Author: Claude, Deep Tide TechFlow

Deep Tide Guide: The rental price of Nvidia's B200 chip has dropped from a high of $6.11/hour at the end of May to $4.22/hour, falling about 30% in three weeks. Meanwhile, the semiconductor sector is showing a rare divergence: the SMH semiconductor ETF has risen 15% in the past month, Micron and SanDisk have surged nearly 60% each, while Nvidia has declined 3% during the same period. For those holding Nvidia or considering investments in AI infrastructure, a key question has emerged: the money for AI has not decreased, but has moved elsewhere.

Nvidia has still risen about 12% this year, but current market attention seems to have shifted away from it.

In the past month, the VanEck Semiconductor ETF (SMH) has risen strongly by 15%, with Micron Technology and SanDisk each soaring nearly 60%. Nvidia not only failed to keep up but has actually declined by about 3%. What underscores the issue further is that the core indicator supporting Nvidia’s pricing narrative, the cloud rental price for the B200 chip, is also softening.

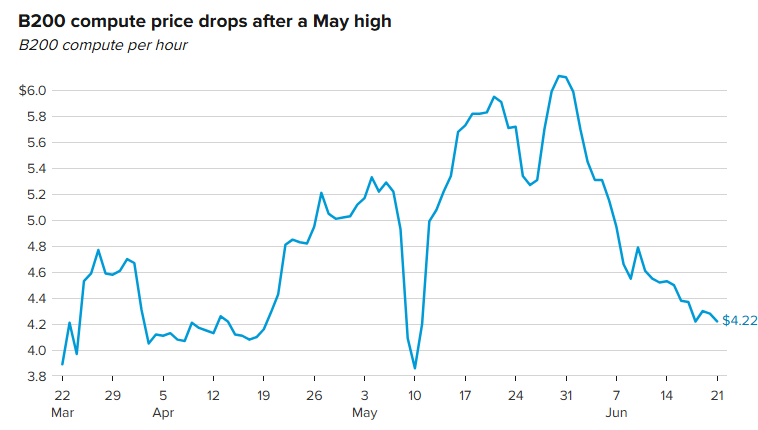

According to GPU pricing platform Ornn, the B200 rental price hit a three-month high of $6.11/hour on May 30, and has since continued to decline, falling to $4.22 as of last weekend, a decrease of about 30%. Goldman Sachs One-Delta desk head Rich Privorotsky directly pointed out last week: the myth of AI's "scarcity of computing power" may be falling from grace.

B200 rental prices down 30% in three weeks, "scarcity of computing power" narrative under pressure

The Nvidia B200 is a core computing chip for large-scale data centers, and its rental price is seen as a barometer of supply and demand for AI infrastructure. Data from multiple third-party tracking platforms indicates that B200 pricing is easing.

Ornn data shows that the B200 rental price has steadily decreased from the May 30 high of $6.11/hour, reporting $4.22 as of last weekend. The monthly price index compiled by AIMultiple from 63 cloud service providers indicates a median price of $6.11/hour for the B200; however, new cloud vendors have pushed their bottom price down to $3.44/hour. Data from 26 B200 cloud service providers tracked by GetDeploying is even more extreme: the average price is $4.99/hour, with the lowest offer at just $2.25/hour (for a three-year reserved contract).

There are three driving factors for the price decline: TSMC's improved yield in the 4NP process has lowered B200 shipment costs; SK Hynix and Micron's HBM3e supply will significantly ease in the second quarter of 2026; and more new cloud vendors have acquired B200 inventory, with RunPod, Lambda, Nebius, Spheron, and others offering ready stocks, leading to competitive pressure that has lowered overall pricing.

Pressure will be even greater in the second half of the year. As Nvidia's next-generation Blackwell Ultra B300 begins to enter the spot pool, some B200 capacity will shift from on-demand to bidding mode. The bidding (spot) price for the B300 has already been observed to drop as low as $2.45/hour, which is cheaper than the lowest listed price for the B200. Organizations like Spheron and Thunder Compute predict that the on-demand price for the B200 might stabilize in the range of $2.50 to $3.00 in the fourth quarter of 2026.

For investors holding Nvidia, softening rental prices mean that Nvidia’s downstream customers (cloud vendors, new cloud platforms) are under pressure on profit margins, and the purchasing willingness of these customers directly determines Nvidia's order pace.

Big diversity in the semiconductor sector: memory surges, Nvidia lags

The data from this round of divergence is quite striking.

Nvidia has risen about 12% year-to-date by 2026, but has fallen about 3% in the past month. During the same period, the SMH semiconductor ETF has increased 84% this year, rising 15% in the past month. Micron Technology has surged nearly 60% over the past month, with its stock price hitting a historic high of about $1,089, accumulating a gain of over 700% for the year, and its market value surpassing $1.2 trillion. SanDisk has also risen nearly 60% in the past month, with its 52-week gain exceeding 4,400%.

The market may not be pessimistic about AI anymore, but feels that the bottleneck in the AI value chain is shifting.

The previous logic was "GPU scarcity → Nvidia has pricing power → upstream profits the most." Now the logic has turned to: GPU supply is easing, but the demand for high-bandwidth memory (HBM) and storage from AI models is surging, making memory the new bottleneck.

Micron's latest quarterly report (Q2 2026) shows revenues of $23.8 billion, nearly doubling year-over-year (from $8 billion in the same period last year); after being spun off from Western Digital, SanDisk recorded revenues of $5.95 billion in Q3 of fiscal year 2026, a 97% increase year-over-year.

