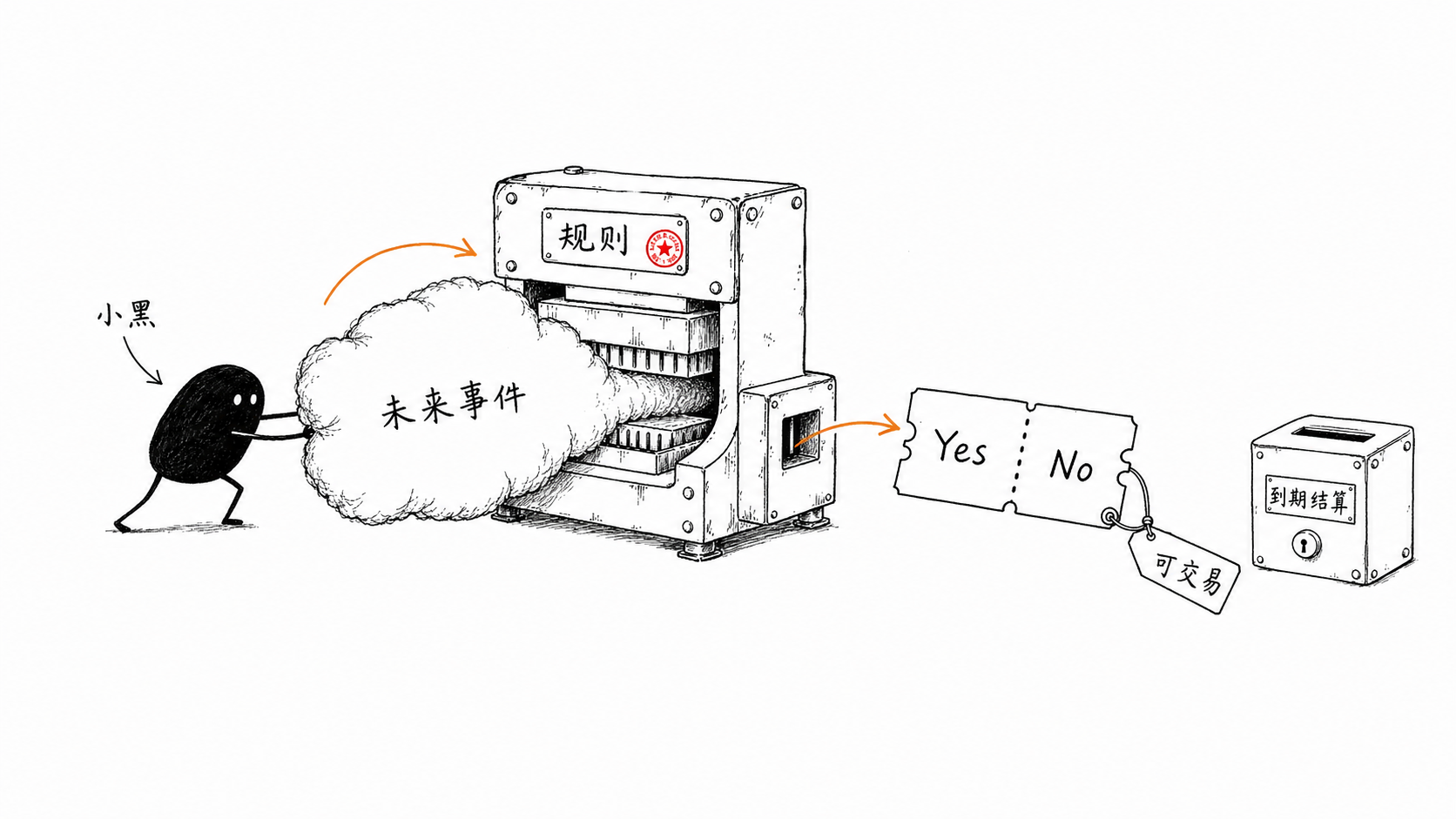

What is an Event Contract?

An event contract poses a verifiable question and predefines outcome options and settlement conditions. Common structures include:

Yes/No: For example, "Will a certain indicator reach the target by the specified date?"

