Source: Bright Company

Earlier, MoonShot AI released its latest model version Kimi K3, which has attracted significant attention in the capital market due to its leading performance across various scores. According to MoonShot AI's introduction on X, K3 is a multimodal model with 2.8 trillion parameters, supports a context of 1 million tokens, has native visual capabilities, and employs multiple innovative technologies.

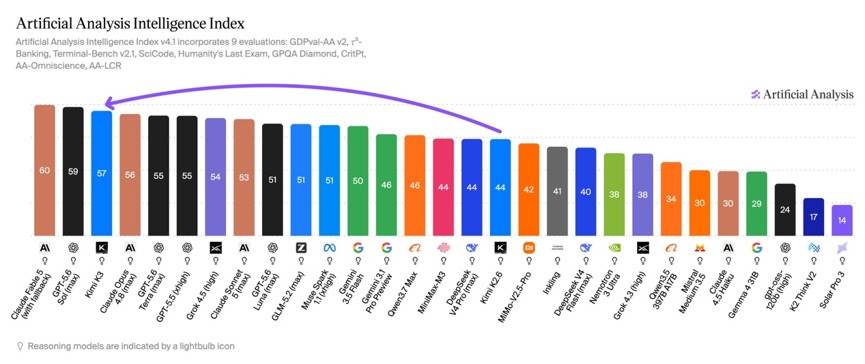

Artificial Analysis stated that Kimi K3 scored 57 on the Artificial Analysis Intelligence Index. Its intelligence level is comparable to Opus 4.8 and GPT-5.5, but still lags behind Fable 5 and GPT-5.6 Sol. MoonShot AI has indicated plans to release the weights of this 2.8T parameter model, which will make it a leading open-source model.

In the AI Arena Code ranking, K3 even surpasses Anthropic's Fable 5, Gpt5.6-sol, and Zhizhu's GLM-5.2 (max). Earlier, MoonShot AI completed its final round of financing, with a post-money valuation of approximately $31.5 billion. If evaluated purely based on ranking performance, this valuation level of MoonShot AI is much lower than that of Anthropic and OpenAI.

Another Chinese AI company that has also attracted significant attention in the primary market is DeepSeek. According to reports from The Information and Bloomberg citing informed sources, DeepSeek is advancing its second round of financing with a valuation of $74 billion, just a month after finalizing its first round valuation of $54.3 billion.

From a valuation perspective, the two primary market companies, DeepSeek and MoonShot AI, are approaching or even surpassing their comparables in the secondary market. Perhaps due to limitations in liquidity and information transparency in the primary market, Zhizhu and MiniMax have had a clear narrative consensus after over six months of continuous pricing in the public market—whether rewarded or punished by the market; while DeepSeek and MoonShot AI's valuations, though more aggressive, do not yet have a fully formed narrative around them.

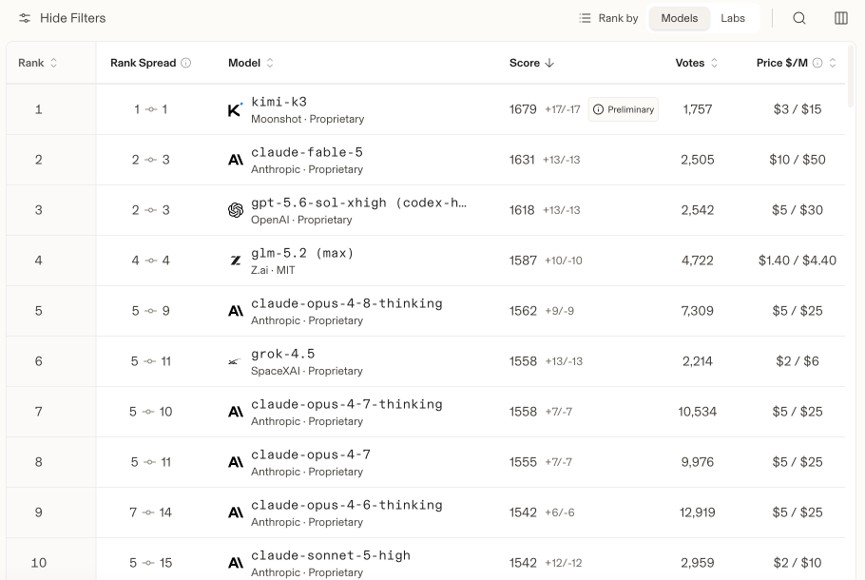

Kimi-K3 temporarily ranks first in the Arena AI Code list (Source: Arena AI)

