TL;DR

- STRC fell to about $89, with a simple current yield of approximately 12.9% based on an annualized dividend of $11.5.

- The market disagreement is not whether Strategy can immediately afford dividends, but how to discount BTC reserves, high-interest financing, on-chain leverage, and competition from similar products.

- Related assets: STRC, MSTR/Strategy, SATA, BTC, Pendle, and associated on-chain yield products.

Over the past two days, the perpetual preferred stock STRC under Strategy has dropped to about $89, significantly deviating from its $100 par value, which has raised its simple yield to about 12.9% based on current prices.

The peculiarity of this situation lies in the fact that STRC was originally designed as a high-yield tool operating around par value. Strategy maintains an annualized dividend of 11.5%, and shareholders approved on June 8 to change the payment frequency from monthly to bi-monthly, with public arrangements expected to start in July, and the first bi-monthly payment date anticipated to be July 15, still pending board declaration. Intuitively, more frequent dividend payments should help the price converge towards $100.

The market is not pricing it this way. Strategy and Michael Saylor emphasize the asset coverage logic: as of June 15, the company disclosed it holds 846,842 BTC, and the credit metrics page shows BTC Years of Dividends at approximately 31.6 years, with an STRC BTC Rating of 3.1x. The market's concern expressed at $89 is another layer: such high-interest financing tools supported by BTC reserves need to bear higher leverage, liquidity, competition, and cash flow discounts.

For holders, the question is not whether 12.9% seems high enough, but rather why high yields have not pulled the price back to parity. This determines whether the current discount on STRC is a temporary mispricing or a new risk premium starting point.

High-Yield Assets Can Trigger Reverse De-leveraging

After STRC falls to $89, one of the most discussed explanations in the market is the potential reverse unwinding of carry trades.

Carry trade refers to borrowing low-cost funds to purchase high-yield assets. Investors borrow dollars or stablecoin funds to buy STRC, earning the spread between the nominal dividend of 11.5% and the financing cost. As long as STRC is steady around $100, this trade seems low volatility and backs the BTC narrative of Strategy.

The risk emerges when the price anchor weakens. Once STRC drops from around $100 to $95, 92, or 89, the risk control logic for leveraged accounts will change. Some investors may need to add margin, reduce positions, or even sell STRC to repay loans. Selling pressure depresses prices, and the price drop can trigger more risk controls, resulting in high-yield assets being sold off further.

A boundary must be maintained here. Currently, there are no exchanges, brokers, or custody-level public data to prove large-scale liquidation by institutions. More accurately, if the high-yield stable narrative of STRC attracted enough leveraged funds in recent months, the downturn near $89 may not be solely a fundamental revaluation but also involves mechanical de-leveraging.

This explains why an increase in yields does not necessarily lead to immediate buying. For unleveraged cash buyers, 12.9% is more attractive. For leveraged buyers, price declines first bring margin pressure, and higher yields may not be realized in time.