Higher/Lower: Determining if the expiration price is higher or lower compared to the entry price.

Threshold: Determining if the final value is above, below, or not below a certain value.

Multiple Outcomes: Setting multiple mutually exclusive results for the same event, with each result quoted separately.

Participants trade on the contract's outcome. The contract terms typically specify the market question, cutoff time, time zone, official data source, boundaries, handling of event cancellations or delays, and the payout amount for the winning contract. Markets with similar titles may follow different rules.

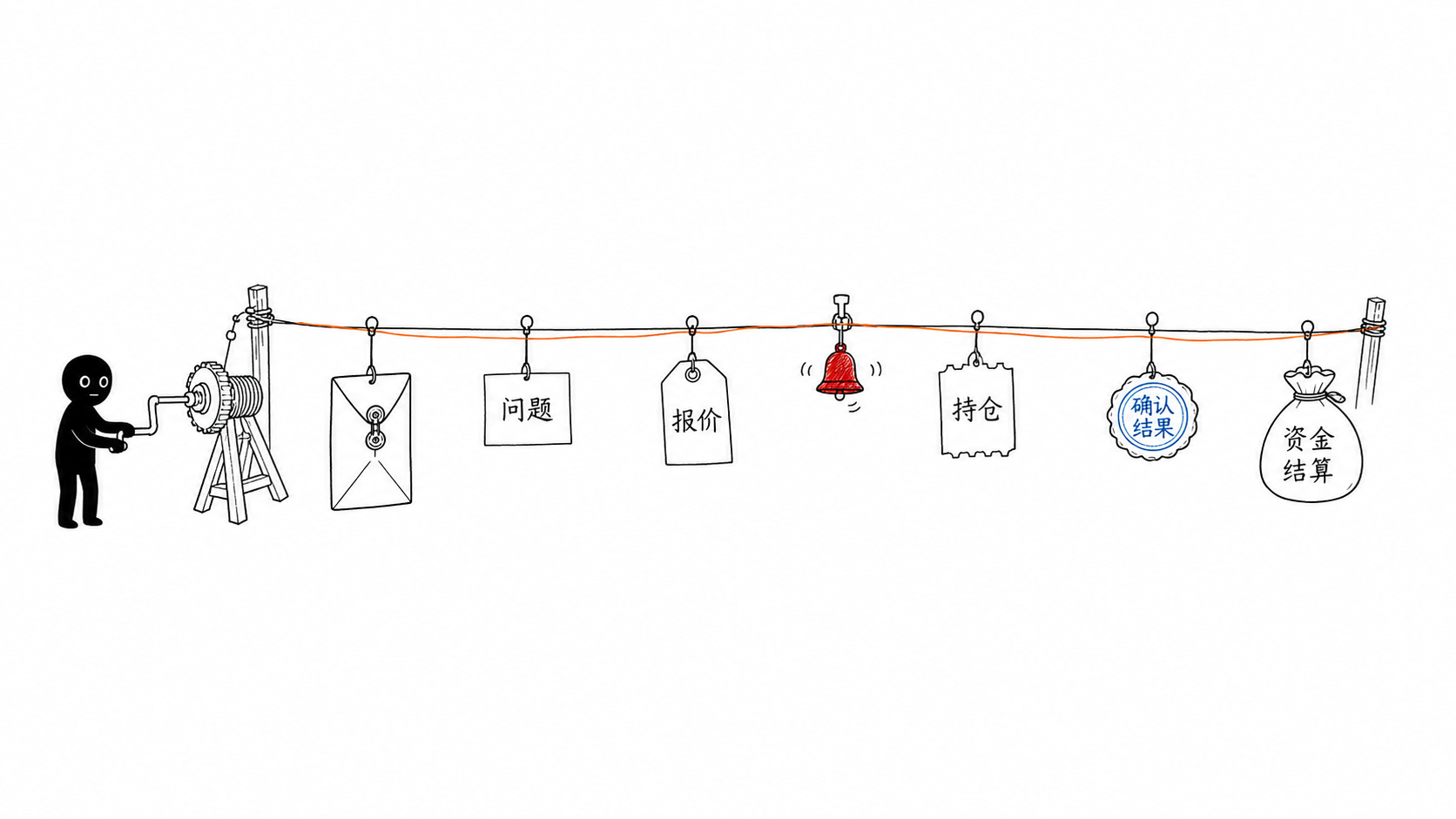

How Does an Event Contract Operate?

