Author: Nancy, PANews

Amid continuing weakness in crypto assets, crypto mining companies are facing increasingly severe survival pressures. In search of new growth trajectories, more and more mining firms are accelerating their entry into the AI sector. This transformation narrative has quickly gained favor in the capital markets, with the stock prices of many mining companies rising sharply, even reaching all-time highs.

However, while AI business injects new growth imagination into mining companies, the huge capital expenditures, ongoing financial investments, and lengthy payback periods behind it are pushing mining firms towards another battle of capital consumption. With the profitability of mining operations under sustained pressure, this gamble towards AI transformation is testing the financial strength and execution capabilities of mining companies.

Stock prices significantly outperform Bitcoin, mining company valuations enter a differentiation phase

Mining companies are transforming into power landlords in the AI era.

As the profit margins for Bitcoin mining continue to shrink, some mining companies have even fallen into losses, while the explosion of AI is driving a sharp increase in global demand for data centers, power resources, and GPU computing power. An increasing number of mining firms are beginning to accelerate their transition into the AI infrastructure field, seeking new growth curves.

For mining companies, this transition has natural advantages. For a long time, to meet the demands of large-scale mining, mining firms have acquired key assets such as abundant power resources, land reserves, substation access capabilities, and mature heat dissipation and cooling systems. Compared to data center operators starting from scratch, mining companies only need to upgrade existing facilities to quickly enter the AI infrastructure market, meeting AI computing power demands at lower costs and shorter timeframes.

Since last year, the pace of mining companies transitioning to AI has accelerated significantly. Some miners have decisively downplayed or even exited traditional mining operations, fully shifting to AI computing power and data center operations; others have retained some mining machine business but gradually shifted resource allocation and capital expenditure focus towards the AI field. Now, several mining companies have grown into important participants in AI infrastructure construction.

In terms of transition timing, companies like CoreWeave, Applied Digital, and Bitdeer began laying out AI computing power and data center businesses as early as 2022 to 2023, representing some of the earliest transformers in the industry; while mining companies such as Iris Energy, Terawulf, Hut 8, Riot Platforms, and Bitfarms began to intensively invest in AI infrastructure construction starting in 2025, coinciding with the AI industry entering a rapid expansion cycle.

In terms of stock price performance, the market has given high recognition to the narrative of mining companies' AI transformation. The average increase for 11 mining companies has reached 75.97% since the beginning of the year, significantly outperforming Bitcoin's performance in the same period, with most seeing their stock prices even reaching new highs after the transition. Among them, Bitfarms (129.62%), Hut 8 (131.87%), Terawulf (118.68%), and Riot Platforms (93.71%) have performed particularly well, benefiting from this round of AI infrastructure re-evaluation.

From a market capitalization perspective, mining companies have shown significant differentiation, with CoreWeave, as a successful transition representative, reaching a market capitalization of $62.855 billion, far exceeding other mining firms and becoming the new valuation benchmark in the industry. Iris Energy, Terawulf, Hut 8, Applied Digital, and Riot Platforms have formed a market capitalization tier ranging from $10 billion to $20 billion, while MARA Holdings, Core Scientific, Bitdeer, CleanSpark, and Bitfarms remain below $5 billion. This differentiation is not only due to first-mover advantages but also because the market has begun to apply differentiated pricing based on each mining company's execution capabilities in AI strategy, customer resources, and progress in establishing data centers.

However, from a fundamental perspective, most mining companies are still in the heavy investment phase of AI transformation. Although many mining companies' latest quarterly reports show revenue growth, overall profitability remains under pressure. On one hand, fluctuations in the value of cryptocurrency investment portfolios have dragged down profit performance; on the other hand, the construction of AI data centers requires substantial capital expenditures, with increasing investments in power expansion, infrastructure construction, and GPU equipment procurement, pushing operating costs continuously upward, resulting in many mining firms still not escaping losses.

It is noteworthy that despite generally pressured performance, the stock prices of related mining companies have still seen significant increases, indicating that the current market focus is not on short-term profitability, but rather on the growth potential of mining companies as operators of next-generation computing infrastructure.

The survival battle for mining companies escalates, and the AI transformation still needs to overcome multiple hurdles

The downturn in the Bitcoin market is making the survival environment for mining companies increasingly severe.

