Introduction

Since 2026, on-chain trading in TradFi has seen a significant surge: CEX platforms are collectively entering the market, issuers on-chain are accelerating the migration of US stocks, ETFs, and private equity exposure onto the chain, while traditional brokers, custodians, clearing systems, and financial infrastructure providers are also assessing market opportunities in security tokenization. According to RWA.xyz data, as of July 9, 2026, the distribution scale of tokenized stocks is approximately $2.16 billion. Stock tokens are no longer just niche RWA experiments; they have entered a new phase where CEX platforms, on-chain platforms, RWA issuers, and traditional financial institutions compete for market share.

Source: https://app.rwa.xyz/stocks

However, as the market heats up, a more critical question may be overlooked: What are users actually buying? Just because NVDA, TSLA, MSFT, or SpaceX is displayed on the trading interface does not mean that users become shareholders of Nvidia, Tesla, Microsoft, or SpaceX directly. Stock perpetual contracts may only represent a price index; stock spot tokens may be on-chain mirror certificates packaged around underlying securities held by the issuer; Pre-IPO tokens might correspond to SPV, private equity shares, income rights, or synthetic exposure. In other words, on-chain stock trading makes "buying US stocks" seem simpler and more open, but it also complicates the chain of rights between users and actual stocks, making it longer and more complex.

1. What Are You Buying: On-Chain Stocks Are Not Real Stocks

The most misleading aspect of on-chain stock trading lies in the fact that different products may use stock names, stock codes, or price trends resembling stocks on the front-end interface, yet they differ legally in structure, asset backing, trading mechanisms, and user rights. What users are actually buying may not be the stocks themselves but rather economic exposure to stocks packaged by issuers, on-chain contracts, exchange accounts, index prices, market maker liquidity, and redemption terms.

1.1 Stock Spot: Underlying Stocks Exist, But No Shareholder Rights

Stock token spot is currently the easiest type of product for ordinary users to understand. Users see tokens corresponding to specific stocks, such as AAPLX, TSLAON, MSFTB, etc., in CEX or on-chain wallets, and then purchase them using USDT, USDC, or other stablecoins. Due to the front-end experience resembling spot trading, users easily interpret it as "buying US stocks on-chain." However, what users are typically buying is not the underlying publicly traded company stocks themselves but tokenized assets designed around underlying securities or related rights by issuers like xStocks or Ondo.

Compared to traditional stock markets, stock token spots often emphasize longer trading hours on-chain or within the platform and lower participation thresholds. However, the biggest difference between stock token spots and traditional stocks does not lie in the front-end trading experience, but in the underlying product structure and rights arrangements. Whether users enjoy shareholder rights, can redeem underlying assets, how the underlying assets are held, and which parties bear specific risks depend on the issuer's product terms, platform rules, and risk disclosures. In other words, it offers a gateway for trading that closely resembles stock price performance, but it cannot simply be equated with direct stock ownership, nor can it be assumed that all rights corresponding to traditional stocks are automatically granted.

1.2 Stock Contracts: No Underlying Stocks, Only Trading Prices

The "stock attributes" of a stock perpetual contract mainly manifest in price anchoring, not asset ownership. The NVDA, TSLA, AAPL users see on the trading page are more the contract targets or price reference sources and do not indicate that the platform has delivered the corresponding stocks to the users. In fact, what users buy or sell is neither stocks nor stock tokens but rather perpetual contract positions established around the price performance of a specific stock.

The core value of stock perpetual contracts lies in providing exposure to stock prices, not ownership of stocks. Regardless of whether the price references underlying stocks, stock tokens, or related indices, what users obtain is leveraged trading capability on price fluctuations, rather than shareholder rights. Therefore, it enables 24/7 trading, supports dual positions, and allows leveraged trading, but also comes with derivative risks like funding rates, forced liquidation, margin, and price deviations. Essentially, it trades prices, not the stocks themselves.

1.3 Pre-IPO Tokens: What You Might Buy Is Equity Exposure or Event Expectations

Pre-IPO products are among the most easily exaggerated on-chain stock products by marketing language. Before SpaceX went public in June of this year, Pre-IPO products related to it sparked widespread market attention, with many platforms launching relevant traded targets. This has also led more investors to begin focusing on this new track of "tokenization of private company equity." Given the market's generally high expectations for the IPO potential and growth of hot unicorns, users easily interpret these products as "buying shares in unlisted companies in advance."