Data released by TrendForce on June 16 shows that memory contract prices have soared over 100% in the first half of 2026, and structural shortages are expected to continue into the second half. Apple CEO Tim Cook admitted in an interview last week that Apple can no longer absorb the rising costs of memory. When even the strongest price-advocating buyer like Apple publicly states they "can’t hold on anymore," it reveals the pricing power of memory manufacturers.

Micron will release its third quarter financial report tomorrow (June 24), with the market generally expecting it to set another record. This financial report will serve as a key verification of whether the "memory supercycle" can continue.

Goldman Sachs trading head: the core indicator is rental price

Goldman Sachs One-Delta desk head Rich Privorotsky proposed a clear judgment framework last week:

If computing power resources are indeed scarce, rental prices should remain firm, making continued capital expenditure justifiable. If supply increases and rental prices continue to decline, the core assumption supporting the valuation of the entire AI hardware chain, which is "scarcity of computing power," will be shaken.

He further pointed out that this pressure will first be reflected at the hardware level. The true beneficiaries are the companies selling complete systems and monetizing through usage, rather than those just selling "picks and shovels" upstream. The greater risk lies in the upstream segments of the hardware and infrastructure stack, as their valuations are still based on the premise of "continuous shortage."

The direction of these remarks is clear: Nvidia’s business model is selling chips (picks and shovels), rather than charging based on usage. If downstream customers' rental prices are falling, but Nvidia's chip prices are not decreasing, there will be a profit squeeze in the intermediate segment, which will ultimately feed back into a slowdown in orders.

Citadel Securities' recent "Tokenomics" report echoed similar judgments: the core constraint on AI adoption has shifted from "model capability" to "cost and scarcity of computing power," with users accelerating their migration towards cheaper models. The Token Price Index has fallen for seven consecutive days, marking the longest decline this year.

Seoyoung Kim, a finance professor at Santa Clara University, described it more bluntly: most buyers do not know how much computing power they will need next year, suppliers do not know how many GPUs to order, and Nvidia does not know how many to produce. All three parties are guessing, and when the direction of guesses shifts from "not enough" to "maybe too much," prices will come under pressure.

$30 billion contract between SpaceX and Google: long-term market remains hot

While spot rental prices are falling, the long-term market tells a different story.

According to a document submitted by SpaceX to the SEC on June 5, Google has agreed to pay SpaceX $920 million per month from October 2026 to June 2029 to lease about 110,000 Nvidia GPUs and associated processors, memory, and other components. The total contract value is about $30 billion. In May, Anthropic signed a similar agreement with SpaceX, paying $1.25 billion a month to lease all available computing power at its Colossus 1 data center in Memphis, with a total value of nearly $45 billion.

The context for these two contracts is that after SpaceX completes its merger with xAI in February 2026, it will convert xAI's previously self-built Colossus supercomputer cluster into an externally rentable commercial asset, locking in substantial revenue ahead of its IPO (with a target valuation of $17.5 trillion).

For Nvidia, this is a contradictory signal. On one hand, the long-term contract for 110,000 GPUs proves that large clients are still locking in computing power on a large scale. RBC Capital Markets stated after the announcement of the deal that Nvidia is "in the most advantageous position among its peers," believing that these GPU rental agreements can at least alleviate market concerns about ASICs eating into Nvidia's market share in the short term.

On the other hand, Google’s need to lease computing power from SpaceX precisely stems from its self-built capacity not keeping up with demand. Google’s capital expenditures for 2026 are between $180 billion to $190 billion, with SpaceX's monthly fee of $920 million accounting for less than 6% of its annual budget, essentially acting as "bridge capacity." When these super clients' data centers gradually come online between 2027 and 2028, whether external leasing demand can maintain its current scale remains an open question.

The contract also includes a termination clause with a 90-day notice period. This does not seem like a contract signed during a time of "extreme scarcity of computing power," but rather a provision that buyers have left for an exit.

Nvidia’s risk: not on the demand side but on pricing power

Tying together the clues above, the issue facing Nvidia is that the profit distribution in the AI value chain is changing.

On the GPU supply side, factors such as TSMC's improved yields, more vendors acquiring inventory, and the impending large-scale launch of the B300 are alleviating the extreme shortage expected in 2024-2025. On the demand side, super clients are still purchasing on a large scale, but the purchasing tactics are shifting from "spare no effort to grab goods" to "comparative pricing, locking in long-term contracts, and reserving exit rights." On the profit side, the rental prices for downstream cloud vendors are already falling; if Nvidia's own chip prices cannot adjust downward simultaneously, the profit squeeze in the intermediate processes will ultimately backfire into order reductions.

The rise of memory chips as a new favorite is another side of the value chain shift.

The larger the AI models and the more inference tasks there are, the greater the rigid demand for high-bandwidth memory becomes. GPUs can improve efficiency through architectural upgrades (for example, the FP4 precision of the B200 halves each parameter byte), but memory bandwidth is a physical bottleneck with no shortcuts. Micron's HBM capacity is sold out for all of 2026; this "can't buy even with money" situation is in stark contrast to the declining rental prices for Nvidia's B200.

Micron's financial report tomorrow will provide the next key data point. If revenues and guidance exceed expectations again, the narrative of "the AI value chain migrating from GPUs to memory" will be further reinforced. For investors, this is not bearish on AI but a need to rethink who is gaining pricing power and who is losing it along the AI supply chain.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。