1. Create Market: The platform defines the question, outcomes, trading cutoff time, and settlement source.

2. Form Quotations: The order book platform generates quotes from buyers and sellers; products using an automated market-making mechanism generate quotes from a market-making model and display participation amounts and return information before confirmation.

3. Establish Position: Once the order is executed, participants hold a position in a particular outcome direction. Some platforms allow selling before the market closes, with execution depending on liquidity.

4. Stop Trading: The market stops accepting trades after the cutoff time is reached, the event begins, or other conditions set by the platform are met.

5. Confirm Result: The platform, exchange, or pre-designated oracle confirms the result based on contract terms and data sources.

6. Complete Settlement: Binary contracts typically settle the winning side at $1 per share, while the losing side returns to zero; fixed return products calculate according to rules locked in at confirmation.

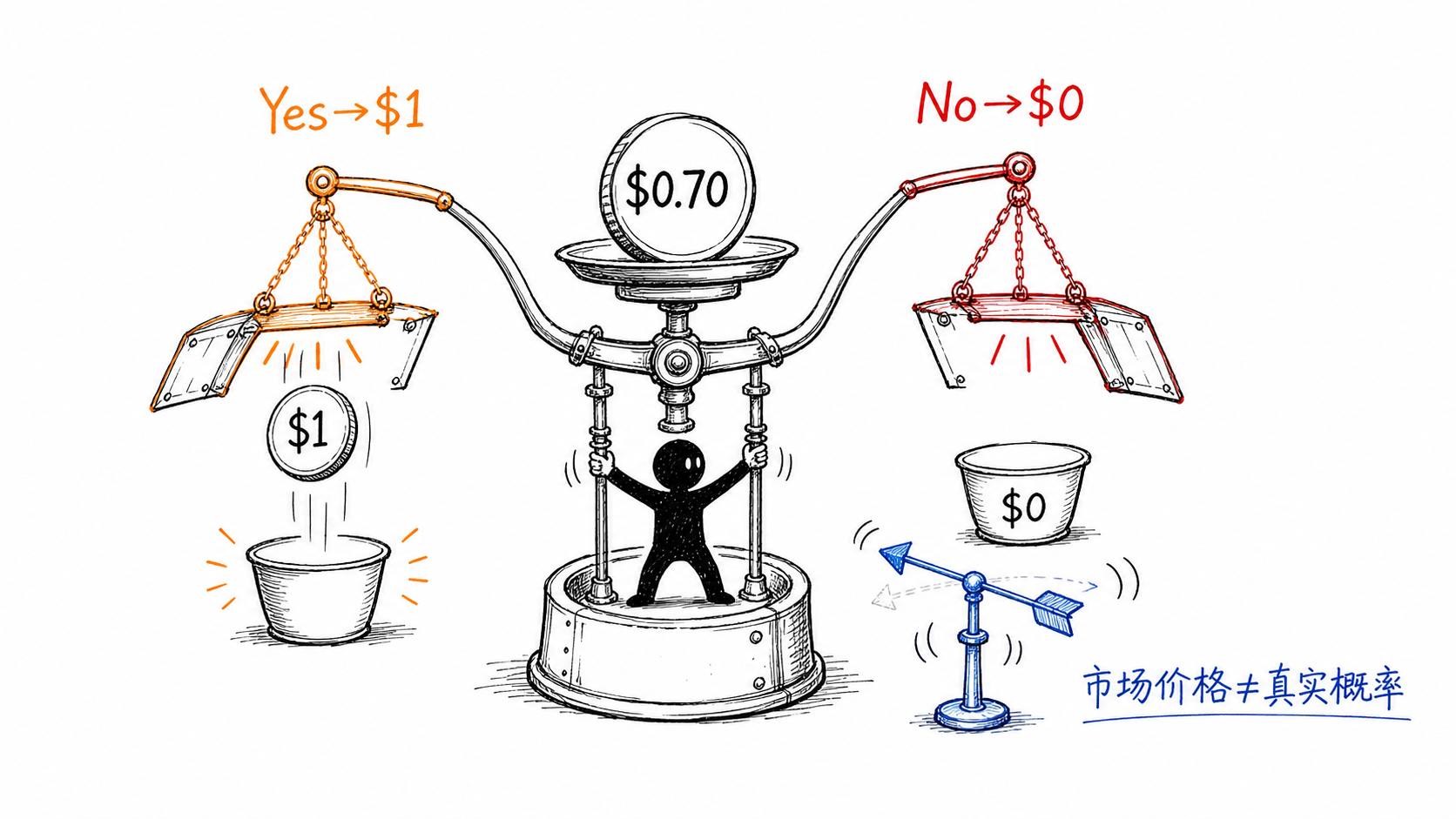

What Does 70 Cents Represent in Pricing?

In binary contracts with prices quoted between $0 and $1, the price is often understood as the market's implied probability. A "Yes" contract price of $0.70 implies that the current market pricing corresponds to a probability of occurrence of about 70%.

If the final result is "Yes," each share typically pays out $1, yielding a gross profit of $0.30 before costs and spreads; if the result is "No," that contract's value returns to zero, with a maximum loss of the $0.70 invested.

Prices are affected by new information, order book depth, bid-ask spreads, and participant supply and demand. The displayed 70% only reflects the current market price and cannot guarantee that the true probability of the event is 70%. Fixed return products using an automated market-making mechanism also take into account cycle, volatility, and risk parameters to form quotes and display return rates; participants should simultaneously consider principal, expected returns, and maximum potential losses.

