Original Title: "Korea Triggers 'Black Tuesday', Global Chip Stocks Face 'Sudden Shock' in Bull Market, Is It Just a 'Technical Adjustment'?"

Original Source: Wall Street Journal

The recent plunge in chip stocks was not unexpectedly triggered by a "small article" from Korea, but rather a necessary clearing in an extremely crowded AI sector with weak leverage. Analysts at Goldman Sachs and others believe the AI narrative has not changed, with the sell-off concentrated on crowded long positions, resembling a "technical correction." However, with rising interest rate expectations and 65% of companies in a buyback blackout period, multiple pressures are already building, and there is no clear boundary between correction and mid-term risks.

On Tuesday, June 23, global chip stocks were caught off guard by Korea. A Wall Street strategist referred to the plunge as a "chip wreck."

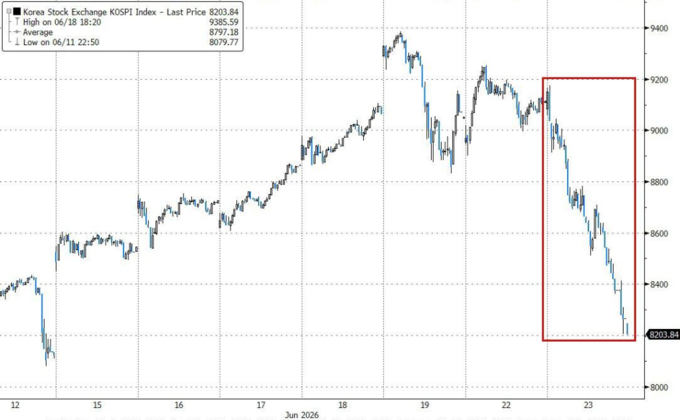

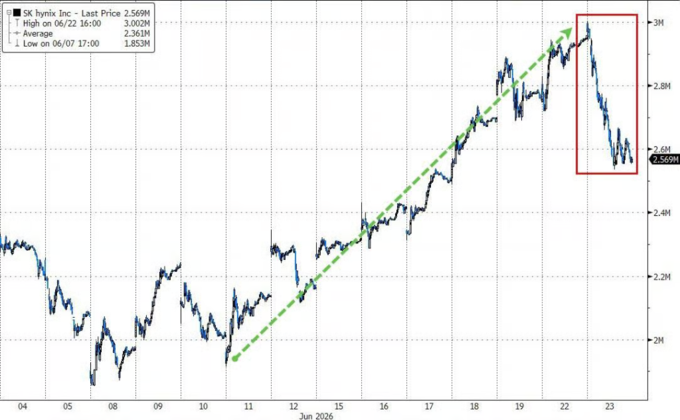

The first to crash was this year's "strongest global stock market"—Korea. The KOSPI index in Korea fell 10% in a single day, triggering multiple circuit breakers, with SK Hynix and Samsung Electronics each dropping over 10%.

Several small articles ignited this storm: South Korean media reported that Nvidia's Rubin expects production cuts, while SK Hynix is slowing down the production of its cache storage chips (HBM4) and shifting to cheaper standard DRAM; secondly, the Korean Central News Agency reported that South Korean multi-party lawmakers are discussing taxing unrealized gains on stocks, real estate, and other assets—meaning taxes are owed even on paper profits that haven't been sold.

This "chip earthquake" quickly transmitted to the U.S. stock market.

Overnight, the Philadelphia Semiconductor Index (SOX) dropped 7.9% in a single day, with all 30 component stocks falling, leaving no one unscathed. Micron Technologies fell 13%—prior to Tuesday, it had already gained over 300% this year, making it the strongest component of the Philadelphia Semiconductor Index. Micron, Nvidia, and AMD together accounted for about 50% of S&P 500's decline. The Nasdaq Composite fell 3.3%, the Dow Jones barely fell 0.1%, and the S&P 500 dropped 1.4%.

BTIG LLC Chief Market Technician Jonathan Krinsky stated: "Regardless of whether there’s a short-term rebound, we still believe the tech/AI sector faces mid-term downside risks." He thinks the semiconductor sector has more room to fall, around 10% to 15%, describing Tuesday's market action as a "chip catastrophe."

However, Goldman Sachs Global Banking & Markets TMT sector expert Peter Callahan wrote in a quick comment on June 24: "Most of today's discussions with investors revolved around 'What are you seeing over there?', rather than signs of a broader narrative change." This statement is key. It sets a boundary for this round of selling: the market looks bad, but at least on that day, there was no evidence of funds completely abandoning AI trading.

