Extreme emotions, extreme cash reserves, growth that does not decline! Reversal? Bounce back? A slight difference in thought‼️

This morning I was still looking at last week's data, unexpectedly this afternoon the Bank of America data for this week came out, especially the global fund manager data is very important, three charts, three sentences for this week's data.

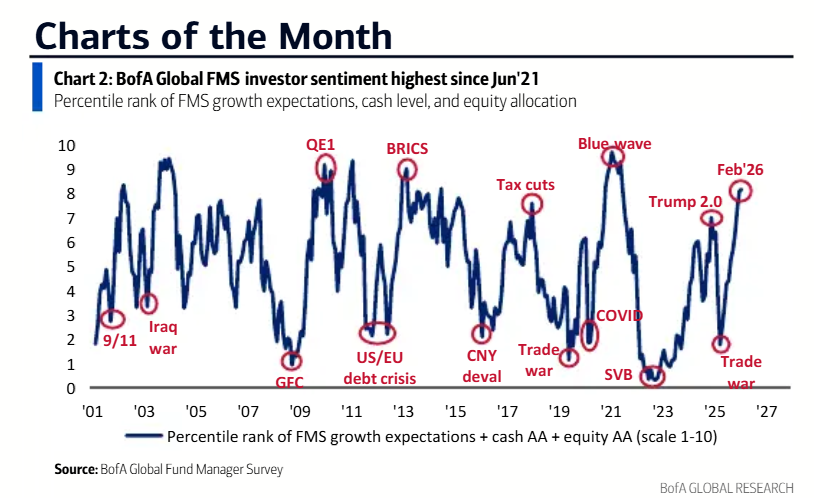

1. Extremely optimistic emotions.

Currently, global fund managers are very enthusiastic about the U.S. stock market, very optimistic, with very heavy positions.

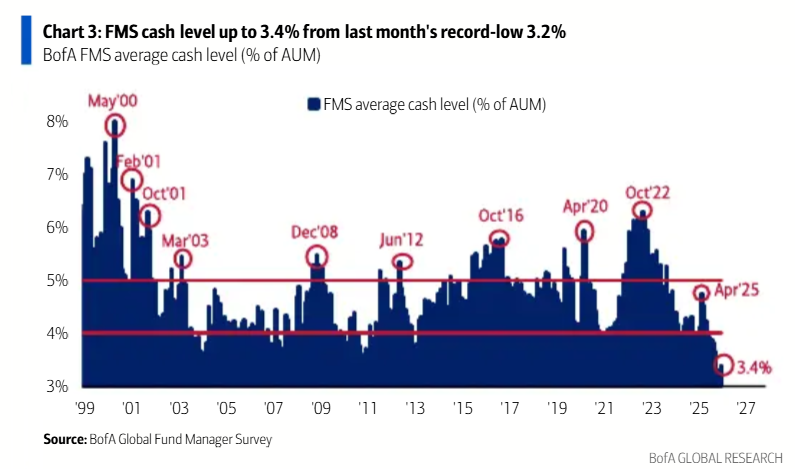

2. Extremely low cash reserves.

Last month, global fund managers set a new record for the lowest cash reserves, reaching a historical low of 3.2%. After a decline last week, it slightly rebounded to 3.3%, and this week it rose to 3.4%.

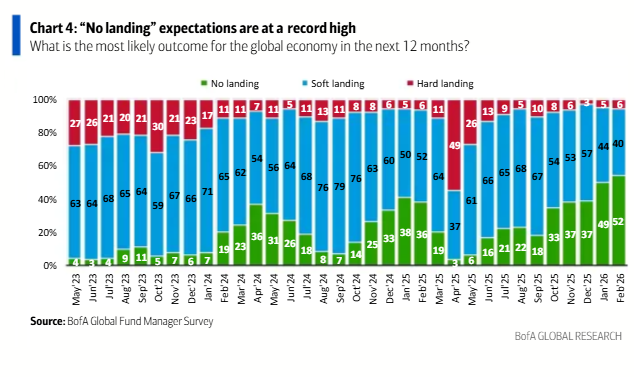

3. The economy is not landing.

Recent macro information has increased the global managers' perception of the U.S. economy's strength to 52%, while the likelihood of a soft landing has decreased to 40%, and the probability of an economic recession has slightly increased to 6%, but it is still the second lowest point in three years.

These three pieces of data combined represent that global fund managers are still very optimistic about the current U.S. market, optimistic about U.S. stocks, believing that the current high interest rates will not trigger an economic recession, and U.S. growth remains strong, but the cash on hand is still at a historically very low level.