However, unlike listed stock tokens, Pre-IPO products do not usually mean that users directly hold equity in unlisted companies. What users obtain may be rights arrangements corresponding to private equity, special purpose vehicle (SPV) shares, income rights, debt certificates, or only synthetic exposure tracking changes in company valuation. As unlisted companies do not have public trading markets, the rights arrangements, liquidity, and exit mechanisms of related products tend to be more complex. Therefore, the core value of Pre-IPO is to provide investment exposure to the growth expectations of unlisted companies and cannot simply be understood as "becoming a shareholder in the company ahead of time."

2. What Are the Intermediaries: The Chain from Real Stocks to User Accounts

Whether it is stock spot, stock contracts, or Pre-IPO products, they do not come directly from stock exchanges to user accounts, but rather pass through a chain of rights composed of traditional financial infrastructure and on-chain issuance systems. What truly determines what users buy is not the trading page, but each participant in this chain.

2.1 Underlying Asset Layer: What Securities Are Anchored

The starting point of the entire chain is not the tokens but the underlying assets. Although different platforms sell "stock products," the underlying assets corresponding to different products can vary entirely, which is the first step in determining product structure and the subsequent chain.

For stock spot products like xStocks, Ondo Stocks, and Binance bStocks, the underlying assets usually correspond to publicly traded securities like US-listed stocks, ETFs, ADRs, etc. For example, xStocks has covered over 160 stocks and ETFs and emphasizes that the relevant tokens are supported by corresponding underlying securities. In contrast, for stock contracts, the targets usually correspond to a particular stock or stock price index, essentially a financial derivative that does not require actual stocks to enter the trading chain, nor is there any actual delivery of the underlying stock. As for Pre-IPO products, their underlying assets may further extend to private equity, SPV-held rights, income rights, or other financial arrangements built around unlisted companies.

Stocks are merely the names visible to users, while what truly determines the product characteristics, risk boundaries, and rights arrangements are the underlying assets intended. The underlying assets not only determine whether users ultimately receive shareholder rights, economic exposure, or other financial rights but also dictate what type of brokers, custodians, issuers, and clearing systems will be involved later on.

2.2 Infrastructure Layer: Who Holds and Clears

Between the underlying assets and on-chain tokens, the most important yet often overlooked layer is the traditional financial infrastructure. Real stocks do not automatically enter the blockchain simply because tokens are issued; instead, transactions, holdings, settlements, and asset custodianship need to go through brokers, custodians, securities depository systems, and clearing networks. In other words, on-chain stocks do not bypass the traditional financial system but add a layer of on-chain issuance and trading structure on top of it.

In this layer, different institutions have different responsibilities. Brokers connect to the securities market and execute trades, custodians are responsible for safely holding underlying assets, and securities depository and clearing institutions handle securities registration, delivery, and clearing, while legal entities (such as SPVs and trusts) are responsible for asset isolation and rights arrangements. Among them, Alpaca is currently one of the more representative securities infrastructure providers in the stock token ecosystem. Its securities brokerage services are provided by Alpaca Clearing and rely on traditional securities infrastructures like FINRA, SIPC, DTCC, FICC, and OCC for securities custody, clearing, and settlement. Similarly, US securities infrastructure service providers like DriveWealth and Apex Clearing also provide brokerage, custody, and clearing capabilities to several global brokers and fintech platforms, but they do not directly issue stock tokens; rather, they exist as essential infrastructure linking traditional securities markets.

For ordinary users, these institutions are far less familiar than exchanges or token issuers, but together they determine whether the underlying assets actually exist, whether independent custody is achieved, how securities are delivered, and whether risk isolation can be implemented under extreme circumstances. They do not directly determine what rights users have but provide a reliable underlying infrastructure for the entire stock token system and are indispensable links connecting traditional securities markets with the on-chain world.

2.3 Token Issuance Layer: Who Defines User Rights

If brokers, custodians, and clearing systems are responsible for connecting to the real securities market, then token issuers are responsible for repackaging the underlying assets into on-chain products. They not only determine how tokens are issued but also what rights the user ultimately receives, what risks are borne, and under which legal frameworks and regulatory requirements the related products apply. In other words, the same stock can lead to entirely different on-chain products depending on the issuer.