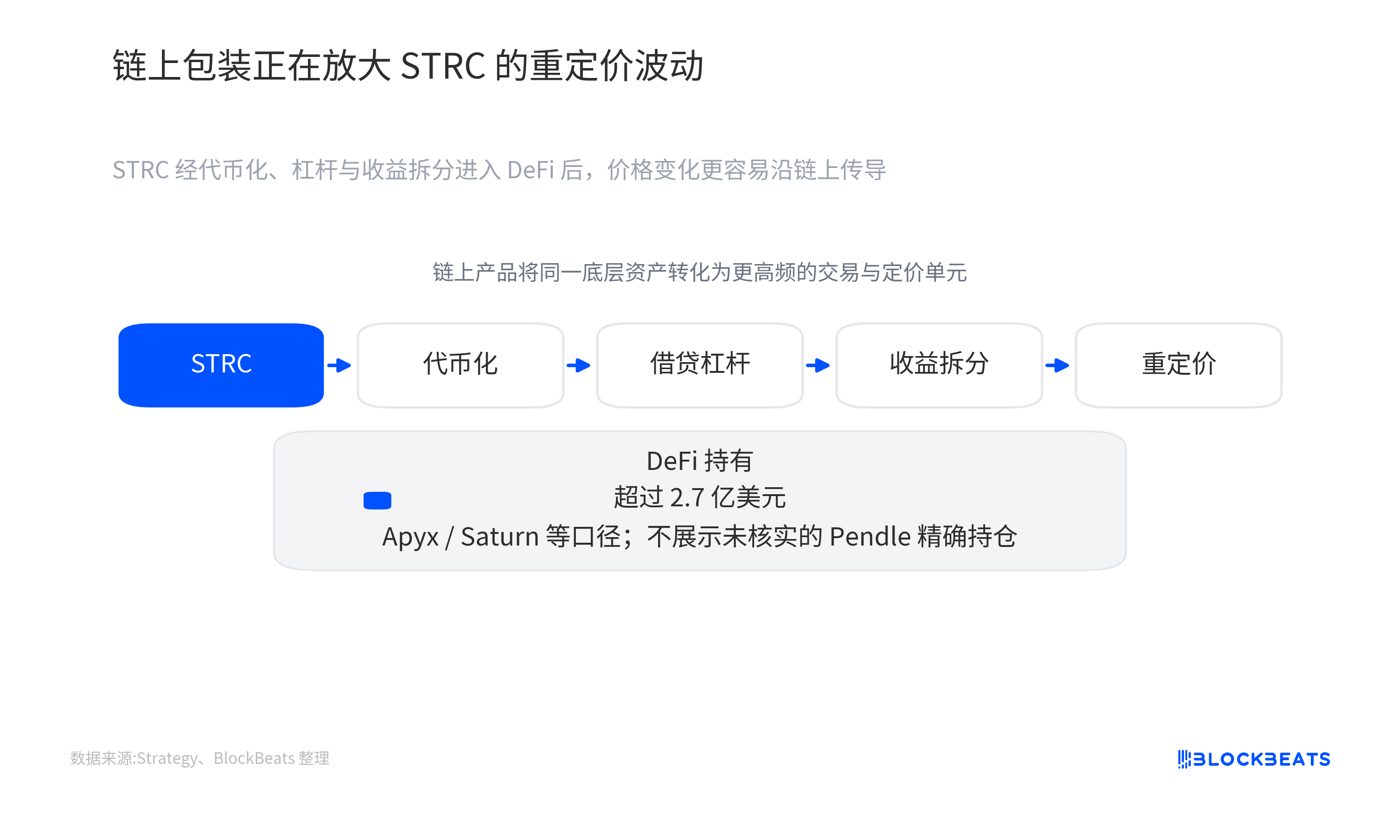

On-Chain Wrapping Amplifies Price Adjustments

The new variable with STRC is that it no longer only exists within traditional brokerage accounts, as it has also been wrapped into DeFi yields and leverage structures.

Preferred stock is originally a relatively slow asset: dividends are paid at intervals, traded in secondary markets, with prices fluctuating around yields. Once STRC is tokenized and enters loan, leverage, and yield-splitting systems, it connects to faster clearing and speculative mechanisms in the crypto market.

Protocols like Apyx, Saturn, and Pendle have built different forms of on-chain products around STRC. Saturn tokenizes it into a yield-bearing asset, Apyx offers leveraged yield aggregation, and Pendle can split assets into PT/YT parts, where PT represents the principal part and YT represents the rights to future income. Investors can not only buy STRC itself but can also trade based on principal discounts or expectations for future dividends.

In layman's terms, this is akin to splitting a traditional high-yield preferred stock into multiple layers of crypto yield components. Some buy stable yields, some leverage to amplify annual yields, and some bet on future dividends separately. Funding efficiency has increased, but so has vulnerability. If the underlying asset price falls, on-chain collateral rates, loan positions, and yield expectations can all adjust simultaneously.

Currently, a more prudent judgment is that STRC has entered on-chain yields, leverage, and splitting systems. Strategy documents mention Apyx's scale of about $280 million, xSTRC's scale of about $83 million, and STRC supporting stablecoins of about $70 million, among others. Pendle-related pools and transactions also have considerable scale, but public information is insufficient to support claims that its vault holdings reach the hundred million level.

Therefore, understanding DeFi wrapping as a channel for amplifying volatility is more suitable. It is not necessarily the first domino to fall, nor can it directly prove that this round of decline is led by on-chain liquidations. However, it makes what was originally a slow price adjustment much faster, more transparent, and more easily traded by leveraged funds.

