Author: Tyler

In today's crypto world, obtaining a consumer-oriented U card is no longer a difficult task. However, having a compliant foreign currency account at the level of a bank account, with personal real-name verification, is still quite rare.

Whether you are a crypto user or an ordinary player who has not yet engaged with Web3, you likely hope to easily deposit funds into overseas brokers like Interactive Brokers (IBKR) to invest in US and European stocks, pay for foreign services with foreign currency, or transfer tuition fees to overseas friends and family.

In simple terms, the vast majority of users need more than just a prepaid foreign currency card that can directly consume cryptocurrency; they need a complete and compliant financial account system. Earlier this year, I had an in-depth experience with the banking channel service launched by SafePal in collaboration with Swiss Fiat24 Bank.

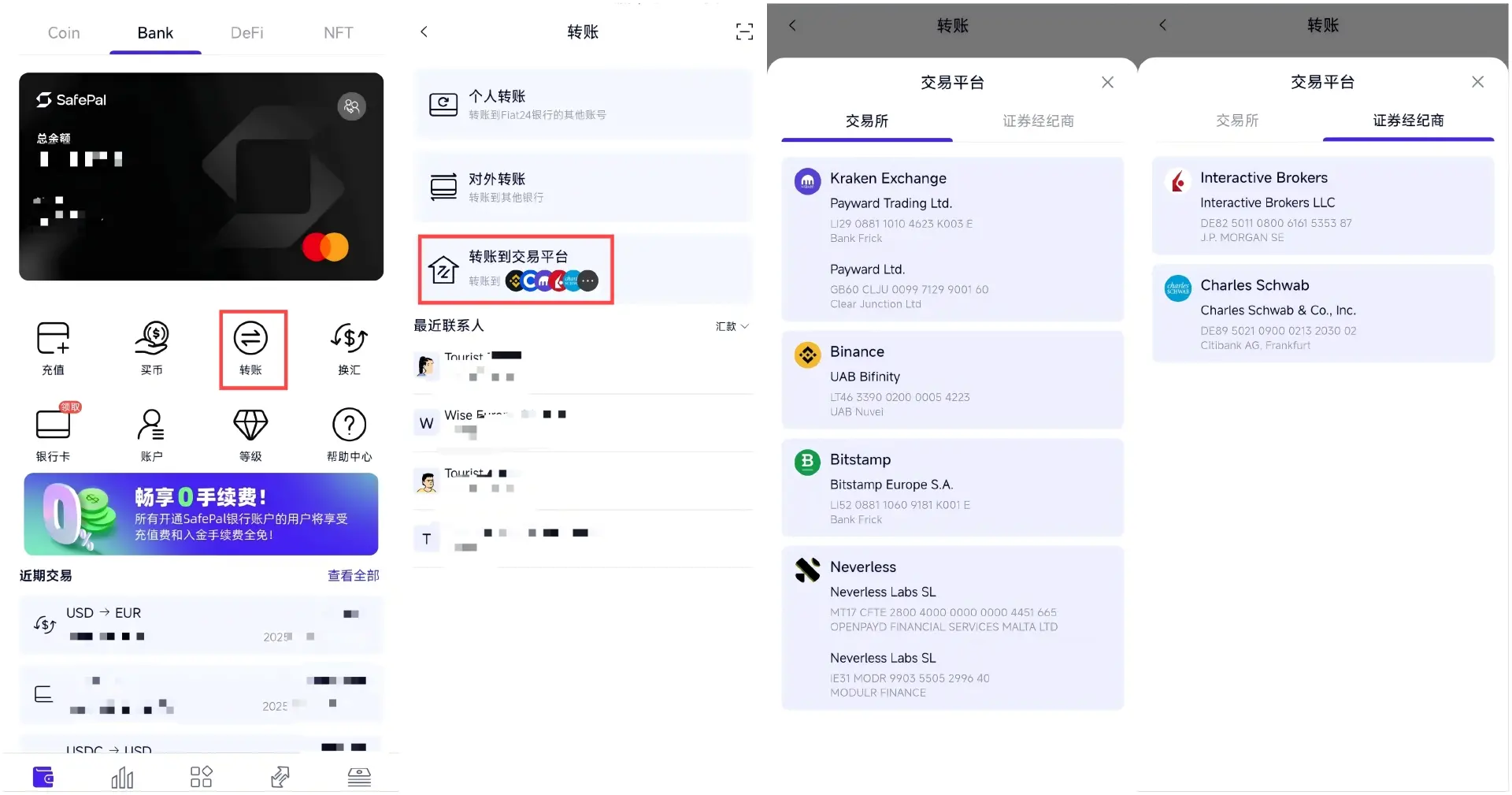

This service not only provides a convenient Mastercard for small consumption and withdrawals but, more importantly, it is also a compliant Swiss bank account that supports Euro and Swiss Franc transfers, which can be used for deposits and withdrawals with overseas brokers (such as IBKR, Charles Schwab, Tiger Brokers, etc.) and crypto exchanges (such as Kraken, Bitstamp, Binance, etc.) (see further reading: “Understanding SafePal Bank Account and Mastercard: A Complete Guide from Account Opening to Depositing with Overseas Brokers”, “Using U for Consumption, A Step-by-Step Guide to Registering and Using SafePal Mastercard”).

After nearly three months of in-depth testing, I found that the SafePal & Fiat24 banking channel service essentially provides users in mainland China and other regions that previously lacked similar services with a low-threshold convenient channel for Euro SEPA transfers: based on the IBAN Euro transfer channel, it allows crypto wallets to have nearly full-functionality of a commercial bank account.

After nearly three months of in-depth testing, I found that the SafePal & Fiat24 banking channel service essentially provides users in mainland China and other regions that previously lacked similar services with a low-threshold convenient channel for Euro SEPA transfers: based on the IBAN Euro transfer channel, it allows crypto wallets to have nearly full-functionality of a commercial bank account.

In simple terms, compared to traditional "U cards," the SafePal banking channel service not only includes crypto consumption functions but is also a complete financial account that can freely send and receive Euros, associate with crypto assets, and has a compliant identity label—users can open a compliant Swiss offshore bank account remotely from the comfort of their homes, enjoying sound banking account deposit and withdrawal, transfer, and remittance functions, making it particularly suitable for users with cross-border transfer and deposit/withdrawal needs.

Therefore, this article will delve into the derivative use cases that can be achieved through this Euro SEPA transfer channel, thoroughly testing various aspects such as overseas brokers, traditional banks/remittance service providers, crypto exchanges, Apple Pay/Google Pay, etc., to help everyone better acquire and master a bank account that is both compliant and multifunctional.

1. Bidirectional Connectivity Between Crypto and Euro

As mentioned above, the banking channel service jointly launched by SafePal and Fiat24 essentially provides users with a compliant channel for low-threshold bidirectional conversion between crypto assets and Euros.

Before performing Euro transfers or deposit/withdrawal operations, it is first necessary to ensure that there is sufficient Euro balance in the bank account. Currently, there are mainly two ways:

