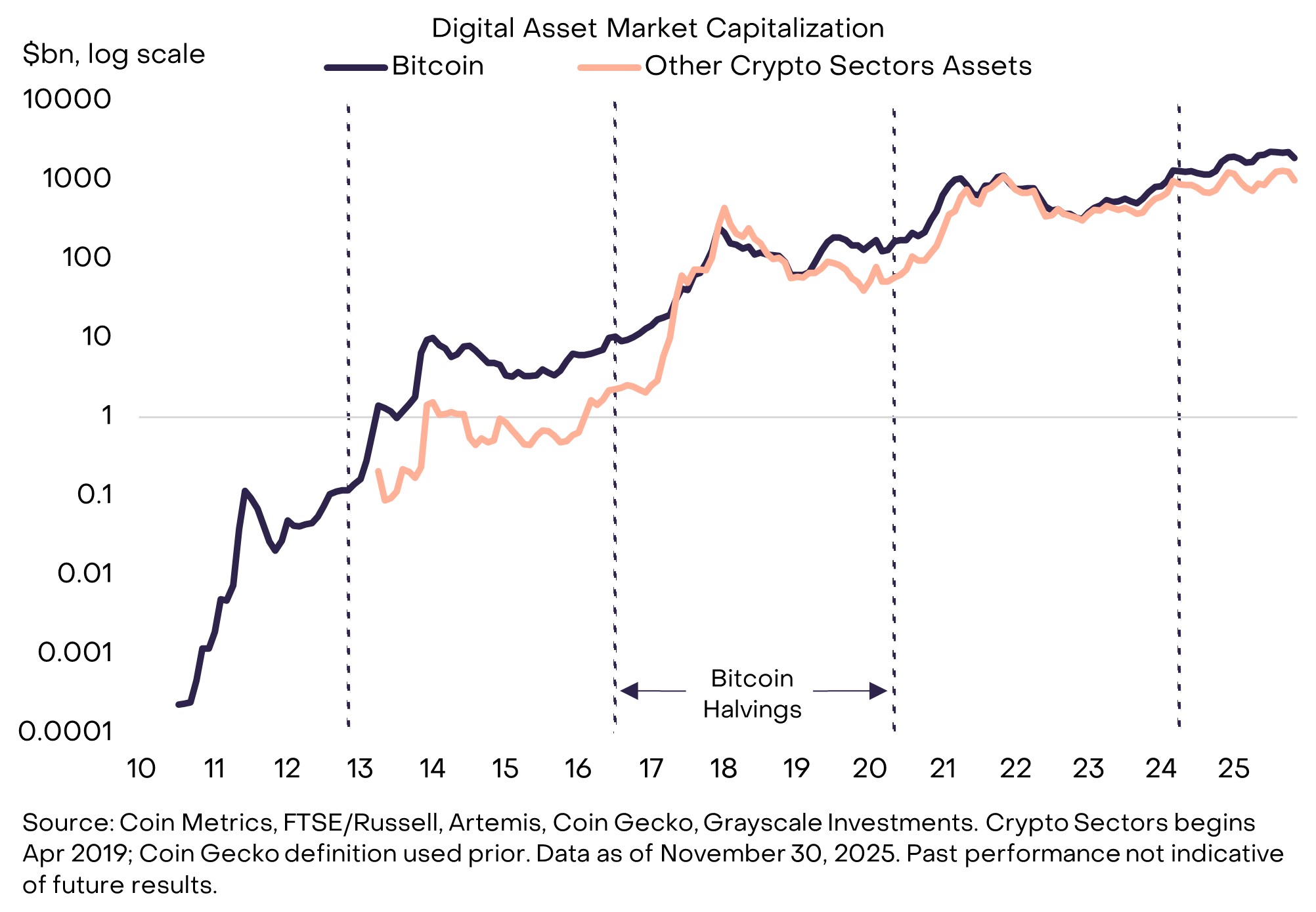

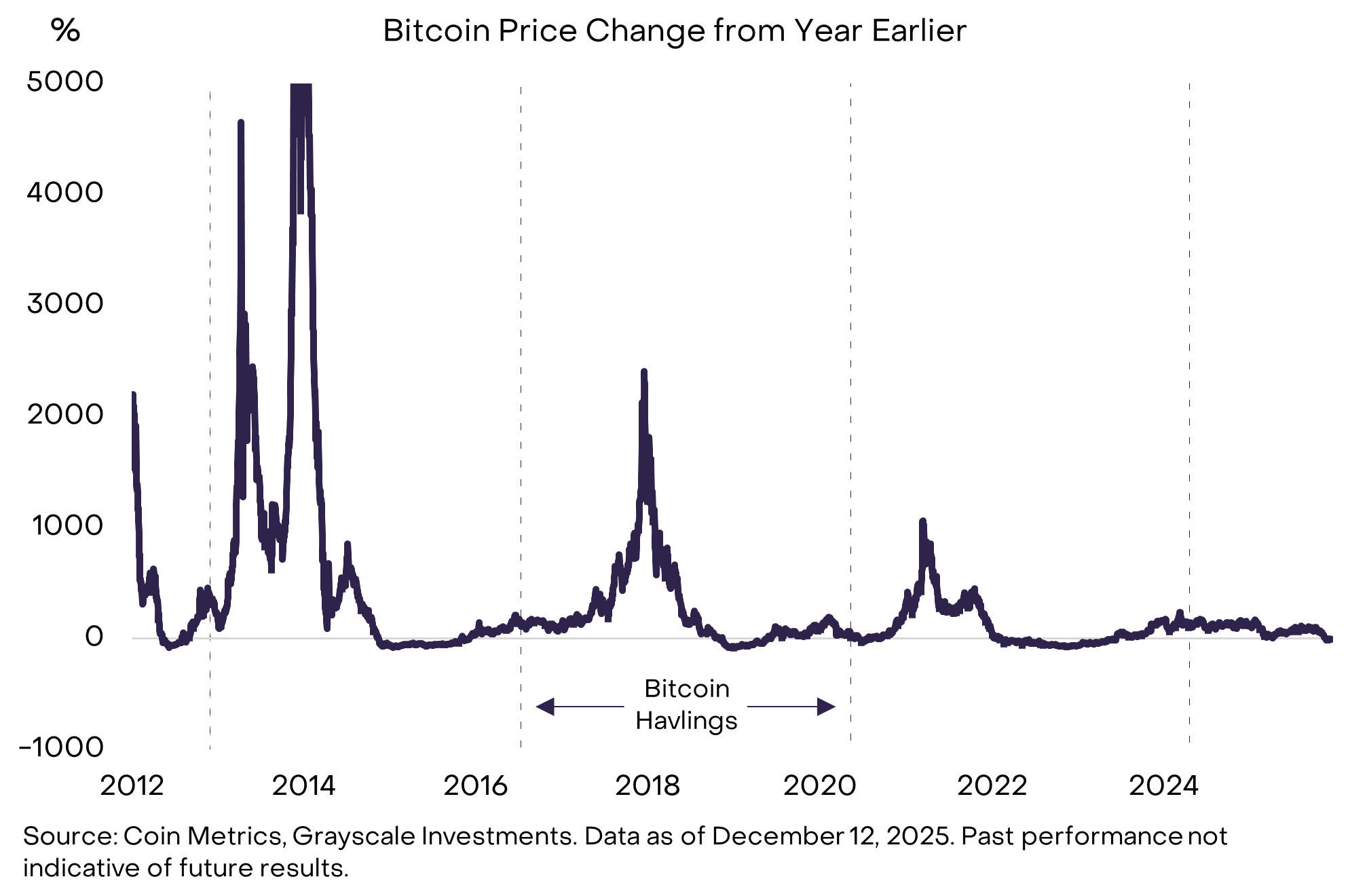

Throughout the development of cryptocurrency, token valuations have experienced four major cyclical corrections, approximately every four years (see Figure 2). In three of these cases, the cyclical peaks in valuations occurred 1 to 1.5 years after Bitcoin halving events, which happen every four years. The current bull market has lasted over three years, and the most recent Bitcoin halving occurred in April 2024, more than 1.5 years ago. Therefore, some market participants traditionally believe that Bitcoin's price may have peaked in October 2025, making 2026 a challenging year for cryptocurrency returns.

Figure 2: The rise in valuations in 2026 will mark the end of the "four-year cycle theory"

Grayscale believes that the crypto asset class is in a sustained bull market and predicts that 2026 will mark the end of the "explicit four-year cycle." We expect that valuations across all six major crypto asset sectors will rise in 2026, and we believe that Bitcoin's price may break previous all-time highs in the first half of the year.

Our optimistic outlook is supported by two pillars:

First, the macro demand for alternative value storage tools continues to grow.

