Organized & compiled by: Shen Chao TechFlow

Speakers: Josh Kale, Marketing at AnthropicAI; Ejaaz Ahamadeen, former Product Manager at Coinbase

Podcast source: Limitless Podcast

Original title: Leopold Aschenbrenner says "No More Stocks!"

Broadcast date: June 17, 2026

Key Summary

Leopold Aschenbrenner, regarded as one of the most aggressive AI investors in the world, is shorting NVIDIA, ASML, and Oracle with a nominal position of about $9 billion in the open market while reallocating funds to electricity, memory, data center networks, and deeper AI infrastructure and model assets like Anthropic. The two hosts believe this does not mean that the AI bubble has burst, but rather signifies a rotation of infrastructure deals from "chip-first" to "energy, networks, data center construction first," especially after NVIDIA just completed a $25 billion bond financing and Anthropic's valuation was pushed up, making this judgment's market implications rapidly amplified.

Highlights of Viewpoints

Leopold's Core Trading Logic

- "The classic 'selling shovels' trade in AI has become too crowded, and Leopold's recent position change conveys this signal."

- "His judgment is not that AI infrastructure has peaked, but that certain layers in the infrastructure stack, especially semiconductors and traditional hot stocks, have become too crowded."

- "If the question becomes where the funds will flow next, there are two answers. The first, most direct, is to flow into the next real infrastructure bottleneck, which is electricity, memory, and data center networks. The second answer is that mysterious investment revealed a few weeks ago."

- "What he has always bet on are very infrastructure-oriented assets, both investing in these optical companies and in electricity-related companies."

- "If he is cautious about NVIDIA, the funds will go into electricity and memory; at the same time, he wants to invest directly in the 'mine' itself, instead of just buying 'shovels,' with Anthropic being his favorite mine."

Signals from NVIDIA Financing

- "The issue is not whether NVIDIA will continue to make money, but why a highly profitable company with a large cash reserve would go to external sources for another $25 billion."

- "If a company simultaneously conducts a large stock buyback, significantly increases dividends, and borrows money, it is obviously not borrowing because it lacks cash. A more reasonable explanation is that this is cheap money, and the financing methods of the current AI market are showing slight changes."

The Next Wave of AI Infrastructure Dividend

- "The real bottleneck is no longer just GPUs, but electricity, memory, data center networks, and the ability to actually build these things."

- "Even if you raise more money, you can’t build data centers fast enough, expand enough memory chip capacity, or immediately upgrade the grid, power lines, and related infrastructure. There aren’t enough hands on the ground, and approvals, regulations, and various processes are holding you back."

- "Whoever has the ability to build data centers will make the money."

Optical Modules, Copper, and Fiber Optics

- "As GPU scales grow larger, copper wires become hotter, energy loss increases, and efficiency deteriorates, while fiber optics will become the next upgrade direction under these circumstances."

- "In short-distance high-bandwidth transmission scenarios, copper is almost the only material people genuinely want to use. Only when it starts to become unsuitable, such as when the distance is too great or the heat is too high, will it switch to fiber optics. Therefore, the current market demand for the combination of copper and fiber optics is very strong."

- "Copper futures have recently performed strongly because everyone needs it; it is the critical foundational material for short-distance high-bandwidth transmission, while fiber optics is the next step."

- Copper remains the most critical material in short-distance high-bandwidth transmission, but once the distance is extended or the heat becomes excessive, fiber optics must be transitioned to.

- "The next funds will flow into those infrastructure companies that don’t sound sexy."

Why Energy is the Safest Bet

- "I have always been optimistic about energy, because even if AI demand slows down, energy itself is still a global necessity, and this demand will only increase."

- "The single trend that will persist in any scenario is our demand for energy, electricity, and power; these companies are the ones I am most willing to invest in for the long term."

- "The companies I want to follow closely are those that Jensen is investing in, which also intersect with Leopold's logic. So the stock I am closest to following now is Marvell."

- "The best long-term position is not necessarily the hottest chip companies but rather those power infrastructure that can’t be bypassed in any macroeconomic scenario."

Leopold's AI Investment Portfolio

Josh Kale:

Leopold Aschenbrenner is a 24-year-old who specializes in investing in AI, and he is now almost regarded by the market as the strongest AI investor globally. Rumor has it that the nominal position of his fund has exceeded $20 billion. A month ago, when we looked at Ejaaz's post, the fund's scale was only $13.7 billion, which means it is essentially doubling every quarter.

