Original | Odaily Planet Daily (@OdailyChina)

Author|Azuma (@azuma_eth)

On June 18, Beijing time, the Federal Reserve officially announced the latest interest rate decision. There was no suspense; the federal funds rate remained unchanged within the established range, consistent with prior market expectations.

In recent weeks, there has been almost no controversy in the market pricing of interest rate paths, and the market had long fully priced this in. Therefore, the real focus of this interest rate decision was not on "whether to cut rates," but on how the newly appointed Federal Reserve Chair Waller would initiate his first policy communication —— this is Waller's first FOMC meeting since taking over as chair, and it is the market's first opportunity to observe how he will shape the framework for monetary policy communication in the coming years.

The Dot Plot is Still There, but Waller is Absent

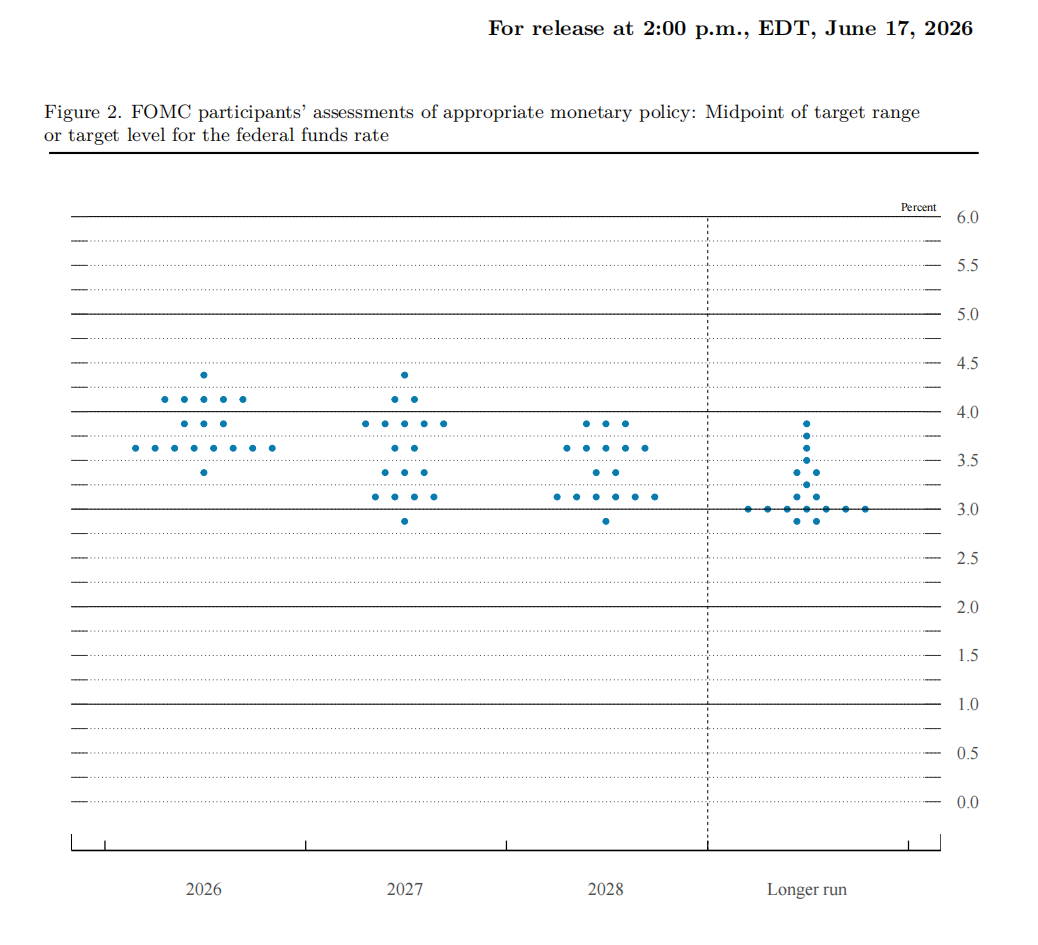

The most discussed change in this meeting came from the economic forecasts and the structure of the dot plot itself.

- Odaily Note: The so-called "Dot Plot" is the interest rate prediction tool released quarterly by the Federal Reserve, where each point represents an FOMC member's expectation for future interest rate levels. Although these predictions are not formal policy commitments, they have long been viewed by the market as an important reference for interpreting the Federal Reserve's policy direction as they reflect the decision-makers' overall judgment of economic and inflation prospects.