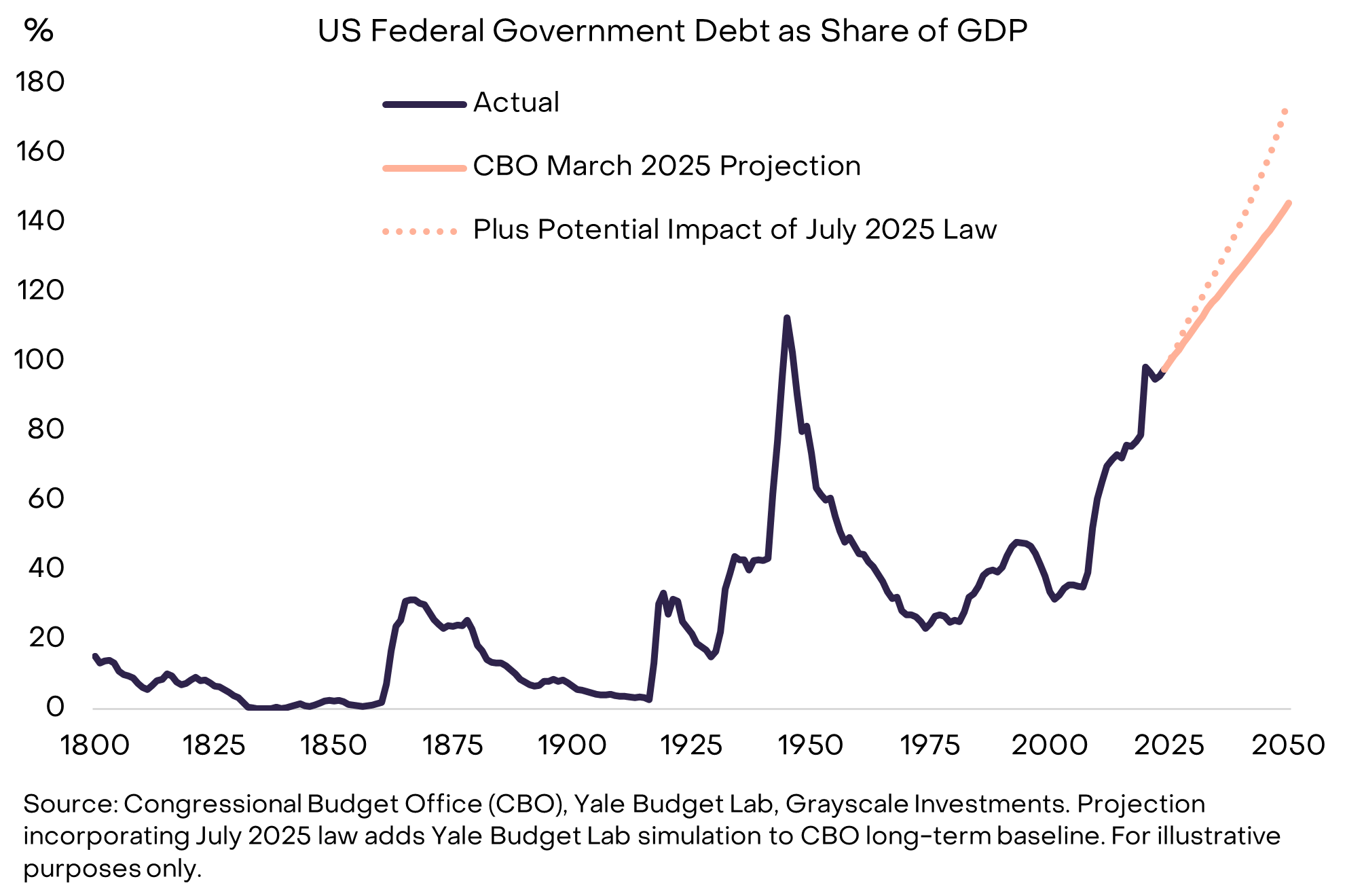

Bitcoin and Ethereum, as the two largest cryptocurrencies by market cap, can be viewed as scarce digital commodities and alternative currency assets. Due to high public sector debt and its potential impact on long-term inflation (see Figure 3), fiat currencies (and assets priced in fiat) face additional risks. Whether it is physical gold and silver or digital Bitcoin and Ethereum, these scarce commodities have the potential to serve as a " ballast" in portfolios to hedge against fiat currency risks. In our view, as long as the risk of fiat currency depreciation continues to rise, the demand for Bitcoin and Ethereum in investment portfolios may also continue to increase.

Figure 3: The U.S. debt issue raises questions about the credibility of low inflation

Second, regulatory clarity is driving institutional investment into the public blockchain technology space.

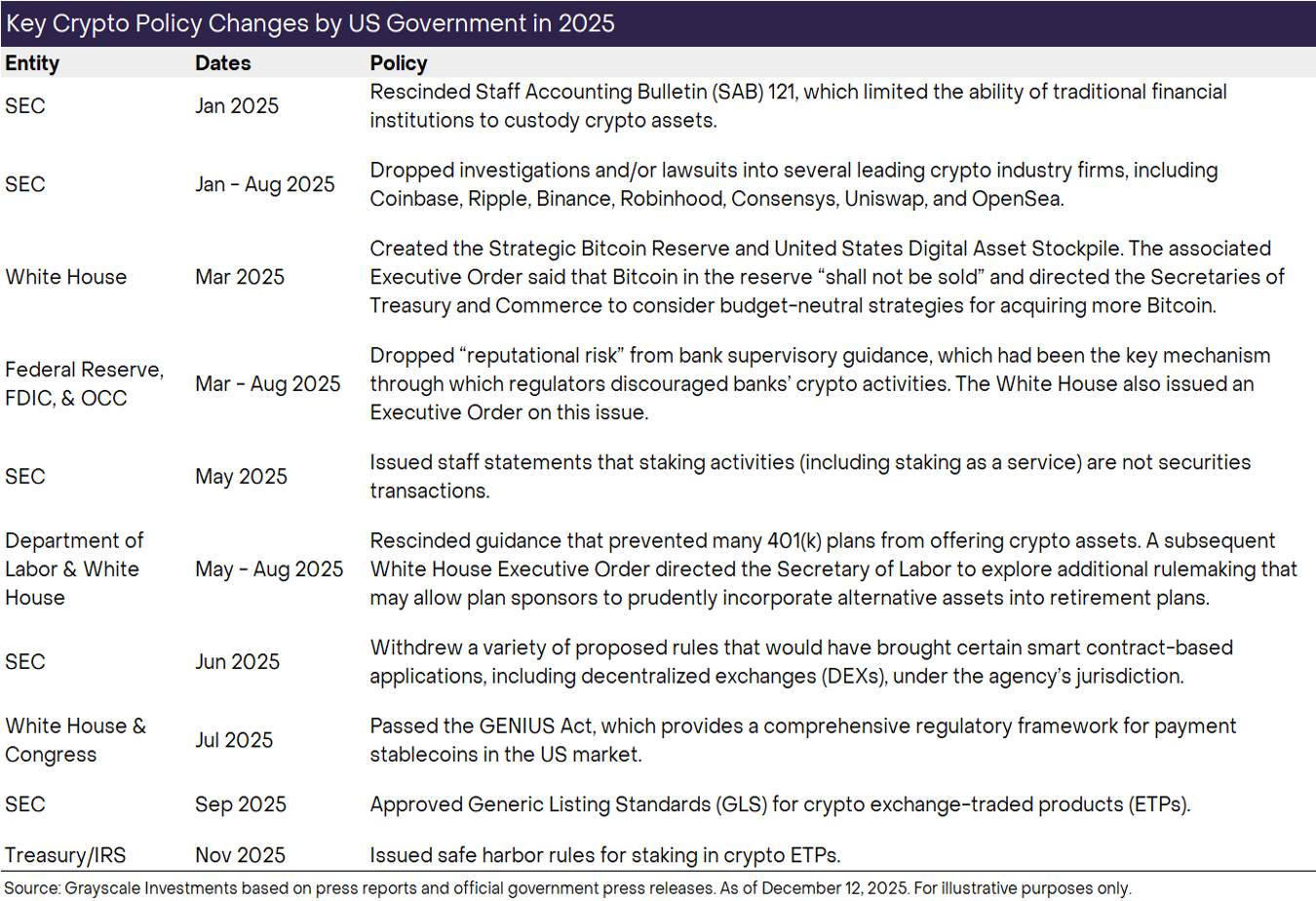

While this may be overlooked, until this year, the U.S. government was still investigating or suing many leading companies in the crypto industry (including Coinbase, Ripple, Binance, Robinhood, Consensys, Uniswap, and OpenSea). Even now, exchanges and other crypto intermediaries are still operating without clear guidance on the spot market.