This time we have obtained several significant new changes in his recent investment trends. In the last episode, we discussed his investment portfolio; one of the most surprising things at that time was that he was shorting a company that almost everyone is familiar with, which is NVIDIA, the world's highest market cap and hottest AI stock. Many people couldn't understand why he would take a short position exceeding $9 billion against such a company.

Now we have obtained a possible clue that explains this matter. NVIDIA is actually financing, and it is through bond financing. On the surface, this seems unreasonable. Why would a company as colossal and highly profitable as NVIDIA need to take out another $25 billion after just completing a cash inflow? Today we want to discuss this, combined with Leopold’s portfolio, to talk about how he can make so much money, what he is looking at next, and what this financing from NVIDIA really means.

Ejaaz Ahamadeen:

First, let me give you a bit of background. Leopold Aschenbrenner was previously a researcher at OpenAI and raised a fund about a year and a half to two years ago, which initially was not large, I recall it was about $200 million, but according to his latest 13F filing, this fund's publicly disclosed holdings are already valued at $13.7 billion.

So the market is naturally very curious about what positions he has, what his core investment logic is, and where the next major trade will land. To understand this, you need to know that a month ago, Leopold was indeed very optimistic about the entire AI track, especially favoring the "selling shovels" logic, which means companies like NVIDIA and upstream hardware suppliers.

But about a month ago, the market discovered that he did not see the semiconductor line as optimistically as before. He still sees potential in memory, electricity, and those real bottleneck segments, perhaps also in new cloud suppliers, but he notably does not see the most valuable company in the world, NVIDIA, positively. More specifically, he had placed approximately $9 billion in bearish positions against several companies considered core beneficiaries of AI infrastructure, like NVIDIA, ASML, and Oracle.

The Logic Behind Shorting NVIDIA

Ejaaz Ahamadeen:

Once this matter came to light, many people started worrying about whether the AI bubble was about to burst. After all, on the surface, NVIDIA's GPUs are still selling well, and demand hasn’t shown significant weakness, so where is the problem?

