Original author: David, Trend Research

In recent days, the positive news for storage has been coming one after another.

On June 29, South Korea launched a semiconductor super plan totaling over 1,000 trillion won (approximately 650 billion USD), with the official goal of doubling DRAM production capacity in five years;

At the same time, China's DRAM leader Changxin Technology has passed the approval process, and the market expects it to be listed from mid-July to early August, with institutional valuations reaching 2 trillion to 4 trillion yuan; combined with the judgment that major storage manufacturers will be out of stock until 2028, the reasons for being optimistic about storage and semiconductors have never been this clear.

Furthermore, this sentiment has even spilled over to external networks.

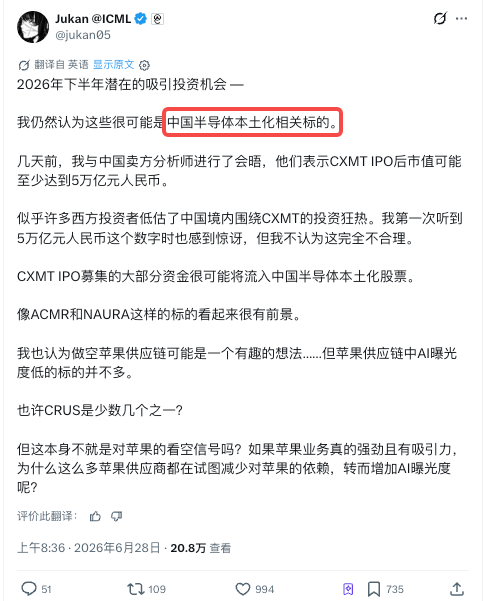

Famous tech investment blogger Jukan (@jukan05) on X posted that the most promising direction to bet on in the second half of 2026 is likely still Chinese semiconductor independence targets.

He quoted his communication with Chinese sell-side analysts, stating that Changxin Technology's market capitalization after the IPO is at least 5 trillion yuan, with most of the raised funds flowing into domestic semiconductor independence stocks. Therefore, he believes that companies like Shengmei (ACMR) and North Huachuang (NAURA) still have prospects.

Just rushing in with the wind may not always be a good timing.

Currently, nearly 30 Changxin concept stocks in A-shares have a combined market value exceeding 1.9 trillion yuan, and most leading stocks in the upstream and downstream of the industry chain are generally already close to 52-week highs, so rushing in blindly is not necessarily the optimal solution.

After a round of increases, there are not many aspects that have not yet met market expectations.