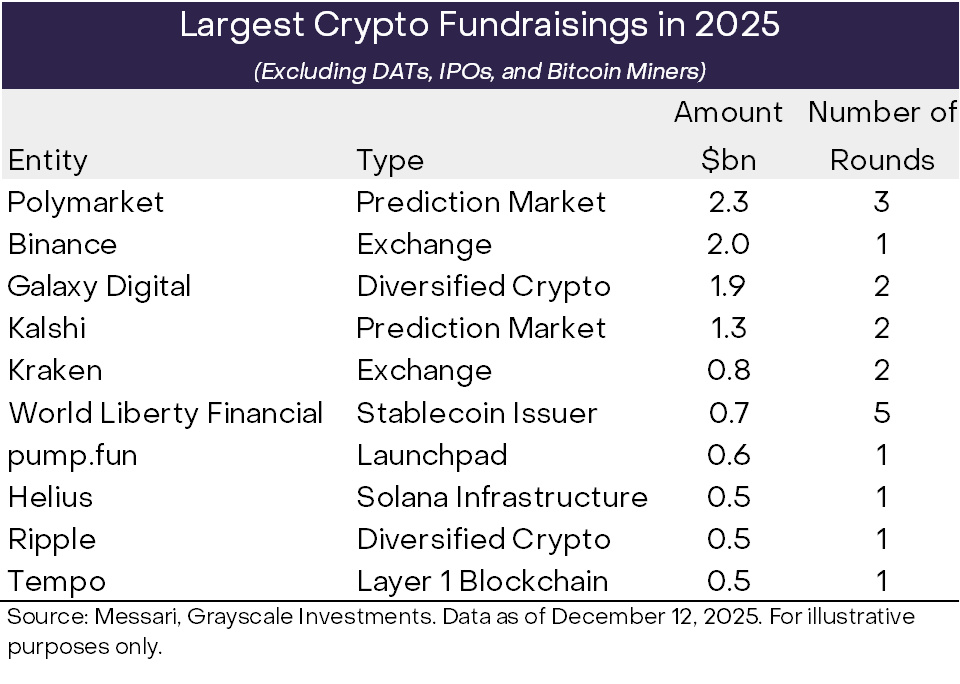

However, this situation is gradually improving. In 2023, Grayscale won its lawsuit against the U.S. Securities and Exchange Commission (SEC), paving the way for spot crypto exchange-traded products (ETPs). In 2024, spot ETPs for Bitcoin and Ethereum will officially launch. In 2025, the U.S. Congress passed the GENIUS Act, regulating the stablecoin market, and regulators adjusted their stance towards the crypto industry, collaborating with the industry to provide clear guidance while continuing to focus on consumer protection and financial stability. Grayscale expects that by 2026, the U.S. Congress will pass bipartisan-supported legislation on crypto market structure, further solidifying the position of blockchain-based financial systems in U.S. capital markets and promoting continued inflows of institutional investment (see Figure 4).

Figure 4: Higher fundraising amounts may indicate increased confidence among institutional investors

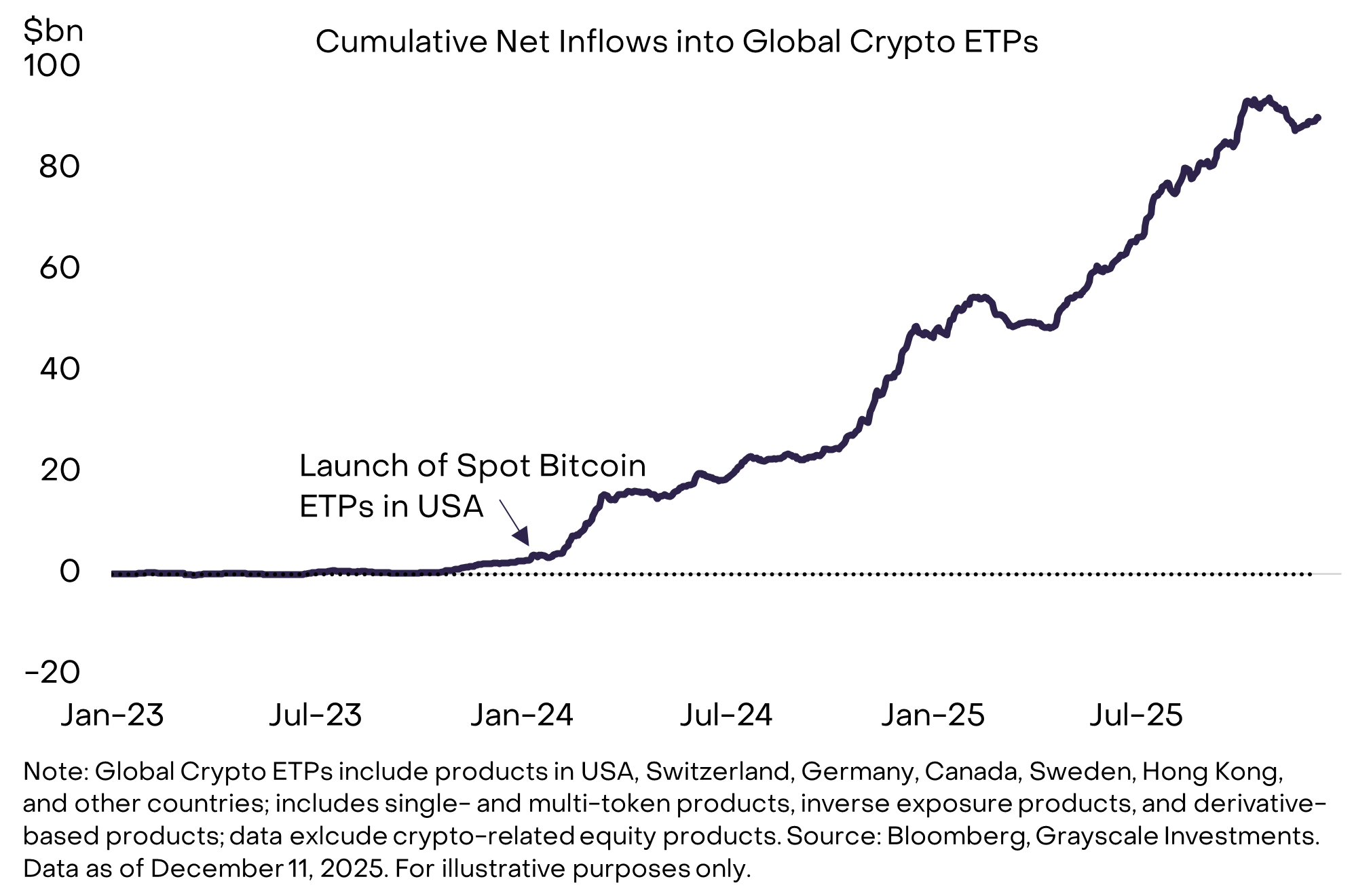

We believe that new capital entering the crypto ecosystem will primarily flow through spot ETPs. Since the launch of Bitcoin ETPs in the U.S. in January 2024, global crypto ETPs have seen a net inflow of $87 billion (see Figure 5). Although these products have achieved early success, the process of incorporating crypto assets into mainstream portfolios is still in its early stages. Grayscale estimates that the proportion of assets managed by U.S. wealth management advisors allocated to the crypto asset class is less than 0.5%.[2] As more platforms complete due diligence, establish capital market assumptions, and incorporate crypto assets into model portfolios, this proportion is expected to grow.

Beyond wealth management, early institutional investors have already included crypto ETPs in their portfolios, including Harvard Management Company and Abu Dhabi sovereign wealth fund Mubadala.[3] We expect that by 2026, this list will expand significantly.

As the crypto market increasingly becomes driven by institutional capital inflows, the characteristics of its price performance are also changing. In every previous bull market, Bitcoin's price increased by at least 1000% within a year (see Figure 6). This time, Bitcoin's maximum annual increase was about 240% (as of March 2024). We believe this difference reflects the more stable buying behavior of recent institutional investors, rather than the momentum effect of retail investors chasing prices in previous cycles. Although crypto investment still carries significant risks, we believe that at the time of writing, the likelihood of a deep and prolonged cyclical correction in prices is relatively low. Instead, we believe that a steady price increase driven by institutional capital inflows is more likely to become the mainstream trend in the coming year.

