NVIDIA's financial report is extremely impressive and can be said to clear away all the #AI bubble discussions.

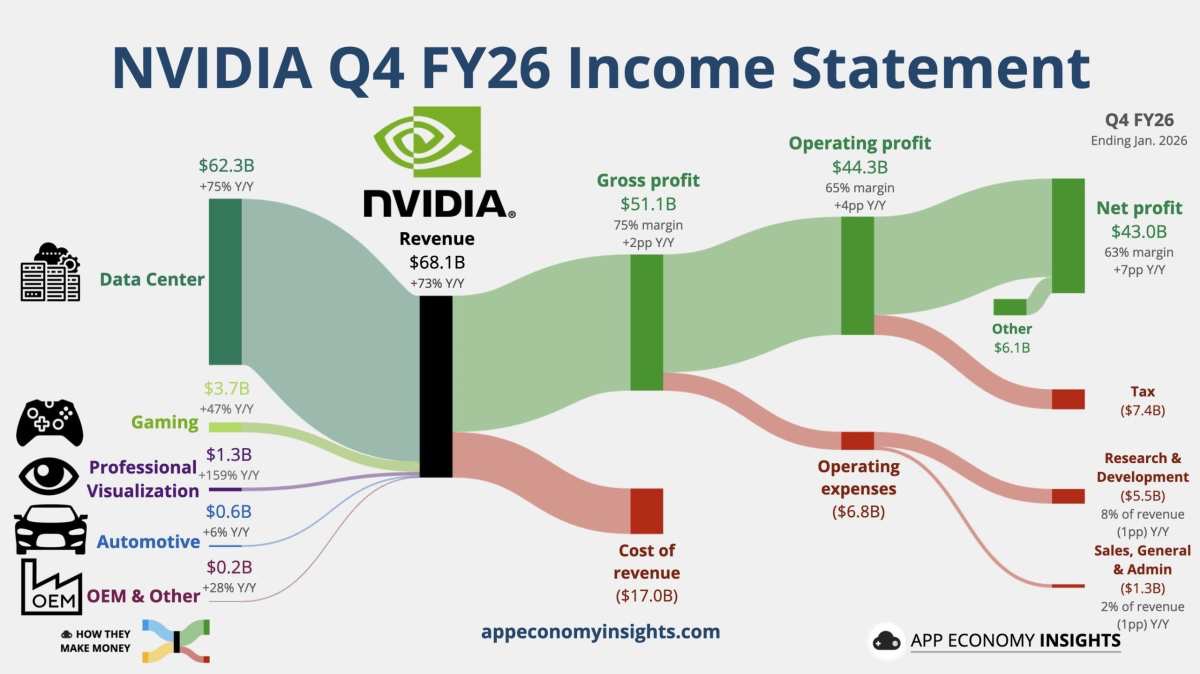

NVIDIA's Q4 financial report shows revenue reaching a record $68.1 billion, a 73% increase. The Q1 guidance is "explosive," marking a new high, and the revenue forecast has been raised to $500 billion. Last night, it directly drove the Nasdaq 100 index up 1.41%, further boosting the entire cryptocurrency market significantly!

With a market capitalization of over $4 trillion, achieving a revenue growth rate of 73% is indeed remarkable. Jensen Huang is not just selling chips; he is reshaping the profit distribution of the entire semiconductor industry. Many people believe the stock price fluctuations after earnings indicate that the good news is already fully priced in, but when viewed over a longer time frame, this seems more like long-term funds changing hands, and the logic remains solid and resilient.

1️⃣ Why is this financial report described as "flawless"?

Deep economic moat: Data center network revenue has increased 2.6 times. This means customers are not just purchasing GPUs but are deeply bound with NVLink, switches, and the entire software suite. If they want to switch to AMD or custom TPUs midway, the migration costs are prohibitively high.

Blackwell is not capacity constrained: Huang mentioned the delivery status, stating that Q4 is the "starting point," Q1 will "explode," and 2026 will be a big delivery year for Blackwell, with gross margins returning to over 75%, and Q1 guidance reaching $78 billion. Huang described the demand as "Off the charts," indicating that North America's cloud giants' thirst for computing power has not yet peaked.

Rubin chips are on the way: Huang has confirmed that the next-generation Rubin architecture platform will start mass production in 2026. This means NVIDIA is currently “eating from the bowl (Hopper/Blackwell) while watching the pot (Rubin).” This annual update pace makes it very painful for AMD and custom chip manufacturers to catch up and difficult to surpass.

$500 billion pie: Huang raised the chip revenue target to over $500 billion during the conference call. What does this mean? It almost aims to reshape the output structure of the entire semiconductor industry. His mention of skyrocketing "AI agents" is actually telling investors: AI is no longer just a toy in the lab; it has begun entering enterprise processes and generating real productivity.