The price is rising, but the sales volume has hardly changed

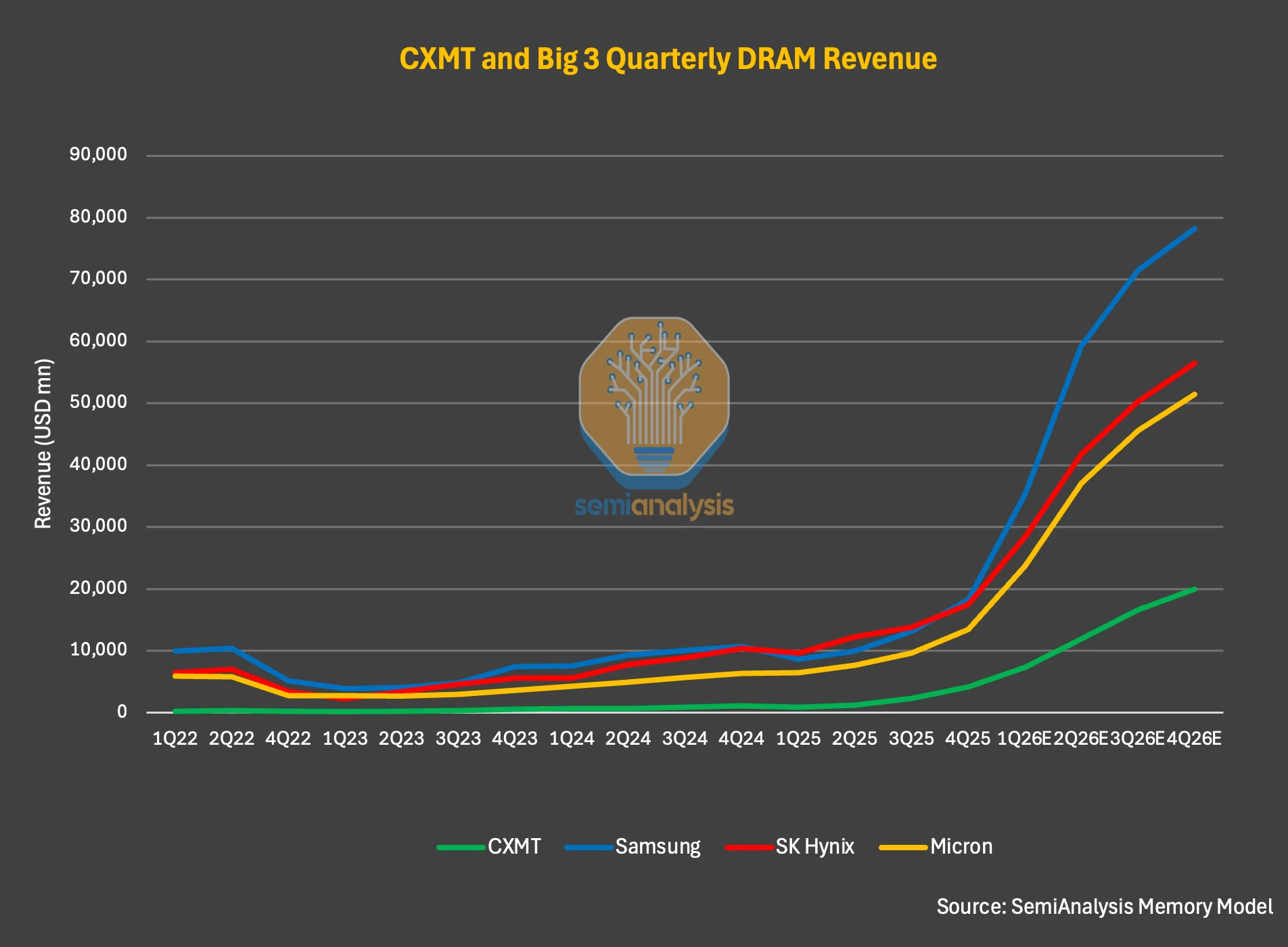

On June 23, the American semiconductor research organization SemiAnalysis released a report titled "China's CXMT Is Set to Challenge DRAM Incumbents," breaking down a set of data:

Changxin Technology's bit shipment in the first quarter of 2026 only increased by 11% quarter-on-quarter, while the average selling price (ASP) increased by about 57% quarter-on-quarter. Bit shipments measure the actual sales in terms of storage capacity, indicating "how much was sold"; ASP measures "how expensive it was sold."

The meaning of these two numbers together is that this season, Changxin hardly sold more goods; it was just selling at a higher price.

Therefore, SemiAnalysis concluded that Changxin's current profit explosion relies on the industry cycle itself, not on breakthroughs in technology or market share.

In the price market, the first to profit are the original manufacturers directly selling chips, namely Samsung, SK Hynix, Micron, and Changxin itself. Their profits have expanded linearly with ASP, and they have been among the most aggressively rising over the past year.

SK Hynix's stock price rose more than 350% this year at one point. However, at this point, the expectations along the original manufacturer chain have already been fully priced in: the expected price-to-earnings ratios for Samsung and SK Hynix are currently only between 3 to 5 times, which seems cheap, but underlying this is that the market has already factored in the AI-driven demand and profits from 2026 to 2027 into the stock prices.

The profits realized through price increases have essentially been accepted by the market. The batch of storage original manufacturers and module stocks in A-shares are the same; their price increases have been substantial, leaving little room for further pushes. As for whether the upstream production expansion chain (such as equipment and materials) has also been bought to the same position, without data to look into later, we won't draw conclusions here.

Overall, I believe Changxin is at a delicate crossroads:

On one side, selling DRAM and profiting from rising prices makes it a beneficiary of this cycle; on the other side, using the 29.5 billion yuan raised from the IPO to expand production and purchase equipment and materials makes it a spending entity.

In recent months, there has been a prevalent voice in the market, which is to directly “buy Changxin's upstream and downstream.” Looking back, this reckless gamble has indeed generated significant returns, but at the current position, if you believe that the storage and semiconductor market will continue, it is really necessary to clarify a few things.

First, the targets you are focusing on, where exactly do they stand in the industry chain, and how do they benefit;

Second, is their current price still at the foot of the mountain, or has it climbed to the halfway point or even the top?

Let’s first address the first question.

“Changxin concept stocks” is a label that has been overused. Breaking it down, the demand driven by Changxin has two paths, and the benefiting companies are not the same batch, nor is the timing of realization the same.

The first path is the expansion chain of ordinary DRAM. Currently, 99% of Changxin's shipments are ordinary DDR and LPDDR, with over 22 billion out of the 29.5 billion raised from the IPO explicitly designated for the purchase of equipment for wafer production lines and technology upgrades. This amount primarily goes to the front-end equipment, specifically the machines used to manufacture chips, making it the largest component of expansion investment; after the production lines are operational, materials will be continuously consumed.

