The disinflation story is under pressure.

Our markets team has been flagging this for three months, and this week's CPI print is the confirmation. That's a meaningful shift from the pre-war outlook and removes one of the reasons 2026 looked more resilient than 2022.

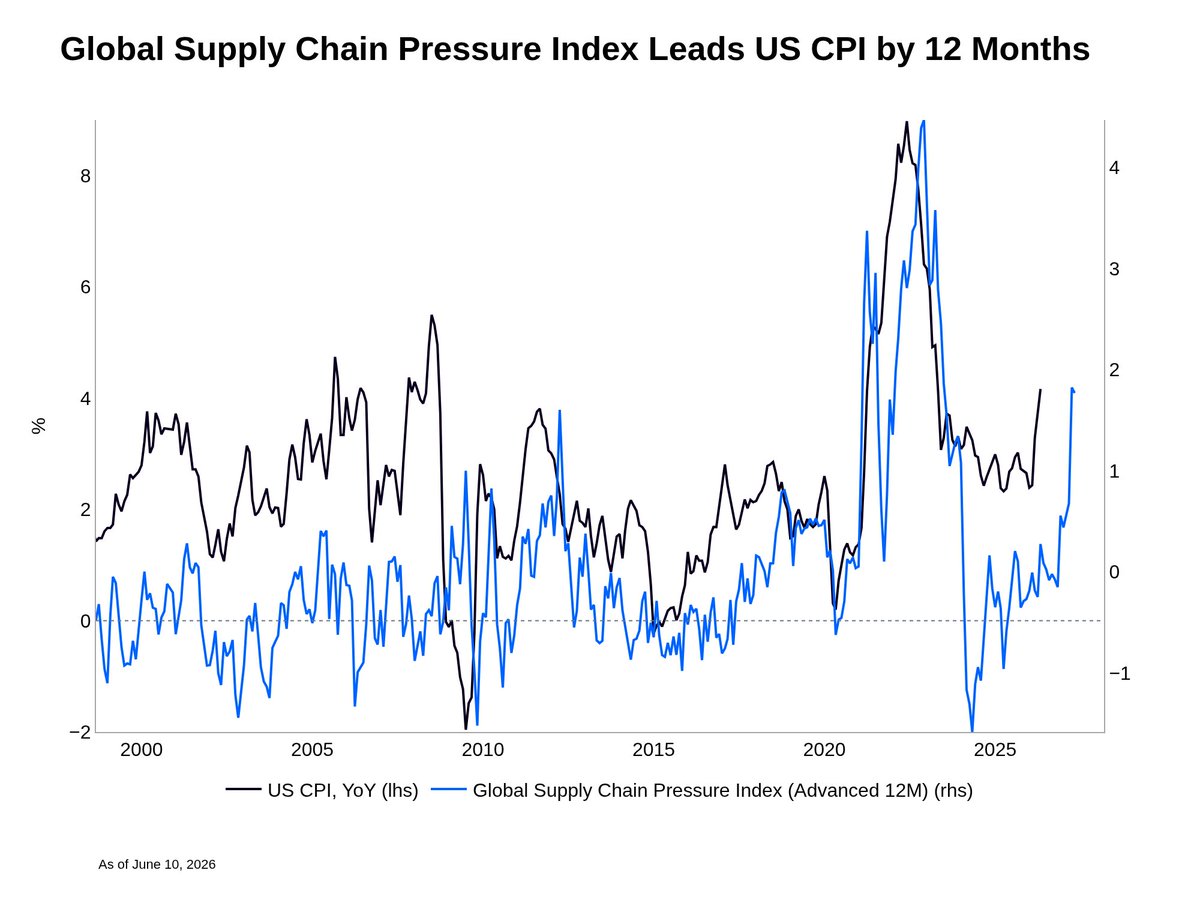

The oil shock from the Iran conflict is showing up in headline CPI. Core leading indicators are moving in the same direction. Prices paid remain elevated across manufacturing and services, and import prices ex-petroleum are picking up.

Wages are what's giving the Fed cover. Wages aren't yet accelerating enough to force the Fed's hand, but last Friday's reaction to a strong jobs print is a preview of how quickly that changes if labor data runs hot.

Against that backdrop, Warsh's first FOMC meeting lands next week. The market has a habit of testing incoming Fed Chairs (Greenspan in 1987, Bernanke in 2006). Consensus expects him to anchor on Dallas Fed Trimmed Mean PCE since it remains subdued.

But as a reminder, headline CPI leads it by six months.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。