Figure 6: No dramatic surges in Bitcoin prices during this cycle

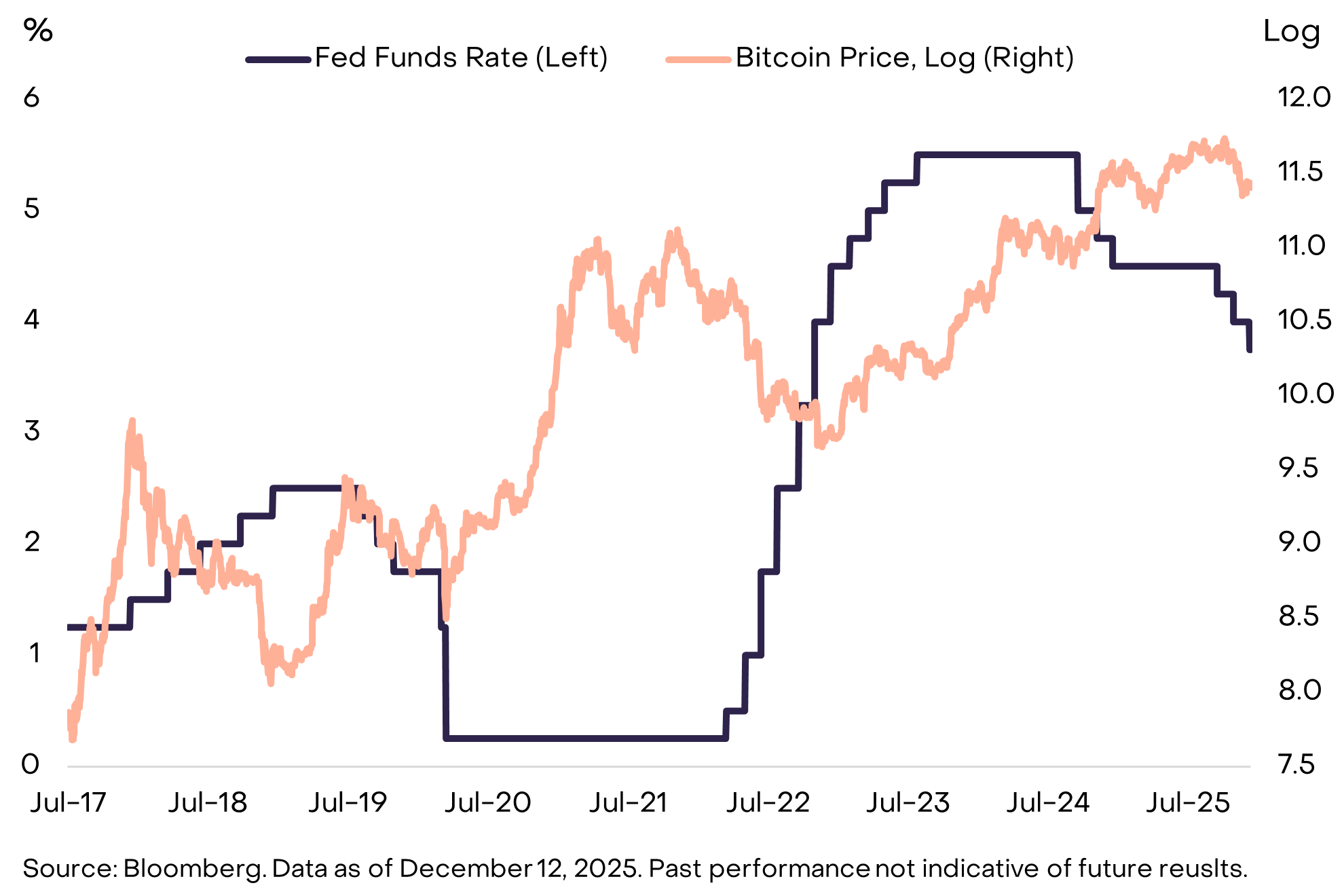

The supportive macro market backdrop may also limit some downside risks to token prices in 2026. The last two cyclical peaks occurred during periods of Federal Reserve interest rate hikes (see Figure 7). In contrast, the Federal Reserve is expected to cut rates three times in 2025 and continue to do so next year. Kevin Hassett, who may succeed Jerome Powell as the Federal Reserve Chair, recently stated on "Face the Nation": "The American people can expect President Trump to choose someone who can help them get lower interest rates on car loans and easier access to low-interest mortgages."[4] Overall, economic growth and the generally supportive policies of the Federal Reserve should align with improved investor risk appetite and the potential returns of high-risk assets, including crypto assets.

Figure 7: Previous cyclical peaks related to Federal Reserve interest rate hikes

Like all other asset classes, the driving force behind the crypto market comes from a combination of fundamentals and capital flows. The commodity market is cyclical, and the crypto market may experience longer cyclical corrections at certain points in the future. However, we do not believe this will occur in 2026. From a fundamental perspective, the crypto market shows strong support: we expect macro demand for alternative value storage tools to continue growing, while regulatory clarity will drive institutional investment into public blockchain technology. Additionally, new capital continues to flow into the market: by the end of next year, crypto ETPs (exchange-traded products) are expected to appear in more portfolios. In this cycle, there has not been a wave of massive retail demand; rather, there has been sustained demand for crypto ETPs from a broad range of portfolios. Against the backdrop of overall supportive macro conditions, we believe these factors will lay the foundation for new highs in the crypto asset class in 2026.

Top Ten Crypto Investment Themes for 2026

Cryptocurrency is a diverse asset class that reflects numerous application scenarios of public blockchain technology. The following section outlines Grayscale's views on the ten most important crypto investment themes for 2026—along with two "disruptive factors." For each theme, we list the most relevant tokens from Grayscale's perspective. For more background information on the types of investable digital assets, please refer to our Crypto Sectors Framework.

Theme 1: The Risk of Dollar Depreciation Drives Demand for Currency Alternatives

Relevant Crypto Assets: BTC, ETH, ZEC

The U.S. economy is facing a debt problem (see Figure 3), which may ultimately weaken the dollar's role as a value storage tool. Other countries face similar issues, but because the dollar is currently the dominant global currency, the credibility of U.S. policy has a more significant impact on potential capital flows. In our view, only a few digital assets can be considered viable value storage tools, possessing sufficient adoption, high decentralization, and limited supply growth capabilities. These include the two largest cryptocurrencies by market cap, Bitcoin and Ethereum. Similar to physical gold, their value partly derives from their scarcity and autonomy.

The supply of Bitcoin is capped at 21 million coins and is entirely controlled by programmatic rules. For example, we can be certain that the 20 millionth Bitcoin will be mined in March 2026. A digital currency system that is transparent, predictable, and ultimately scarce in supply, while conceptually simple, is increasingly attractive in today's economy due to the tail risks associated with fiat currency. As long as the macro imbalances leading to fiat currency risks continue to increase, the demand for alternative value storage tools in investment portfolios may also continue to grow (see Figure 8). Additionally, Zcash, as a smaller decentralized digital currency, may also be suitable for hedging against dollar depreciation risk due to its privacy features (see Theme 5).

Figure 8: Macro imbalances may drive demand for alternative value storage tools

Theme 2: Regulatory Clarity Supports the Adoption of Digital Assets

Relevant Crypto Assets: Almost All Crypto Assets

In 2025, the U.S. made significant progress in regulatory clarity for crypto, including the passage of the GENIUS Act (regarding stablecoins), the repeal of SEC Staff Accounting Bulletin No. 121 (on custody issues), the introduction of universal listing standards for crypto ETPs, and addressing traditional banking access issues for the crypto industry (see Figure 9). Next year, we expect another major advancement with the passage of bipartisan market structure legislation. The House passed a version of this legislation—the Clarity Act—in July, and the Senate has initiated related procedures. While many details still need to be resolved, overall, this legislation provides a set of traditional financial rules for the crypto capital market, including registration and disclosure requirements, crypto asset classification, and insider trading rules.

In practice, a more refined regulatory framework for crypto assets in the U.S. and other major economies may mean that regulated financial service companies can report digital assets on their balance sheets and begin trading on the blockchain. This may also allow for on-chain capital formation, enabling both startups and established companies to issue regulated tokens. By further unlocking the full potential of blockchain technology, regulatory clarity should help enhance the overall value of the crypto asset class. Given the potential importance of regulatory clarity in driving the crypto asset class in 2026, we believe that interruptions in the bipartisan legislative process in Congress should be viewed as a potential downside risk.

Figure 9: The U.S. made significant progress in crypto regulatory clarity in 2025