Currently, different platforms have adopted different issuance paths. xStocks is issued by Backed Assets (JE) Limited, its public disclosures emphasize that the product is supported 1:1 by corresponding underlying assets and held by regulated custodians; at the same time, the product terms also make it clear that holders typically do not enjoy traditional shareholder rights, such as voting rights, and that corporate actions like dividends are handled according to product rules. Ondo Stocks is issued by Ondo Global Markets (BVI) Limited, adopting a model closer to securities-type RWA issuance and setting corresponding investor access requirements based on different jurisdictions. Binance bStocks are issued by BTech Holdings Limited based on relevant issuance documents and product terms; Bitget’s rStocks and some Pre-IPO products partner with Reality, where the issuer is responsible for product issuance and underlying rights arrangements while the exchange handles product distribution and user transactions.

From this, it can be seen that the legal attributes of stock tokens are not determined by the exchanges but by the issuer's legal structure, issuing entity, product terms, and risk disclosures. Even if different platforms offer tokens corresponding to the same stock, the issuing entities, underlying rights, redemption mechanisms, investor rights, and regulatory arrangements may vary significantly.

2.4 Distribution and Trading Layer: How to Bring Stock Products to Users

After issuance, stock tokens truly enter the trading environment familiar to ordinary users. For most users, what they encounter is not brokers, custodians, or issuers but CEX trading platforms like Binance, Hotcoin, or decentralized exchanges like Hyperliquid. From searching for stock codes, checking prices, placing trades to managing positions, what users see is almost indistinguishable from traditional stock trading—but the platform displays only the final link of the entire chain.

Take Hotcoin as an example; the platform acts as the distribution and trading access role for stock products, rather than being the holder of underlying assets or the token issuer. Whether it’s stock spot, stock contracts, or Pre-IPO products, Hotcoin serves more as a terminal access to connect users with the whole stock token chain: on one hand, it lowers the user participation threshold through a unified trading interface, allowing users to trade stock products as if trading crypto assets; on the other hand, the platform connects to the corresponding issuance systems and trading liquidity for different products, providing trading, settlement, and asset management services while not directly deciding the legal structure behind the products and investor rights.

Therefore, while users are indeed facing a trading platform, the trading platform is not the starting point of the stock token system but the endpoint of the entire chain. Trading platforms are gradually evolving from crypto asset trading markets into common distribution channels for stock tokens, RWAs, and traditional securities, but what truly defines product characteristics and investor rights is the entire underlying issuance chain behind it.

It should be noted that the above chain primarily applies to stock spot products. In the case of stock perpetual contracts, the operation logic is different. Because stock contracts are essentially financial derivatives and do not involve the actual holding of underlying stocks, they typically do not require a complete chain involving brokers, securities custody, issuers, and other entities, but are instead built around a price discovery mechanism. Platforms usually acquire underlying stock prices through oracles or price indices and use perpetual contract trading engines to accomplish matching, margin management, and risk control. In other words, stock spot connects to "real stocks," while stock contracts connect to "the prices of real stocks."

3. On-Chain Stock Ecosystem: Different Platforms' Development Paths

Having understood the complete chain from underlying assets to user accounts for stock tokens, a more concerning question arises: why do different platforms choose entirely different development paths while engaging in “on-chain stocks”?

The answer lies in their different interpretations of “who leads the entire product system.” Some platforms choose to have exchanges centrally control issuance, trading, and user access; other platforms open the issuance network to share among multiple trading platforms; while still others focus competition on trading capabilities themselves instead of the issuance system. These different control methods have formed three distinctly different development routes in the stock token market.