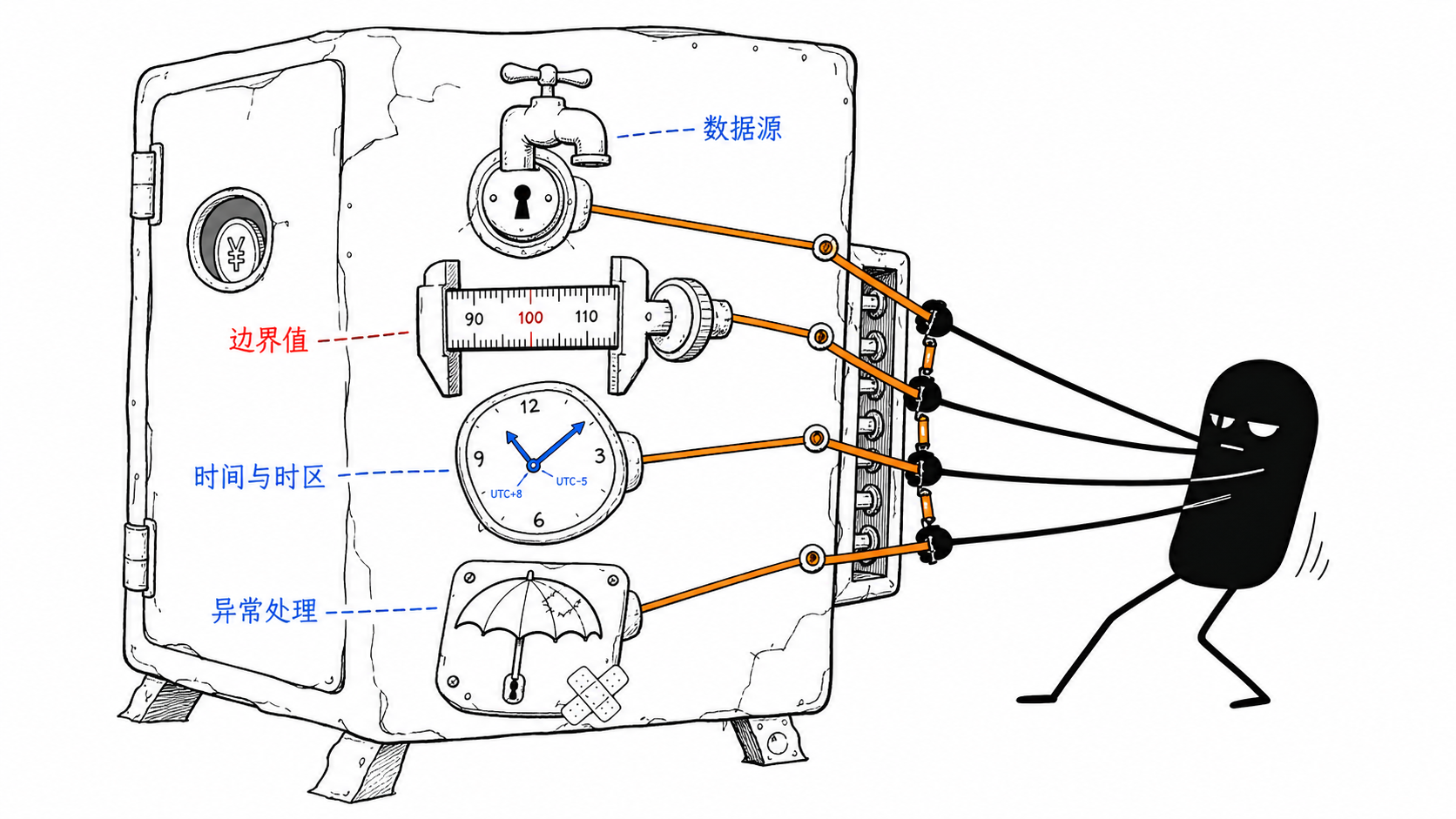

What Details Should One Look at in Settlement Rules?

Settlement Data Source: Government agencies, event organizers, price indices, exchange data, or oracle may all serve as the final basis.

Comparison Symbols: "Above 100" typically means strictly greater than 100; "100 or above" includes equal to 100.

Time and Time Zone: The specific time point and time zone for settlement, and whether the price sampling is instantaneous, closing value, or an average over a period.

Exception Handling: How to handle delays, cancellations, data corrections, price source interruptions, or long-unresolvable results.

Dispute Process: Who can propose results, how long the objection period lasts, and who makes the final decision.

Fees and Payout: Trading fees, platform commissions, on-chain fees, and withdrawal costs can all affect actual returns.