Theme 3: The GENIUS Act Drives Continued Growth in Stablecoin Influence

Relevant Crypto Assets: ETH, TRX, BNB, SOL, XPL, LINK

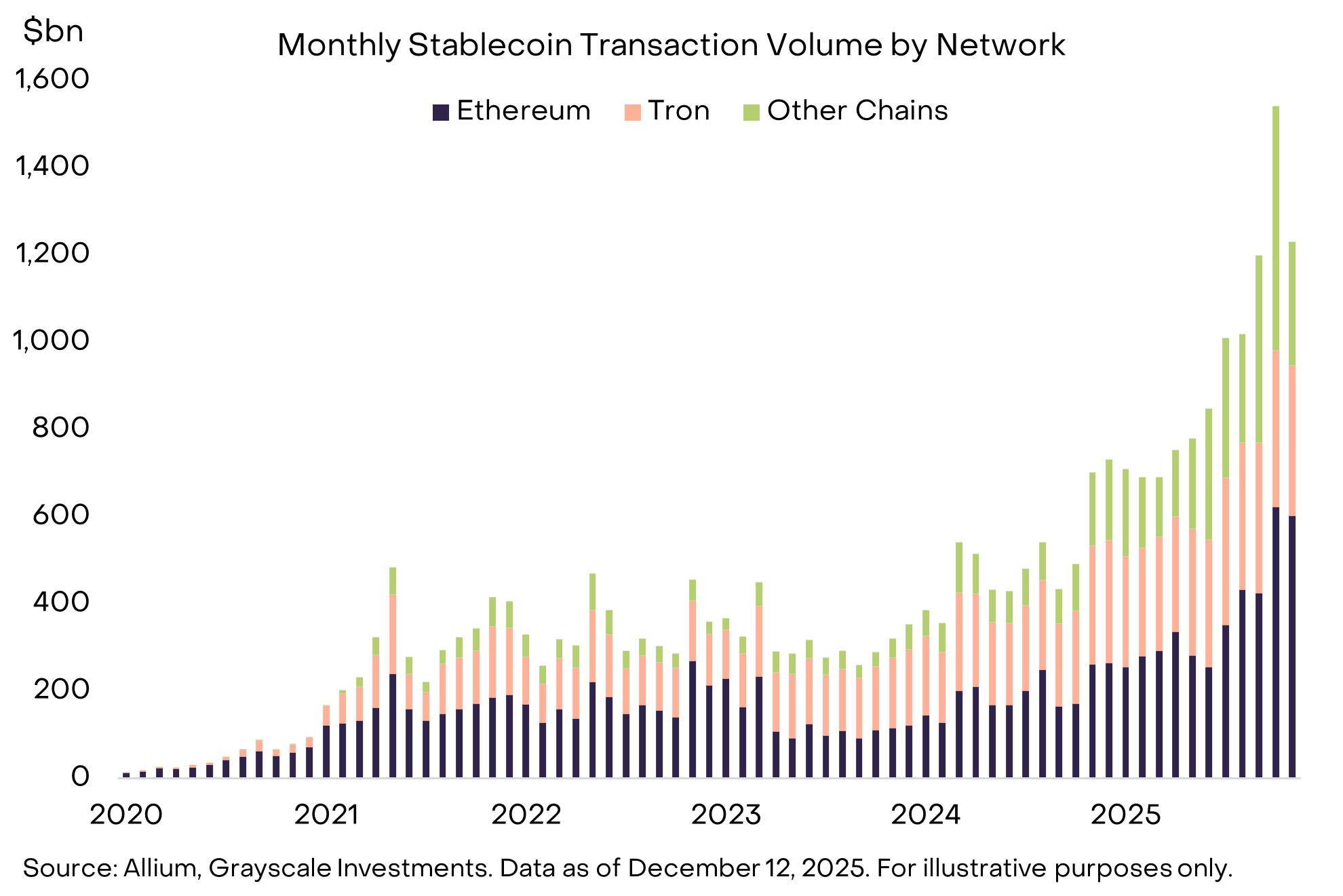

2025 was the "breakout year" for stablecoins: the total circulation reached $300 billion, with an average monthly trading volume of $1.1 trillion over the six months ending in November[5]. Additionally, the U.S. Congress passed the GENIUS Act, leading to a significant influx of institutional capital into the industry (see Figure 10). In 2026, we expect to see the tangible results of these changes: stablecoins will be integrated into cross-border payment services, used as collateral in derivatives exchanges, appear on corporate balance sheets, and serve as alternatives to credit cards in online consumer payments. The growing popularity of prediction markets may also drive new demand for stablecoins. The increase in stablecoin trading volume is expected to benefit the blockchains that record these transactions (such as ETH, TRX, BNB, and SOL), while also promoting the development of related infrastructure (such as LINK) and decentralized finance (DeFi) applications (see Theme 7).

Figure 10: Stablecoins experience explosive growth

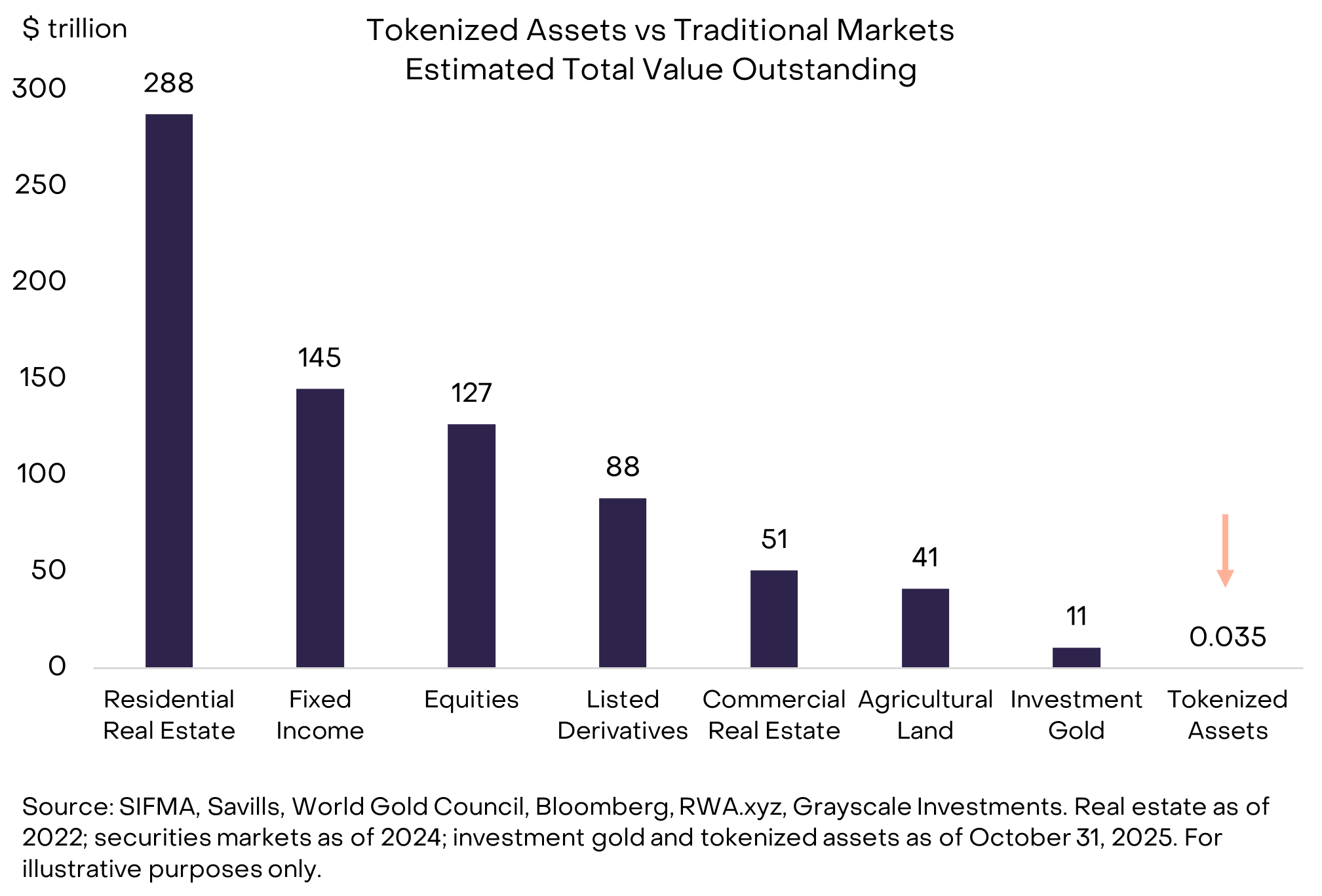

Theme 4: Asset Tokenization Reaches a Turning Point

Relevant Crypto Assets: LINK, ETH, SOL, AVAX, BNB, CC

Currently, the scale of asset tokenization remains small: it accounts for only 0.01% of the total market capitalization of global stocks and bonds (see Figure 11). Grayscale expects that, driven by more mature blockchain technology and clearer regulatory frameworks, asset tokenization will grow rapidly in the coming years. By 2030, the scale of tokenized assets could increase by about 1,000 times, which is not surprising. In our view, this growth will bring value to the blockchains that handle tokenized asset transactions (such as Ethereum, BNB Chain, and Solana) and various supporting applications. Among on-chain supporting applications, Chainlink (LINK) has unique potential due to its distinctive software technology suite.

Figure 11: Asset tokenization has enormous growth potential

Theme 5: The Mainstreaming of Blockchain Technology Calls for Privacy Solutions

Relevant Crypto Assets: ZEC, AZTEC, RAIL

Privacy is a normal component of financial systems: almost everyone wants their salary, taxes, net worth, and consumption habits to remain private. However, most blockchains are inherently transparent. If public blockchains want to integrate more deeply into the financial system, they need stronger privacy infrastructure—this has become increasingly evident as regulation drives the integration of blockchain technology. Privacy features are gaining attention from investors, with potential beneficiaries including Zcash (ZEC), a decentralized digital currency similar to Bitcoin but with privacy protection features; Zcash's price surged significantly in Q4 2025 (see Figure 12). Other major projects include Aztec (a privacy-focused Ethereum Layer 2 network) and Railgun (DeFi privacy middleware). Additionally, we may see an increase in the adoption of confidential transactions on leading smart contract platforms like Ethereum (via ERC-7984) and Solana (via Confidential Transfers token extension). Improving privacy tools will also require better identity and compliance infrastructure to support DeFi.