The representative companies in the equipment sector include North Huachuang (002371), Zhongwei Company (688012), Tuojing Technology (688072), Huahai Qingke (688120), and Shengmei Shanghai (688082); the material sector includes Anji Technology (688019), Jiangfeng Electronics (300666), Yake Technology (002409), and Hu Silicon Industry (688126). This chain benefits from the money Changxin is currently spending, with the highest order certainty.

The second path is the HBM chain, which is not the same group of people as the first path. HBM is the high-bandwidth memory required for AI servers, and the technology is more complex than ordinary DRAM. Changxin's HBM is still catching up, with production lines set to operate at the end of 2026, which is one step later than the expansion of ordinary DRAM. More critically, the value of HBM does not lie in the front-end etching and deposition but in the packaging stage, which involves stacking, bonding, and encapsulating multiple chips. Therefore, the beneficiaries of HBM are another group of companies:

Testing equipment: Zhi Zhi Da (688627), packaging materials: Huahai Chengke (688535), Lianrui New Material (688300), Shanghai Xinyang (300236), along with advanced packaging and testing: Shenghe Jingwei (688820) and Tongfu Microelectronics (002156).

Upstream and downstream, is it too cold at high altitudes?

Looking at the targets of the two chains above, arranging them according to their current stock prices relative to their highest point in the past year shows a clear trace of where capital has flowed, as of the trading day on the 29th.

There is a clear boundary between the tables.

For ordinary DRAM equipment and materials, these segments are all nearly at 52-week highs, with most within 3% of the year-high. On June 29, Huahai Qingke hit the daily limit and reached a historical high; Yake Technology also refreshed its high point, with Zhongwei, Anji, and Hu Silicon all showing increases of around 10%.

This segment is the market's recognized “Changxin expansion sell shovel holder,” with the most robust logic and the highest certainty, and thus capital has been buying it most fully. In other words, the certainty of the expansion chain has already been written into the price.

Trailing behind are the packaging stages of HBM.

Lianrui New Material is about 18% away from its 52-week high, closing down against the trend on June 29; Shenghe Jingwei is similarly around 18% from its peak; Tongfu Microelectronics is about 9% away from its peak. The difference between them and equipment materials isn't because they are cheaper or ignored, but because the realization pace is slower:

Changxin's HBM production line won't go into production until the end of 2026, meaning that these companies' orders and performances will only be truly released once the production line is operational and yields are improved. Their current lower positions correspond to “it’s not their turn yet,” and simply looking to “pick up a bargain” may incur time costs and opportunity costs.

As for the overall conclusion, it is already clear.

The so-called “buy Changxin's upstream and downstream” at this position is no longer about whether to get on board; we need to see whether they are at the top of the mountain.

Just looking at prices, the ordinary DRAM side's equipment and materials are basically all at the highest point in a year, meaning cheap entry is no longer available; the HBM packaging segment is slightly lower, but the premise is that you are willing to wait.

Moreover, price only answers half of the question about "how expensive." The other half cannot be explained by price itself; it depends on whose money is buying and selling at this position.

Hot money is supporting, while some are retreating

The essence of this layer is that pricing power has shifted from long-term funds that look at fundamentals to short-term hot money driven by speculative sentiment.

On one side, industrial capital, the national big fund, and the national team are systematically reducing their positions at high levels; on the other side, speculative funds and retail investors are rushing in capitalizing on the AI theme. The former may understand this business the best and are selling; the latter want to buy low and sell high and are currently buying.

Looking first at the selling side, we have compiled a round of information from public sources:

- The actual controller of Zhaoyi Innovation, Zhu Yiming, reduced his holdings of about 6.33 million shares between May 11 and 25 (company announcement). He is also the founder and chairman of Changxin Technology, who should have the most faith in the Changxin industry chain, but he reduced his stake in his associated leading company at a high level.

- The National Integrated Circuit Big Fund has continuously reduced its holdings of Hu Silicon Industry since January, cashing out approximately 3.882 billion yuan by early June (company reducing announcement).

- Many semiconductor heavyweight stocks like Lanjie Technology, Haiguang Information, and Tuojing Technology have had shareholders reduce their holdings after stock prices soared since 2026 (announcements from various companies).