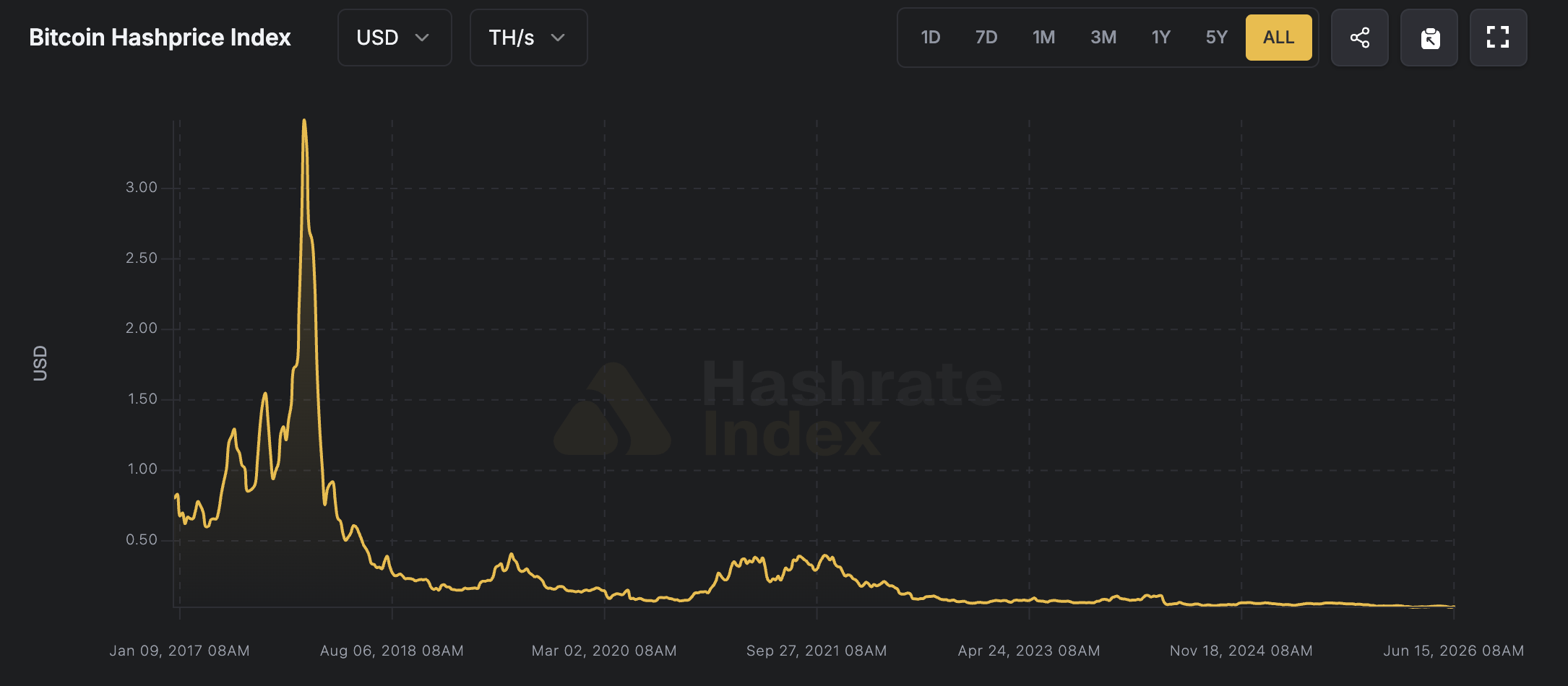

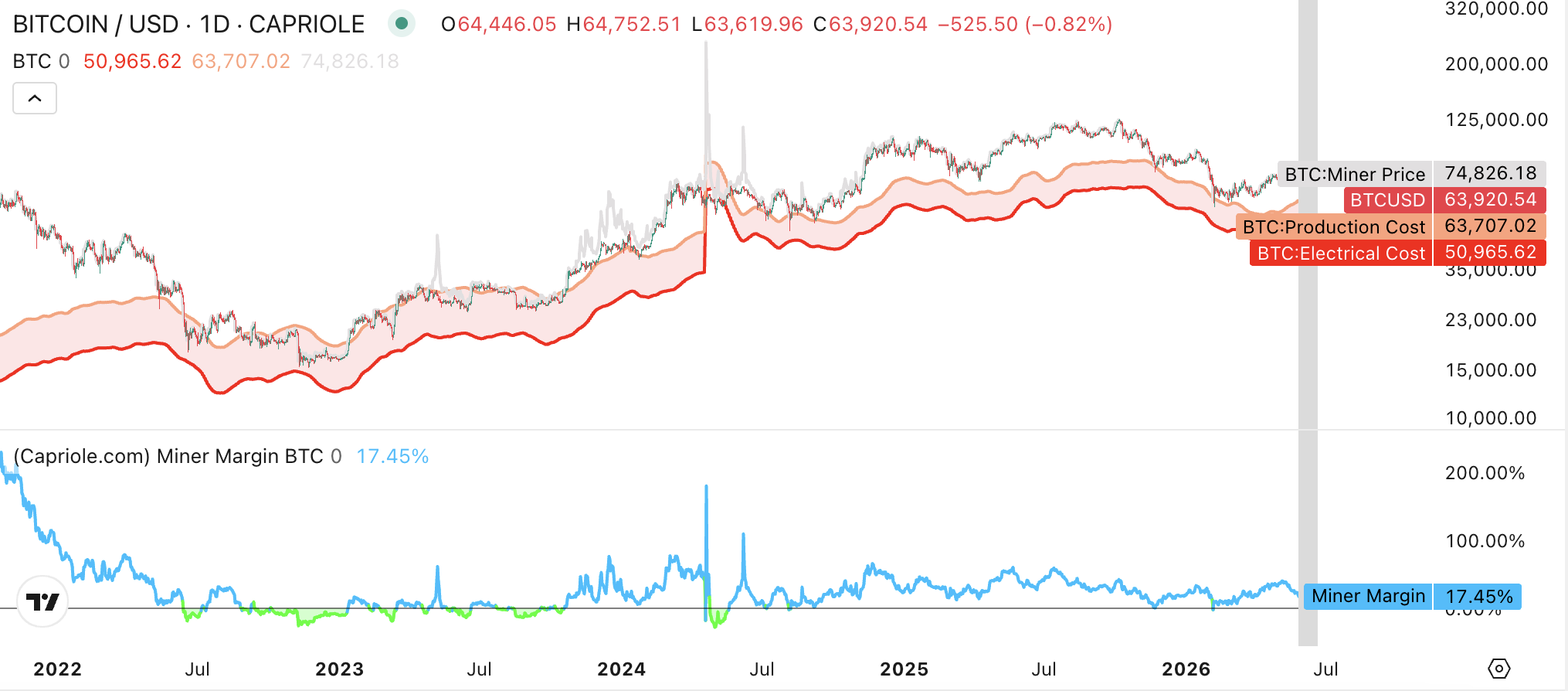

According to data from Capriole Investments, as of June 18, the average production cost of Bitcoin is about $63,707, of which electricity costs about $50,965, resulting in a miner's profit margin of only 17.45%. Over the past 30 days, the miner's profit margin has contracted by 47.8%. At the same time, the Luxor Hashrate Index also shows that as of June 18, the daily return for 1 TH/s computing power has dropped to $0.032, a significant decline from $0.053 in the same period last year.

As mining revenues continue to shrink, many mining companies are forced to sell Bitcoin to maintain cash flow, with the survival pressure on small and medium-sized miners further exacerbated, accelerating the concentration of mining resources towards leading players. Currently, Foundry USA, AntPool, and F2Pool collectively hold a 59% market share of total network hashrate. In contrast, in 2022, the top three Bitcoin mining pools only accounted for 44% of the hashrate market share.

Although traditional mining operations face an unfavorable market, the explosive growth in demand for AI data centers is driving a market reassessment of mining companies' value. VanEck’s latest research report points out that the most valuable assets of mining companies are not the mining machines but rather the power resources, substation access capabilities, land reserves, and data center infrastructure, which are precisely the core resources currently most scarce in the AI industry. Because AI customers are willing to pay electricity prices and rents far exceeding those of traditional mining operations, AI infrastructure is expected to become the main growth engine for mining companies over the next decade.

According to a report by research firm Bernstein, major cloud providers, AI cloud service providers, and chip companies have announced over $90 billion in AI infrastructure partnerships, involving approximately 3.7 GW of power capacity. Currently, chasing power resources is becoming the core of AI infrastructure competition, with Bitcoin mining companies collectively controlling over 27 GW of planned power capacity. In some areas of the United States, the new electricity access cycle for 1 GW can take up to 50 months, which makes existing mining sites important landing spots for AI data center expansion.