Figure 12: Crypto investors' attention to privacy features is increasing

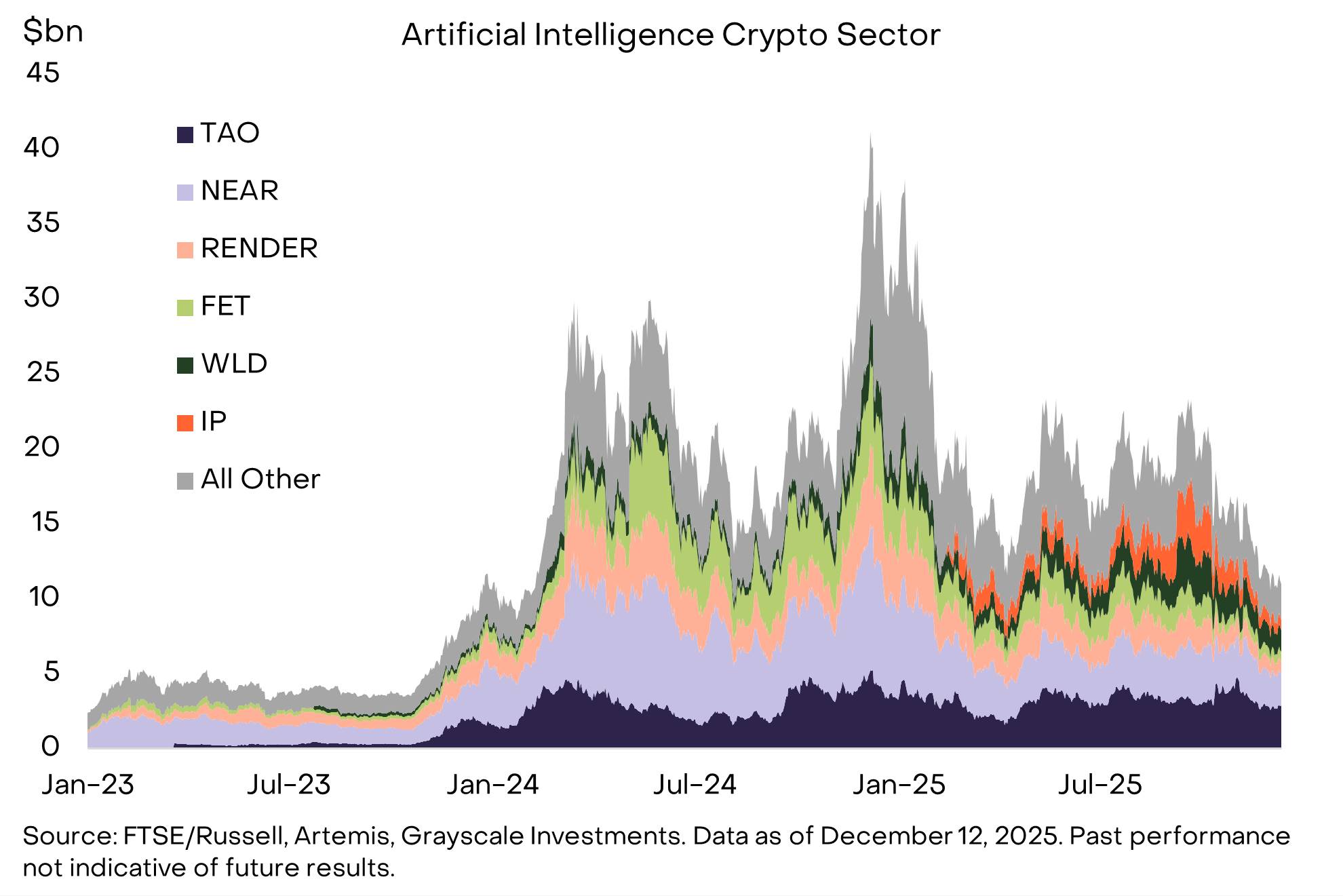

Theme 6: AI Centralization Calls for Blockchain Solutions

Relevant Crypto Assets: TAO, IP, NEAR, WORLD

The fundamental alignment between crypto technology and artificial intelligence (AI) is clearer and tighter than ever. AI systems are increasingly centralized among a few dominant companies, raising concerns about trust, fairness, and ownership, while crypto technology provides foundational tools to directly address these risks. Decentralized AI development platforms like Bittensor aim to reduce reliance on centralized AI technologies; verifiable "Proof of Personhood" systems like World can distinguish humans from synthetic agents in a world flooded with artificial activity; and networks like Story Protocol provide transparent and traceable intellectual property in an era where the sources of digital content are increasingly difficult to discern. Additionally, tools like X402—a zero-fee stablecoin payment layer suitable for Base and Solana—support low-cost, instant micropayments, meeting the needs of agent-to-agent or machine-to-human economic interactions.

These components together form the early infrastructure of the "Agent Economy," where identity, computation, data, and payments must be verifiable, programmable, and censorship-resistant. Although this field is still in its early and uneven development, the intersection of crypto technology and AI is generating one of the most compelling long-term use cases in the space. As AI becomes increasingly decentralized, autonomous, and economically viable, protocols dedicated to building real infrastructure are expected to benefit from this trend (see Figure 13).

Figure 13: Blockchain Solutions for AI Risks

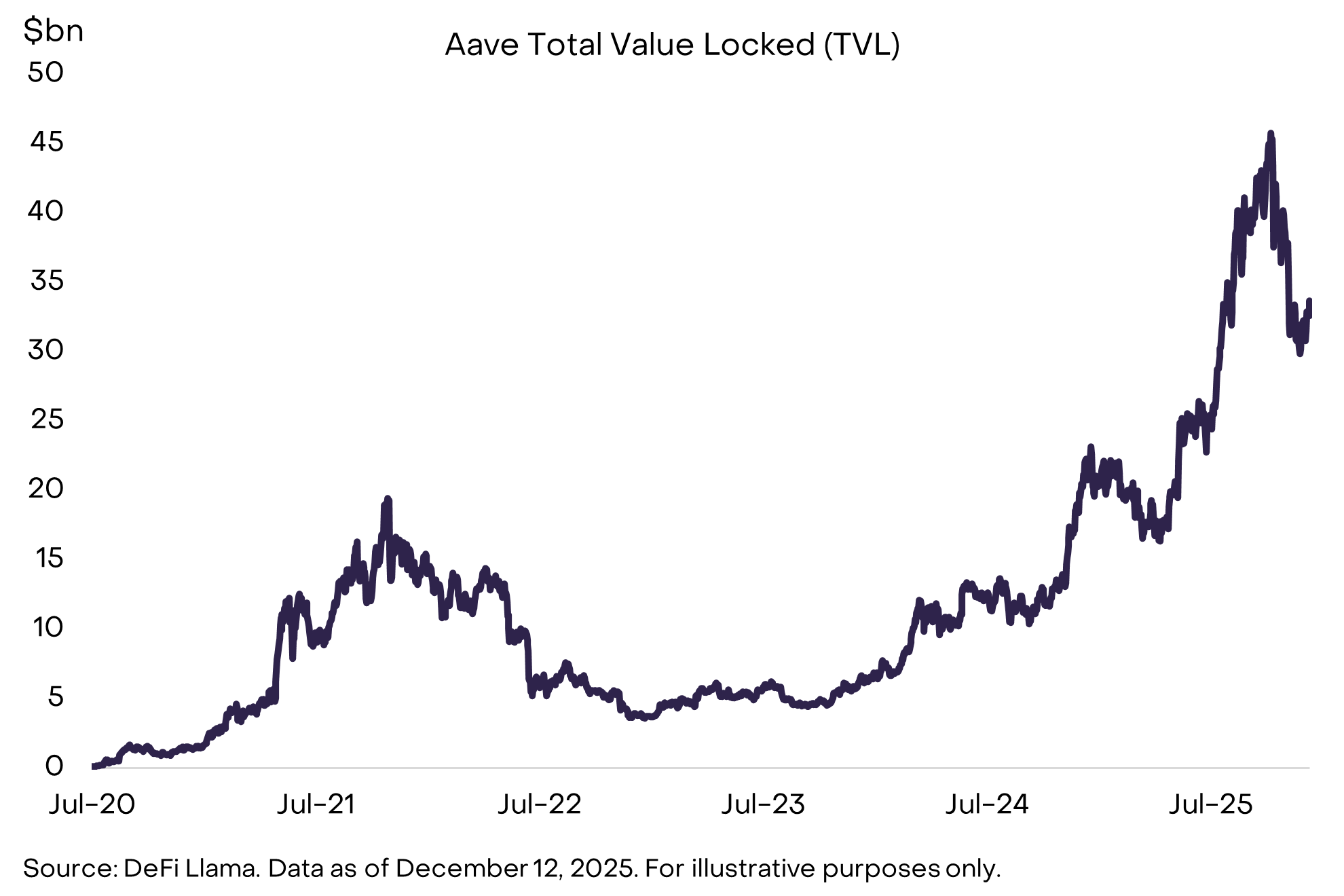

Theme 7: DeFi Accelerates Development, Lending Sector Leads the Trend

Relevant Crypto Assets: AAVE, MORPHO, MAPLE, KMNO, UNI, AERO, RAY, JUP, HYPE, LINK

Driven by technological advancements and favorable regulations, decentralized finance (DeFi) applications achieved significant development in 2025. The growth of stablecoins and tokenized assets are important success stories, but the DeFi lending sector also saw substantial growth, particularly led by lending platforms such as Aave, Morpho, and Maple Finance (see Figure 14). Meanwhile, decentralized perpetual futures exchanges (like Hyperliquid) have begun to rival some of the largest centralized derivatives exchanges in terms of open contracts and daily trading volume. Looking ahead, the increasing liquidity, interoperability, and connection to real-world prices of these platforms make DeFi a credible alternative for users wishing to conduct financial transactions directly on-chain. We expect more DeFi protocols to integrate with traditional fintech companies to leverage their infrastructure and existing user bases. We anticipate that core DeFi protocols will benefit from this, including lending platforms like AAVE, decentralized exchanges like UNI and HYPE, as well as related infrastructure like LINK, while blockchains supporting most DeFi activities (such as ETH, SOL, BASE) will also benefit.