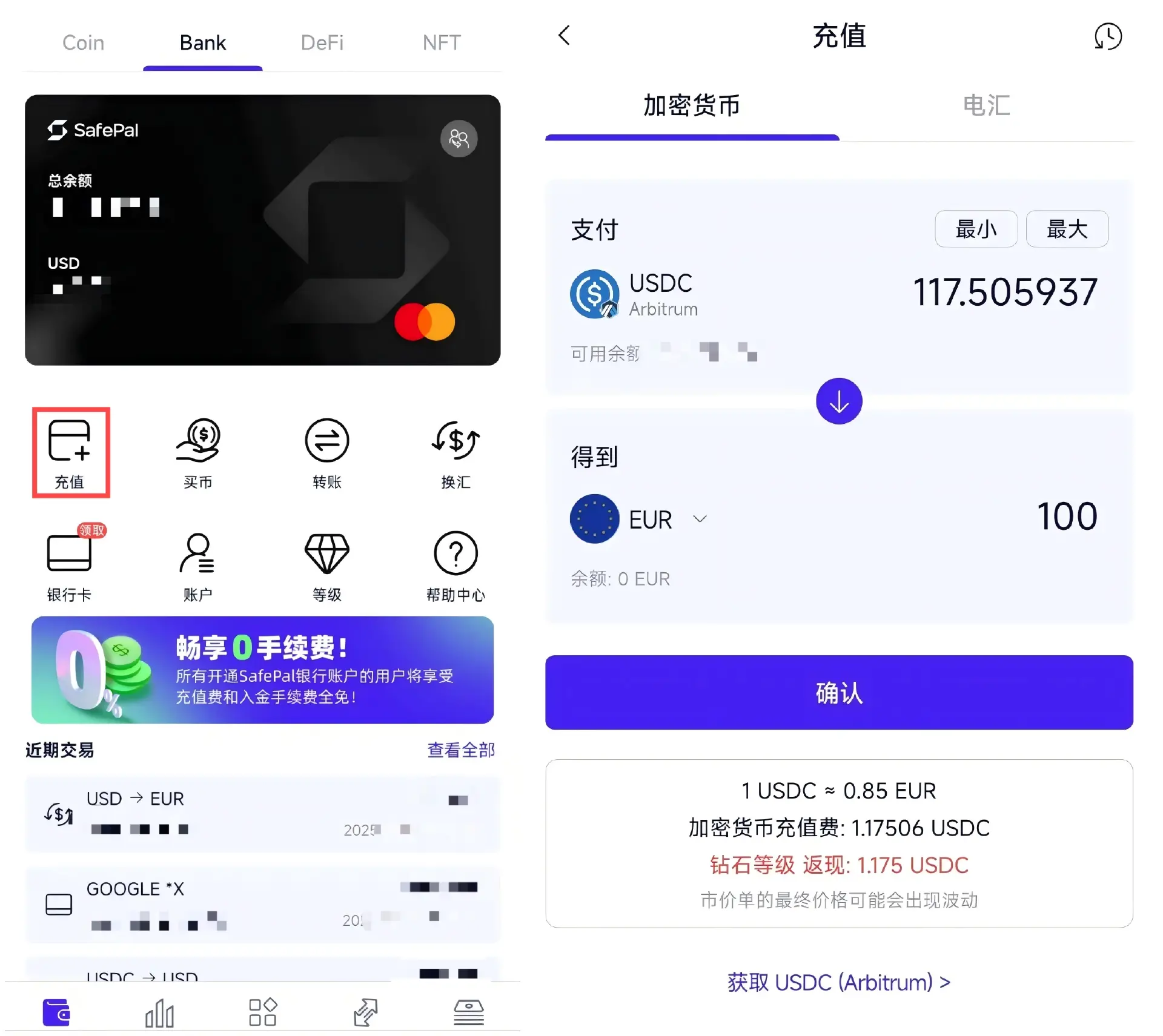

1. Recharge and Exchange USDC (Arbitrum) for Euros via SafePal Wallet App

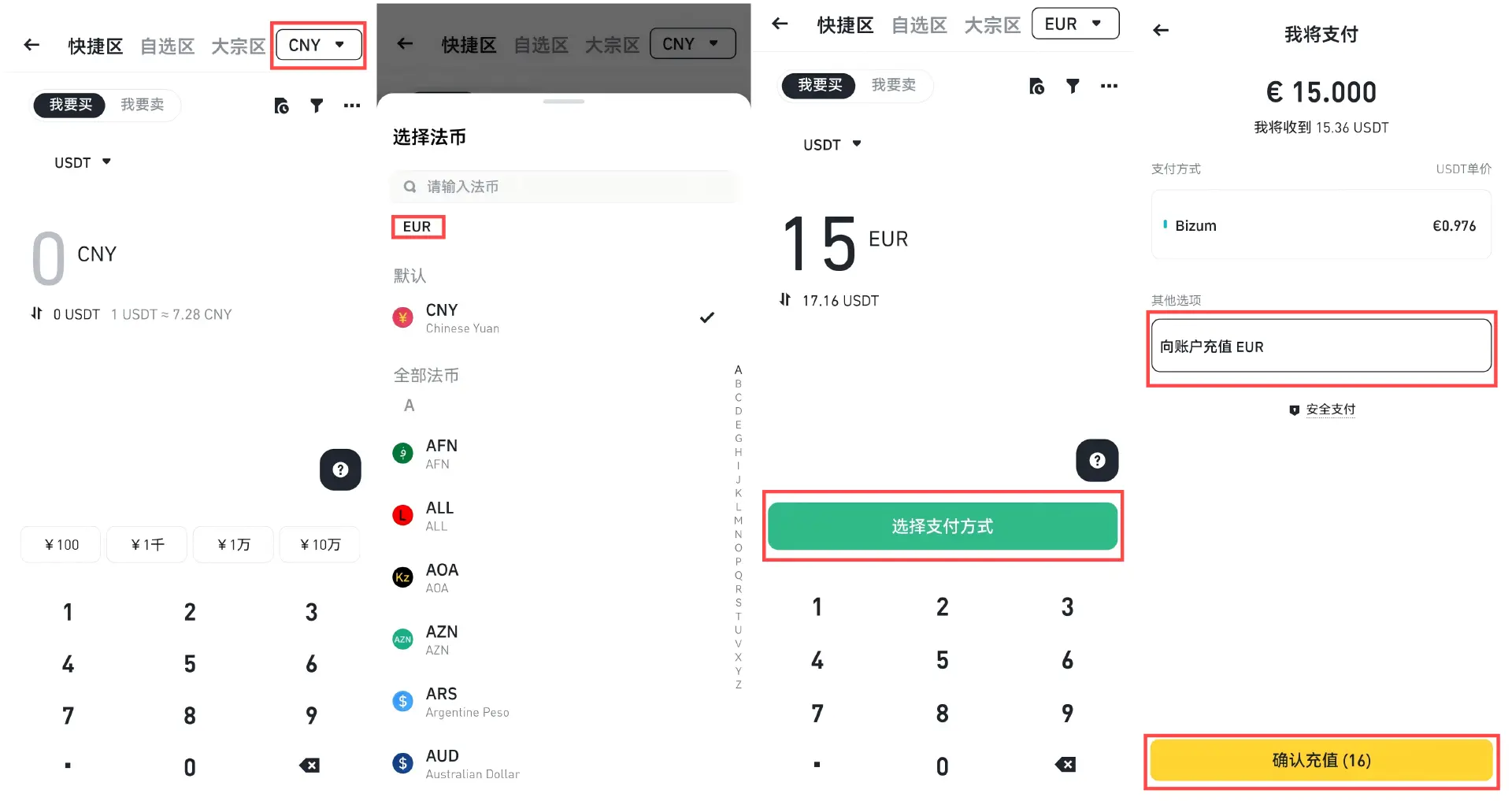

Users can select the "Recharge" service on the "Bank" page of the SafePal Wallet App to recharge USDC (Arbitrum) on-chain into EUR. The system will automatically convert USDC into Euros based on the real-time exchange rate.

As shown in the figure, when using 117.5 USDC to exchange for 100 Euros, the system displays an exchange rate of approximately 1 USDC ≈ 0.85 EUR, and a recharge fee of 1.175 USDC (1%) will be displayed.

It is important to note that SafePal currently implements a 100% refund policy for all USDC to fiat currency recharge fees, meaning that the fees paid by users will be fully refunded in USDC form, which can be viewed and withdrawn in "Level" - "Total Rewards."

2. Transfer Euros into Personal SafePal Swiss Bank Account via SEPA

In addition to recharging through crypto assets, users can also transfer Euro funds from other banks or financial institutions into the Swiss bank account provided by SafePal via SEPA (Single Euro Payments Area). This method is suitable for users who have Euro funds in other banks or financial institutions.

The specific operation steps are as follows:

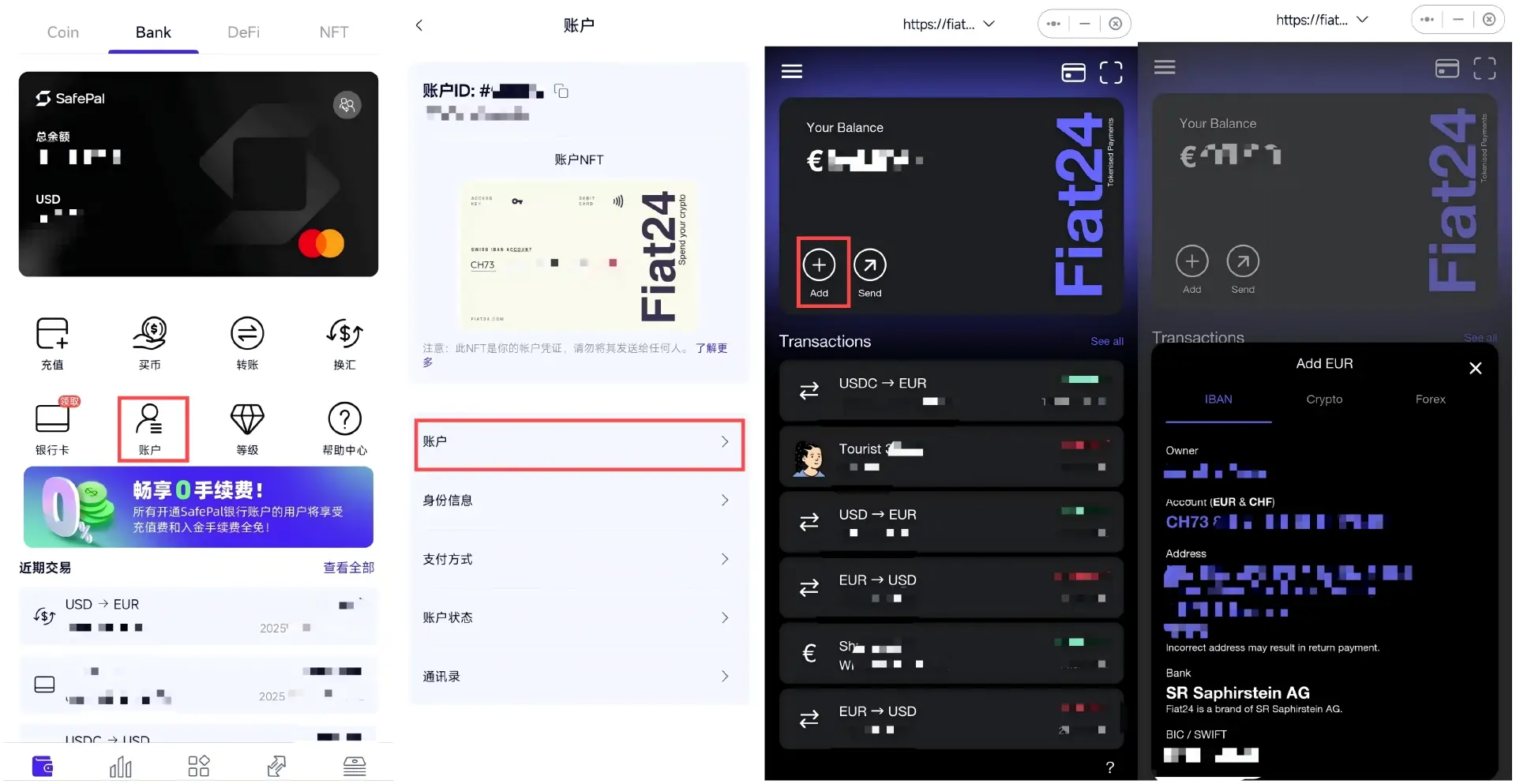

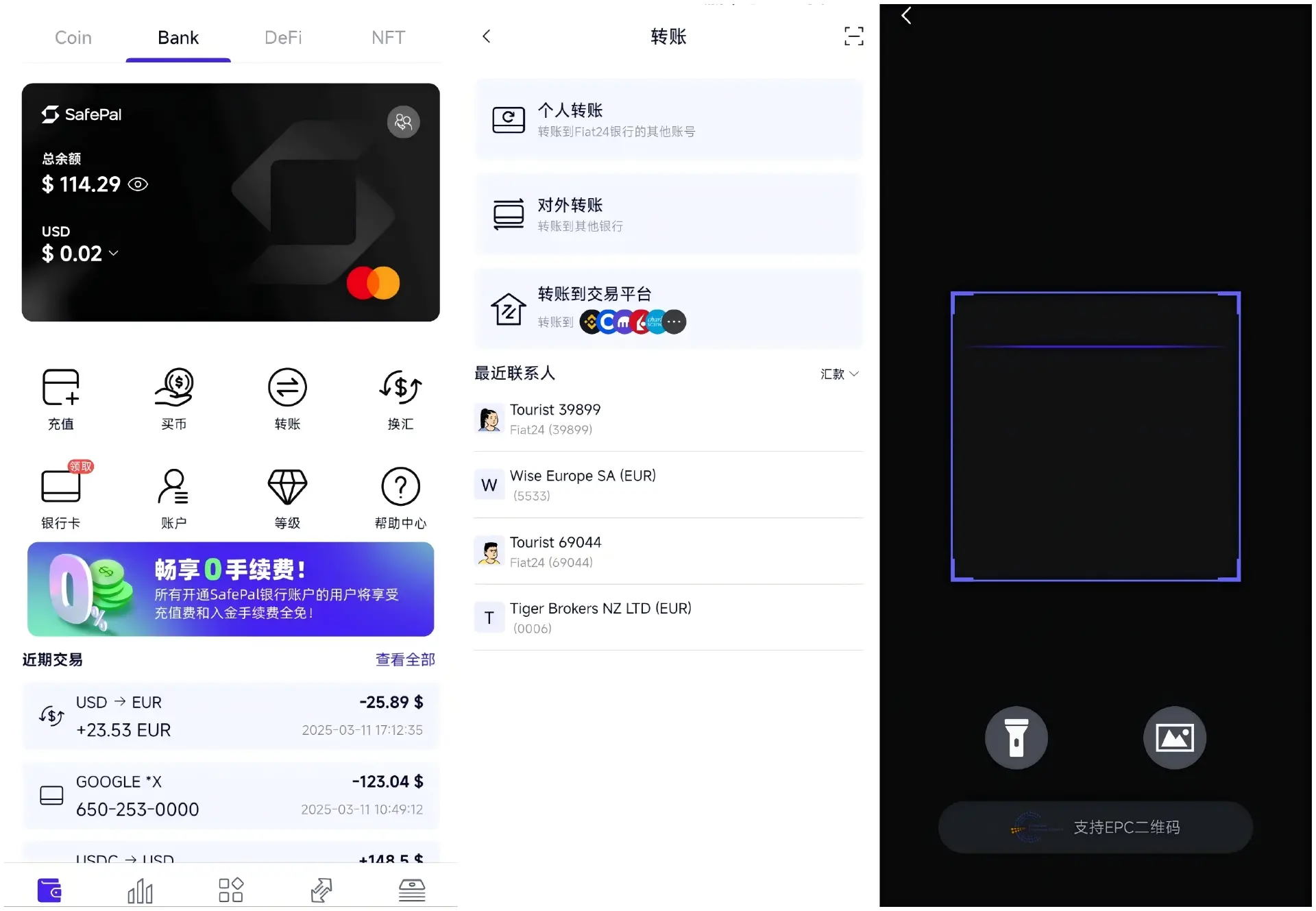

In the SafePal Wallet App's "Bank" page, click "Account" to enter the account details page, then click the "Add" button to obtain your personal IBAN (International Bank Account Number) and BIC/SWIFT (Bank Identifier Code);

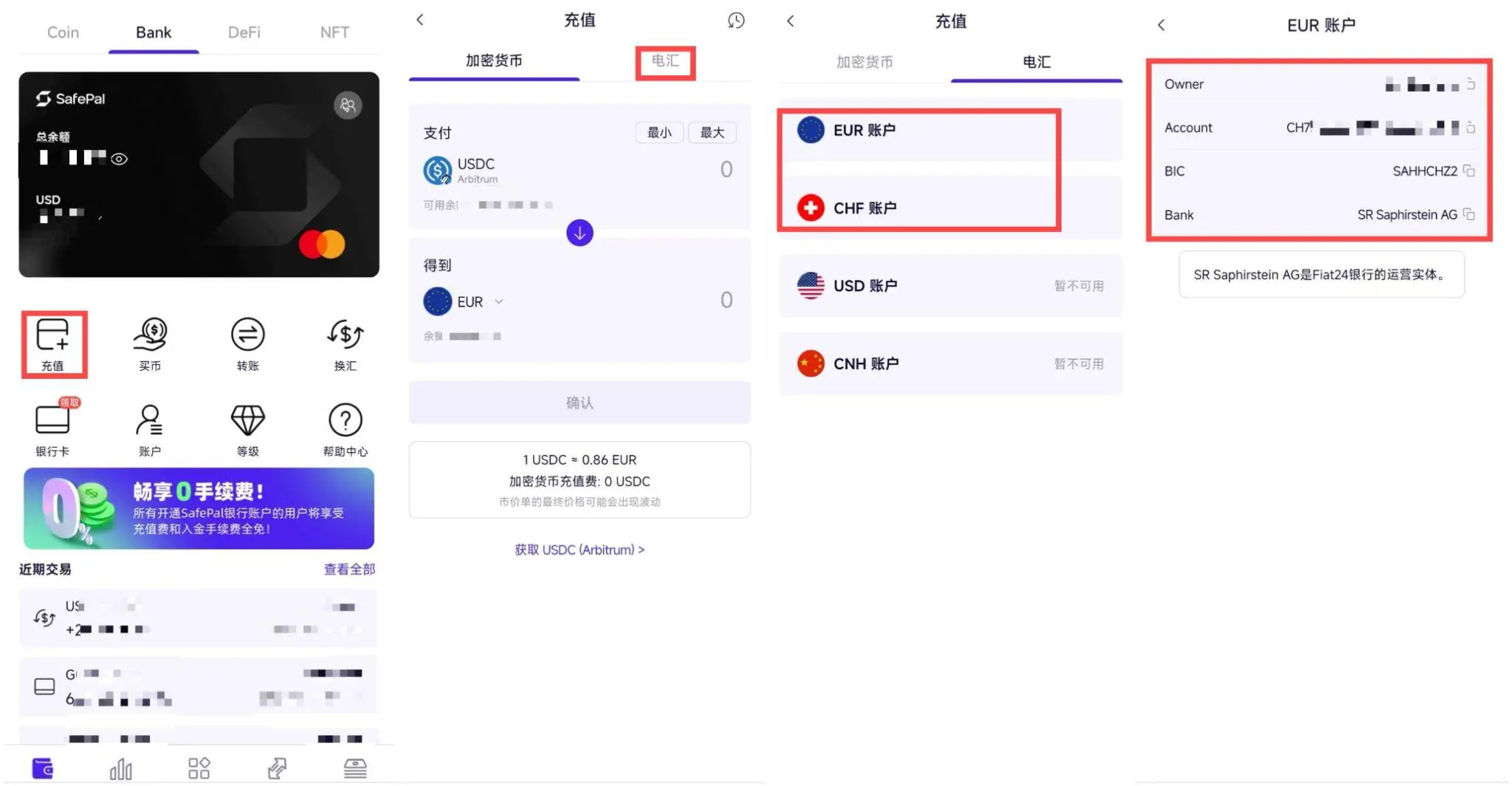

Alternatively, in the SafePal Wallet App's "Bank" page, you can directly click "Recharge," and on the right side, you can enter the account details page to obtain your personal IBAN and BIC/SWIFT.