In simple terms, global fund managers are optimistic about the economy and the market, but they are already out of ammunition.

The drop in the past few weeks, I mentioned at that time that it was very likely because global fund managers had no money to push up the stock market, coinciding with Microsoft's pessimistic expectations for its earnings report, leading to passive reduction by institutions, on one hand, institutions to avoid risk, and on the other hand, global fund managers to realize profits and increase cash reserves. The retail investors who were continuously buying at that time and a small number of hedge funds became the liquidity for institutions to exit.

Looking back at the current data, the likelihood of this scenario is very high. Along with the decline, global fund managers' cash positions have rebounded by 0.2%. Although still low, it is clear that institutions are in a selling state. Coupled with the data from last week showing that institutions, retail investors, and hedge funds are all selling, this again supports this viewpoint.

The decline is not because investors suddenly lost confidence, but because institutions have no money to continue pushing prices up, so they can only first free up positions for cash. The current mentality of institutions is actually very contradictory. Institutions have strong confidence in the economic non-recession, but not so strong confidence in valuation and capital expenditure.

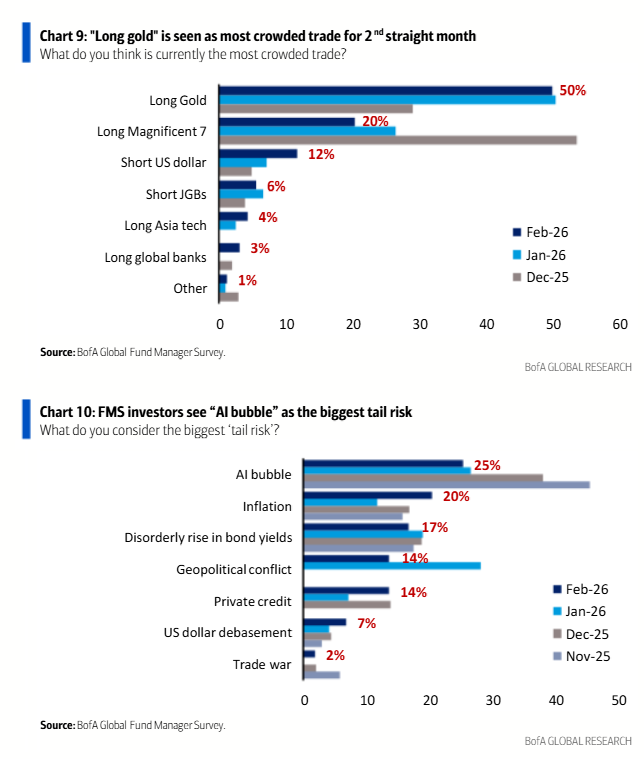

The current situation is very likely that institutions are optimistic about the market but worried about excessive capital expenditures, especially in the AI field, believing that the biggest risks may come from excessively high valuations of AI, overly high capital expenditures, and potential major defaults in the private credit sector.

Therefore, it can be seen that fund managers can passively reduce positions, can increase cash reserves, but are not willing to short, and to hedge against potential risks, they chose to go long on gold.

The upcoming scenario is probably like this: if macro data continues to support the economy without landing, AI profits continue to stabilize, and the Federal Reserve's monetary policy does not present surprises, institutions will slowly replenish cash, and the market may instead have conditions to move up a bit more, as institutions' ammunition replenishes and trends can continue.

However, if any narrative breaks, such as AI capital expenditure returns not meeting expectations, long-term U.S. Treasury rates suddenly going out of control, or substantive defaults appearing in private credit, then under a structure of high emotions and low cash, market pullbacks may be quicker, more violent, and more severe.

In summary, this report and the extended market expectations do not tell everyone to be bearish, but rather to inform everyone that the current market, while strong, is very fragile.

This is also why I used this title; the U.S. stock market is indeed still strong, driving cryptocurrencies and $BTC to have a fighting chance, but the premise is that AI and private credit do not blow up, and the Federal Reserve should not stir up trouble, otherwise the seemingly bullish market may collapse overnight.

PS: Many friends already know that the rise of Bitcoin is closely related to traditional institutions' purchases. When institutional cash stock is low, BTC and cryptocurrencies are definitely not on the priority purchase list. This is also why the U.S. stock market is strong, but cryptocurrencies always feel somewhat lacking.

However, it has been proven that the U.S. stock market, especially tech stocks, and Bitcoin still have a strong correlation; as long as the U.S. stock market is good, at least $BTC will not be too bad, but for a reversal, liquidity support is still needed.

@bitget VIP, lower fees, better benefits

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。