The tokenization of real entity credit cannot avoid the challenges of offline debt collection.

Written by: Liam 'Akiba' Wright

Translated by: Saoirse, Foresight News

Key Points Overview

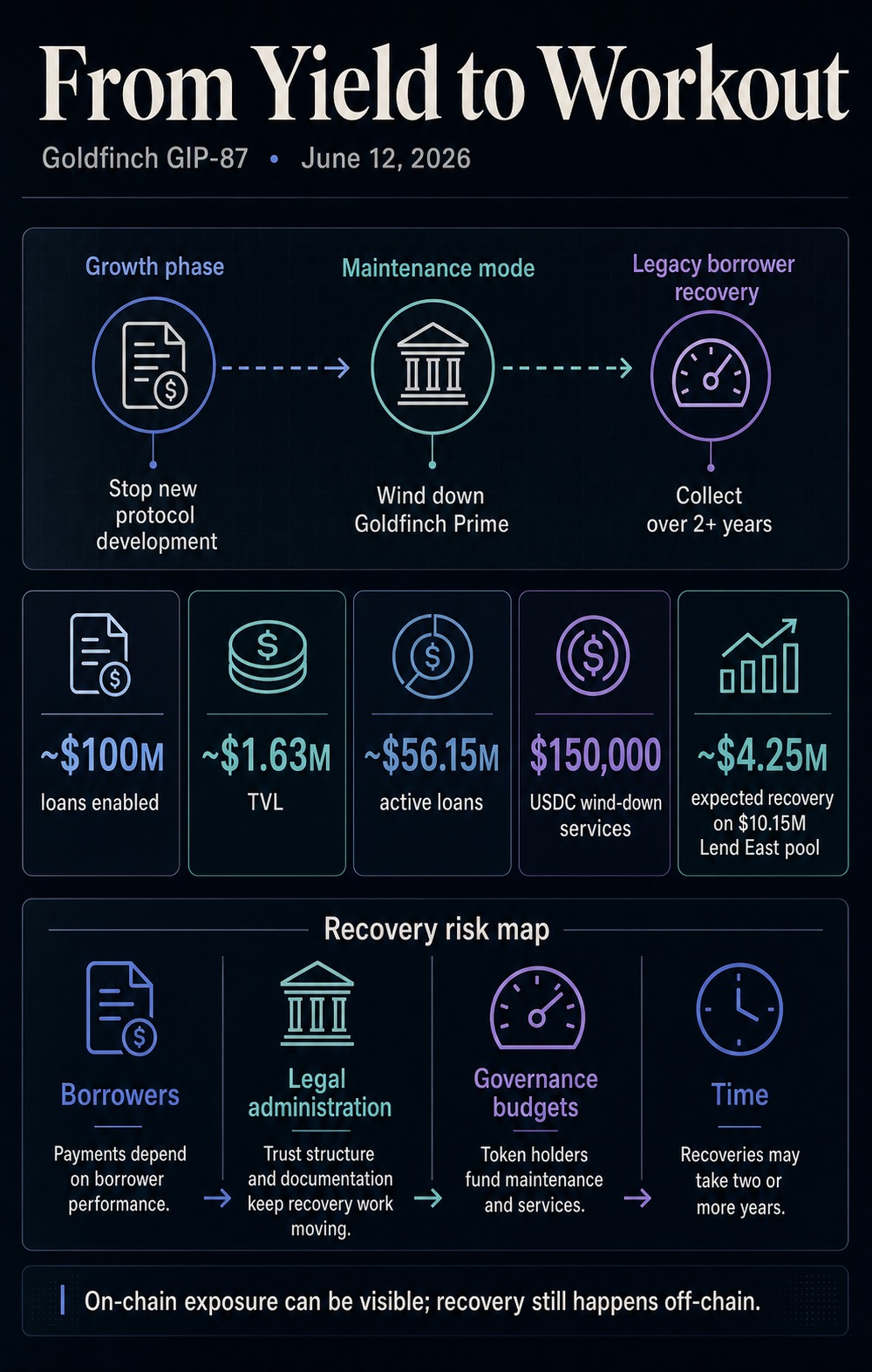

- The governance proposal GIP-87 plans to halt all new feature development, shut down the core product Goldfinch Prime, and allocate 150,000 USDC for subsequent asset collection disposal work.

- This proposal is significant: the protocol still has a large number of outstanding loans, and the current value of the platform entirely depends on subsequent repayment execution, post-loan services, and the actual repayment situation of borrowers.

- The community governance has not yet voted to approve the liquidation plan, and key issues such as trust structure, user backend access rights, and the details of non-performing asset disposal remain unresolved.