Then, initiate a SEPA transfer from your other bank account holding Euro funds, entering the recipient information with the IBAN and BIC/SWIFT obtained from the SafePal App, and submit the transfer request after confirming that the transfer information is correct.

This means that after users transfer Euros into the personal Swiss bank account provided by SafePal, they can use "Buy Crypto" to convert Euros back into on-chain USDC or other crypto assets (currently supporting other swap-supported tokens), thus achieving bidirectional connectivity between crypto and Euros.

It is important to note that since SafePal & Fiat24 provide Swiss bank accounts, the personal IBAN starts with CH (the IBAN code for Switzerland) + 19 digits of the account number.

While SafePal and Fiat24 do not charge bank transfer fees, if the transfer involves Euro transfers outside the EU (such as from a New Zealand bank outside the EU), third-party banks may charge certain fees. Therefore, it is recommended to consult the relevant bank's fee policy before making a transfer.

In summary, through the above two methods, SafePal users can conveniently convert crypto assets into Euros or transfer Euro funds from other banks/financial institutions into their personal Swiss bank accounts and exchange them for USDC and other on-chain tokens, meeting the compliance needs for fund circulation.

On this basis, whether for deposits and withdrawals with overseas brokers, CEX deposits and withdrawals, daily consumption, transfers, or paying subscription fees for international services like 𝕏, the SafePal banking channel provides an efficient and low-cost solution.

2. Practical Application Scenarios of SafePal Banking Channel Service

The banking channel service jointly launched by SafePal and Fiat24 provides users with a compliant channel for low-threshold bidirectional conversion between crypto assets and Euros. Below are several typical scenarios of this service in practical applications:

1. Euro Deposits and Withdrawals with Overseas Brokers (such as Interactive Brokers, Charles Schwab)

Since the personal Swiss bank account provided by SafePal supports Euro transfers, users can directly transfer Euro funds into overseas broker accounts that support Euro SEPA deposits, such as Interactive Brokers (IBKR) and Charles Schwab, providing a more convenient funding channel for cross-border investment needs.

This article takes the Euro deposit process of Interactive Brokers as an example, with zero fees for deposits (and through Interactive Brokers, users can also exchange for USD, HKD, and other currencies at the best rates before withdrawing to US or HK cards, and more channels can be developed and tested by users themselves).

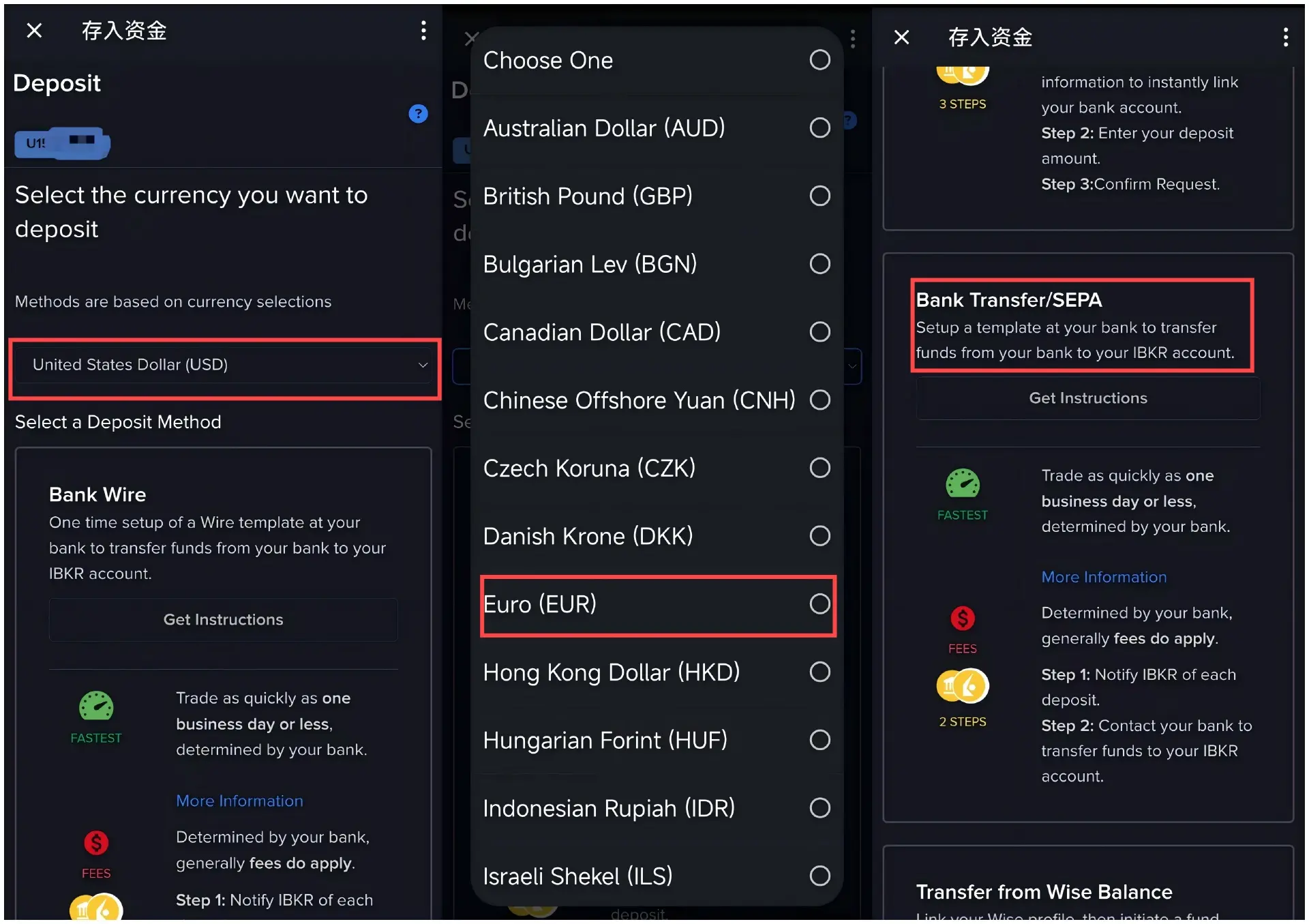

First, open the Interactive Brokers APP (the PC version can refer to a similar process), click the menu button in the upper left corner to enter the personal settings page.

Then click "Deposit Funds," and in the pop-up options, select the first "Standard Deposit" to enter the deposit page:

Previously, I have made multiple Euro deposits through SafePal & Fiat24, so as shown in the figure, there is a record of "Bank Transfer-SR Saphirs," which can be directly clicked later;

If it is a new user making their first Euro deposit, they need to click "Use a new deposit method" below to select and add a deposit payment method;

Then select EUR as the currency for remittance, choose the second deposit method "Bank Transfer/SEPA," and click "Get Instructions" to enter the transfer instruction page.

On the transfer instruction page, there are four items to fill out from top to bottom:

Remitting Institution (required): You can fill in "SR Saphirstein AG" (the operating entity name of Fiat24);

Account Number (optional): This is the personal IBAN number mentioned above (CH + 19 digits);

Deposit Instruction Remark (required): Generally, after filling in the first item, this item will be automatically filled;

Deposit Amount (required): Fill in the specific amount you plan to remit for deposit, for example, 50;

Note that after filling in the above four items, there is no need to check the "Make this a recurring transaction" box; simply click "Get Transfer Instructions" to obtain the transfer instructions.