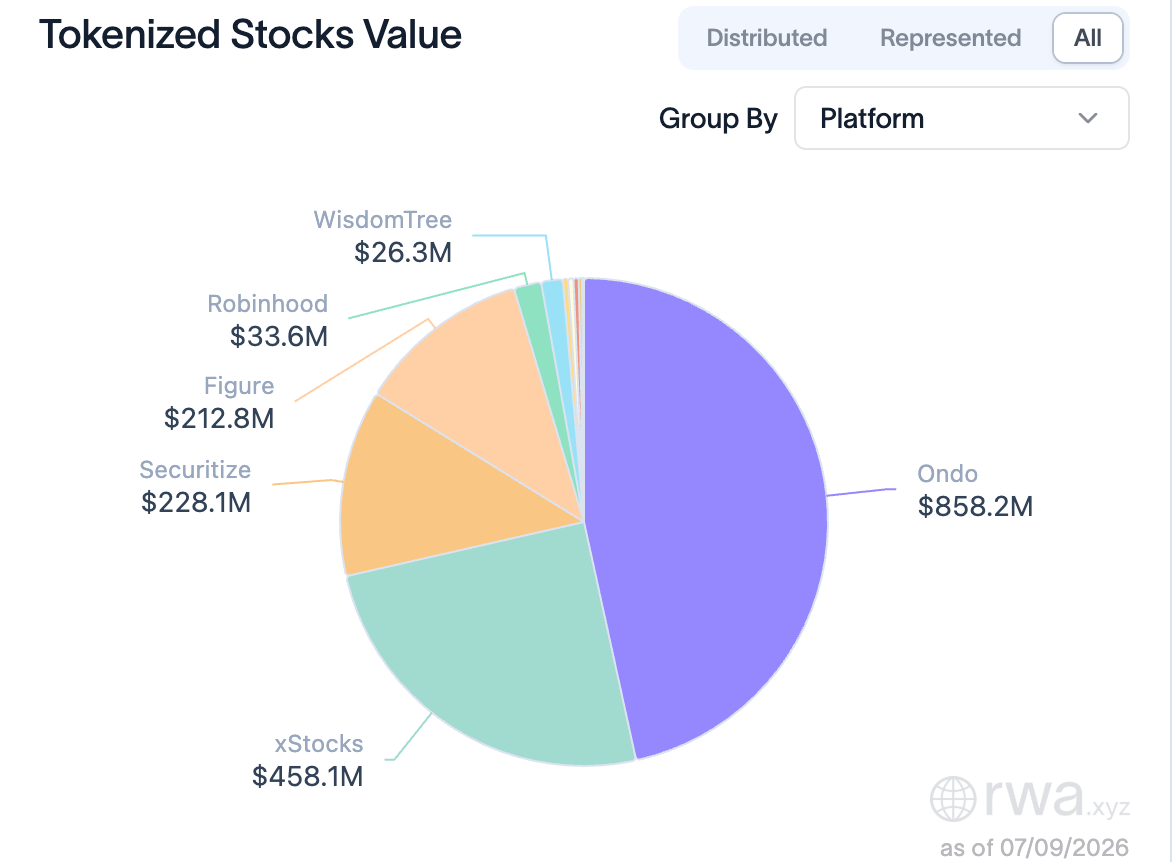

According to RWA.xyz data, as of July 9, 2026, based on total value statistics, Ondo accounts for approximately 46% of the market, xStocks about 25%, Securitize about 12%, Figure around 11%, and Robinhood about 2%. Leading issuance systems have already captured over 90% market share, and industry competition is transitioning from "who can launch stock tokens first" to "who can master the issuance network, trading access, and liquidity."

Source: https://app.rwa.xyz/stocks

3.1 Issuance Network Dominated

xStocks and Ondo represent the development path dominated by issuance networks, with the representational path being: Issuance Network → Multi-Platform Distribution → On-Chain Financial Eco-system.

Whether it is xStocks or Ondo, they place emphasis on the issuance systems themselves, rather than on trading access. For example, xStocks' tokens are issued by Backed Assets (JE) Limited, and the same set of stock tokens can be accessed across multiple platforms like Jupiter, Kraken, Bybit, and Kamino; Ondo Stocks, issued by Ondo Global Markets (BVI) Limited and others, places greater emphasis on traditional securities issuance frameworks and institutional investor access. While both serve different clientele, they essentially build ecosystems around the “issuance network” rather than relying on a single trading platform.

The greatest advantage of this model is that stock tokens can break through the limitations of a single platform, circulate between various trading platforms and on-chain protocols, and further participate in lending, staking, liquidity management, and other on-chain financial applications. The platforms may change continuously, but the issuance network remains unified, which is one of the most scalable ecosystem models currently in the stock token market.

3.2 Exchange Dominated

Binance, Bitget, Hotcoin, etc., represent the exchange-dominated path, with a representative path being: Exchange Dominated Issuance System → Platform Distribution → User Trading.