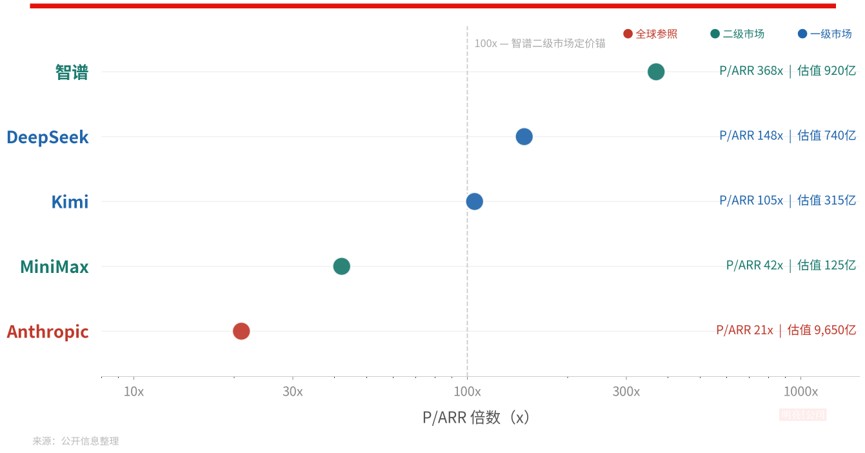

The narratives of the two companies in the secondary market: Coding performance and ARR growth slope

Zhizhu (02513.HK) and MiniMax (00100.HK)'s listings provide an evaluation line for independent model manufacturers in China. Viewed through the lens of P/ARR, the clarity of their narratives and the growth rate of ARR determine the extent of their premiums.

Since its listing in January this year, Zhizhu's stock price has surged over 1000%, with a market value of approximately $92 billion. This price is supported by a rare steep revenue curve: ARR increased from $67 million in January to $1 billion in July, growing 15 times in 7 months, completing its annual target six months ahead—multiple brokerages have pointed out that this slope exceeds Anthropic's previous record of reaching $100 million to $1 billion ARR in 15 months. The latest information from 36Kr shows that Zhizhu's ARR has already reached $1 billion, far faster than the expected $1 billion by the end of the year.

MiniMax's market value has retreated from its peak of about 410 billion Hong Kong dollars by approximately 75% to about 81 billion Hong Kong dollars, implying a P/ARR of about 13 times. "Bright Company" recently discussed the challenges of MiniMax's valuation narrative: as the industry focus shifts to Coding and Agent, MiniMax's "multimodal, C+B dual-wheel" multi-line layout has become the subject of market skepticism.

Active financing in the primary market

DeepSeek's first round of financing was signed at the end of May: with a scale exceeding 50 billion yuan, approximately $7.4 billion, it set the record for the largest single round in the history of Chinese AI large models.

According to The Information, the company explicitly informed investors during the first round roadshow: there was no intention to commercialize the model and would focus on cutting-edge research and development, without a specific IPO timetable. Liang Wenfeng had already begun planning for the second round before the first round financing was officially completed. The terms of this round underwent a fundamental shift: the valuation rose to $74 billion, an increase of about 36% from the first round.

The Information also stated that DeepSeek has planned to submit its application this year and aim for an IPO on the Shanghai STAR Market in 2027. The core factor driving all of this is the huge computational power expenditure required for model development.

The financing pace of MoonShot AI is also rare: at the end of 2025, the post-money valuation was only $4.3 billion; in May 2026, they completed $2 billion financing, with a post-money valuation of $20 billion, and by June 30, a new round had begun with a pre-money valuation of $31.5 billion, a more than 7-fold increase in valuation over half a year.

Both DeepSeek and MoonShot AI have achieved high valuations in the primary market, but the logic supporting these valuations seems to be different. The former relies more on usage volume, technical influence, and efficiency engineering; the latter seems to be replicating Anthropic's early revenue curve.

According to informants, DeepSeek's recent annualized revenue has reached $400 million to $500 million, mainly from API services; with a $500 million upper limit, a $74 billion valuation corresponds to approximately 148 times P/ARR—making it not only the highest among the four Chinese companies but also far surpassing many American AI startups.

From an analytical perspective, the reasons supporting this multiple may stem from three aspects.

The first is usage volume.