Figure 14: The Scale and Diversity of DeFi Continues to Grow

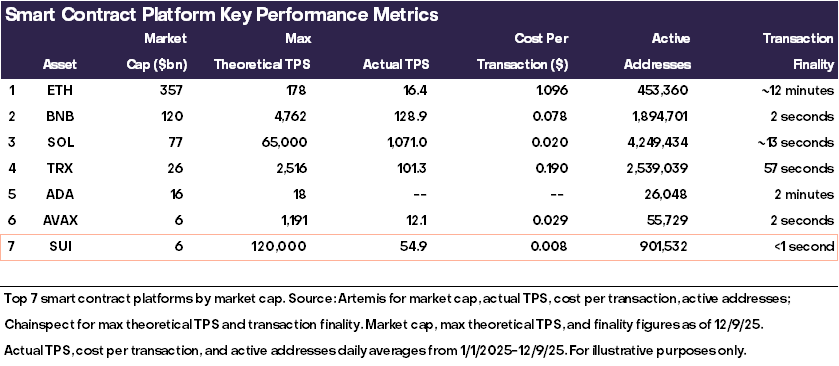

Theme 8: Mainstream Adoption Calls for Next-Generation Infrastructure

Relevant Crypto Assets: SUI, MON, NEAR, MEGA

Next-generation blockchains are continuously pushing the frontier of technology. However, some investors believe that more block space is not needed, as the demand for existing blockchains has not yet saturated. Solana was a typical example of this criticism: a fast but underutilized blockchain that was seen as a representative of "excess block space," but after a wave of adoption, it became one of the most successful cases in the industry. While not all high-performance blockchains today will follow a similar path, we expect a few to stand out. Superior technology does not guarantee widespread adoption, but the architecture of these next-generation networks gives them a unique advantage in emerging fields such as AI micropayments, real-time gaming loops, high-frequency on-chain trading, and intent-based systems. In this area, we expect Sui to stand out due to its technological advantages and integrated development strategy (see Figure 15). Other promising projects include Monad (parallelized EVM), MegaETH (ultra-fast Ethereum Layer 2 network), and Near (a blockchain focused on AI, which has achieved success with its Intents product).

Figure 15: Next-Generation Blockchains like Sui Offer Faster and Lower-Cost Transactions

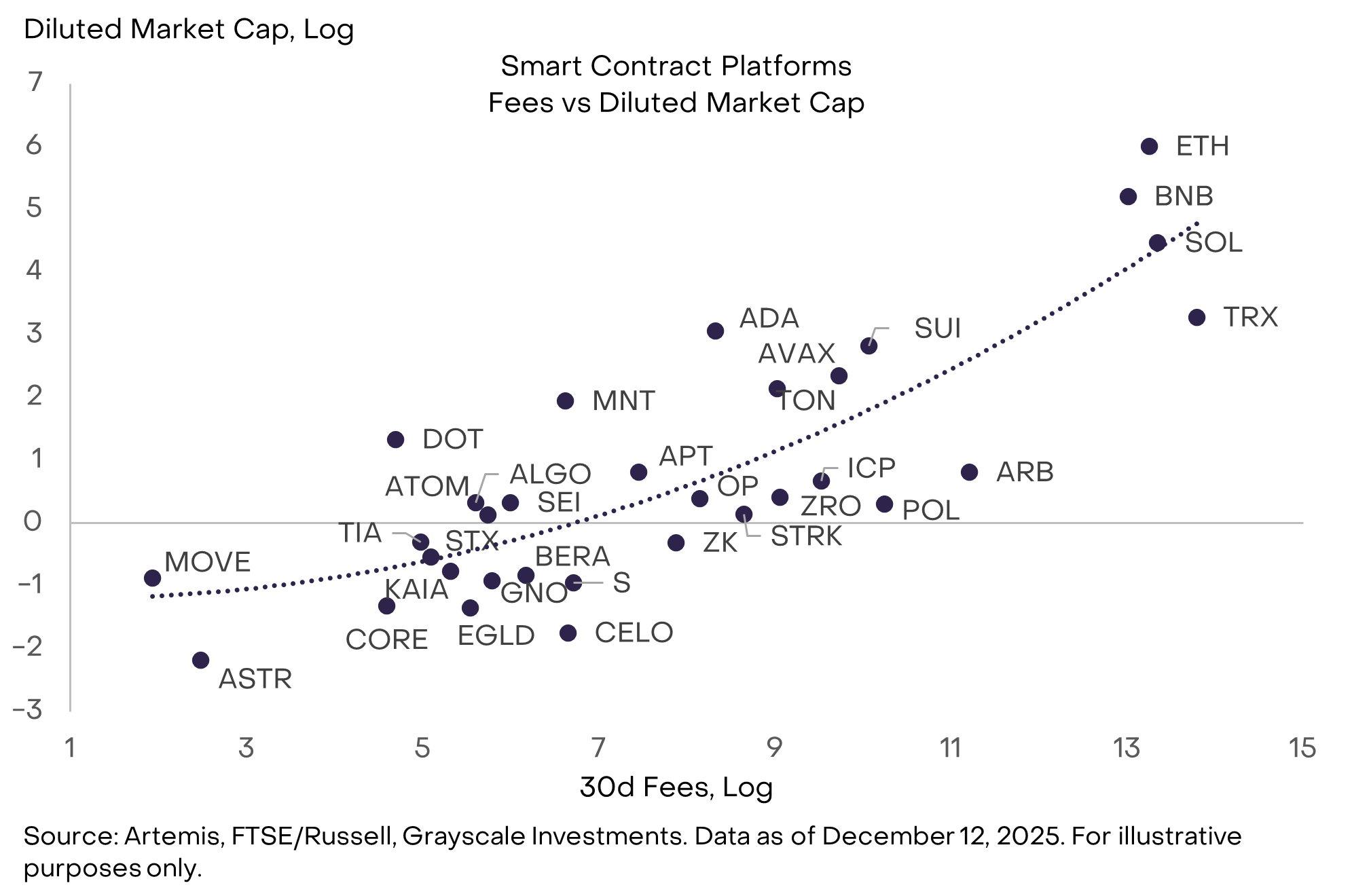

Theme 9: Focus on Sustainable Revenue

Relevant Crypto Assets: SOL, ETH, BNB, HYPE, PUMP, TRX

Blockchains are not traditional enterprises, but they do have measurable fundamentals, including user numbers, transaction volumes, fees, capital/total locked value (TVL), developers, and applications. Among all metrics, Grayscale believes that transaction fees are the most valuable fundamental indicator because they are the hardest to manipulate and have the highest comparability across blockchains (and are also the best empirical fit indicator). Transaction fees can be likened to "revenue" in traditional corporate finance. For blockchain applications, it is also important to distinguish between protocol fees/revenue and "supply-side" fees/revenue. As institutional investors begin to allocate capital to the crypto space, we expect them to focus on blockchains and applications with high revenue and/or revenue growth (excluding Bitcoin). Smart contract platforms with relatively high revenue include TRX, SOL, ETH, and BNB (see Figure 16). Application layer assets with relatively high revenue include HYPE and PUMP.

Figure 16: Institutional Investors May Pay More Attention to Blockchain Fundamentals