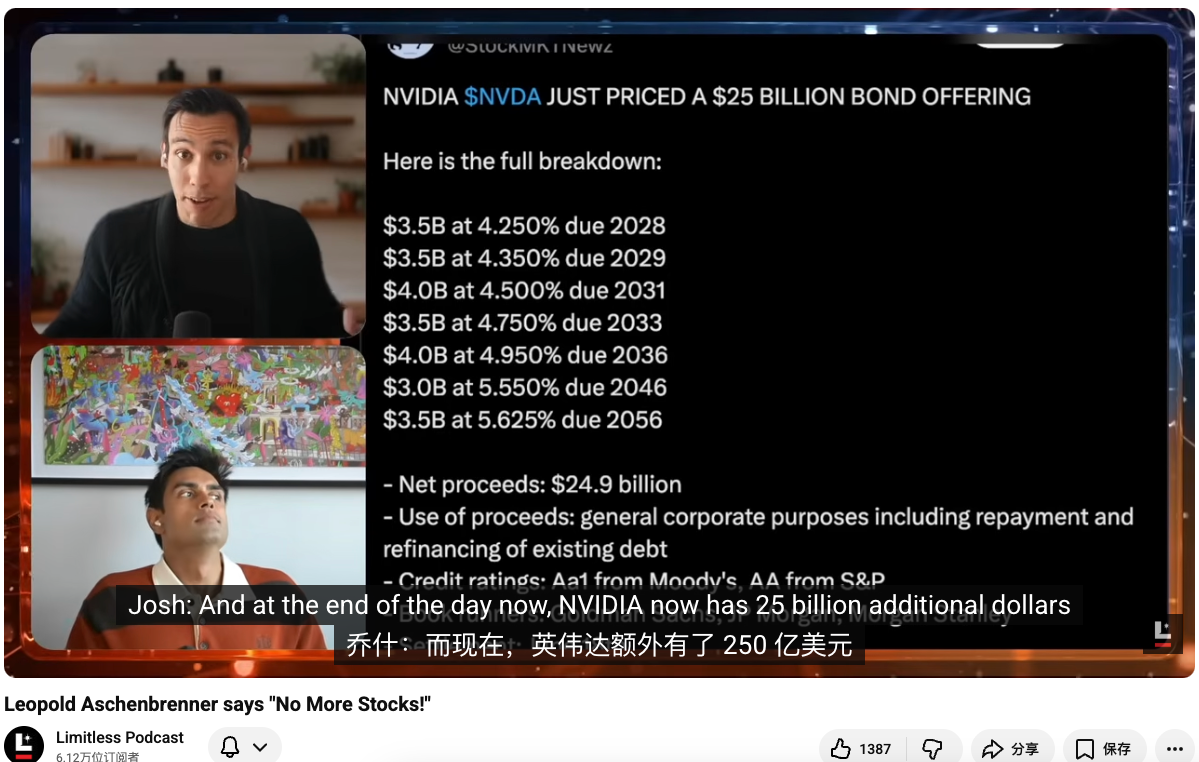

Later, we dug up some new clues, the most important of which is that NVIDIA just raised $25 billion through bond financing. This means it is not just using its cash on hand but is leveraging externally. So the question arises: Why would a globally highly profitable company with the highest profit margin and cash flow still need to borrow $25 billion?

Josh Kale:

Moreover, they initially planned to raise only $20 billion but ended up expanding it to $25 billion, with subscriptions exceeding 3 times. In the last time we discussed this investment portfolio, we said not to worry about bubbles because although these companies have massive capital expenditures, their income is sufficiently high, and theoretically, they could fully sustain expansion through their balance sheets.

However, this is the first time NVIDIA has clearly financed externally since 2021, rather than directly using its cash on hand. I remember they currently have over $12 billion in cash. When all these aspects come together, there is a strange tension: on one hand, Leopold is shorting, and on the other, NVIDIA, which clearly has endless cash and profits, is still issuing bonds. So what has really happened?

Decomposing NVIDIA's Bond Financing

Josh Kale: Ejaaz, can you help us break down this transaction itself? Because this is not ordinary financing but rather bond issuance. After all, now NVIDIA's balance sheet has an additional $25 billion, and the interest rate seems to be quite low.

Ejaaz Ahamadeen:

Let me present both explanations. NVIDIA originally had about $13.7 billion in cash on hand, meaning it could fully spend its own money. So why does it still need to finance externally? A simple analogy is buying a house. Many people would still choose to take out a loan even if they have the full amount because they can use their capital for other things, and if the borrowing cost is low enough, it is actually more cost-effective.

These past few years, the interest rate environment has not been friendly, but if you are NVIDIA, one of the most valuable and sought-after companies globally, you can borrow money under very good conditions. This $25 billion bond financing has a maturity ranging from 2 to 30 years, which can almost be considered very cheap money, with interest rates now nearing U.S. Treasury yields.

Additionally, this financing was apparently oversubscribed 4 times, in other words, $85 billion in the market wanted to rush into this $25 billion allotment, meaning NVIDIA could practically choose its investors at will. If we only look at the official explanation, NVIDIA states that this is primarily a financial arrangement to repay and refinance part of the existing debt. Google did something very similar a few weeks ago and also did it back in February this year. So you could certainly accept this explanation and see it as financial optimization.

However, it is also hard to ignore the other side: In the past month and a half, NVIDIA, Amazon, Google, and a few other massive cloud providers have almost all been increasing external financing. Some have issued bonds, while others have sold stock. Leopold's view may not be entirely unfounded; could this signal that the bubble has begun to lose steam, and the house of cards is starting to wobble? Yet, if you look at the financial structure alone, this event does not clearly point to danger.

Josh Kale:

I see it the same way. $9 billion to short NVIDIA is indeed a very large position. However, in our research, we also noticed another thing: on May 18, NVIDIA's board authorized an additional $80 billion in stock buybacks, and raised its dividend from $0.01 per share to $0.25, effectively increasing it by 25 times.

If a company, in the same month, conducts large-scale stock buybacks, significantly increases its dividends, and borrows money, it is obviously not because it lacks cash that it borrows. A more reasonable explanation is that this is cheap money, and the financing methods in this AI market are showing slight changes. Everyone wants to participate in these capital operations, and NVIDIA realizes that issuing bonds to raise money may actually be cheaper than other financing methods, so they simply went with the flow and did it. At least for now, NVIDIA itself is still doing very well.

Why He Changed Positions

Josh Kale: This brings us back to another question. What is Leopold really thinking? Why did his judgment change? The stock price chart you just showed also indicates that NVIDIA's recent performance has indeed not been particularly strong, but it has not dropped much either. It is still close to $5 trillion market cap, only down 7% in a month, which is nothing in the context of other AI stocks soaring.

Ejaaz Ahamadeen:

I don't think NVIDIA will disappear. Its GPUs, including the newly launched CPU product line just a few weeks ago, I believe will perform very well. AI product demand is now exponentially excessive, and the core machine suppliers that can handle that demand are mainly still NVIDIA.