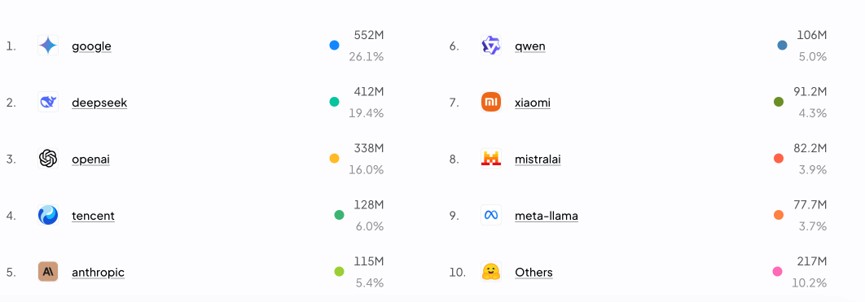

Zhongyin International's report on July 3 states that as of the week of June 22, DeepSeek ranked first globally on the OpenRouter platform with 6.7 trillion tokens, surpassing Anthropic's 4.25 trillion; in the second quarter of 2026, the total usage of OpenRouter increased from about 21 trillion to 46.66 trillion tokens, doubling within a single quarter, mainly due to contributions from Chinese open-source models, with Chinese manufacturers collectively surpassing American manufacturers in usage volume.

Source: OpenRouter

From the latest weekly market share rankings of OpenRouter, DeepSeek is only surpassed by Google, ranking second in market share.

The second is efficiency engineering. V4 has a token computation load in a million token context that is only 1/20 of that of the previous generation; V4-Pro's performance matches top proprietary models, and Jiangsu Securities assesses its performance to be close to Claude's non-thinking mode level.

The third is verified user experience. According to Bloomberg, despite its API charges being only a fraction of those of OpenAI and Anthropic, V4's sales gross margin remains over 50%—low prices do not equate to low margins, which is a key data point validating the "computational efficiency" narrative.

Additionally, strategically, the company launched the official version of V4 in mid-July and introduced a peak-valley pricing mechanism—this is its first pricing action with clear commercialization intentions; V4 is deeply adapted to domestic computational power from Huawei's Ascend and Cambrian, adding to its strategic positioning as a "domestic computational power closed-loop model layer anchor point," which is evident.

Now let’s look at MoonShot AI.

Its $31.5 billion pre-money valuation corresponds to about 105 times P/ARR, and if we use the $400 million to $500 million ARR guideline from experts given during the Nomura expert call, it would be about 70 times. As the Kimi K3 model is released, the market generally anticipates that the K3 model, expected to be released in the third or fourth quarter, will open up new pricing space.

Multiple brokerages have drawn parallels between MoonShot AI's revenue curve and Anthropic's early curve: a surge in developer usage, an increase in the proportion of APIs, growth in overseas paid subscribers, and price system elevation driven by model iteration.

Nomura's expert call minutes from July 6 indicate that experts expect its ARR to exceed $1 billion by the end of the year. However, from publicly available information channels, Yang Zhilin has never discussed the target of "ARR reaching $1 billion by the end of the year."

The premium of the narrative: where does it come from, and what will it face in the secondary market?

Comparing Zhizhu's approximately 100 times to MiniMax's approximately 13 times public market pricing, the sources of premiums for the two primary companies are distinctly different.

At least from previous valuations, MoonShot AI's premium leans more towards being "financial premiums" and "performance premiums."

If the ARR does indeed reach $1 billion by the end of the year, the $31.5 billion valuation corresponds to a forward multiple of only about 30 times—cheaper than Zhizhu's current valuation basis; investors are simultaneously betting on a "replication of Zhizhu's path" revaluation post-IPO. Zhizhu's last primary round valuation was $13.7 billion, and after listing, its market value once exceeded $100 billion.

This type of premium can be falsified and tracked, with monthly ARR data putting it to the test.

In comparison, for MoonShot AI, DeepSeek's premium contains non-financial premium components: usage volume, technical influence premium constituted by architecture definition authority, geopolitical options arising from national strategic scarcity, and the "founder's belief" backing formed by Liang Wenfeng's personal investment of 20 billion yuan... etc., especially the impact of the "DeepSeek moment" on the revaluation of Chinese assets, which at present seems impossible for other manufacturers to replicate.

A static multiple of 148 cannot be reconciled with any cash flow model; investors are buying into the belief that "when the commercialization switch is completely turned on, it has the ability to generate Anthropic-level revenue."

However, as these two companies head toward IPO, they will face the continuous pricing mechanism of the public market, which will also bring some changes, even pressures, to their valuation logic.