Goldfinch is a crypto lending platform that connects crypto investors' funds with offline entity borrowers. As the wave of lending expansion fades, the platform reveals the significant hidden risks in the industry: when business growth stagnates, the hardest problem to solve is collecting debts from offline borrowers.

The GIP-87 proposal released on June 12 outlines the following: to terminate all new feature development for the protocol, shut down the flagship product Goldfinch Prime, retain login access for old users, establish a domestic trust legal framework in the U.S., and pay 150,000 USDC to the development team Warbler Labs as remuneration for the full liquidation services.

As of the writing of this article, the proposal is still in the community governance review stage, and public discussions will continue until June 20. The official results on whether the vote is approved or rejected have not yet been announced. However, this sends a unified signal to the entire industry: the tokenized private credit business will transition from a growth phase of earning stable returns to a phase of debt restructuring and collection of bad debts, with outstanding loans continuing to persist.

As for Goldfinch itself, the platform's next phase of work will revolve around four major challenges: recovering debts from existing borrowers, deteriorating asset quality of multiple borrowing pools, ongoing post-loan operational costs, and the lengthy debt liquidation cycle.

The complete shift in business focus has transformed decentralized private credit from a category of investment with low thresholds and high yields into a stress test for bad debt disposal. For ordinary investors, various lending protocols, and all RWA lending platforms, the core question arises: once the lending scale stops growing, can the platform’s pre-loan risk control, default handling, and debt collection system operate normally?

From Scale Expansion to Bad Debt Disposal

The proposal document shows that the Goldfinch protocol has historically facilitated approximately 100 million USD in real loans, but several borrowing pools have serious asset quality issues. According to the plan, the protocol will enter an operational maintenance state, halting capital investment in developing new features, and concentrating all operational resources on recovering debts from historical borrowers.

The operational logic of debt collection is radically different from that of front-end lending: new lending pursues approval speed, channel coverage, and funding efficiency; debt recovery heavily relies on complete written evidence, ample time, legal recourse, continuous follow-up with borrowers, and clarification of the cost bearer of the collection. Goldfinch is now equivalent to establishing a publicly available bad debt disposal channel for a portfolio of private credit assets.

Recent publicly available data indicates that on June 23, the total value of on-chain locked assets in Goldfinch was only 1.63 million USD, but the volume of unsettled active loans on the platform far exceeds this figure. Specific data will fluctuate in real time, but the core contradiction is clear: the actual credit risk exposure borne by the protocol far exceeds the currently retained liquid funds on-chain.

Industry statistical rules generally do not include unsettled loans in the total value of locked assets, thus reflecting the same risk from two different dimensions: the total value of locked assets only reflects the current weak capital volume in DeFi protocols, while active loans represent a substantial amount of credit that still requires ongoing monitoring, maintenance, or collection.

This graphic interprets the Goldfinch GIP-87 proposal: the project will stop new feature development, shut down Goldfinch Prime, and enter an operational phase, taking over two years to recover 56.15 million USD in outstanding loans, revealing that RWA credit is only transparent on the debt side, while repayments depend entirely on offline borrowers, legal measures, governance funds, and lengthy cycles.

The lending platform data dashboard will continue to show the significant gap between the total value of locked assets and outstanding loans, with the two sets of indicators corresponding to different segments of the system. The total value of locked assets represents the idle funds currently stored within the protocol; active loans are the credit exposures requiring ongoing maintenance, restructuring, or collection. The persistent gap between the two indicates that the responsibilities and costs related to loan recovery will continue to exist long after the platform's growth phase has ended.

It is this gap that strips tokenized private credit of the facade of high liquidity DeFi products and essentially reduces it to a publicly available private credit collection service carrier.

The platform's past risk disclosure documents have already hinted at such hidden dangers: documents related to senior funding pools clearly indicate that if borrowers refuse to repay, participants will incur principal losses; if USDC reserves in the funding pool are insufficient, investors will also face liquidity restrictions due to assets not being able to be redeemed promptly.

This liquidation plan will transform the generalized product risks on paper into practical issues that community governance needs to address: how much operational funding should be allocated, who will be responsible for collection work, how old users can retain system login rights, and what legal framework will be adopted to handle overdue claims against borrowers.

Past cases in the Lend East borrowing pool have materialized these risks. A community forum announcement in April 2024 indicated that this pool, totaling 10.15 million USD, was only expected to recover 4.25 million USD at the time, meaning investors would face a significant principal gap.

This data was merely the estimated recovery amount at the time of the announcement and not the final actual disposal result, but it sufficiently demonstrates that recovering private credit bad debts is a long and complex game fraught with principal losses, multiple rounds of negotiations, and legal litigation, rather than a simple numerical balance shown on a data dashboard.