In this model, exchanges are not only responsible for trading access but are also deeply involved in product design and the construction of the issuance system. For instance, bStocks are issued by BTech Holdings Limited, associated with Binance, which is responsible for product distribution, transaction matching, and user operation, and Hotcoin has also launched a large number of bStocks. For ordinary users, stock products are almost entirely presented under the exchange's brand.

The greatest characteristic of this model is the formation of a unified closed loop in issuance, trading, liquidity, and user operation. Exchanges can quickly launch products, standardize the user experience, and increasingly expand market size through platform traffic. However, at the same time, the tight binding of product design, issuance entities, and platforms also means that exchanges have to bear more product management and compliance responsibilities.

3.3 Traditional Finance Dominated

In contrast to the first two models, the traditional finance dominated path does not center around a crypto-native issuance network or exchanges but retains mature systems for securities issuance, registration, custody, and oversight, progressively introducing securities assets like stocks into the blockchain, with the representative path being: Traditional Securities System → Digital Securities Issuance → On-Chain Trading and Distribution.

Currently, institutions represented by Robinhood, Securitize, Figure, and Dinari are promoting development in this direction. For example, Robinhood has launched stock token products backed by its established securities brokerage system; Securitize has long been focusing on compliant securities token issuance and collaborating with traditional financial institutions like BlackRock and Apollo to promote the chainup of securities assets; Figure has built issuance, trading, and clearing systems around digital securities; and Dinari’s dShares have been successively integrated with on-chain trading infrastructures like Hyperliquid HyperCore, providing new distribution channels for stock tokens.

Compared to crypto-native ecosystems, this path emphasizes securities regulatory frameworks, investor protection, and institutional access, with product designs closer to traditional capital markets. Although the pace of development is relatively slower, as more traditional financial institutions begin to engage in securities tokenization, this path is expected to attract more institutional funds and traditional investors into the on-chain stock market.

4. Risk Contradiction: Shorter Entry vs. Longer Rights Chain

What stock tokens truly change is not the stock itself but rather the way investors access stocks. Users no longer need to open traditional US stock accounts, handle cross-border broker processes, or wait for US trading hours; they can gain exposure to stock prices through stablecoins, CEX platforms, or on-chain wallets. However, on-chain stock trading has not eliminated intermediaries. Rather, it has restructured traditional securities markets' brokers, custodians, clearings, issuers, market makers, and trading platforms into a new chain. User operations have become simpler, but asset relationships are more complex; front-end access is shorter, but the chain of rights is longer.

4.1 Trading Convenience vs. Ownership Weakening

In traditional stock accounts, users can at least clearly know whether they are purchasing stocks, funds, or ETF shares. In stock token products, however, what users buy may only be issuer certificates, economic exposure, or index contracts. xStocks holders have no ownership rights to underlying stocks, voting rights, distribution rights, or legal claims to remaining assets upon liquidation of the underlying company, and bStocks also do not grant holders direct ownership of the underlying publicly traded company stocks.

This indicates that the convenience of stock tokens often comes at the cost of weakened ownership. Users have a more convenient trading entry but may lose traditional shareholder rights. For trading users who only focus on price fluctuations, this may be acceptable; but for users aiming at long-term holdings, shareholder rights, dividends, voting rights, or corporate governance, this difference is crucial.

4.2 On-Chain Transparency vs. Off-Chain Asset Opacity

One major selling point of stock tokens is their on-chain transparency. Users can view contract addresses, transaction records, holder counts, and on-chain circulation statuses. However, on-chain transparency does not equal full transparency of the underlying assets.

On-chain contracts can only prove that a certain token exists on a specific chain, what transfers have occurred, and which addresses currently hold it. They cannot automatically verify how many underlying stocks are genuinely held within the issuer’s holdings, whether the custody arrangements are independent, whether broker accounts are pledged or indebted, nor can they prove the priority of repayment rights users will have in case the issuer goes bankrupt. Even if the issuer provides reserve proofs, they only reflect the asset status at a specific point in time and cannot substitute for ongoing audits, independent custody, and legal assurances.