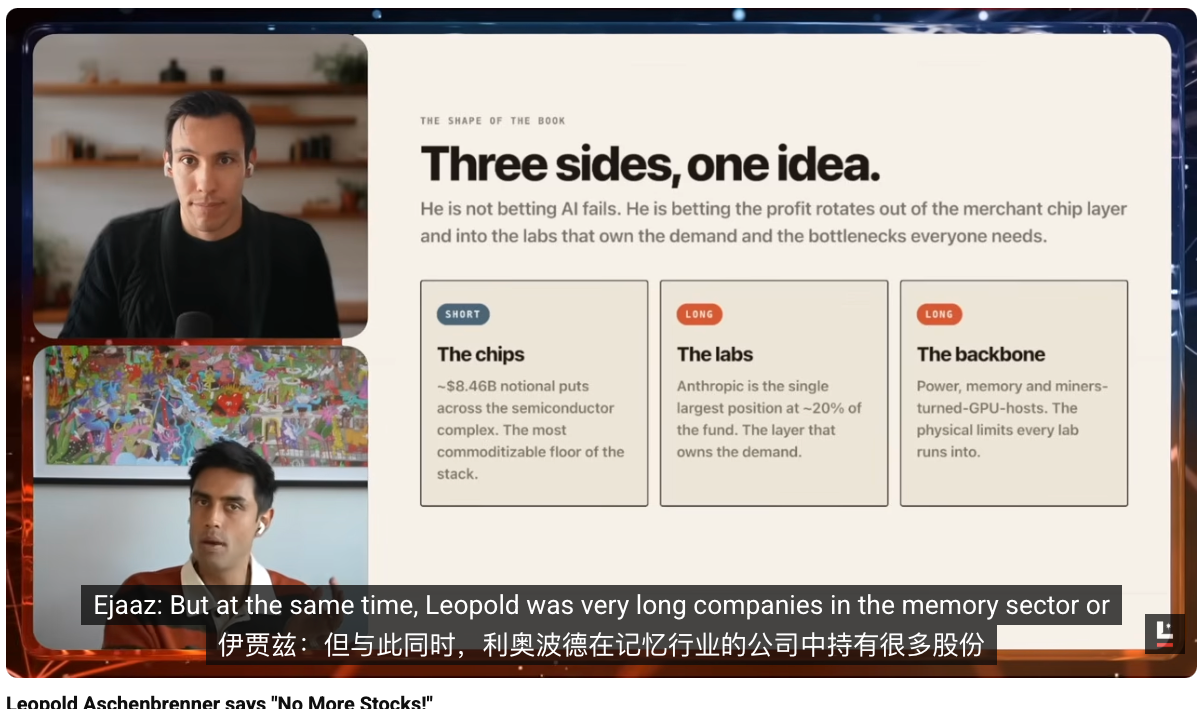

But I do feel that the classic 'selling shovels' trade in AI has become too crowded, and Leopold's recent position change conveys this signal. Just looking at his recent 13F, his bearish positions are clearly leaning bearish on the semiconductor sector, such as NVIDIA, ASML, Oracle, and other infrastructure-level companies.

But at the same time, he has heavily invested in memory, electricity, and new cloud directions. This indicates that his judgment is not that AI infrastructure has peaked, but that certain levels in the infrastructure stack, especially semiconductors and traditional hot stocks, have become too crowded.

If the question becomes where the funds will flow next, there are two answers. The first is the most direct, flowing towards the next real infrastructure bottlenecks, which are electricity, memory, and data center networks; the second answer is the mysterious investment that was exposed a few weeks ago.

Unexpected Exposure of Anthropic Position

Josh Kale:

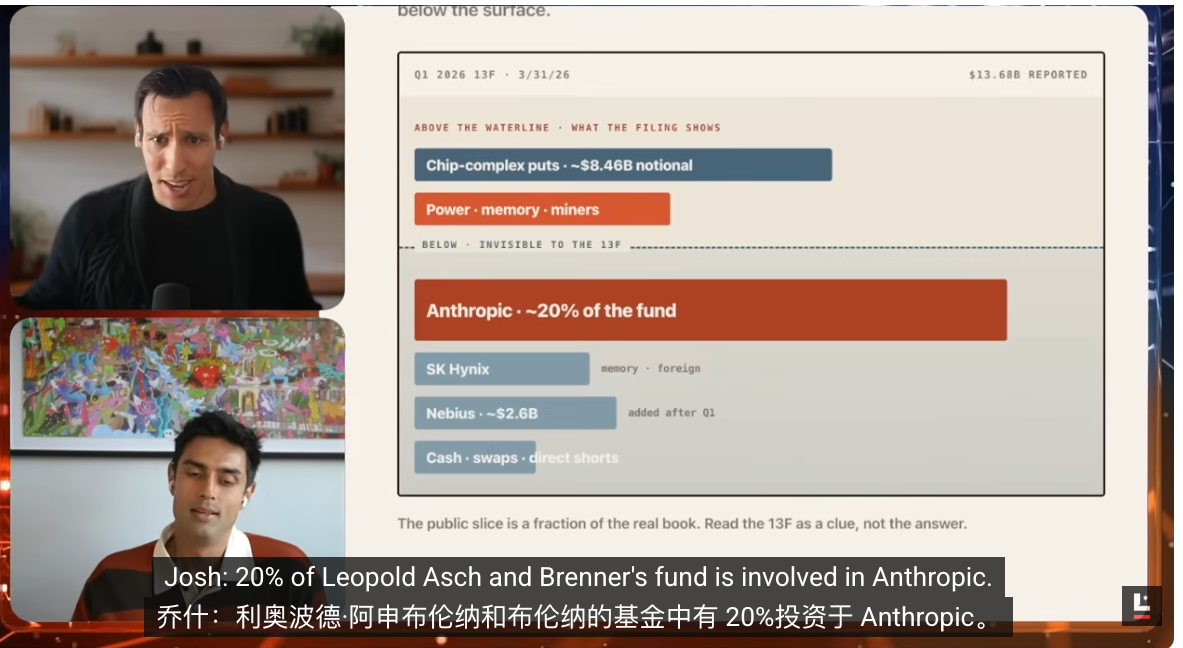

This is the most surprising for me. Just yesterday I heard you mention it, and my first reaction was impossible. Could it be that Leopold's fund "Situational Awareness" has 20% allocated to shares of Anthropic? Rumors are circulating that this company accounts for about one-fifth of Leopold's fund position, as confirmed by reports from the Wall Street Journal and other media, along with sources very close to the transaction.

This has become a card in his portfolio that the market did not expect at all. Since a 13F can only disclose publicly traded holdings and will not disclose private equity, and Anthropic is precisely a significant block of unlisted equity. It is precisely for this reason that everyone is starting to understand why the valuation of his portfolio is set so high at $20 billion.

If 20% of his fund is in Anthropic, and he likely invested in it at the beginning of 2025, then the return on that investment could be equivalent to seven years' worth of gains. This change will significantly adjust our understanding of his entire investment portfolio.

Ejaaz Ahamadeen:

Yes. His first investment into Anthropic through private channels or the fund was probably in March 2025 when Anthropic was valued at around $60 billion. Now according to the latest valuation round, it has been set at $965 billion.

This is close to a 15-fold increase. Based on the algorithms we showed in today's program, the liquidity value disclosed in his most recent 13F filing is $13.7 billion, and if you add the Anthropic position mentioned in the Wall Street Journal, that could increase by another $7 billion, bringing the total fund management scale to $20 billion.

How exaggerated is this? A top investor like Bill Ackman, who has been in the market for three to four decades, also has a fund size of about $20 billion. Leopold has only been in this game for a year and a half, and he is only 24 years old, with practically no significant investment experience.

However, he has made some extremely remarkable judgments, and the crazy part is that he actually wrote all of this out in advance. He published a 65-page long document on AI called "Situational Awareness" when he launched his fund a year and a half ago, explaining the entire set of logic almost completely, including how funds would rotate from semiconductors and parts of the infrastructure segment to other bottleneck constraints. Now the market is developing along this line, which is truly astonishing.

The Next Wave of Infrastructure Market

Ejaaz Ahamadeen:

So this also tells me where the next money will flow. If he is cautious about NVIDIA, then funds will flow to electricity and memory; at the same time, he wants to invest directly in the "mine" itself rather than continue just buying "shovels," and Anthropic is his favorite mine.

Josh Kale:

This indeed looks like a new trend, and he still seems to be ahead of most people. In the past 12 months, everyone has been trying to find where the bottleneck in AI is, whether it be rare metals, memory, RAM, etc.; the market has chased after these sectors in a wave. These judgments are not incorrect, as that wave of the market indeed happened.

But looking at it now, those sectors seen as bottlenecks are gradually aligning with reasonable valuations. People have begun to better understand these companies' business models, market spaces, and future revenues, so a lot of value has already been priced in. In the next round, we are more concerned about where the subsequent funds will continue to flow.