This also marks the core intersection where decentralized private credit conflicts with traditional private credit: blockchain can allow debt positions, token circulation, and protocol business activities to be clearly traceable, but whether loans can ultimately be repaid still depends on offline borrowers' willingness to perform, professional post-loan management, complete compliance documentation, and legal recovery channels after default.

Governance Mechanisms as Part of Credit Risk Control Processes

Compared to Goldfinch’s loan scale exceeding 100 million USD, the 150,000 USDC allocated to Warbler Labs for liquidation services is not particularly high, yet it brings the hidden cost of bad debt collection to the forefront. During the expansion phase of the business, community governance budgets are usually allocated to product development, user incentives, cross-chain integrations, and market expansion.

Once entering the liquidation phase, governance funding will need to be used to maintain system operations, ensure normal use of user backends, handle legal and administrative work, and cover the human costs of following up on outstanding debts.

This directly alters the core content of token holders’ voting decisions: the community is no longer voting on ecological expansion plans but is now assessing how to maintain existing credit assets after all growth capital has exited.

The proposal plans to establish a U.S. trust structure and retain login rights for old users, all pointing to the same operational phase: the platform must retain basic operational capabilities to support repayment and collection operations while cutting all new business unrelated to existing loans.

For all RWA lending platforms, this presents an unavoidable lesson: tokenized private credit platforms cannot solely prove their ability to attract borrowers; they must also build a robust borrower screening mechanism, standardized information disclosure rules, effective bad debt disposal processes, sustainable collection incentives, and a supporting governance control system.

If there are shortcomings in any of these areas, blockchain will only transparently display asset losses and will not simplify the debt recovery process.

CryptoSlate's previous reports have covered related information on the growth aspects of this space: some private credit institutions use artificial intelligence to compress paper approvals that take months into loans on the chain issued within a day; the industry is widely discussing how tokenized assets can adapt to the composability limitations of DeFi.

The Goldfinch proposal fills in the latter half of the expansion narrative that has been deliberately avoided: a fast lending business model must be accompanied by a reliable mechanism to address late repayments, overdue debts, debt disputes, and other issues.

This stark contrast also highlights the research value of the Goldfinch case. This governance proposal fully demonstrates the transformation of the entire operating logic of credit business after the lending boom subsides; of course, looking at the entire space, the overall market demand for RWA lending far exceeds this single project of Goldfinch.

Although the debt has been registered on-chain, the debt recovery process still relies on offline borrowers’ performance, legal procedures, written evidence, and the human handling supported by governance budgets.

The Core Competency RWA Lending Platforms Must Self-Validate Going Forward

Goldfinch itself is just a single case in the tokenized private credit space. Data from DeFi data platform DefiLlama shows that the total value of locked assets and the scale of active on-chain loans in the entire RWA lending space far exceed Goldfinch's current size, and the overall demand in the space cannot be solely defined by a protocol entering a maintenance phase.

But this brings highly valuable industry conclusions: the tokenized private credit sector exists simultaneously in two completely disconnected market cycles. The first cycle is the fund injection stage: capital continues to enter the market, generating discussions about annual yields, corresponding to tokens being freely traded in the secondary market; the second cycle will arrive after several years: borrowers fail to fulfill their obligations on time, the debt collection cycle lengthens, and community governance requires continuous disbursement to maintain the entire collection system operations.

This makes Goldfinch not just a DeFi protocol but more like an investment target for bad debt disposal. Its future value will no longer depend on new feature iterations but rather on actual repayment amounts from borrowers, standardized collection operations, and whether the newly built trust structure can retain sufficient operational capability to recover all remaining debts.

Moving forward, the market will closely track several key signals:

- Whether community governance formally approves the GIP-87 liquidation proposal to finalize the subsequent operational route;

- Announcements from the newly established trust agency and asset management personnel to assess whether collection work forms a stable process;

- Public disclosure of borrower repayment progress to confirm whether outstanding claims can be converted into actual cash collections or remain stuck in prolonged negotiations;

- How all other RWA lending platforms can improve overdue asset disclosure rules, reserve operational funds for collection, and protect investors' rights after the income properties of credit products disappear.

The Goldfinch case straightforwardly points out the core dilemma of bad debt disposal: on-chain private credit can only simplify the tracking and statistical exposure of risks, yet debt collection is still constrained by offline borrowers, legal processes, governance budgets, and lengthy time cycles.

High-yield promotions can attract massive amounts of capital; however, during the bad debt disposal phase, the quality of the underlying credit assets will be truly tested for reliability.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。