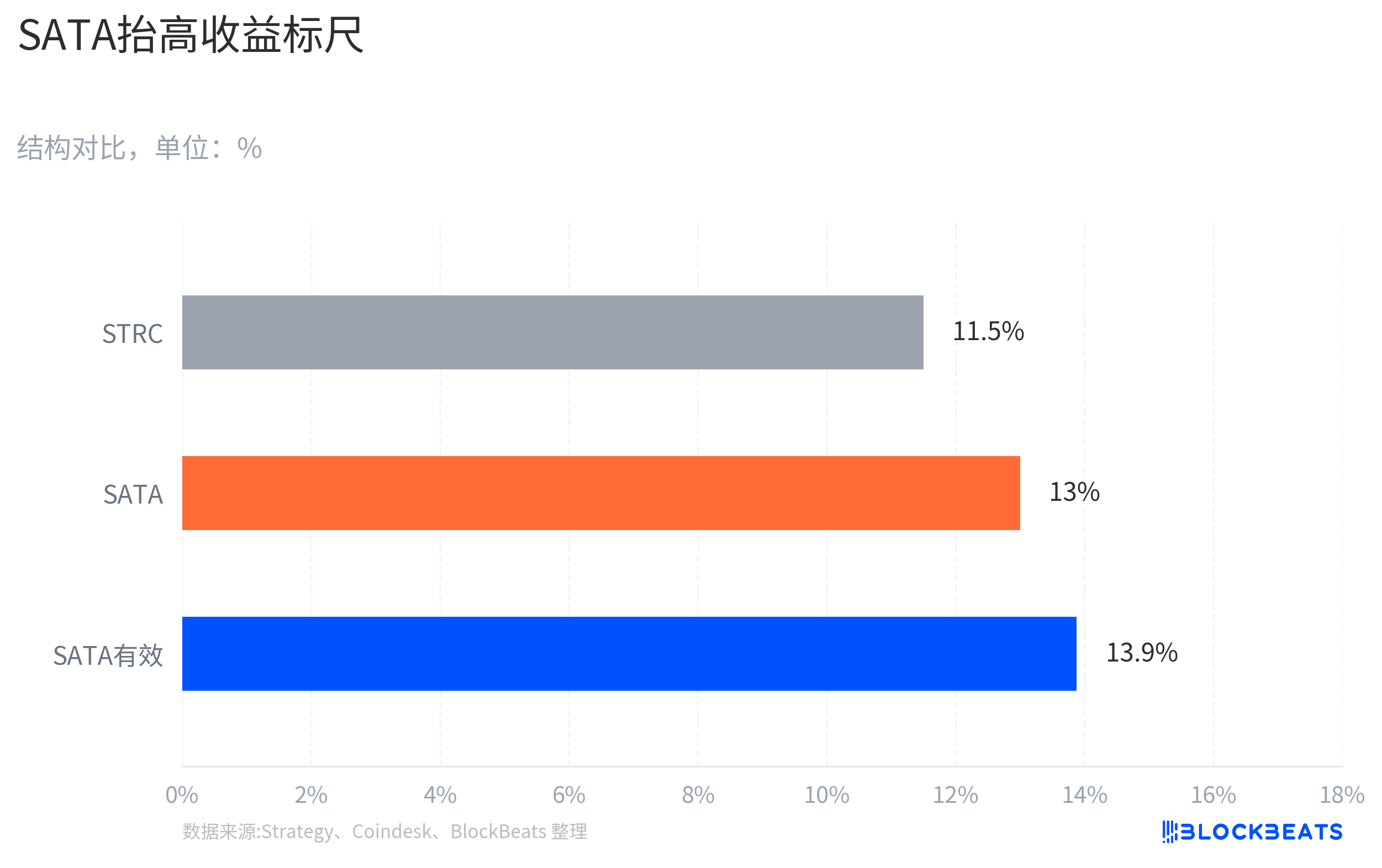

SATA Changes the Yield Reference

STRC's past attractiveness partly stemmed from its scarcity. It is an important product for earning funds within the Strategy BTC financing system, combining high yields, the BTC narrative, and a relatively clear par value anchor.