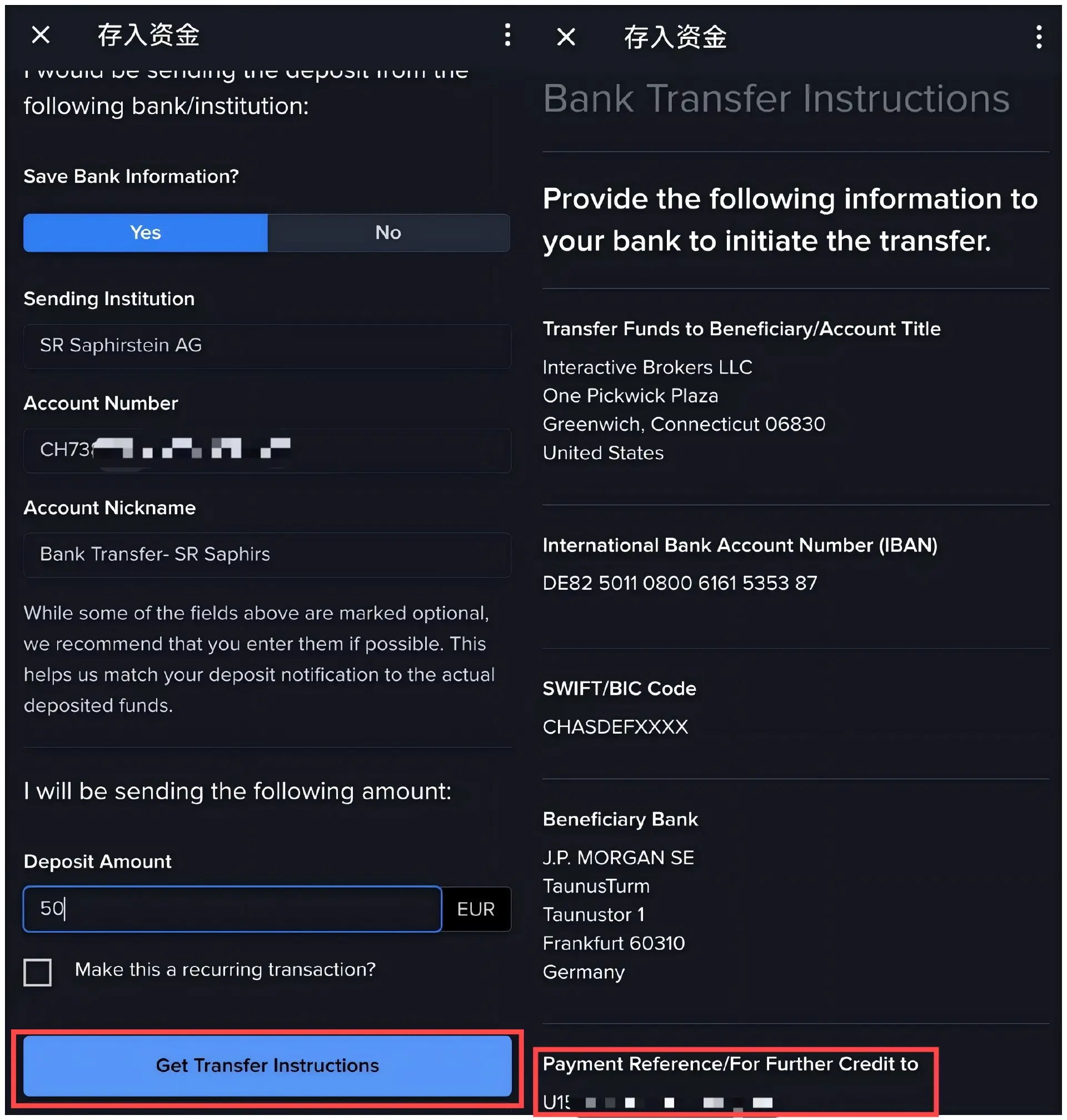

In the right half of the image below, detailed transfer instruction information will be displayed. Simply copy the payment reference at the bottom—personal UID/personal name in pinyin starting with U, similar to "U12345678/Tyler."

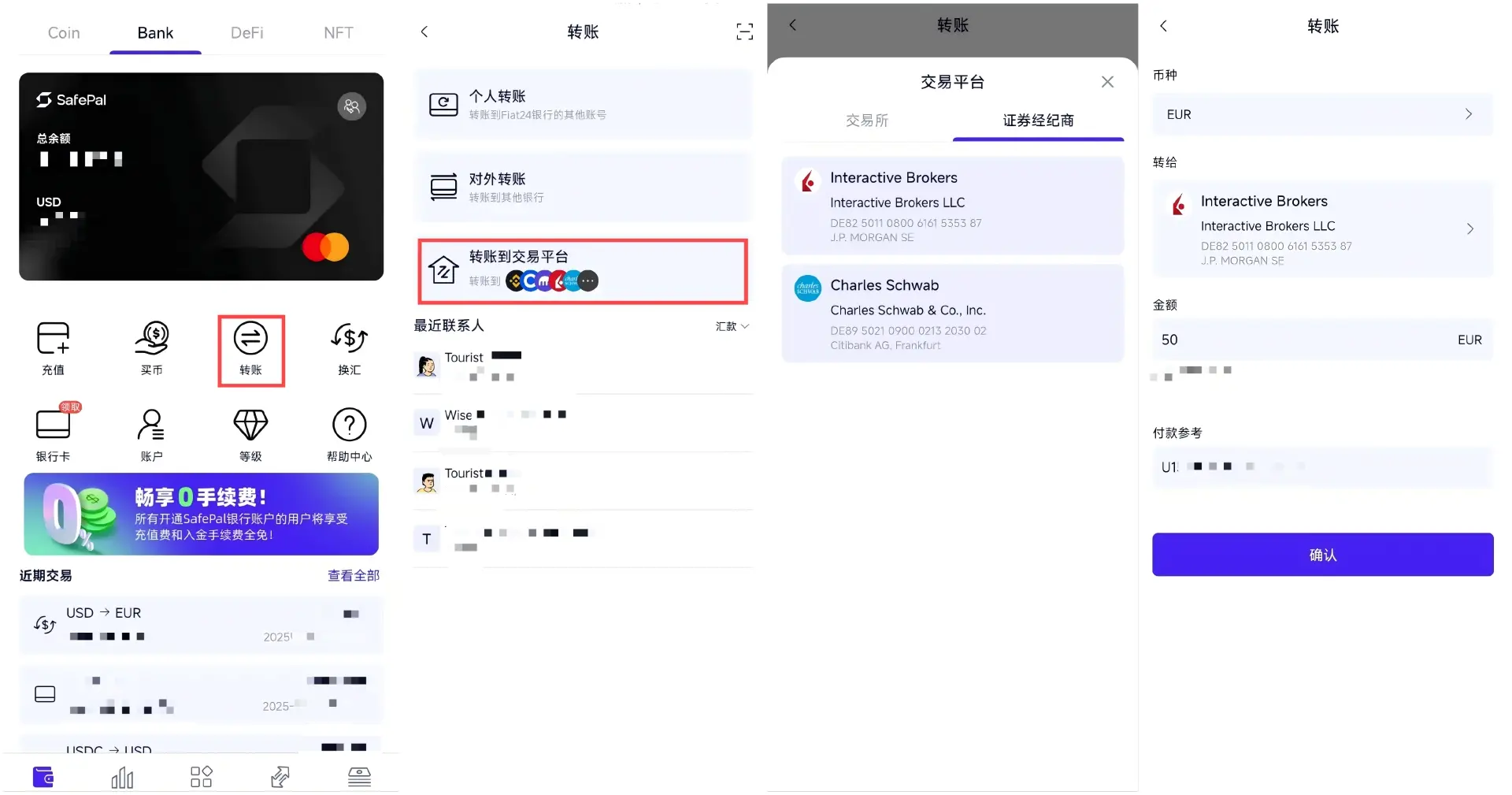

Then return to the "Bank" page in the SafePal Wallet APP, enter the "Transfer" service, click on the "Transfer to Trading Platform" option, select "Broker" and Interactive Brokers, and finally fill in the same transfer amount and payment reference as before in Interactive Brokers, click confirm, and complete the on-chain transfer.

Tips: After Fiat24 transfers Euros, users will receive an email notification; once transferred, funds can generally be credited to Interactive Brokers within a few hours on business days in Europe and the US.

2. Euro Deposit and Withdrawal Guide for Traditional Banks/Remittance Service Providers (such as domestic banks, Wise/Panda Remit, etc.)

For users who wish to achieve Euro deposits and withdrawals through traditional financial channels, SafePal provides a personal IBAN account in cooperation with the Swiss licensed bank Fiat24, supporting SEPA standard Euro transfers. Below, we will detail how to operate through domestic banks or third-party remittance service providers (such as Wise, Panda Remit).