In the latest FOMC economic forecast, only 18 out of 19 Federal Reserve officials submitted a dot plot prediction. Among them, 1 believes that a cumulative rate increase of 75 basis points should occur for the remainder of 2026, 5 believe a cumulative increase of 50 basis points is warranted, 3 believe a cumulative increase of 25 basis points is appropriate, 8 believe rates should remain unchanged, 1 believes a cumulative decrease of 25 basis points should occur, and 1 was absent.

Waller also admitted in the subsequent press conference that it was he who did not submit a rate prediction. Waller explained, "I did not put forth any of my own predictions, which is consistent with my long-held view, at least in terms of its current structure."

In contrast to his predecessor Powell, who had a highly transparent and frequent communication style, Waller has long been seen as a representative of the "less is more" approach. He has repeatedly expressed doubts about the "effectiveness of the dot plot," "overly forward guidance," and "frequent signaling of policy." In Waller's view, the Federal Reserve does not need to tell the market what each step will be in the future but should make decisions based on real-time economic data.

Although the market speculated that Waller might push for reforms to the dot plot mechanism, even potentially abolishing it, the dot plot was not directly canceled according to this meeting. However, Waller's absence still sent a clear signal — the Federal Reserve is downplaying the guiding significance of the dot plot.

The Implicit Shift in the Federal Reserve's Communication Framework

Waller also stated at the press conference that in the future there will be a series of reform measures implemented at the Federal Reserve, including the establishment of multiple special task forces, exploring more open data collection methods, and studying improvements to the Federal Reserve's existing statistical indicator system.

During the subsequent Q&A session, when asked repeatedly by reporters whether there would be a rate hike next, and whether the current rate was restrictive, Waller repeatedly refused to provide clear guidance.

For over a decade, one of the Federal Reserve's core capabilities has been to continuously reduce market uncertainty through the dot plot, SEP (Summary of Economic Projections), and press conferences. The reason the market closely monitors the various dynamics of the Federal Reserve is fundamentally that it provides a "predictable path."

However, Waller's statements are changing this logic. Clearly, Waller emphasizes data dependence, decision-making at successive meetings, and maintains a more restrained expression regarding future paths.

If this tendency continues, the market will face a structural change — the Federal Reserve will no longer try to "explain the future," but will only describe "current judgments." This will directly weaken the certainty function of forward guidance.

Rate Hike Expectations Rise, Market Risk Appetite Declines

After the interest rate decision was announced, the market quickly began to reprice the policy path.

Following Waller's statement that "the central bank will not tolerate high inflation," the market began to reassess the upper bound of the Federal Reserve's policy response function, namely whether a more aggressive tightening possibility existed under the circumstances that inflation has not notably receded.

This change was first reflected in short-term assets.

Traders began to rebet on a higher terminal interest rate path, with some interest rate futures contracts pricing in the possibility of another rate hike as early as around October, while not ruling out the tail risk of a more aggressive path. Polymarket probability data also moved upwards, reflecting that the market's pricing for the "reopening of the rate hike window" is now opening.

The U.S. stock market notably retreated after the decision, with all three major indices collectively closing lower; the S&P 500 (-1.2%) and the Nasdaq (-1.3%) both fell more than 1%, with technology stocks leading the market decline, and market risk appetite significantly cooled.

Structurally, this round of adjustment is not driven by a single factor "interest rate increase shock," but rather a more typical triple repricing:

- Short-term interest rates rise: the rate hike path is reopened;

- Risk assets withdraw: sensitivity of valuations to interest rates amplifies;

- U.S. dollar strengthens + yield curve fluctuation: reflecting rising policy uncertainty.

It is noteworthy that the market is not simply trading "economic weakness" or "disappearance of rate cut expectations," but is engaging in a more complex logic — under Waller's new communication framework, inflation constraints are being raised again, and the "upside tail risks" of the policy path are becoming more real.

In other words, if inflation does not quickly recede, will the Federal Reserve shift towards tightening earlier and more aggressively than the market originally expected?

Waller's Shift May Have Just Begun

In summary, looking only at the outcome of this meeting, the Federal Reserve did not make a radical shift; the interest rate remained unchanged, the dot plot is still there, and the system continues to operate. However, if the focus shifts from "policy path" to "communication method," the changes have begun to appear.

Waller's debut resembles a signal test; he did not abolish old tools but also did not rely entirely on them; he chose to "weaken effects, reduce weight."

From a longer-term perspective, the biggest question left by this debut is not "Will the Federal Reserve hike rates next?" but rather "How will the market reprice the world when the Federal Reserve no longer hints at the market path?"

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。