Throughout June, major exchanges have been intensively laying out U.S. stock products. As one of the earliest and most aggressive platforms in this space, Bitget has also launched its own RWA platform, Reality, and made significant upgrades to its U.S. stock products. Today, we invite Bitget CEO Gracy to discuss this trend and other hot industry topics.

Bitget has previously integrated stock token solutions like Ondo; now it has chosen to switch to Reality for U.S. stock 2.0. What is the biggest difference between the two? What problems does this upgrade aim to solve?

Gracy: We started collaborating with Ondo in the third quarter of last year, capturing nearly 90% of the market share of their issued stock tokens at one point. Not just with Ondo, we have also collaborated with xStocks to launch U.S. stock tokens. However, the most frequent feedback we received from users during this process was that the liquidity was not good enough, and the mechanisms for dividends and stock splits were not clear or transparent enough.

Therefore, we decided to personally address this issue. Reality is our compliant RWA protocol, and its biggest difference is that it directly interfaces with the U.S. licensed broker, Alpaca, allowing orders to flow directly to NASDAQ and the NYSE. Simply put, when trading Reality’s U.S. stock rTokens, users will buy at the same price that Apple and Tesla are trading for in the U.S. stock market, with liquidity directly comparable to traditional brokers.

Additionally, Reality also resolves the pain points related to dividends and stock splits. Cash dividends will automatically convert into USDT airdropped to users, and stock splits can also synchronize 1:1, avoiding any disconnection between token price and the real stock price.

Will users in the future be able to use stock tokens like Nvidia and Tesla as margin to continue trading BTC, ETH, or other contracts?

Gracy: This feature has already been launched on June 4th. This is also the core reason why we insist on tokenization rather than just “broker direct connections.” Users who buy rNVDA, which is the Nvidia rToken, can directly use it as margin for contracts on Bitget, and it can be transferred via public chains like Arbitrum and Morph for use in DeFi scenarios. What we want to do is truly activate the U.S. stock tokens that users have in hand and enhance overall capital efficiency.

Recently, several exchanges have been upgrading their U.S. stock-related products. What are the core differences of Bitget’s recent upgrade compared to other platforms' stock products?

Gracy: It is true that many platforms have been laying out U.S. stocks recently, but after looking around, I found that most competitors are still focused on “broker direct connections.” This means that users deposit stablecoins and then open accounts with traditional brokers for trading. Bitget recently launched U.S. stock 2.0, one of the important upgrade points is that we chose a more crypto-native path, which is RWA stock tokens.

The core difference is that stocks bought through “broker direct connections” usually can only sit in the user's U.S. stock account. However, at Bitget, the rTokens issued through Reality are truly on-chain assets, and we have already integrated with the Arbitrum and Morph public chains. This means that users can not only use them as collateral internally on Bitget but can also withdraw them to their wallets and, in the future, even stake them to earn yields in DeFi protocols.

We specifically solved two long-standing issues in the industry. The first is liquidity: our orders flow directly to NASDAQ and the NYSE, with prices, order books, and depths synchronizing with the real market. Secondly, dividend distributions and stock splits: cash dividends will directly be converted into USDT and automatically airdropped, and stock splits will also be synchronized 1:1, avoiding disconnection between token prices and real stock prices.

More importantly, in the context of UEX, these rTokens can truly play a higher capital efficiency. For example, users holding rNVDA, the Nvidia rToken, can directly use it as margin to continue trading BTC or ETH contracts, allowing the same asset to function in two markets simultaneously. This is a more native on-chain experience, which traditional broker direct connections cannot offer.

A long-standing criticism of stock tokens is: What exactly are users buying – a tokenized representation of real stock rights or merely a price tracking tool? How will Reality prove to users that the underlying stocks exist, are auditable, and traceable? Will there be provisions for reserve proof, custodian disclosures, audit reports, and broker structural clarifications in the future?