(1) Deposit Service

For deposits, users in mainland China can use the legal foreign exchange purchase service of domestic banks to transfer Euro funds into the SafePal bank account through the following steps:

Purchase Foreign Currency: Buy Euro cash in a personal account at a mainland bank;

Obtain Payment Information: As mentioned above, in the SafePal Wallet App, click "Bank" > "Account" > "Account" > "Add" to get personal IBAN account information (or directly click "Recharge" on the "Bank" page to access the account details page for your personal IBAN account information);

Remittance: Transfer the purchased Euro cash into the Swiss bank account provided by SafePal through a bank counter or online banking;

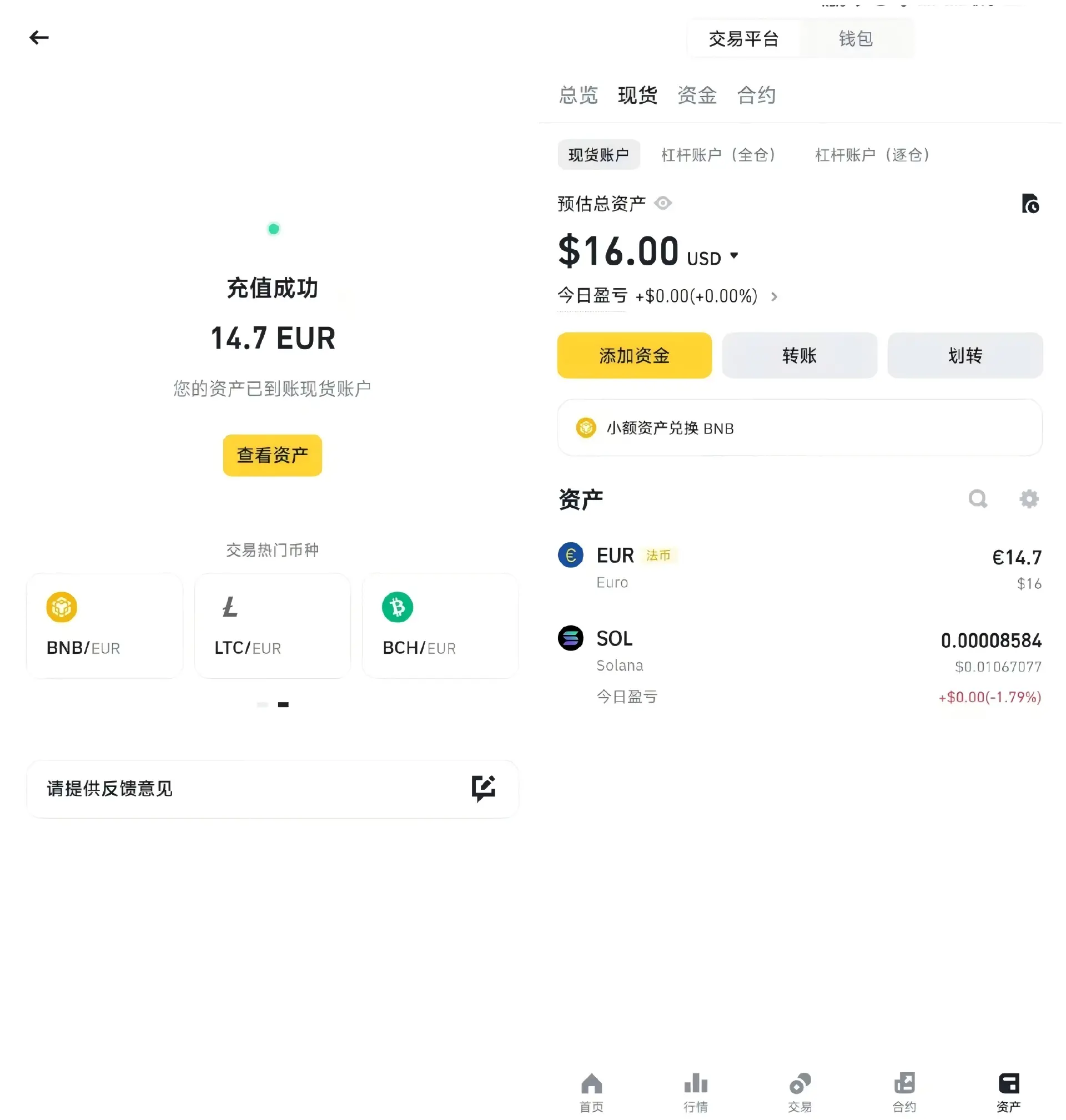

Buy Crypto: After the funds arrive, go to the "Buy Crypto" function on the SafePal bank page to exchange Euros for USDC or other swap-supported tokens, and the funds will automatically transfer to the user's SafePal wallet address;

Tips: Most domestic banks' mobile applications support online foreign exchange purchases and overseas remittance functions, making it easy to complete the above operations (be sure to compare the foreign exchange and remittance fees of different banks to find the most favorable path); in addition, you can also use international remittance service providers like Panda Remit to complete the deposit via the CNY-->EUR route.

(2) Withdrawal Service

Similarly, for withdrawals, you can choose to transfer Euros back to domestic banks that support SEPA Euro receipts for currency exchange and withdrawal.

Additionally, users can also transfer Euro funds from their SafePal bank account to a Wise account, and then use Wise to transfer funds to bank accounts in other countries or regions—such as Alipay or WeChat in mainland China, thus achieving cross-border fund transfers. This method is particularly suitable for users who need to transfer funds back to China.

When operating, you need to first register and activate a Wise account: new users can download the Wise App and complete registration (users in mainland China can use their passport), then activate the Euro account—Wise generally requires you to transfer a certain amount (e.g., 20 Euros) to activate the account. The transfer steps are as follows (the subsequent remittance to Wise follows the same steps).

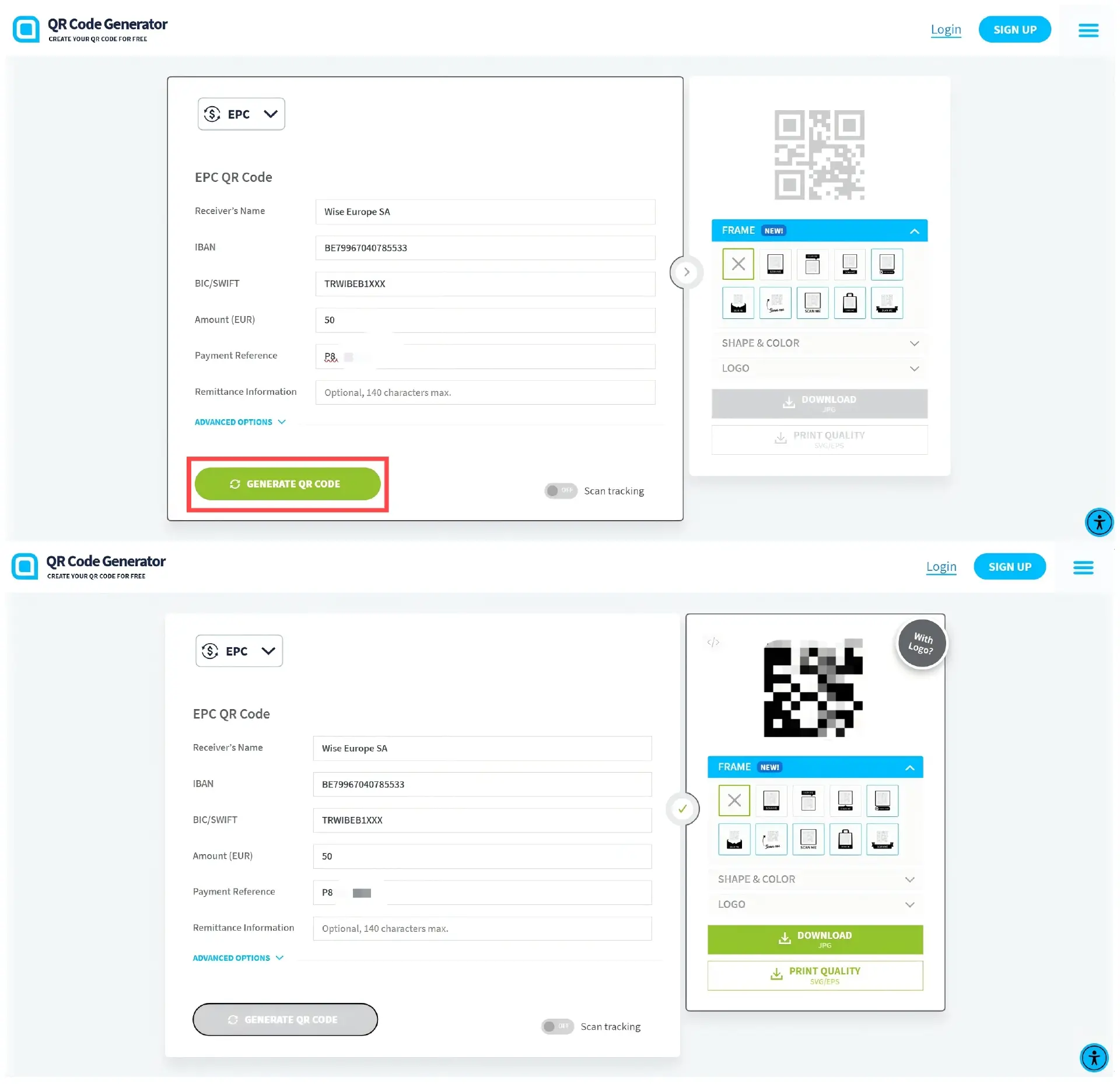

First, open Wise, click "Top Up" on the homepage, select EUR, enter the amount you want to remit to Wise (e.g., 50 EUR), and then choose "Manual Bank Transfer" as the payment method (other methods are currently not available for mainland users).

