TL;DR

- According to a Morgan Stanley research report, the capital expenditures of the five largest cloud vendors could reach $1.4 trillion by 2028.

- The cost of building per GW is increased by memory, electricity, and construction, and computing capacity may expand from 30GW to 120GW.

- META is listed as the top choice in AI internet, with a target price of $775 depending on the realization of API, advertising, and subscription monetization.

Morgan Stanley has raised its capital expenditure estimates for major cloud vendors in a sell-side research report, forecasting that the total capital expenditures of the five platforms will reach $1.2 trillion and $1.4 trillion in 2027 and 2028, respectively, and continues to list META as the top choice for AI internet with a target price of $775.

These figures belong to the model scope of the research report and do not equate to the company's formal guidance. The publicly available version of Morgan Stanley's materials has mentioned that global AI-related infrastructure investments could approach $3 trillion by 2028, with data center capital expenditures of about $2.9 trillion. The $1.4 trillion figure for the five platforms comes more from sell-side estimates that split the major cloud and internet platforms.

The most newsworthy change in this research report is that AI infrastructure spending continues to be raised. By 2028, the available computing capacity for major platforms in the model approaches 120GW, which is about four times the 30GW of 2025. The cost per GW for construction is also increased, as the new generation platforms like GB200, GB300, and Vera Rubin require more memory, electricity, racks, and engineering investment.

For investors, the issue has shifted from "Will AI giants spend money?" to "How long will it take for this money to turn into revenue?". META is placed in a priority position because it is facing higher AI capital expenditure pressures while having more direct monetization entry points through advertising, consumer applications, model APIs, and subscription tools.