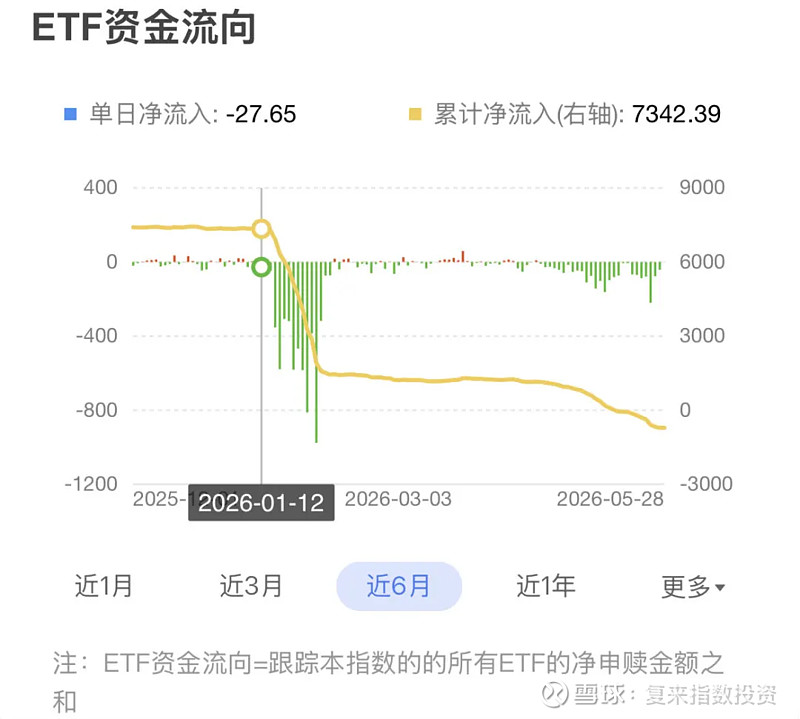

- The national team (Central Huijin) has performed high-level reductions on broad-based ETFs like the CSI 300 (according to "Caijing" calculations based on Central Huijin's holdings and fund circulation shares). It's not that it is reducing semiconductor stocks themselves, but performing a counter-cyclical exit from high positions in the entire market, and semiconductors have been the area with the largest increase and the most overdue for realization this round.

Image source: Xueqiu Index Investment Column

The motives behind these reductions cannot be generalized. Large funds have exit cycles, and reducing holdings to cash in is a routine action;the national team adjusts its broad-based holdings, possibly for counter-cyclical rebalancing rather than bearish sentiments toward a particular sector; the reasons for industrial capital and executives reducing their holdings also vary.

Interpreting them as “collectively bearish” is certainly a bit excessive, but one thing is certain:

At current price levels, these original long-term holders have coincidentally chosen to cash in a portion of their profits. Regardless of the motives, this action itself conveys the message that the current price has reached a level that makes long-term funds willing to pocket gains.

Now let's look at the buying side.

According to market data cited by Sina Finance, the main force driving this round of technology speculation is hot money:

Northbound purchases have increased by approximately 400 billion this year, while the scale of financing has swollen to about 2.8 trillion. This type of money seeks themes and momentum, and the targets being close to 52-week highs or having high PEs do not affect their entry; they are buying the rise itself.

Regulators have also detected overheating, stepping on brakes through raising financing margin ratios and suspending trading for consecutive limit-up stocks; chip-related ETFs have frequently suspended trading as on-site prices far exceed net asset values, with premiums once exceeding 30%.

When placing buyers and sellers together, the conclusion is not complicated:

At the current price level, long-term funds related to storage and semiconductors are taking profits in batches, and short-term hot money is stepping in. The marginal pricing power at this position is increasingly falling into the hands of funds driven by speculative sentiment.

Note, this does not mean the market will immediately peak. Storage shortages are expected to continue until 2028, and Changxin's production expansion is a solid prospect. However, most institutions judge that the sector will digest profit-taking through drastic fluctuations and enter a ranking competition that places more importance on performance realization, rather than experiencing a trend decline.

The author's views

Combining the two layers of judgment with the financial context above, I believe the inclination is as follows:

Short term (around Changxin's listing), sentiment still has inertia. The enthusiasm for new listings and the concept fermentation on listing day may give the sector another wave of rises, but this is the last segment driven by sentiment; the further it goes, the more it becomes a game of succession, posing a greater risk than reward for chasing highs.

Mid-term (looking at Changxin's HBM production line realization), what is truly worth waiting for is the differentiation realization between the ordinary DRAM expansion chain and the HBM chain. The order fulfillment for equipment and materials will depend on the speed of capital expenditures after Changxin's listing; meanwhile, the tickets in the HBM packaging segment that are still at lower positions will need to wait for the production line’s operational status and yield improvement in late 2026; hedging now is betting on time.

Several signals to pay attention to:

- Turning point of DRAM spot prices. The foundation of this round is price increases; once the spot prices start to decline, original manufacturers and modules benefiting from price increases will react first.

- The pace of capital expenditures after Changxin goes public. The realization of orders will largely need to look at these data; if money is spent quickly, equipment and materials can sustain high valuations.

- Whether the reductions of industrial capital and large funds expand. If smart money continues to withdraw, it is a leading signal of emotional retraction.

- Whether the premium of chip ETFs can converge. If the premium remains high, it indicates that retail hot money is still taking the baton.

Cheap entry is no longer available; what remains are conditional opportunities, and the conditions may be implicitly contained in these several signals.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。