Then open the QR code generator website: based on the recipient account information from the last page of Wise, fill in the 5 required fields in order and generate a QR code (except for the last UID, the first four items should theoretically be the same for all users):

Recipient Name: Wise Europe SA;

IBAN: BE79967040785533;

BIC/SWIFT: TRWIBEB1XXX;

Amount to be Transferred: Fill in the specific amount you plan to remit, e.g., 50;

Payment Reference: UID starting with P + 8-digit number;

Then click "GENERATE QR CODE" in the lower left corner to generate the transfer QR code.

Finally, return to the "Bank" page in the SafePal Wallet App, click "Transfer," and use the QR code scanning function in the upper right corner to scan the generated QR code above, authorize the remittance transfer, and the specified amount of funds will be transferred to the account provided by Wise.

Finally, return to the "Bank" page in the SafePal Wallet App, click "Transfer," and use the QR code scanning function in the upper right corner to scan the generated QR code above, authorize the remittance transfer, and the specified amount of funds will be transferred to the account provided by Wise.

Once Wise receives the Euro transfer, simply select to remit to Renminbi (CNY) in the Wise App, choosing Alipay or WeChat as the payment method, and the maximum single transfer limit from Wise to mainland China is 50,000 RMB, with each recipient able to receive up to the equivalent of 50,000 USD in RMB per year.

Regarding fees, the remittance fee from Wise to mainland China is approximately 1%, with specific fees depending on the remittance amount (the higher the amount, the higher the fee, but the increase becomes smaller; in practice, transferring 50,000 RMB incurs about 450 RMB, which is less than 1%)—SafePal remitting Euros/Swiss Francs to Wise or any financial institution is free.

Tips: Wise's initial attempts may sometimes fail and refund the amount; from personal experience, if a failure occurs, try again a few times, gradually increasing the amount; after a successful remittance, wait a while, and the SafePal transfer page will have a contact record, allowing you to transfer funds directly to historical contacts without scanning the QR code again (according to official disclosures, a channel for directly adding contacts will be launched in the second quarter).

3. Deposit and Withdrawal Guide for Crypto Exchanges (CEX) (Binance, Kraken, etc.)

In the current financial environment, some traditional financial institutions may trigger risk control mechanisms for funds directly transferred from crypto exchanges (such as Kraken), leading to funds being returned or frozen.

To avoid such risks, users can utilize the crypto-friendly banking services provided by SafePal & Fiat24 as a transit channel to bypass risks, ensuring smooth fund flow.

Withdrawal Operation: Withdraw from the Exchange to SafePal Bank Account

Users can withdraw Euros from exchanges like Kraken to the Swiss bank account provided by SafePal. This operation not only reduces the risk of being flagged by traditional banks but also ensures the safe arrival of funds. After withdrawal, users can choose to convert the funds into USDC or other stablecoins for further investment or transfer.

Deposit Operation: Recharge Euros to Binance via SafePal Co-branded Mastercard

For deposits, you can also use the co-branded Mastercard of the SafePal banking channel service to achieve Euro deposits, with two entry points available in the Binance APP (you can choose either):

(1) Enter from the homepage "Add Funds," first switch the currency in the upper right corner from "CNY" to "EUR," then click "Recharge EUR."

(2) In the C2C service, first switch the currency in the upper right corner from "CNY" to "EUR," then click "Recharge Account with EUR."

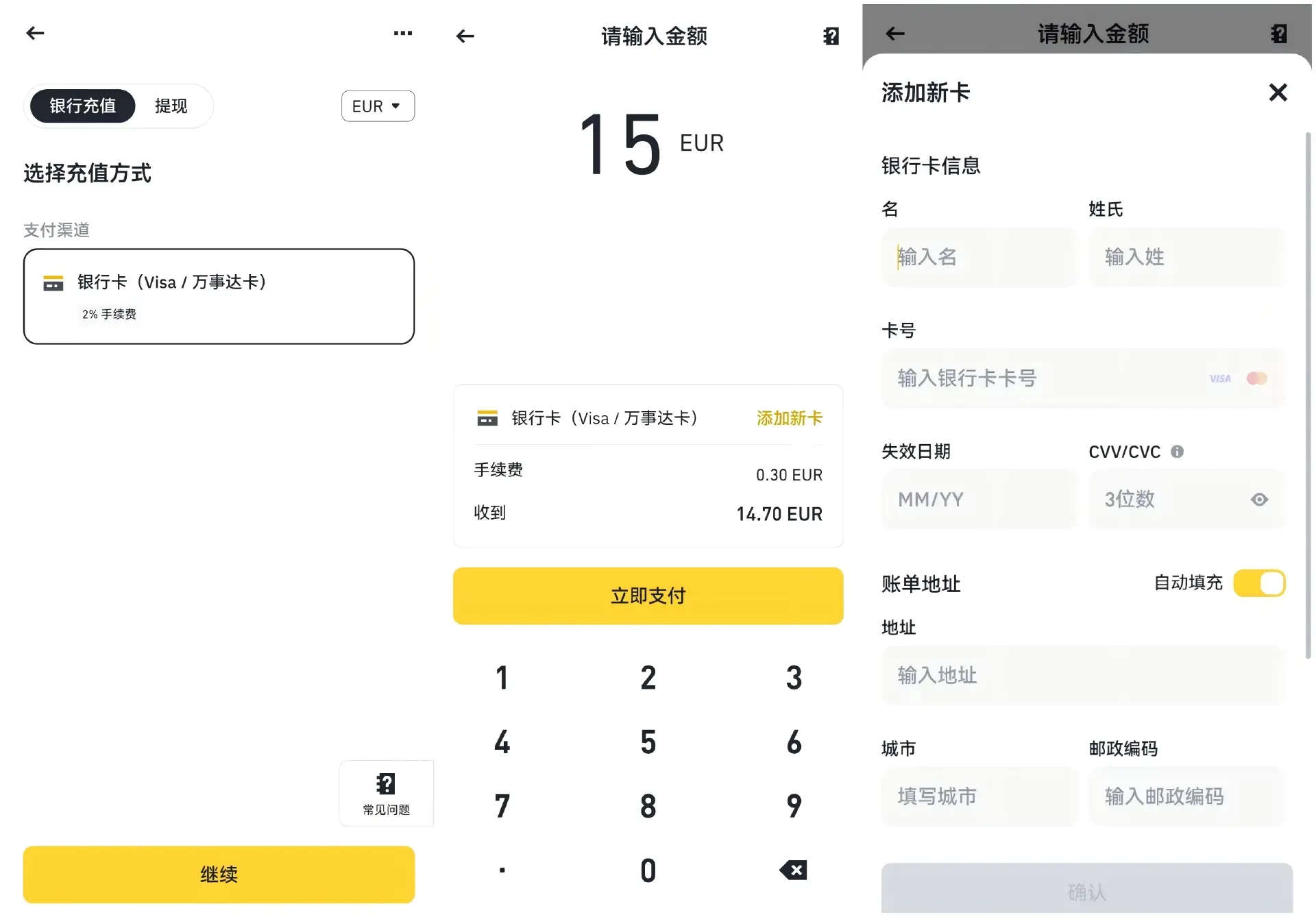

By using either of the above methods, you will enter the recharge page shown below, enter the recharge amount, fill in the SafePal Mastercard number, expiration date, and CVV, and proceed with the payment.

After completing the payment, the funds will be credited to the Binance account almost instantly, achieving Euro (SafePal Mastercard) → Euro (Binance account).