You just mentioned land, electricity, housing, and physical infrastructure; this direction indeed seems correct. Because if we think about what is truly important for AI, the answer increasingly resembles the capability for physical construction. Look at xAI or, more accurately, look at SpaceX, which has already gone public; its core revenue is not rocket sales but AI infrastructure construction.

Then look at its transactions with Anthropic and Google; the value they bring has already exceeded the total sum of Starlink, Starship, and the entire satellite business. There is clearly huge demand and significant value embedded here. So the question becomes, who can truly bring these things to fruition?

SpaceX is clearly one answer. Last night, its stock price reached $230, corresponding to an approximate valuation of $3.1 trillion. We will dedicate an episode to SpaceX this week because its price movement has been so extravagant, having just completed an acquisition of Cursor, now valued at $3 trillion, with Elon earning in one day more than Warren Buffett has throughout his entire career.

Who Will Benefit from the Next Round of Dividends

Josh Kale: We are interested in which companies are best at developing this hardware infrastructure, skilled at creating those 'machines that make machines.' Given Leopold's direction and the overarching trend, we believe the funds will flow this way next. So Ejaaz, in reality, which companies will this rotation end up benefiting?

Ejaaz Ahamadeen:

Many will be those infrastructure companies that don’t sound sexy. The name that has been frequently mentioned in the last month is Marvell. Just a few weeks ago, at Computex in Taiwan, Jensen Huang directly stated on stage that this would be the next trillion-dollar company.

And just three months prior to this statement, NVIDIA had just invested $1.5 billion in Marvell. I find it hard to distinguish whether this counts as insider trading or market manipulation, because after he made this statement, the stock price surged by 70%.

I think making a direct judgment that AI infrastructure has peaked is actually quite easy; however, if you compare it to historical financial crises, such as 2008, the taste of high leverage, financial engineering, and systemic manipulation hasn’t fully appeared in this round.

The two critical differences are as follows. First, the products these companies produce today have genuine buyers. Neither the internet bubble nor the financial crisis had such solid real demand. Second, constrained by the laws of physics, we currently cannot excessively leverage because the entire system is constrained by human resources and construction capabilities.

No matter how much money you raise, you can’t quickly finish building data centers, expand enough memory chip capacity, or immediately upgrade the grid and related infrastructure. There aren’t enough hands on the ground, and approvals, regulations, and various procedures are holding you back.

So on the contrary, I think this gives investors an advantage. Since you know that the hottest chips and the 'selling shovels' trade are too crowded, the money will next flow to electricity, data networks, such as companies like Astera Labs, and then to other related sectors. What you really need to think about is when these contracts will start to be realized, when these fabs will genuinely become operational, when SpaceX's rockets will finally launch AI satellites into space, and even when we can begin utilizing solar energy to train AI models.

The timeline dictates the rhythm of betting. At least I am investing under this framework, of course, this is not investment advice. The reason I view it this way is that over the past year and a half, we have seen firsthand how funds have shifted from general AI stocks to semiconductor and infrastructure deals.

Josh Kale:

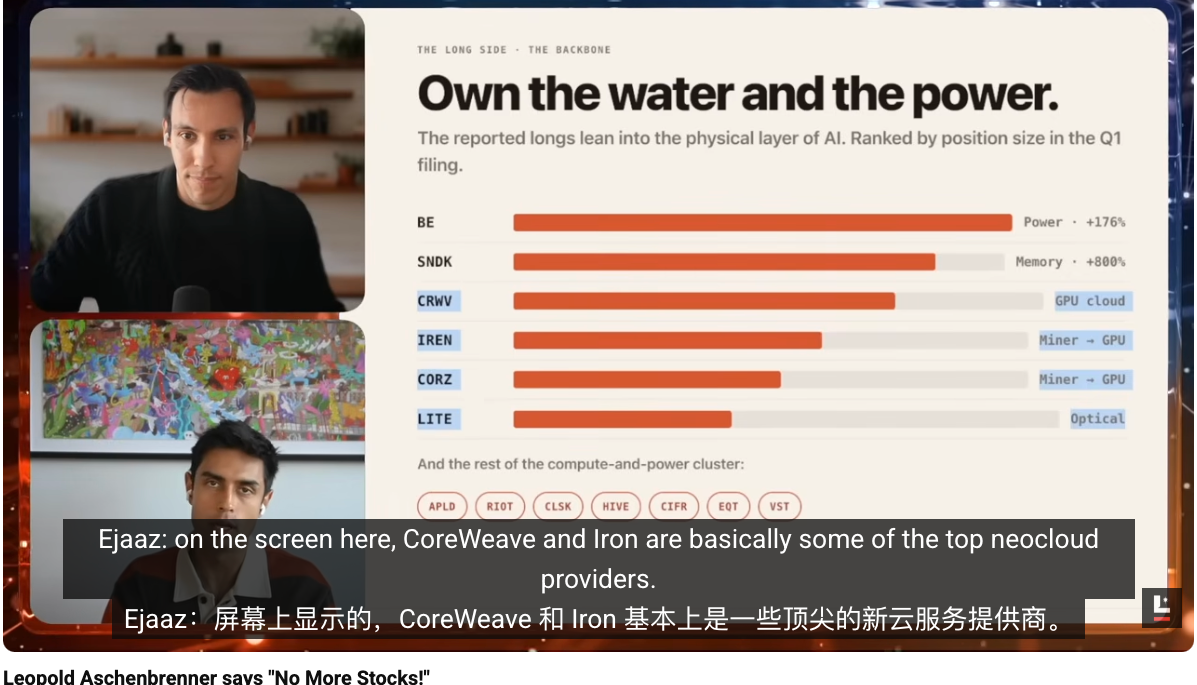

If we continue to look at this portfolio chart, you might find that this story has already been clearly written into his holding structure. By category, what is his largest position? It is electricity and energy. Next is memory, followed by cloud and GPU miners, which are the most solid infrastructure.

He wants to hold companies like CoreWeave, which are new types of cloud providers, as well as miners that have pivoted to cloud computing. What he wants to own are these physical infrastructures because he believes this is where the real bottlenecks lie. You also mentioned that there are many finer aspects, such as actual construction, hardware manufacturing, and the construction of data centers themselves, which are all greatly challenging.

If you had to identify where the largest bottleneck is, even approval permits could be considered one. Who is working to solve these issues? SpaceX aims to move data centers into space, while Tesla wants to use humanoid robots to address workforce issues. But both of these things are still far away. In the short to medium term, there are a lot of blank opportunities, which is precisely the direction Leopold is betting on.

Advantages of Optical Modules and Fiber Optics

Josh Kale: I also want to add a detail we didn’t expand on earlier. For those who want to dig deeper and find more excess returns, many of his clues are actually hidden in optics and deeper technology stacks. Ejaaz, you have been researching this recently; can you share his thoughts?

Ejaaz Ahamadeen:

If you look at his positions on the screen, CoreWeave and Iron are essentially top-tier new cloud service providers. Simply put, they are somewhat like Amazon Web Services, except AWS provides cloud services to internet companies, while these companies provide ready-made GPU infrastructure to AI firms.

They help you set up the GPU, networks, and deployments, so AI companies don't have to worry about the bottom-layer infrastructure and can directly train models and access computational power. CoreWeave and Iron have been among his largest concentrated positions since he began building his stake, bringing the highest returns.

And significantly, he still keeps these two companies as his largest positions today. This also indicates one issue: in his view, this transaction has not finished at all. Furthermore, he also privately invested in Core Scientific, a company that can help release CoreWeave’s infrastructure supply capacity. In a sense, he has added yet another layer of leverage to CoreWeave.

Aside from these, look at companies like Coherent and Lumentum; they are fundamentally suppliers related to fiber and optical connections. To explain in simplest terms, for semiconductor and GPU communication, traditional methods usually rely on a lot of copper wires. The problem is, as GPU scales grow larger, copper wires get hotter, energy loss increases, and efficiency deteriorates. Under these circumstances, fiber optics will become the next upgrade direction. It can achieve faster data transmission, greater cost efficiency, and allow companies providing inference and training computational power to earn more money. So you will find that what he has always bet on has been very infrastructure-oriented, investing in both these optical companies and electricity-related companies. It may sound less attractive, but in my opinion, this is where the funds are genuinely getting allocated right now.

Josh Kale:

The aspect of copper is also interesting to me because I only recently realized how critical it is for short-distance data transmission. In many high-bandwidth short-distance transmission scenarios, copper is almost the only material people really want to use. Only when it starts to become unsuitable, such as when the distance is too great or the heat is too high, will it switch to fiber optics, thus the current market demand for the combination of copper and fiber optics is very strong. This is why observing this copper trade is very intriguing. Copper futures have recently performed strongly, essentially because everyone needs it; it is the critical foundational material for short-distance high-bandwidth transmission, while fiber optics is the next step.