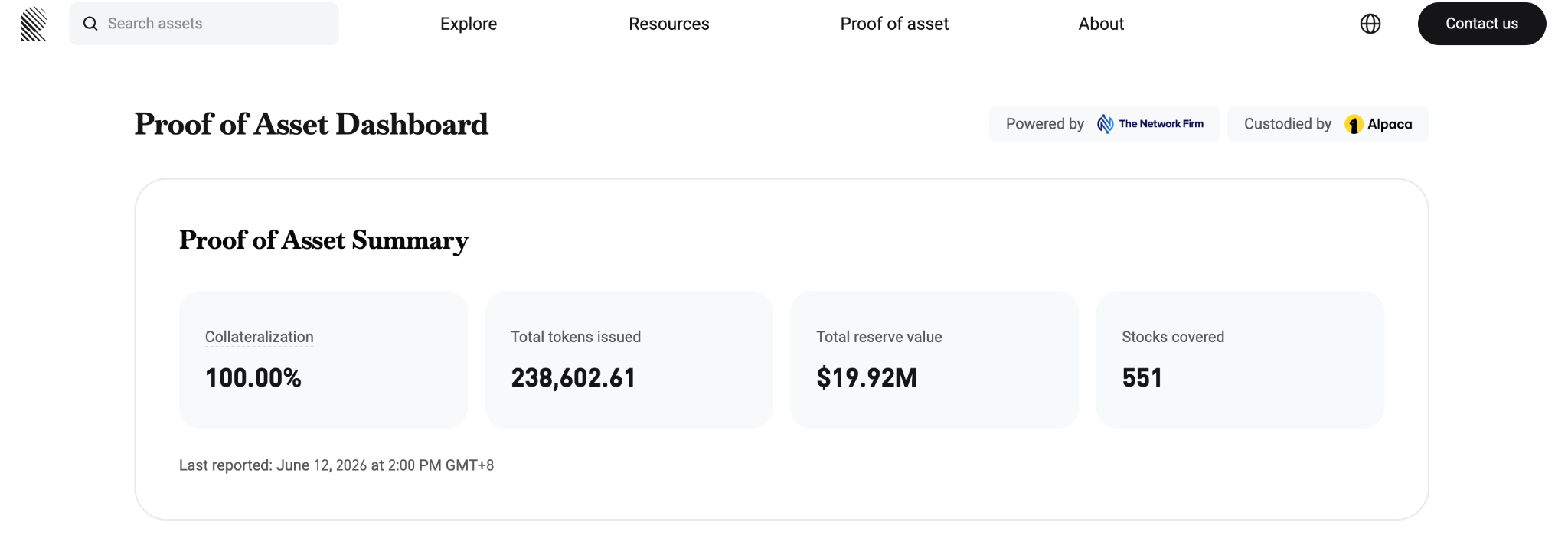

Gracy: That’s a very good question. Indeed, if it's just a “synthetic asset” that tracks price, it lacks substance. Reality's rToken has real underlying asset support. Our underlying stocks are held by the U.S. licensed broker Alpaca in an independent SPV, completely isolated from the platform's own assets. We have achieved 1:1 full reserves.

At the same time, we will have third-party U.S. licensed auditing firms conduct daily audits. The Reality official website has already launched a real-time audit dashboard, where users can check the reserve ratios at any time. After the CPA licensed auditing firm is expected to finish the report in August, we will also synchronize that audit report into this dashboard. Additionally, with Bitget having more than $300 million in a user protection fund as a safety net, we can say this forms a threefold safeguard.

(Source: Reality PoR dashboard screenshot at 2:00 PM GMT+8 on June 12, 2026)

If a stock experiences a split, merger, special dividend, acquisition, or delisting in the future, how will Reality handle it?

Gracy: Our handling of corporate actions is indeed where we are stronger compared to many products in the market. For example, looking at splits, such as Netflix's 1:10 split last year, some platforms' tokens did not synchronize rebase, causing some stock token prices to be ten times higher than the actual stock price, which can confuse users. But in Reality, splits will automatically synchronize. A user’s 1 token will increase to 10 tokens, with the unit price reflecting the real stock price, ensuring that total asset value remains unaffected.

Cash dividends will also directly convert into USDT and automatically airdrop into the Bitget account to ensure clarity and transparency. Whether for retail investors or for institutions we support in the future, particularly for those needing hedging, valuation, clearing, and portfolio management, a structure of “price is price, dividends are dividends” is closer to the usage habits of traditional financial systems.

Over the past few years, the main narrative for crypto users has revolved around BTC, ETH, DeFi, NFT, Meme, L2, and public chain competition. But recently, it’s clear that assets and companies like AI, U.S. stocks, Nvidia, OpenAI, SpaceX have attracted a lot of capital and attention.

Have you observed this migration in your platform data? What percentage of non-cryptocurrency trading accounts for Bitget currently? What is the growth rate?

Gracy: We have indeed observed this trend. As early as late 2024 and early 2025, we noticed that altcoins were performing poorly, while users' enthusiasm for AI, U.S. stocks, gold, and silver commodities began to rise. This is why I proposed the vision of UEX (Universal Exchange, a panoramic exchange) last September.

In December last year, our cumulative trading volume for U.S. stock perpetual contracts exceeded $10 billion, ranking second globally. Early this year, our TradFi segment, including gold and forex, also first crossed a daily trading volume of $2 billion. Currently, 40% of Bitget's trading volume comes from non-crypto assets.

The reason is simple: capital is profit-seeking. Wherever there is more certain growth and wealth effects, funds will flow there. The AI giants in the U.S. stock market have delivered tangible revenues and profits, while many crypto projects are still in the storytelling phase.