$1.4 trillion expenditure depends on 120GW computing power

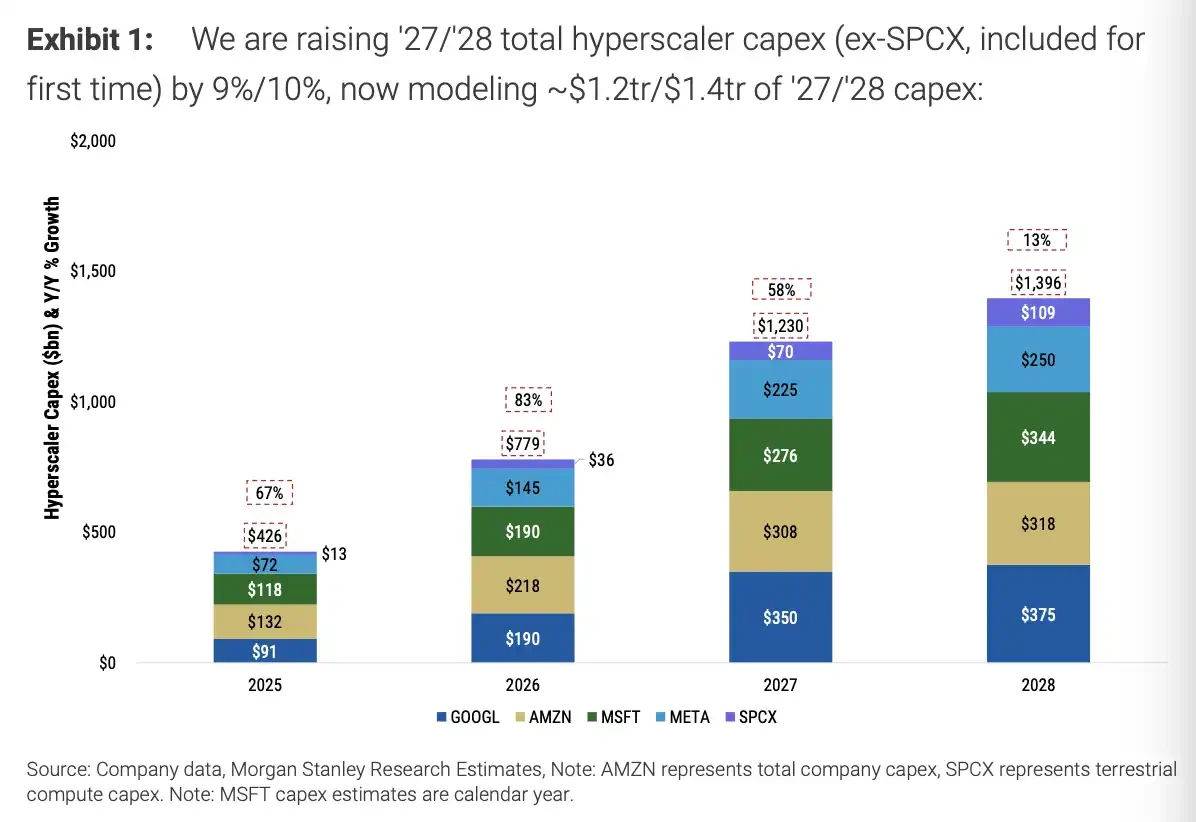

The report raises the expected capital expenditures of the five major cloud vendors in 2027 and 2028 by 9% and 10% respectively, to $1.2 trillion and $1.4 trillion. This figure covers AI infrastructure spending related to Amazon, Google, Microsoft, META, and SPCX.

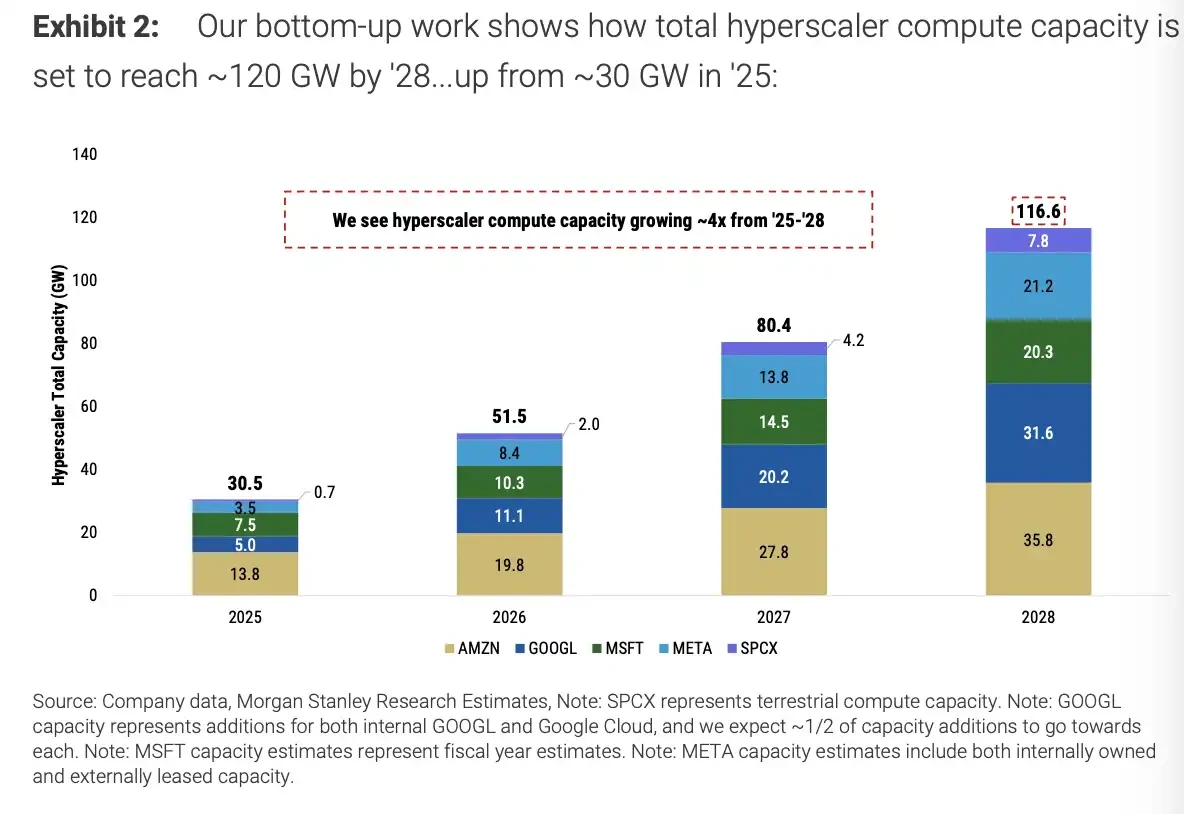

Capacity expansion is one of the main reasons for the expenditure increase. In this model, the available computing capacity of the major platforms rises from about 30GW in 2025 to nearly 120GW in 2028. Amazon's total is expected to be about 35GW by 2028, while Google is anticipated to add the most capacity in 2027 and 2028, and META is projected to increase from approximately 3.5GW at the end of 2025 to 14GW in 2027 and 21GW in 2028.