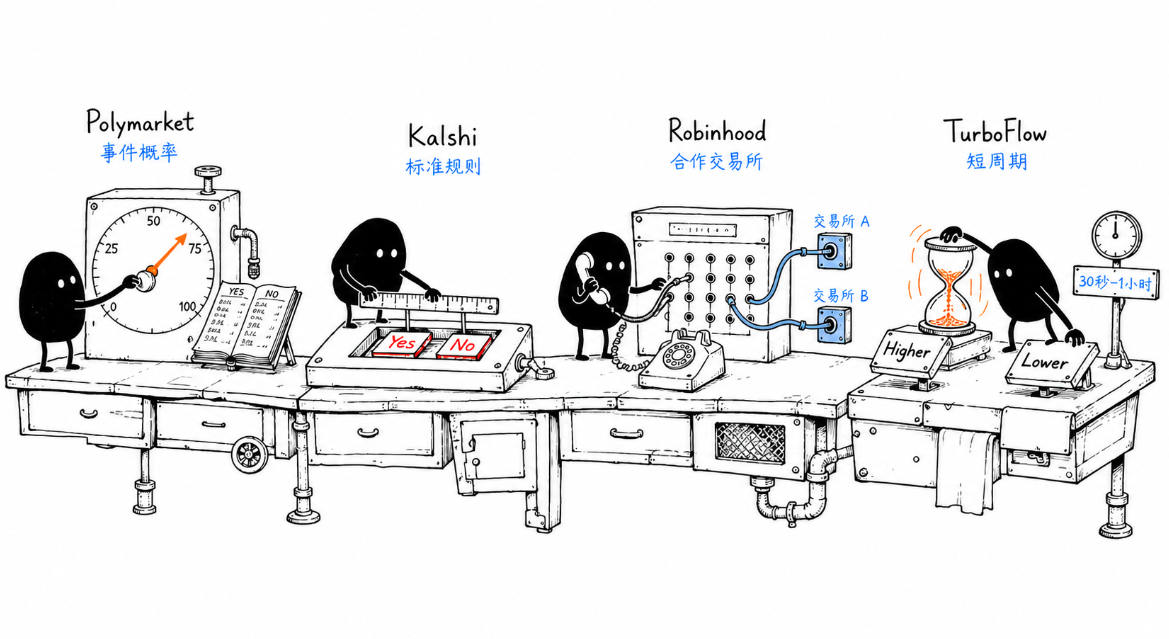

Platform Product Evaluation

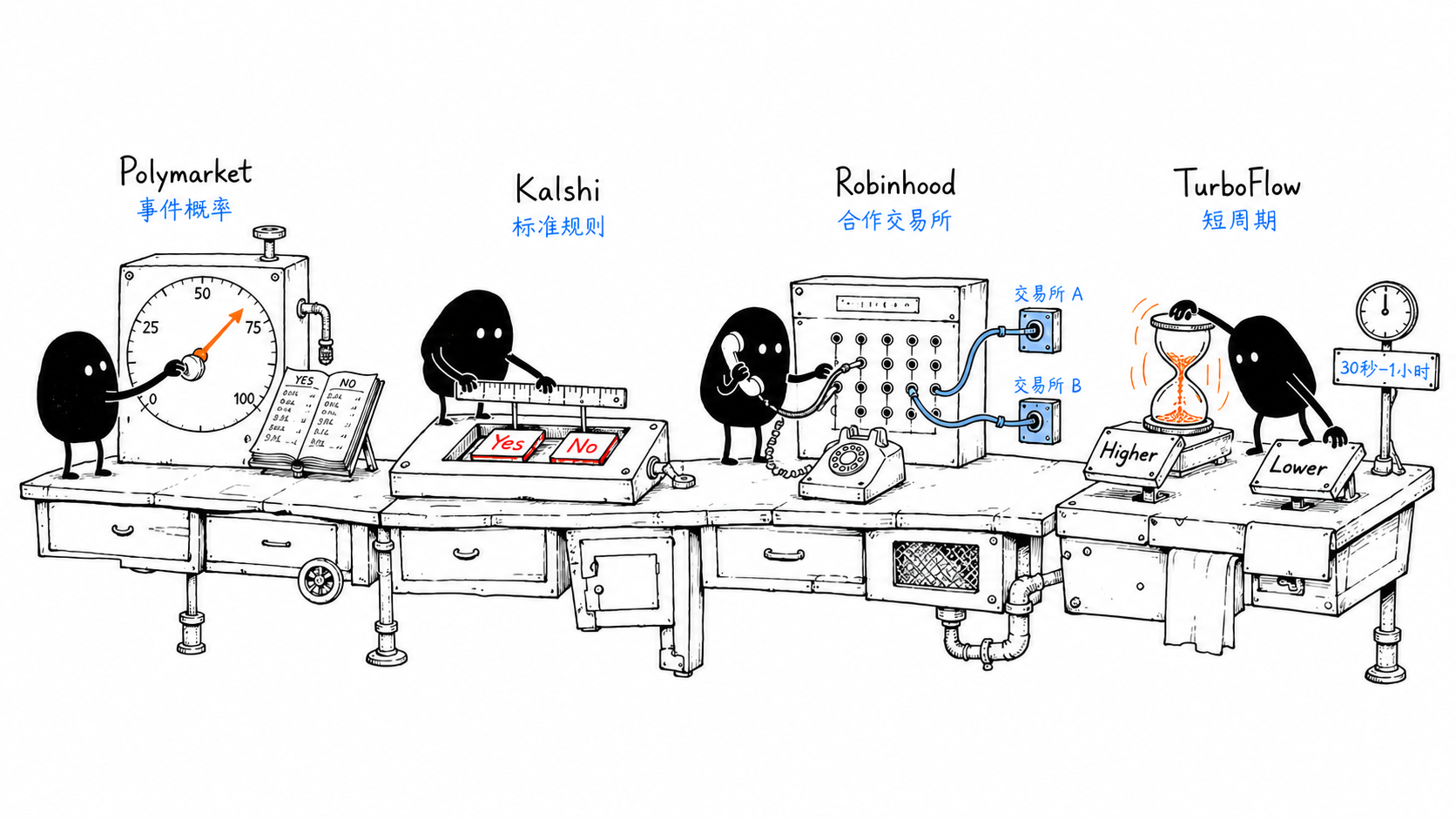

Polymarket: Continuous Trading Event Market

Polymarket is a prediction market that continuously trades around event probabilities, forming prices through an order book and involving the UMA oracle in result confirmation.