The emergence of SATA has weakened this scarcity. According to reports from Coindesk, Strive's SATA offers 13% annualized yield and has changed to daily payouts starting June 16. Compared to STRC, SATA has a smaller scale and weaker liquidity, and cannot simply be seen as a comparable substitute. But for pure yield funds, it provides a new comparison coordinate.

This impact does not need to rely on the premise that large amounts of funds have already flowed from STRC to SATA. Yielding funds will compare nominal yields, payout frequencies, liquidity, issuer credit, asset coverage criteria, and secondary market discounts. As long as the market sees a comparative reference with higher yields and higher payout frequencies, STRC's original narrative of being a "unique high-yield BTC tool" will be re-examined.

When priced near $100, the 11.5% of STRC may have been sufficient to attract buying. But after the price drops to $89, the issue becomes whether the simple current yield of 12.9% is enough to compensate for the Strategy financing structure, BTC volatility, potential leverage squeezes, and cash flow uncertainty.

Previously, STRC's anchor was "Strategy + BTC reserves + $100 par value." Now the market has introduced a yield curve of comparable products. When similar products offer higher nominal yields and higher payout frequencies, STRC will need stronger buying, clearer adjustment expectations, or lower leverage pressure to return to par.

Can the Par Mechanism Repair Cash Flow Doubts?

STRC can be understood as a high-yield preferred stock with no maturity date, anchored at a par value of $100. It has no fixed repayment date, and investors mainly look at two things: whether dividends can be sustained, and whether the secondary market price can get close to par.

Strategy designed an adjustable dividend mechanism for STRC. It is not a fully fixed coupon preferred stock left to be priced by the market; the company can adjust the dividend levels monthly, aiming to keep the price around $100. Shareholders' approval of the bi-monthly payment arrangement also follows the same pricing stability reasoning: shortening the waiting period for dividends reduces the uncertainty for yield funds held during that time.

Another layer of endorsement provided by the Saylor system is the BTC reserves. Strategy has packaged STRC as a special security: it is not a typical bank preferred stock, nor is it a pure crypto token but a high-yield financing tool supported by one of the largest corporate BTC holdings globally.

However, asset coverage does not equate to cash flow being risk-free. Approximately 31.6 years of dividend coverage indicates a buffer on a balance sheet level, relying on BTC prices, financing capabilities, and the company's long-term capital market access. It does not mean that every dividend payment has a stable operational cash flow source, nor does it mean that the secondary market must return to $100.

On June 1, Strategy disclosed that it sold 32 BTC at an average price of about $77,135 between May 26 and 31, totaling about $2.5 million, for dividend-related arrangements. This scale only accounts for a small proportion of the holdings, which does not suggest reserve pressure, but it reminds the market to distinguish between two things: having a lot of BTC and having sustainable cash flow.

Whether the Par Anchor Can Repair Determines Financing Costs

The most critical verification point for STRC now is not the approximately 31.6-year coverage statement itself, but whether Strategy will use actual mechanisms to pull the price back toward $100.

If Strategy continues to maintain an annualized dividend of 11.5% while STRC remains around $90 for an extended period, the market may perceive the company as being more tolerant of rising financing costs or believe that the adjustable dividend mechanism has not immediately repaired the anchor. Conversely, if the company further raises the dividend rate, adjusts the issuance pace, or enhances secondary market confidence in other ways, $89 is more likely to be viewed as an excessive discount after leveraged pullback.

On the on-chain side, observation is also needed. Whether STRC-related positions in Apyx, Saturn, Pendle, and other products have cooled off, and whether collateral and yield-splitting transactions are stable will determine whether the DeFi amplifiers continue to amplify volatility or return to being sources of demand after de-leveraging. The size and liquidity of SATA are also critical. If it is merely a small-scale high-yield reference, its impact on STRC will remain more in terms of valuation comparison; if it continues to expand and maintains the attractiveness of daily payouts, the scarcity discount of STRC will be harder to disappear.

For investors, $89 is not just a simple cheap label, nor is it evidence of Strategy's failure. It is more like a stress test: when BTC reserves, high nominal dividends, on-chain leverage, and competing products are simultaneously presented in the market, how high of a yield investors are willing to accept to hold such tools. The next dividend adjustment, whether STRC can return to near par value, and whether leveraged positions continue to loosen will better answer this question than the coverage year statement.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。