So the issue isn't as simple as "a small article from Korea shattered the global AI bull market." It’s more like a sector that has already risen significantly, is overly crowded in trading, and has low leverage, collectively de-risking upon encountering a trigger. In the short term, there do appear to be signs of a "technical adjustment"; in the mid-term, the vulnerabilities in AI trading have not vanished.

This is a transmission, not an accident

The crash in Korea seems sudden, but the underlying logic is not complex.

News of SK Hynix slowing down HBM4 production broke the stock, and this stock’s weight in the Korean stock market is akin to Apple’s in the Nasdaq—too large to withstand an issue without affecting the entire index. More critically, South Korean retail investors heavily utilize leveraged ETFs to participate in AI/semiconductor trading, and these products are forced to sell off to maintain leverage ratios when the market declines, leading to mechanical selling.

The news itself acted as the trigger, while the leverage structure was the explosive material. Meanwhile, market observers are asking: "Will Korean leveraged retail investors be the enders of the U.S. tech bull market?"

This question is certainly somewhat exaggerated, but it points to a genuine vulnerability: AI/semiconductor trading is highly concentrated, with global investor positions highly similar; any sale at one node could potentially transmit along this chain.

From after-hours data by Goldman Sachs, it is clear that both long and short sides were selling that day: Long-only funds had a negative skew of -18%, while hedge funds similarly continued to sell throughout the day, with short sales making up 60% of transaction volume (recent average about 50%). The sell-off scale for both types of institutions exceeded $1 billion in notional exposure.

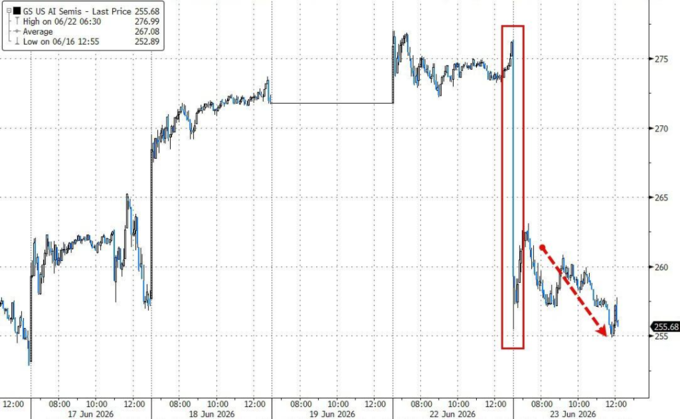

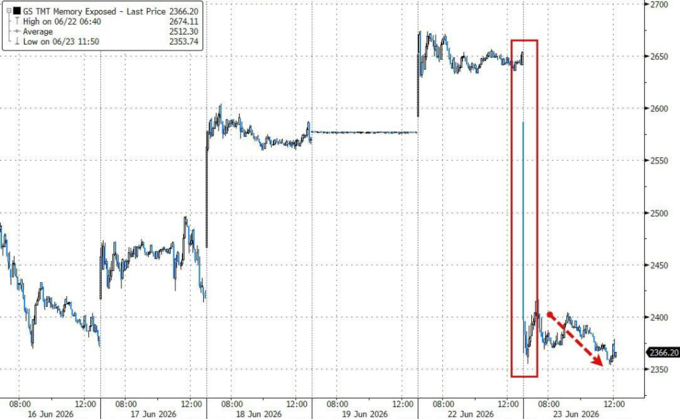

The hardest-hit stocks in the U.S. market were those "crowded longs," specifically those that were "the most profitable this year": Goldman’s storage stock basket (GSTMTMEM) fell 10%, AI semiconductor basket (GSCBSMHX) dropped 620 basis points, AI stock basket (GSTMTAIP) fell 440 basis points, and the strong stock basket over the past 12 months (GSXHUHMOM) dropped 420 basis points.

Technical adjustment? Goldman: No narrative change yet

Given such a significant drop, what does the market really think? If we only look at the magnitude of the drop, Tuesday seemed like AI trading was being re-priced. However, based on trading volume and capital feedback, the conclusion is not so absolute.

Goldman Sachs TMT trading desk expert Peter Callahan wrote in the after-hours report that the feeling of the day can be summarized in one word: "orderly"—despite the significant drop, the overall Nasdaq trading volume was basically in line with the 20-day average, and cash and volatility trading desks were functioning normally.