Specific Products: Mainly consists of yes/no result shares, covering categories such as politics, macro, sports, crypto assets, and cultural events; markets typically remain open until the event occurs and settlement is completed.

Quotations: Utilizes an order book. The displayed page probability usually shows the midpoint between the bid and ask price; when the bid-ask spread exceeds $0.10, the page switches to the most recent transaction price. Matching quotes for "Yes" and "No" total $1.

Trading and Exiting: When the market is open and there are counterparties, participants can buy or sell result shares through the order book. Limit orders can control transaction prices; however, if liquidity is insufficient, exiting at the expected price may not be possible.

Settlement: Handled by the UMA optimistic oracle according to pre-announced market rules. There is a challenge period after the result is proposed; final winning shares pay out $1 each, while losing shares return to zero.

Fees: The current official explanation is that some markets charge fees to the party taking on the orders, while makers are not charged; different market categories may have different parameters, and it is necessary to check the latest rates before entry.

Evaluation: Suitable for users who wish to continuously trade event probabilities, use limit orders, and pay attention to market depth. Main checking points are rule wording, bid-ask spreads, on-chain wallets, oracle dispute processes, and regional availability.

Kalshi: Standardized Yes/No Event Contracts

Kalshi is an event market focused on standardized yes/no contracts, clear market rules, and order book trading.

Specific Products: Primarily consists of yes/no contracts and threshold contracts, with each market listing a clear summary of rules, expiration conditions, and result verification sources.

Quotations: Uses an order book, with contract prices expressed in cents. A $0.70 "Yes" contract and a $0.30 "No" contract can form $1; the bid price, ask price, and available quantities can directly influence execution.

Trading and Exiting: Positions can be established using the order book, and participants can exit by selling orders while the market remains open and liquid. Unfilled orders can be canceled.

Settlement: Each contract's clauses specify the adopted information and sources. After the contract expires, Kalshi confirms results according to these terms; official explanations state that settlement confirmation may take more than one to twelve hours after market closure, depending on the data source.

Fees: Trading fees are calculated based on expected returns and other factors, and some markets may also charge fees to the makers. Canceling unfilled orders incurs no fees, and it is recommended to check the actual fees on the market page before confirming orders.

Evaluation: Product terms and verification sources are clearly presented, making it suitable for users who value standardized rules, order books, and the ability to exit early. The fee formula, market liquidity, and qualifications of the region need to be verified separately.

Robinhood: Accessing Partner Exchanges via Familiar Interface

Robinhood serves as an entry point for event contracts through a familiar interface connected to partner exchanges; actual quotes, settlements, and special rules are determined by the exchanges that carry the contracts.

Specific Products: Robinhood's derivatives business provides event contracts through KalshiEX, ForecastEX, or Rothera Exchange and Clearing, with common formats including single yes/no, threshold contracts, and combined outcomes.

Quotation and Payout: Individual prices typically range from $0.01 to $0.99, with correct results settling at $1 in cash and incorrect results at $0. Before placing an order, the price and applicable fees will be displayed.

Trading and Exiting: Unfilled orders can be canceled; executed orders cannot be withdrawn. As long as the market is open and there are buyers, positions can be sold at current market prices; during market closures or lack of liquidity, positions must be held until settlement.

Settlement: Final results are determined by the corresponding partner exchange based on the official data sources and terms specified in the contract; Robinhood cannot alter the settlement decisions of the exchanges.

Fees: May involve both exchange fees and Robinhood commissions, with specific amounts displayed on the order confirmation page.

Evaluation: Suitable for users who already use Robinhood and value a unified operational interface. When reading terms, it is essential to verify the actual exchange carrying the contract, as settlements, fees, and special event rules are determined by specific contracts.