Capital expenditure forecasts for the five major cloud vendors, totaling $1.4 trillion in 2028, raised by 9% and 10% for 2027 and 2028.

Available computing capacity increasing from about 30GW in 2025 to nearly 120GW in 2028, with META increasing to 21GW and Amazon's total at about 35GW.

The capital expenditure estimation for META needs to retain a distinction. In the report's model, META's capital expenditures for 2027 and 2028 are estimated at $225 billion and $250 billion respectively. Some publicly available secondary reports mention Morgan Stanley's figure for META at around $380 billion for 2027 to 2028, which may involve different scopes including total capital expenditures, AI infrastructure, or off-balance financing.

This type of difference will not change the main narrative: AI data center expenditures continue to pressure free cash flow, depreciation, and short-term EPS, which will determine whether future revenues from cloud, advertising, search, APIs, and enterprise tools can be realized. Those who can convert more computing power into billable products will find it easier to justify today’s capital expenditure.

Cost per GW has risen, memory and electricity elevated the threshold

The increase in expenditure is not only due to "building more data centers," but also due to "each GW being more expensive."

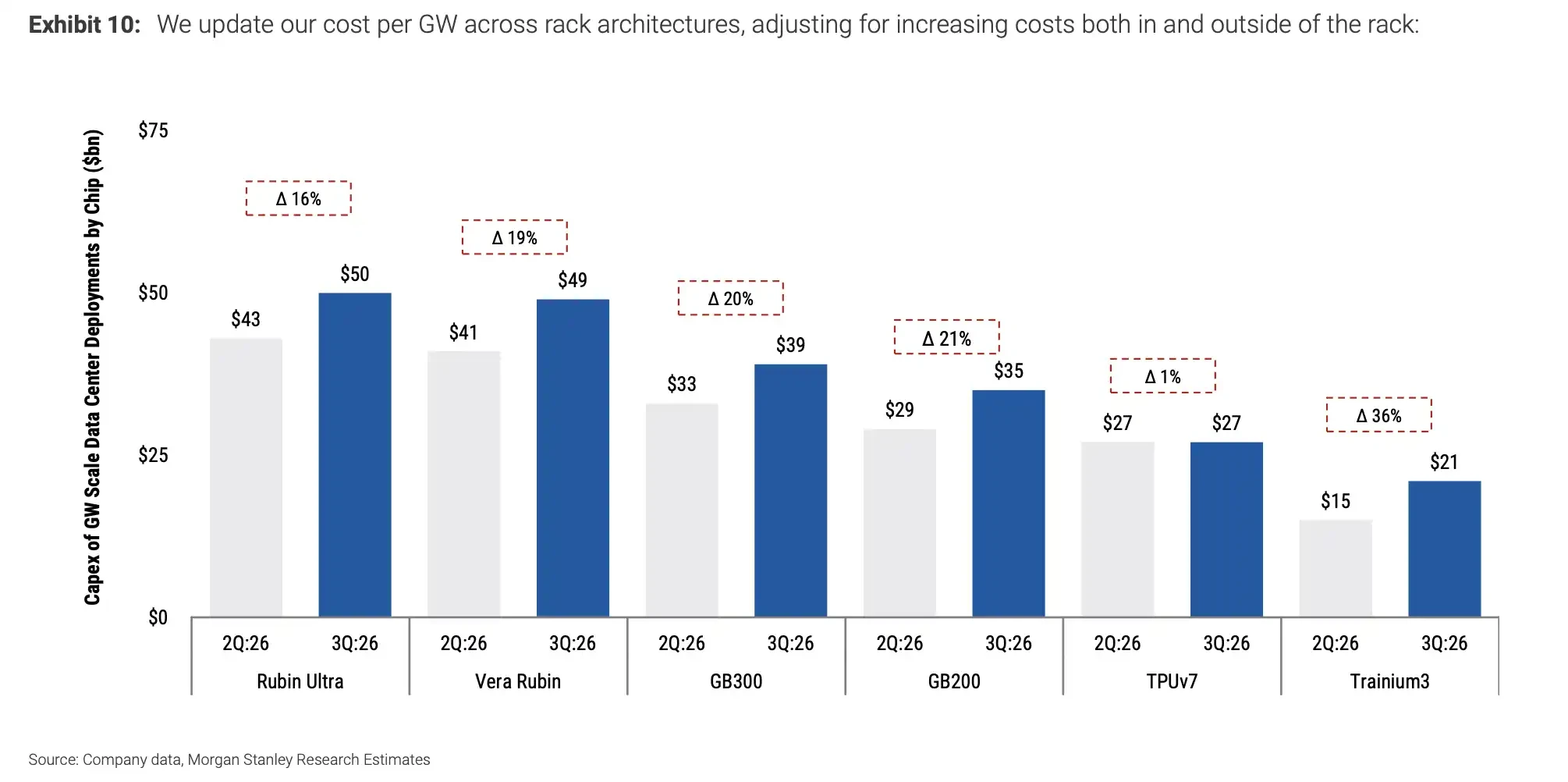

In the bottom-up cost model of the report, the construction cost for GB200 per GW is about $35 billion, up 16% from previous assumptions. GB300 is about $39 billion, an increase of 19%. Vera Rubin is about $49 billion, up 20%. Google TPU v7 is about $27 billion, and Amazon Trainium3 is about $21 billion.