Thinking from a deeper level, the material aspect has always been fascinating. The very core need for intelligence at the most foundational level is which raw materials are required. Copper is one, lithium is another, and there are many others. We really should dedicate an entire episode to materials. Perhaps Leopold hasn't arrived at that layer yet, but we might be able to see the next round of rotation ahead of time.

Josh Kale:

If we delve even deeper into the stack, we could go directly to copper mines to see how these materials are produced. But to return to the core judgment, I believe the next round of rotation will indeed shift from those seemingly smaller bottlenecks to the truly difficult matters, namely hardware and large data center construction.

Whoever has the ability to build data centers will make the money. We have already seen how much money SpaceX earns because of the booming demand for data centers. Whoever can bring more data centers online faster, provide sufficient electricity and GPUs, will make the most money. This is fundamentally the direction Leopold is currently betting on.

Is the Bubble Emerging?

Josh Kale: To summarize, we don’t believe we have entered the bubble-bursting phase yet. Leopold's positions seem more like a rotation rather than a full retreat. So, should we still follow him?

Ejaaz Ahamadeen:

I admit that when I first saw his 13F, my immediate reaction was that this guy is actually shorting the world's most valuable company with demand projected through 2029; that’s too outrageous. But now seeing this financing, I start to think that if NVIDIA continues to add external debt in the future, or even potentially sell shares, if this trend continues, Leopold might again be right.

If that’s the case, his fund could ultimately surpass the world's top traders and best investment funds. He has indeed been winning continuously, and it is hard not to respect that.

Josh Kale:

However, there is also a very important point. Throughout his past life, he has almost only been going long and has never truly experienced the trial of large-scale selling. We previously mentioned Bill Ackman; achieving 30 times returns and surviving in the market for 30 years is actually two different things.

If he can truly sustain this growth while learning when to hit the sell button, how to manage risk, and how to hedge for protection, it becomes even more daunting. We are starting to see the beginnings of this capability. That $9 billion short was not achieved by directly shorting $9 billion in cash but through options and leverage, not on a one-to-one naked short. Regardless, this is definitely worth continuing to observe.

Energy is the Core Bet

Josh Kale: If you had to choose one stock from his entire investment portfolio that you personally want to buy, which one would it be?

My answer would be energy stocks. I have always been optimistic about energy because even if AI demand slows down, energy itself is still a global necessity, and this demand will only increase. Even ignoring AI completely, we need more energy, more electricity. Companies like Bloom Energy that can enhance power supply and delivery capacity are the directions I am most excited about because they represent more of a hedging bet. The single persistent trend in any scenario will be our demand for energy, electricity, and power — these are the companies I am most willing to go long on for the long term.

Ejaaz Ahamadeen:

This answer is a bit of a cheat. The companies I really want to follow are the ones where Jensen is investing, which also intersect with Leopold's logic. The stock I am closest to following right now is Marvell. Although it is not a company publicly held by Leopold, it aligns very well with his bets on fiber optics and power, and Jensen has already invested $1.5 billion in it.

I have observed a phenomenon: as long as Jensen invests in a company through NVIDIA, whether it's Intel, CoreWeave, or others, that stock tends to rise subsequently. Therefore, my current position is approximately here. I also own some CoreWeave because both Jensen and Leopold are extremely optimistic about it.

Josh Kale:

Marvell has already surged 270% in the past six months. This might indeed be a good rule of thumb: people like Jensen, and even those like Trump who have enormous influence, if they publicly say to buy a certain stock, many times you might really want to take a serious look at it.

History has proven multiple times that such signals often have a significant potential for realization. Be it Intel or Marvell, these instances show, on one hand, that they genuinely know what they are talking about, and on the other, they have the capability to influence the outcomes for these companies. So this segment of the market is truly wild.

I hope it continues. It does indeed seem likely to continue based on what we see now. At least we are still leaning bullish, still optimistic, and will continue to judge changes daily.

Josh Kale: Do you have any final thoughts regarding updates on Leopold's investment portfolio?

Ejaaz Ahamadeen:

I would actually love to hear how those who hold skeptical views feel. If you listen to our analysis just now and feel that we are completely wrong or there is some misunderstanding, please feel free to point it out.

Yesterday I stared at the news of NVIDIA's $25 billion financing for a long time, intending to find faults. But if you look at it purely from the financial logic perspective, it does indeed make sense. Why not borrow this almost risk-free cheap money? Borrowing money to expand is clearly more reasonable than selling one's shares, as this allows you to retain more of your future earnings.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。