TurboFlow: On-Chain Trading Ecosystem for Retail Investors

TurboFlow is an on-chain trading ecosystem aimed at global retail investors, integrating prediction markets and perpetual contracts, offering perpetual contracts, event contracts, and prediction markets on the same platform, reducing participation barriers for ordinary users through transparent execution and professional liquidity.

Specific Products: This section evaluates TurboFlow's event contracts, specifically fixed-time window "higher/lower" contracts. Users select markets, participation amounts, cycles, and directions; the minimum participation amount is $2, and the fastest round can be completed in 30 seconds, with real-time parameters based on the product page.

Quotation and Participation: Automated market maker (propAMM) forms quotes based on market, cycle, and risk parameters; before confirmation, entry price, participation amount, cycle, direction, return rate, and expected results will be displayed, and the return rate for that contract will be locked after order confirmation.

Settlement: The entry price is the price at which the order is accepted, and the settlement price is the price used at contract expiration. When choosing "Higher," the settlement price must be higher than the entry price to meet the direction; when choosing "Lower," the opposite is true. If they are the same, principal is returned according to official rules.

Position Management: Automatic settlement occurs once the countdown ends, and there is no need to manage margin, funding rates, or forced liquidations during the holding period; this mechanism differs from the platform's perpetual contract products.

Evaluation: TurboFlow targets retail investors, lowering the participation barrier for event contracts to a minimum of $2 and a maximum of 30 seconds, integrating perpetual contracts and prediction markets on the same platform. Short-cycle "higher/lower" contracts are more sensitive to entry timing, market fluctuations, and price data.

Core Differences

Price Formation: Polymarket and Kalshi mainly rely on order books; Robinhood displays market quotes from partner exchanges; TurboFlow event contracts use automated market makers (propAMM) to form quotes and display entry price, participation amount, cycle, direction, and locked return rates before confirmation.

Time Span: Polymarket, Kalshi, and Robinhood contracts typically operate around the event cutoff time; TurboFlow event contracts employ fixed time windows, with rounds completed in as little as 30 seconds.

Early Exit: The first three types of products can usually sell positions when the market is open and liquid; TurboFlow event contracts emphasize holding until the countdown ends and automatic settlement.

Settlement Authority: Polymarket uses UMA oracle; Kalshi confirms according to its market terms and designated sources; Robinhood is determined by partner exchanges; TurboFlow event contracts automatically settle based on pre-disclosed contract rules, using credible market data sources and multiple oracles to generate entry and settlement prices.

Applicable Scenarios: For those concerned with continuously changing event probabilities, focusing studies on Polymarket would be beneficial; for standardized market rules, research on Kalshi is advisable; for a preference for Robinhood's unified interface, viewing contracts from partner exchanges is recommended; for those wishing to participate in low-barrier short-cycle "higher/lower" contracts, researching TurboFlow event contracts is encouraged.

Main Risks

Principal Loss: If the direction judgment is incorrect, a single contract may return to zero, and fixed return products may also lose the participation amount.

Rule Risk: Ignoring boundary values, time zones, data sources, or exceptional clauses may lead to incorrect expectations regarding settlement results.

Liquidity and Spread: There may be significant differences between displayed probabilities, tradable prices, and early exit prices.

Settlement and Data Risks: Official data delays, corrections, oracle disputes, or price source anomalies may prolong settlement and trigger special rules.

Fee Risk: Trading fees, commissions, on-chain network fees, and deposit/withdrawal fees will reduce actual returns.

Technical and Compliance Risks: Account security, smart contracts, platform operations, and regional restrictions may all impact product availability.

Conclusion

Understanding event contracts involves examining five stages: "Question Definition — Price Formation — Trade Exit — Result Confirmation — Fund Settlement." Polymarket, Kalshi, Robinhood, and TurboFlow event contracts adopt different product paths; TurboFlow itself is an on-chain trading ecosystem integrating prediction markets and perpetual contracts, and this article reviews only its event contract products. The platform name cannot replace verifying the terms of a single contract, as the true determinants of the outcome are the time, data sources, boundary conditions, and exceptional handling rules specified in the contract.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。