2️⃣ What is the market worried about?

Despite explosive performance, the stock price hasn't surged, mainly due to two points:

First is the appearance of "slowing" short-term profit growth caused by accounting standard changes (SBC included in costs);

Second is the market's anxiety over ROI, as giants have spent hundreds of billions on chips. Can the application layer really bring profits back, especially with enormous capital expenditures (the seven big flowers revealed over $650 billion), leading to a particularly lengthy future return period?

3️⃣ The vertical spillover of investment logic

From "computing power" to "electricity," the current bottleneck of AI is no longer GPU capacity but the electrical grid load. In 2026, cloud giants' spending is expected to exceed $650 billion, and this money will not only flow to NVIDIA but also wildly snatch energy infrastructure.

If you think NVIDIA is too expensive, these three "water-seller" paths are worth more attention:

If we compare NVIDIA's GPUs to the most advanced supercars, then electricity is gasoline, transformers are the gas station pumps, and nuclear energy is that never-ending refinery. As observed, from 2025 to early 2026, US stocks' "energy infrastructure" performance has indeed been astonishing, even resembling the doubling trend of tech stocks back in the day.

👇 Here are the most representative US stocks in the "electricity family":

1️⃣ Nuclear energy stocks: AI's "top ration"

AI data centers require 24/7 non-interrupted, zero-carbon base load power; wind and solar energy are too unstable, and nuclear energy becomes the only "standard answer."

1. Constellation Energy (Ticker: #CEG)

Position: The largest nuclear power operator in the US.

Trigger point: It was the first to sign an "exclusive 20-year power purchase agreement" with Microsoft and even restarted the famous Three Mile Island Nuclear Power Plant to supply Microsoft.

Logic: This model of "one power plant supplying one data center" allows it to sell power at a premium far above market rates.

2. Vistra Corp (Ticker: #VST)

Position: One of the best-performing stocks in the S&P 500 in 2024-2025, even previously outperforming NVIDIA.

Logic: It has a large nuclear power asset base, mainly located in Texas (a high-growth area for data centers). Its flexible pricing mechanism makes it very profitable when electricity prices soar.

3. Talen Energy (Ticker: #TLN)

Position: A nuclear power company deeply tied to Amazon (AWS).

Trigger point: Amazon is directly buying land next to its nuclear power station to build a data center (this is the so-called "backyard power supply" model). Although recently there has been some controversy over this model in regulation, it remains a pioneer in nuclear power transformation.

2️⃣ Power and infrastructure stocks: The "heart" of the grid

Having just power plants is not enough; electricity needs to be distributed. The current electrical grid in the US is very outdated and cannot bear the immense load of AI data centers.

1. GE Vernova (Ticker: #GEV)

Position: An energy giant spun off from General Electric.

It is a global leader in gas turbine and grid solution providers. Whether the data centers rely on natural gas power or connect to the grid, they cannot bypass its technology.

Current situation: Its orders have been booked out for years, and its stock performance will be extremely strong in 2025.

2. Vertiv Holdings (Ticker: #VRT)

Position: The "manager" of data center infrastructure.

It does not generate electricity but is responsible for power distribution and liquid cooling in data centers. The heat generated by Blackwell chips is incredible and requires liquid cooling, where Vertiv has a monopoly in this field.

3️⃣ Transformer and equipment stocks: The most unassuming "golden eye"

If you want to invest in something that quietly achieves substantial returns, look at transformers. Currently, orders for transformers in the US are severely backlogged, with waits of 1-2 years for delivery.

1. Eaton (Ticker: #ETN)

Position: An absolute giant in electrical management.

Reason: It can be understood as the "pressure relief valve" and "switch" in the power grid. Each new server added to the data center needs accompanying transformers and distribution cabinets. Eaton's performance is extremely stable and highly determined by AI capital expenditure.

2. Hubbell (Ticker: #HUBB)

Position: A "parts supplier" for US grid construction.

Logic: Specializes in wires, cable fasteners, transformer accessories, etc. While it may not sound glamorous, during grid renewal and AI expansion, every single screw must be purchased from them.

From the current industrial landscape of AI data centers, electricity has become the biggest bottleneck. The power "self-production and self-distribution" policy proposed by Trump requires tech giants to solve energy issues themselves instead of siphoning resident electricity. This is a huge benefit for companies that can provide "independent microgrid" solutions (like CEG, VST). Such related companies deserve long-term attention.

Currently, the companies mentioned above are basically all available on #MSX. When trading US stocks, I choose to use the #RWA tokenized platform #MSX to participate in investing in the US stock market: http://msx.com/?code=Vu2v44

Early US stock investment fans and partners can DM me, and after filling out the form, can enter the US stock exchange and discussion community for free (currently limited to 10 people per week, assistant review required, which may take some time, thanks 🙏)!

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。