However, the AI transition is far from an easy path. VanEck indicates that the current market is still in the early phase of AI transformation, with corporate valuations primarily measured based on gross energized power (Gross Energized Power). Mining companies that have signed AI leases generally receive higher valuation premiums, while projects that remain at the planning stage struggle to gain market recognition. In the future, industry valuation logic will gradually shift from "power capacity" to "project delivery capability," ultimately returning to core metrics such as cash flow, capital return rates, and tenant quality. Currently, the industry has only completed about 25% of the signed capacity delivery, and whether construction of AI data centers can be completed on time and within budget will become a crucial factor in determining corporate valuation.

VanEck also emphasizes that the quality of AI tenants will directly impact the valuation levels of mining companies. Customers like Microsoft, Amazon, and Google, as large-scale cloud providers, can bring more stable cash flows and lower financing costs, while smaller GPU cloud service providers correspond to higher operational risks and capital costs.

The massive financial investment required for the transformation is also testing the financial strength of mining companies. VanEck predicts that mining companies still face huge capital expenditure needs in transitioning to AI infrastructure, with a short-term financing gap of about $50 billion and long-term capital needs potentially reaching $221 billion.

Under this immense financial pressure, many mining companies have already begun to raise funds through various means. For instance, mining firms like Iris Energy, TeraWulf, Bitfarms, and CleanSpark are financing through convertible bonds to attract investors with lower coupon rates and future equity conversion potential; while companies such as Core Scientific, Terawulf, MARA, Bitdeer, and Riot Platforms have chosen to sell or even liquidate part of their Bitcoin reserves to continuously fund their AI transformation.

Additionally, many mining companies are starting to secure future revenues by signing long-term AI or high-performance computing (HPC) contracts for project financing support and reducing overall operating risks. For example, CoreWeave reached a $6 billion AI cloud service cooperation agreement with Jane Street; IREN obtained a $9.7 billion AI cloud computing contract from Microsoft; Hut 8 signed a total worth $9.8 billion data center leasing agreement; and Bitdeer cooperated with DCI in Norway to build the country's largest AI data center project.

For mining companies, AI undoubtedly provides a development path that is far more imaginative than traditional mining operations. However, this transformation is not simply a switch from mining to selling computing power; at its core, it is a long-term competition revolving around capital, resources, and execution capabilities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。