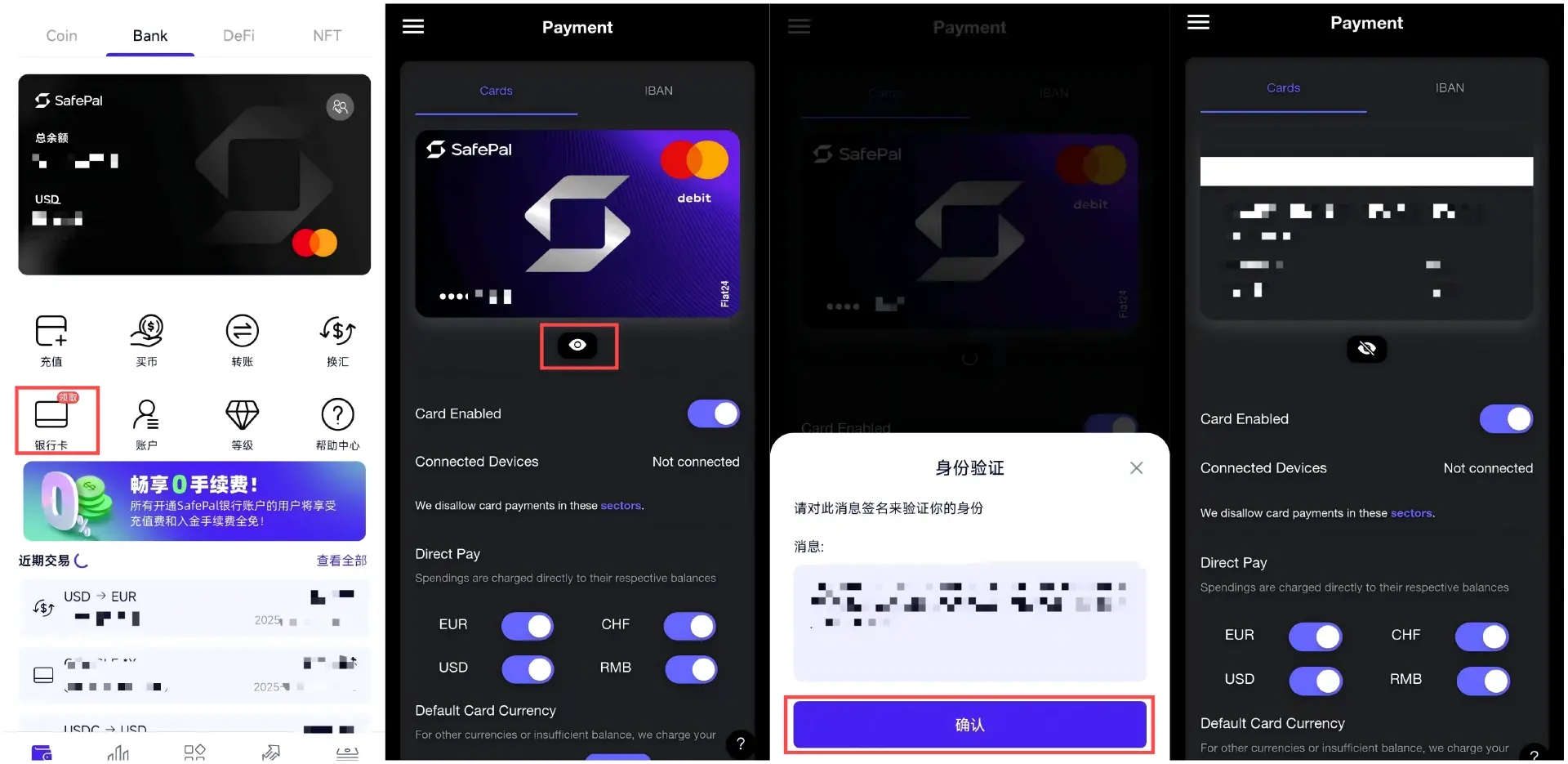

Note that if you need to view the detailed information required for the above Mastercard, you can copy the card information in the SafePal Wallet App:

On the "Bank" page, click "Bank Card" to enter the details page;

Click the "eye icon";

In the identity verification pop-up window, click "Confirm" to complete the wallet signature;

After authorization, you can click to view the complete card number, expiration date, and CVV security code for binding to WeChat, Alipay, or for use in other payment scenarios (note: do not disclose the CVV security code and card number to anyone);

Tips: Using the SafePal Mastercard for USD payments is theoretically possible, but it is not very meaningful, as Euros can primarily be transferred from other financial institution accounts to SafePal/Fiat24 via IBAN, and then deposited into Binance. This essentially provides a personal real-name account transfer channel for Euro deposits into CEX. For USD, the dollars in the Mastercard are originally loaded as USDC, so it just goes in circles.

4. Bind Apple Pay, Google Pay, and Pay for 𝕏 Blue Check and Other Overseas Subscriptions

The Mastercard service in the SafePal banking channel now also supports binding to mainstream payment platforms such as Apple Pay, Google Pay, and Samsung Pay, allowing users to use funds in their SafePal bank account in USD, EUR, CHF, and CNY for daily consumption.

The binding process for Apple Pay, Google Pay, and Samsung Pay is quite similar: (1) Open the "Wallet" App on your iPhone / "Google Pay" App / "Samsung Pay" App, and click to add a card; (2) Enter the SafePal Mastercard number, cardholder name, expiration date, and CVV security code (specific details as mentioned above); (3) Complete the phone number verification as prompted, entering the received verification code to complete the binding.

Once successfully bound, users can use the SafePal Mastercard for payments at merchants that support Apple Pay, Google Pay, or Samsung Pay:

In-App Purchases: Such as purchasing apps or in-game items in the App Store or Google Play;

Online Shopping: Shopping on e-commerce platforms that support Mastercard, such as Amazon, eBay, etc.;

In-Store Consumption: Making contactless payments at physical merchants that support Apple Pay, Google Pay, or Samsung Pay;

Subscribing to Other Services: Such as Netflix, Spotify, YouTube Premium, and other international subscription services;

Taking the recent example of the 𝕏 Blue Check subscription, users in China who lack usable overseas cards often encounter limitations with traditional payment methods. By following these steps, there is a workaround to successfully subscribe using the SafePal Mastercard:

On an Android device, open the "Google Play" App, go to "Payment Methods" settings, and add and bind your SafePal Mastercard;

Open the 𝕏 (Twitter) App, go to "Settings and Privacy" > "Subscriptions" > "Twitter Blue," and select the subscription option;

On the payment page, choose to use Google Play as the payment method, and the system will automatically call the bound SafePal Mastercard to complete the payment (though it may incur slightly higher fees than the web version);

Testing has shown that using the above method can bypass the limitations of traditional payment channels and successfully complete the 𝕏 Blue Check subscription.

III. User Experience and Precautions

Overall, the banking channel services of SafePal & Fiat24 can be divided into two parts:

Compliant Swiss Bank Account (IBAN starting with CH): Suitable for SEPA or SWIFT transfers in Euros (EUR) and Swiss Francs (CHF), commonly used for fund deposits and withdrawals to overseas brokers (such as Interactive Brokers, Charles Schwab) or exchanges (such as Binance, Kraken);

Co-branded Mastercard: Suitable for daily consumption, can be bound to payment platforms like Alipay, WeChat, Google Pay, etc., enabling online and offline payments;

Among them, the deposit and withdrawal operations of personal real-name bank accounts are all conducted in cooperation with licensed financial institutions/traditional banks, and all fund flows comply with the foreign exchange control regulations of mainland China, providing a much more compliant and secure channel for deposits and withdrawals than C2C.

According to the regulations of the State Administration of Foreign Exchange of China, individuals can conduct foreign exchange purchases and settlements equivalent to USD 50,000 per year. Through the SafePal bank account, users can fully utilize this quota to achieve efficient conversion between crypto assets and fiat currencies, meeting the needs for cross-border receipts and payments and asset allocation.

In practice, due to SafePal's ongoing long-term fee waiver activity, and no additional charges for incoming and outgoing transfers, users only need to bear the exchange loss and related fees from mainland banks (in some cases, there may be third-party intermediary banks), with a comprehensive fee loss of about 1%-3%—it is recommended to conduct currency exchange operations on business days to obtain better exchange rates.

It is important to emphasize again that the ownership of the SafePal bank account and Mastercard is bound to the user's wallet address through NFT, so it is essential to properly safeguard the mnemonic phrase and private key to avoid asset loss, and to ensure that the Mastercard-related information (card number and CVV security code) is not disclosed to others.

In Conclusion

Recently, crypto payment cards like U Cards in the Web3 ecosystem have proliferated, seemingly becoming the new darling of the market. However, to be realistic, many products under the "U Card frenzy" are essentially prepaid cards, with functions still limited to basic consumption payments—mainly focusing on binding Alipay/WeChat for offline QR code consumption and online payment subscriptions.

This fails to meet users' diverse needs in cross-border fund flows and asset allocation, as U Cards only achieve "consumer terminal access" but cannot construct a complete ecological closed loop for fund flows—for example, when users need to remit funds to Interactive Brokers, 99% of U Cards can only remain silent.

Therefore, objectively speaking, the services represented by SafePal & Fiat24 not only have competitive rates but also achieve differentiation in functionality—compared to traditional "U Cards," SafePal, based on its personal real-name compliant Swiss bank account, is one of the few products currently supporting Euro transfer remittances, providing users with a compliant, convenient, and secure channel for Crypto-fiat system deposits and withdrawals.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。