Therefore, what stock tokens truly require is "dual transparency": firstly, on-chain contract transparency, and secondly, off-chain asset transparency. The former is provided by the blockchain, while the latter relies on audits, custody proofs, reserve proofs, legal opinions, prospectuses, risk disclosures, and regulatory documents. Only when both exist can stock tokens potentially upgrade from "price tracking tools" to more reliable asset distribution infrastructures.

4.3 Liquidity Expansion vs. Redemption Constraints

Another advantage of stock tokens is liquidity expansion. Users can trade on crypto exchanges or on-chain platforms 24/7, even continuing to buy and sell during traditional US stock market closures. However, trading liquidity does not equate to exit liquidity. Users can sell tokens on the platform, but this does not imply that they can redeem tokens for real stocks at any time. Even if some products support redemption, it may be subject to user qualifications, geographic restrictions, minimum amounts, fees, market trading hours, brokerage settlement cycles, compliance checks, and issuer rules.

This is also a crucial difference between stock tokens and stablecoins. Stablecoin users typically focus on whether they can redeem back to USD; stock token users need to pay extra attention to whether they can redeem into underlying stocks, cash equivalents, or if they can only sell in secondary markets. If selling in the secondary market is the only option, extreme market conditions like discounts, insufficient liquidity, and market maker withdrawal will become the core risks.

4.4 Pre-IPO Narratives vs. Authenticity of Private Equity

The risks inherent in Pre-IPO products require more cautious handling. Its allure stems from scarcity: ordinary users find it hard to directly purchase shares of popular private companies like SpaceX or OpenAI, thus any product proposing similar exposure draws attention.

However, the greatest risk of Pre-IPO is not price fluctuation, but the authenticity of underlying rights. Users need to question: Does the platform genuinely hold shares of private companies? Through what entity are they held? Is it an SPV? Does that SPV have legitimate transfer rights? Do private companies permit such transfers? Are users holding equity, income rights, debt certificates, or synthetic exposure? If an IPO does not occur in the future, how will the product be priced? If the issuer defaults, who do users turn to for redress?

Listed stock tokens at least have a public market price for reference, while Pre-IPO products often lack transparent secondary markets, standardized valuations, and continuous liquidity. Therefore, it is more likely to shift from "equity investment" to "event trading" or "valuation expectation trading." This does not mean that Pre-IPO products lack value, but they should definitely not be simplistically packaged as "buying unlisted stocks in advance."

5. Outlook and Conclusion

Stock tokenization is still in its early stages, but the industry's direction is becoming increasingly clear. In the future, the focal point of competition will not be who lists more stocks but rather who can establish more credible underlying assets, more comprehensive issuance systems, more transparent custody mechanisms, and more efficient trading networks. Exchanges, issuance networks, and traditional financial institutions will coexist in the long term, serving different types of investors.

However, regardless of how the industry develops, one fact will not change: stocks on-chain do not mean stocks have departed from the traditional financial system. The issuance, registration, custody, clearing, and investor rights of stocks still rely on traditional securities laws and financial infrastructure; what is genuinely changing is the way users acquire these assets. From local brokers to global trading platforms, from fiat accounts to stablecoin wallets, from fixed trading times to 24/7 on-chain trading, the assets themselves have not changed—the distribution network has.

Therefore, the future of stock tokenization does not lie in disintermediation but in the reorganization of intermediaries. Brokers, custodians, clearing systems, issuers, on-chain protocols, and trading platforms have not disappeared; rather, they have been reorganized in the blockchain era, forming a new asset circulation chain. What is truly worth competing over is no longer who gets stocks on-chain first, but who can establish a sufficiently credible, transparent, and open on-chain stock ecosystem.

About Us

Hotcoin Research, as the core research institution of Hotcoin Exchange, is dedicated to transforming professional analysis into your practical tool. Through our "Weekly Insights" and "In-Depth Reports," we analyze market dynamics for you; utilizing our exclusive column "Hotcoins Selected" (AI + expert dual screening), we identify potential assets to reduce trial and error costs. Each week, our researchers also engage with you live via live streams, interpreting hot topics and predicting trends. We believe that warm companionship and professional guidance can help more investors traverse cycles and seize the value opportunities in Web3.

Risk Warning

The cryptocurrency market is subject to high volatility, and investments carry risks. We strongly recommend that investors thoroughly understand these risks and invest under a strict risk management framework to ensure the safety of funds.

Website: https://www.hotcoin.com/zh_CN/learn/index/

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。