First is the quarterly verification of growth rates. The primary market can pay for "narratives," while the secondary market is increasingly paying for "realization." In its early days, MiniMax's listing received a market giving its valuation of about 65 times P/ARR, but as the industry narrative shifted to Agents, its monetization path faced questions, and its valuation was ground down by three-quarters.

DeepSeek's mid-range pricing experienced a 95% deflation of inference prices in the second quarter. According to Zhongyin International data, the optimal usage price for the intelligent index in the 40-50 range dropped from $1.2 per million tokens in March to $0.058 in June. Whether "usage volume first" can continue to transform into revenue growth will be a mandatory question for every quarterly report.

The second aspect is the supply side's release pressure. Zhizhu and MiniMax saw their stocks fall by 8.5% and 22.5% respectively during the July release week, followed by a combined over 40 billion Hong Kong dollars in placements—this "release-placement" supply shock will similarly await DeepSeek and MoonShot AI, both of which are set to go public in the future.

Lastly, there’s the need to unify the valuation coordinate system, such as "single token monetization rate" becoming a directly comparable indicator.

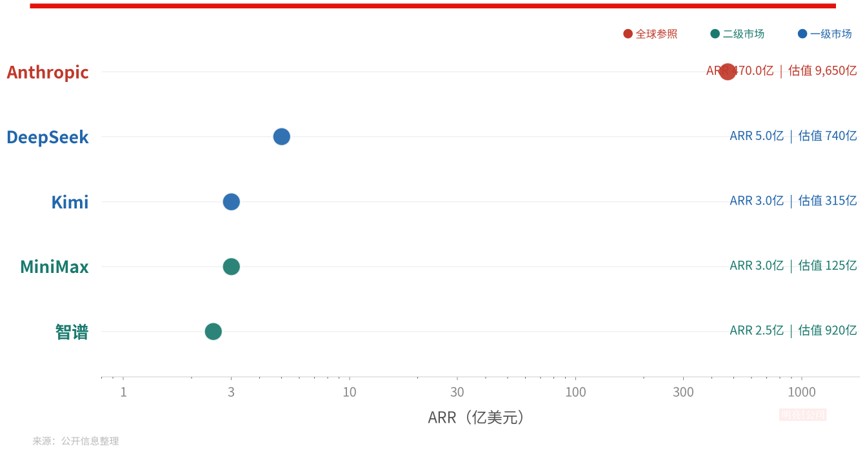

Source: Public information compilation, Bright Company (valuations, market capitalizations as of July 16 close, not including Zhizhu's latest rumored ARR)

Moreover, at the narrative level, a benchmark object that current Chinese model companies cannot bypass is Anthropic.

On May 28, Anthropic completed a Series H financing of $65 billion with a post-money valuation of $965 billion, and it has confidentially submitted an IPO application. Its ARR increased from $9 billion at the end of 2025 to $47 billion by May 2026.

According to Jefferies' citation of SemiAnalysis, its July ARR will exceed $60 billion, with a net revenue retention rate of about 500%, and an API gross margin exceeding 80%, expecting to achieve over $1 billion in GAAP operating profit in the third quarter.

Based on a $47 billion ARR, a $965 billion valuation corresponds to about 20 times P/ARR. OpenAI has also confidentially submitted an IPO application, with an ARR of about $25 billion—once the absolute leader, its revenue scale has now been surpassed by Anthropic.

Anthropic's valuation multiple has compressed from 184 times when its ARR was $1 million to about 20 times now. This means that DeepSeek's 148 times and MoonShot AI's 105 times are essentially prepaying valuation for "revenue growth that has yet to occur"—the downward multiples are certain; the only variable is whether ARR growth can outpace multiple contraction. After Zhizhu's ARR reached $1 billion in July, its present value multiple has significantly digested from early-year levels.

Additionally, in terms of "geopolitical competition," Jefferies’ report on July 13 indicated that as American manufacturers gain more next-generation computational power in the second half of the year, coupled with a reverse distillation mechanism, there exists the possibility that the capability gap between China and the US models will widen again. Currently, the entire logic of valuation for Chinese models—from Zhizhu's 100 times to DeepSeek's 148 times—implicitly presumes the "continuation of the narrowing capability gap," and at least the release of K3 appears to mitigate the judgment of the "expansion of the capability gap" to some extent.

Currently, whether from financing valuation or model performance, MoonShot AI and DeepSeek are performing optimistically.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。