More crucially, he described the conversations with investors that day: "Most discussions with investors centered around 'What’s the situation over there?', and we did not see indications of a broader narrative logic change, nor did we see an increase in inquiries for 'new targets' or 'lagging targets'."

In other words, no one was shifting portfolios, no one was looking for new investment directions. Everyone was just asking each other for news.

Another market strategist at Goldman, Chris Hussey, provided specific data support: Among the 12 tech stocks that fell over 8% that day, with one exception, all others had still seen double-digit gains on the year, with many having already doubled. His judgment is:

"Today's sell-off is more like a 'deflation of the bubble' against a backdrop of a fervent stock price surge, rather than a fundamental re-evaluation of AI infrastructure trading. Investors are not broadly selling off the index, but are re-evaluating how much to pay for those stocks that have doubled in the last six months.”

Jack Janasiewicz, a fund manager at Natixis Advisors, shared a similar judgment direction:

"It seems this is more of a technical sell-off, rather than anything else. Market breadth was still decent after the open, even though there were many big red numbers—that's a signal of narrow selling." He also noted, "When we see such massive crowding in beta and momentum, it can easily lead to an ugly deleveraging."

The other side of "technical adjustment": Structural concerns that cannot be ignored

The term "technical adjustment" sounds comforting, but it can explain everything and may also mask real risks. On that day, there were indeed technical features: the drop was concentrated on winning stocks, trading was not out of control, and investor communication did not show signs of the AI narrative changing immediately. However, there is no clear wall between technical adjustments and structural risks—the former, if severe enough, can completely evolve into the latter.

Several background figures warrant consideration together.

First, the rise was too rapid. The Nasdaq has risen over 30% since the end of March. In June alone, the Philadelphia Semiconductor Index experienced 8 trading days (out of 16 trading days) with daily swings exceeding ±5%—meaning that in half of June's trading days, chip stocks were in violent oscillation. Even after Tuesday’s drop, the Philadelphia Semiconductor Index is still up about 5% this month, outperforming the Nasdaq and S&P by about 8 percentage points. A correction at this level has both technical reasons and vulnerabilities from the height of its rise.

Second, positions are too crowded, and the "supporting" forces are temporarily absent. Evercore ISI Chief Equity and Quantitative Strategist Julian Emmanuel, in an interview with Bloomberg TV, said: "People are looking for reasons to hedge while wanting to maintain their positions." This statement accurately describes the current market's contradictory mentality. At the same time, 65% of publicly traded companies are in buyback blackout periods. In the past, company buybacks were an important "supporting" force during downturns, but this time that card cannot be played.

Third, the macro backdrop is changing. Expectations for Federal Reserve interest rate hikes are rapidly rising—Bank of America predicts three more hikes this year, with the market's pricing probability for a July hike rising from nearly zero to about 50%. The valuation logic for high-growth tech stocks is built on low-rate discounts; once rates rise, the present value of expected future earnings naturally shrinks, hitting those stocks that rely on expectations to support high valuations the hardest.

JonesTrading Chief Market Strategist Michael O'Rourke wrote: "Ultra-large cloud computing companies are the new software stocks. This sector is dragging down the 'Seven Giants' while struggling to find its way out."

Apollo Chief Economist Torsten Slok outlined three core issues facing the current market: What happens if AI companies begin cutting compute budgets due to insufficient ROI? What will be the impact on the stock and credit markets if the Federal Reserve hikes rates in September and December? These questions do not have simple answers, but the market is shifting from 'willing to ignore these risks' to taking them seriously.

The reason a technical adjustment is worth paying attention to is not simply because of the drop itself, but because it occurs when valuations, positions, interest rates, and sentiment are all at extreme levels.

Historically, crashes in Korea are brief—while the next stress test is Micron

Historical data shows that sharp drops in the Korean stock market are often severe but brief. This is a "silver lining" that bulls like to cite.

However, this time the context differs from past purely domestic Korean events: it touches upon the core nerve of global AI trading—whether the demand for storage chips is actually as strong as anticipated? Has the frenzy of data center construction already overdrawn the future?

These questions will receive partial answers after Micron's earnings report on Wednesday. Micron is the strongest component of this year's Philadelphia Semiconductor Index, having risen over 300% before Tuesday, and Wednesday’s earnings report will serve as a genuine stress test.

What BTIG's Krinsky said may be the most direct: "Regardless of a short-term rebound, the mid-term downside risks for semiconductors remain."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。