Updated deployment costs for GPU and ASIC GW level data centers, with GB200 at about $35 billion, GB300 at about $39 billion, and Vera Rubin at about $49 billion.

The cost pressures mainly come from two aspects. The proportion of memory in high-end AI systems continues to rise, and the costs of electricity, land, cooling, power distribution, and construction are also increasing. The report assumes that related costs will rise from approximately $10 million/MW to around $11 million to $19 million/MW.

This is also the reason why it is difficult for AI giants to reduce expenditure in the short term. Improved chip supply can relieve some pressure, but access to electricity, racks, construction, skilled labor, and local approvals will still prolong construction cycles. Some project timelines may extend to about three years; the larger the capital expenditure, the faster the revenue side needs to prove returns.

META's focus shifts to how AI is monetized

META is listed as the top choice, primarily because its AI revenue options are more concentrated than most internet companies.

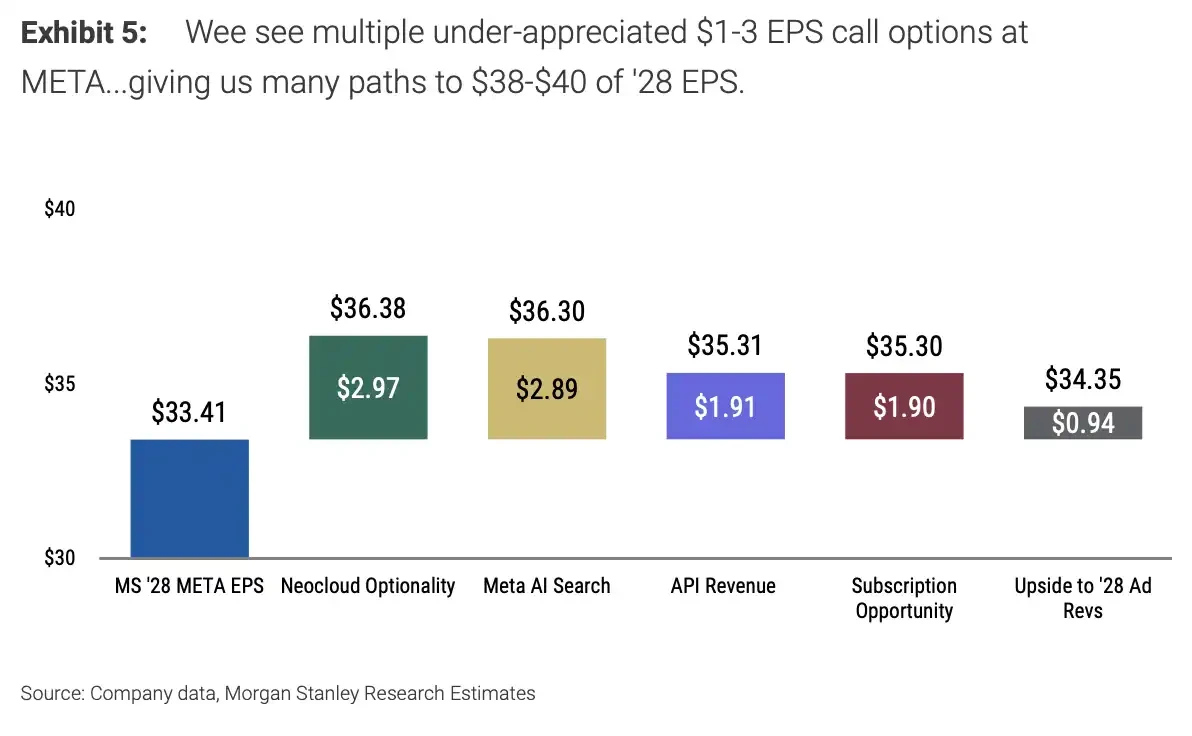

The report breaks down META's potential upsides into avenues like Meta AI search, new cloud services, API revenue, subscription tools, and advertising upgrades, which could contribute about $10 to EPS in 2028. In the base scenario, META's EPS for 2028 is $33.41. If some options materialize, EPS has further upside potential.