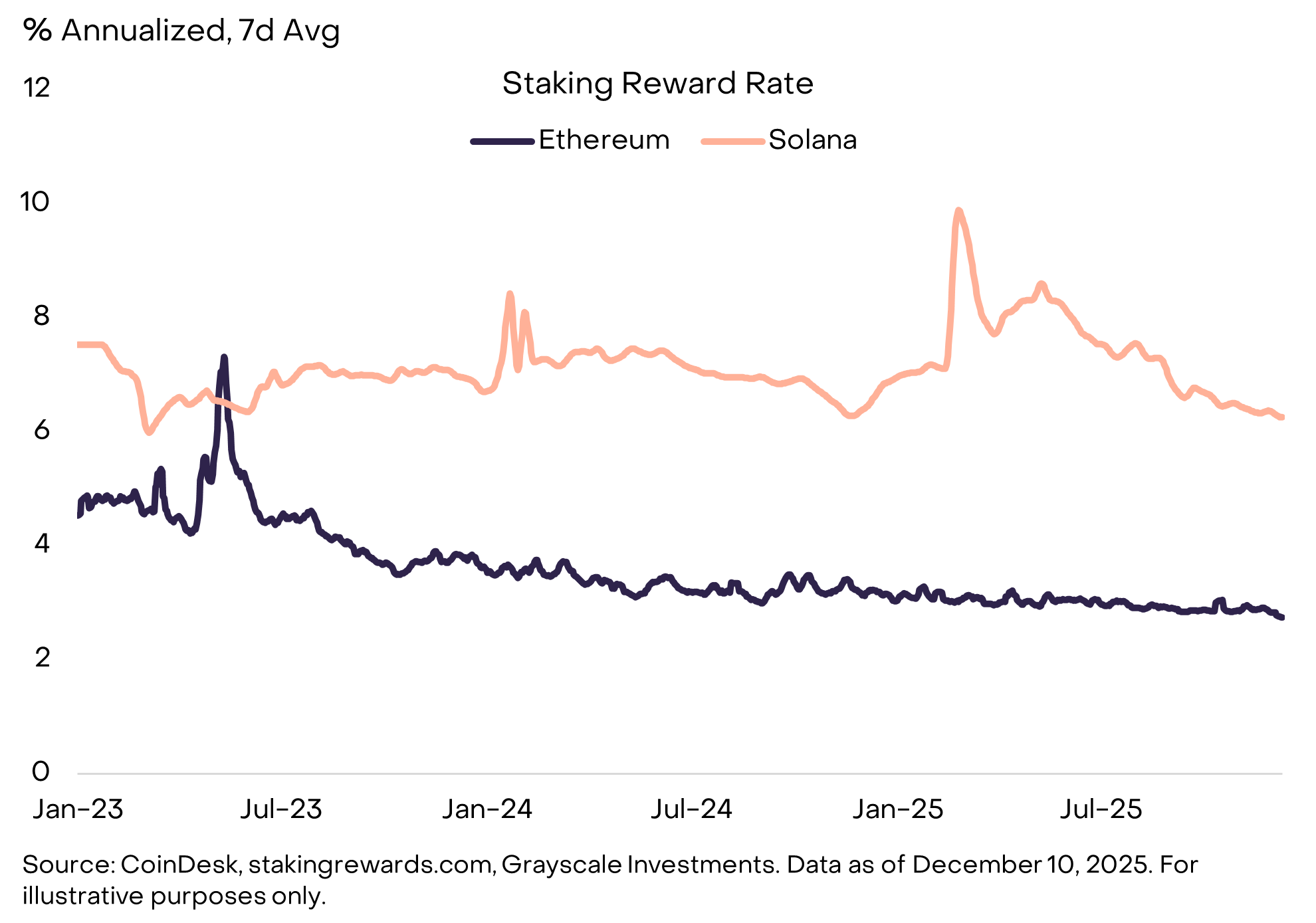

Theme 10: Investors Prefer Default Staking Options

Relevant Crypto Assets: LDO, JTO

In 2025, U.S. policymakers made two adjustments in the staking space that will enable more token holders to participate: (i) the U.S. Securities and Exchange Commission (SEC) clarified that liquid staking activities do not constitute securities transactions; (ii) the U.S. Internal Revenue Service (IRS) and Treasury announced that investment trusts/exchange-traded products (ETPs) can stake digital assets. Guidance on liquid staking services may benefit leading liquid staking protocols Lido and Jito on Ethereum and Solana in terms of TVL (total locked value). More broadly, the fact that crypto ETPs can be staked may make this model the default structure for holding proof-of-stake (PoS) token investment positions, leading to higher staking ratios and putting pressure on reward rates. In an environment where staking is more widely adopted, custodial staking through ETPs will provide a convenient structure for capturing rewards, while on-chain non-custodial liquid staking will have composability advantages in DeFi. We expect this dual structure to persist for some time.

Figure 17: Proof of Stake Tokens Provide Native Rewards

The "Pseudo Hot Topics" of 2026

We expect each of the investment themes mentioned above to have a significant impact on the development of the crypto market in 2026. However, there are two hot topics that we believe will not have a substantial impact on the crypto market next year: the potential threat of quantum computing to cryptographic algorithms and the evolution of Digital Asset Treasuries (DATs). While these two topics may generate a lot of discussion, we do not consider them core drivers of market prospects.

If quantum computing technology continues to make technical progress, most blockchains will eventually need to update their cryptographic algorithms. Theoretically, sufficiently powerful quantum computers could derive private keys from public keys, thereby generating valid digital signatures to spend users' cryptocurrencies. Therefore, Bitcoin and most other blockchains—as well as nearly all economic sectors using cryptographic technology—will ultimately need to upgrade to quantum-resistant cryptographic tools. However, experts estimate that before 2030, the capabilities of quantum computers will not be sufficient to crack Bitcoin's cryptographic algorithms. While research on quantum risks and community preparations may accelerate in 2026, we believe this topic is unlikely to have a noticeable impact on prices.

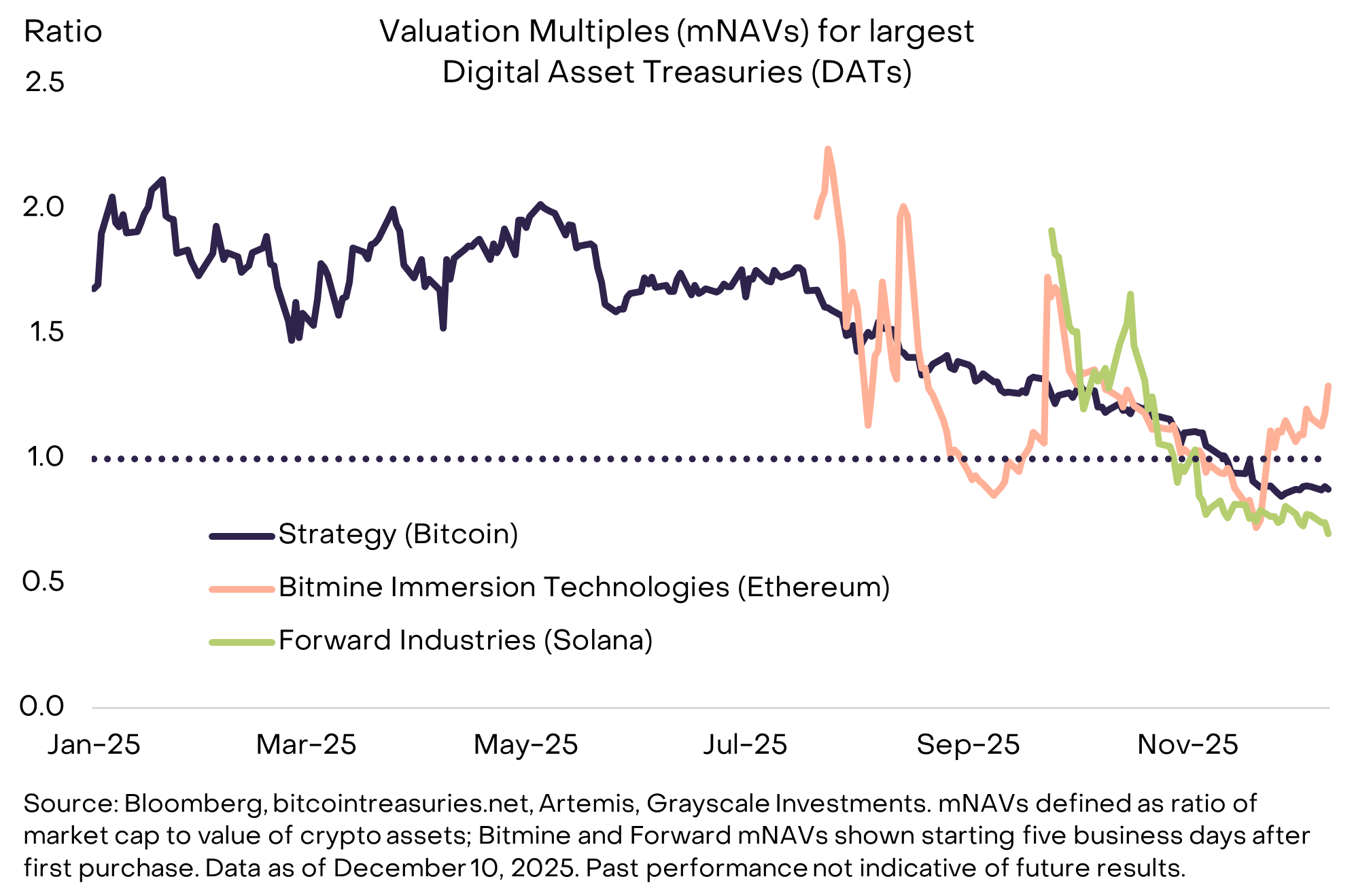

The same goes for Digital Asset Treasuries (DATs). The strategy of holding digital assets on corporate balance sheets, pioneered by Michael Saylor, sparked dozens of imitators in 2025. According to our estimates, the BTC supply held by DATs accounts for 3.7%, ETH for 4.6%, and SOL for 2.5%. However, since demand peaked in mid-2025, the demand for these tools has declined: the market value net asset multiple (mNAV) of the largest DATs is close to 1.0 (see Figure 18). Nevertheless, most DATs are not overly leveraged (or even completely unleveraged), so even in a market downturn, they may not be forced to sell assets. The largest DAT, Strategy, recently raised a dollar reserve fund to continue paying dividends on preferred stock even if Bitcoin prices fall. We expect that the vast majority of DATs will behave like closed-end funds, trading at premiums or discounts to net asset value, with little asset liquidation. Although these tools may become a long-term feature in the crypto investment space, we believe they are unlikely to become a major source of new token demand in 2026, nor are they likely to be a significant source of selling pressure.

Figure 18: DAT Premiums Have Narrowed, but Asset Sales Are Unlikely

Conclusion

We expect a bright outlook for digital assets in 2026, primarily driven by two major forces: macro demand for alternative value storage tools and an increasingly clear regulatory environment. Next year, the connection between blockchain finance and traditional finance will deepen further, while the inflow of institutional capital will also become an important trend. Tokens that can attract institutional adoption are expected to be those with clear use cases, sustainable revenue sources, and the ability to enter regulated trading venues and applications. Investors can look forward to a richer selection of crypto assets through exchange-traded products (ETPs) and, where possible, enable staking features.

At the same time, regulatory clarity and institutional adoption may raise the bar for crypto assets to enter the mainstream market. For example, certain crypto projects may need to meet new registration and disclosure requirements to enter regulated exchanges. Additionally, institutional investors may overlook crypto assets without clear use cases, even if these assets have relatively high market capitalizations. The GENIUS Act has clearly distinguished between regulated payment stablecoins (which enjoy specific rights and responsibilities under U.S. law) and other stablecoins that do not enjoy the same rights. Similarly, we expect that as crypto assets enter an institutional era, the gap between assets with access to regulated trading venues and institutional capital and those without the same access will become more pronounced. Crypto assets are entering a new era, and not all tokens will successfully transition to this new phase.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。