Cumulative contributions of five categories of AI upside options for META to EPS in 2028, with baseline EPS of $33.41, contributing a total upside of about $10.

This estimation does not entirely align with some publicly available secondary reports referring to "four products or catalysts" and "EPS upside of $1 to $3 in 2028," but it is more appropriate to consider it as the scenario estimate from this report. The portion that can truly impact financial statements depends on product adoption rates, charging capabilities, and computing power utilization rates.

API is the most straightforward entry point. Meta announced the public preview of the Meta Model API on July 9. Price tracking entities like Artificial Analysis and other third-party information indicate that the input and output prices for the Muse Spark 1.1 API are $1.25 and $4.25 per million tokens, respectively, lower than some leading competitors.

The report's model further assumes that every 100MW of GB300 capacity used for APIs corresponds to approximately 53,300 GPUs at 75% utilization, which could generate about $8.59 billion in revenue, $640 million in incremental EBIT, and about $1.91 in 2028 EPS increment. This estimation relies on high utilization and sustained demand; low pricing alone can only assist in acquiring customers but cannot guarantee profitability on its own.

Subscription tools are also a potential entry point. The model assumes that 25% of the 15 million advertisers of META pay about $200 monthly for tools like business agents and coding assistants, which could contribute about $8 billion in revenue and about $2 in 2028 EPS. Whether advertisers are willing to continue paying depends on whether these tools can offer higher conversion rates, lower production costs, or stronger automation capabilities.

Amazon and Google benefit, revenue verification still needs to catch up

Amazon and Google are also important subjects in this round of capital expenditure increase, but they are more like background references in this narrative.

Regarding Amazon, the report raises AWS revenue growth outlook, expecting growth rates of 40% and 36% in 2027 and 2028 respectively. It also estimates that AWS backlog increased by about $110 billion quarter-over-quarter in Q2 to about $475 billion. Since Amazon has not yet released its official Q2 financial report, this backlog figure should be viewed as a sell-side forecast metric. What is confirmed in official documents is that AWS's sales grew 28% year-on-year in Q1 2026, with OpenAI adding a $100 billion multi-year commitment, and cash capital expenditures continuing to rise.

Google's advantage lies in its Gemini model, TPU, and full-stack cloud capabilities. The report shows that Google is expected to add the most capacity among major platforms in 2027 and 2028. The short-term pressure lies in that computing resources may still constrain product volume, especially when search, cloud services, and model APIs compete for computing power simultaneously.

These clues point to a concrete reality: AI expenditures have entered the trillion-dollar level, and the market will increasingly directly ask “How much revenue does every dollar of capital expenditure bring?” Cloud services, AI search, APIs, advertising tools, and enterprise subscriptions will all become entry points for validating expenditure returns.

Massive expenditures must navigate power, approvals, and real demand

This round of capital expenditure increases has clear boundaries.

The first constraint is supply. Chips, HBM memory, racks, power access, and skilled labor will all affect the speed of construction. AI data centers must also navigate local approvals, grid upgrades, and construction cycles from planning to production, and cannot land linearly according to model assumptions.

The second constraint is political and regulatory. Large data centers occupying electricity, water resources, and land may provoke local resistance. Energy policies and the rhythm of local approvals may also change around the 2026 midterm elections in the United States and the presidential election in November 2028.

The third constraint is demand. META's API, subscriptions, and advertising upgrades are still in the upward scenario, and revenue realization requires actual customer payments and sustained usage. Pricing lower than competitors may help acquire customers, but long-term profitability will depend on usage volume, gross margin, and tool ROI.

$1.4 trillion in capital expenditure depicts a high-cost growth curve. Giants are locking in AI computing power in advance, and the market will continue to question when this computing power will turn into revenue and profit. META's target price of $775 is based on the gradual realization of AI monetization, and the hardest step is to convert the EPS upward in the model into cash flow in the financial statements.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。