As for whether this trend will reverse in the future, I don’t think it's a zero-sum game. Crypto assets, like BTC as digital gold, can complement U.S. tech stocks within users' investment portfolios. What we aim to do is enable users to seamlessly buy different types of assets using stablecoins like USDT and USDC within a single account.

From a macro perspective, U.S. stocks, particularly AI-related assets, have seen significant growth over the past six months, with many assets increasing tenfold. For many crypto users, they may only start paying attention to U.S. stocks after the profit effects have diminished in the crypto market. Entering the market at this point may instead involve the risk of chasing highs.

What is your view of the current position of U.S. stocks? For users who have just transitioned from crypto to U.S. stock trading, what is the most important mistake they should avoid?

Gracy: The biggest pain point for crypto users is capital efficiency and asset fragmentation. When funds are held in an exchange earning interest, they risk missing out on stock market gains; when they rush to open accounts with traditional brokers, it becomes difficult to return to the exchange for contract trading. Our rToken product is designed to address this issue: when users buy U.S. stocks, their holdings can still be used as contract margin, keeping their capital active.

Whether U.S. stocks are expensive depends on what time dimension users are looking at. Crypto users participating in U.S. stocks must first recognize that, just like crypto assets, the U.S. stock market is not a one-way street. Especially with popular sectors like AI, semiconductors, and tech stocks, the increases have been significant recently, and short-term volatility and valuation pressure need to be assessed comprehensively.

Putting aside my identity as the CEO, as someone managing my personal account, I recently shared on Twitter some observations about the bottom price of Bitcoin in this cycle, and I received skepticism from many users saying, "As an exchange CEO, you shouldn't be bearish on your own business." But I want to clarify that every industry has its cycles. I am merely presenting the data and logic to highlight possible cyclical changes. We certainly have a long-term optimistic view of the crypto industry and believe that tokenized assets will bring new opportunities; however, being optimistic long-term does not mean being bullish at all times. After all, trading opportunities arise from volatility, and for increasingly mature investors, both rises and falls can represent opportunities.

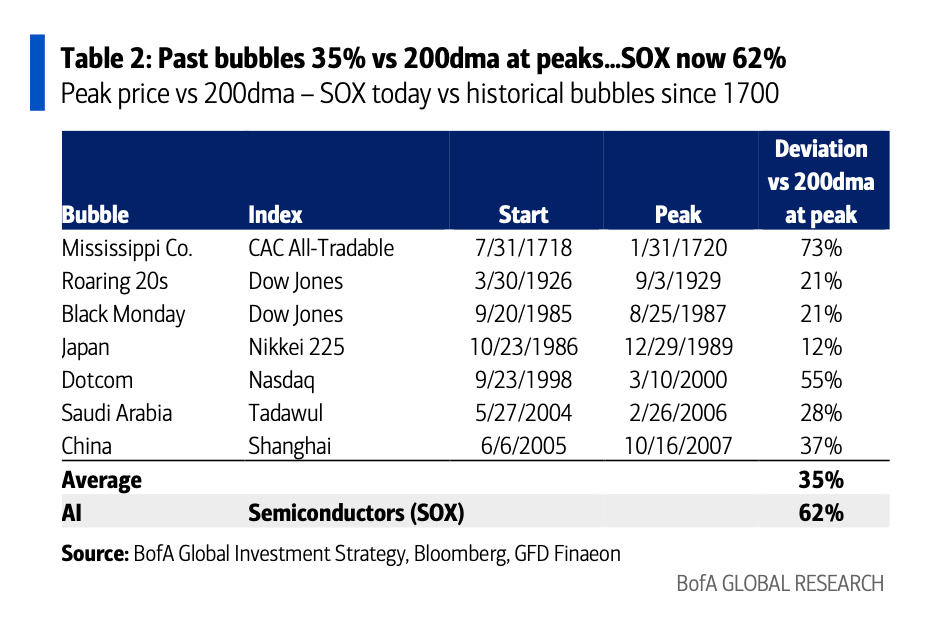

From a technical perspective, there is currently a certain extreme deviation in the market. Reports and related charts from Bank of America (BofA) indicate that the semiconductor index (SOX) has risen to 62% above its 200-day moving average. Historical experience shows that when major market bubbles peak, related market indices typically deviate from the 200-day moving average by about 35% on average. The current degree of deviation has already exceeded the 55% deviation level of the Nasdaq index from its 200-day moving average before the burst of the 2000 internet bubble.

(Source: BofA report The Flow Show at 10:45 PM EDT on May 14, 2026)

Additionally, the current rise in U.S. stocks is heavily dependent on a few tech giants. If super IPO projects like SpaceX and Anthropic list next, they may further divert market liquidity.

Crypto users are accustomed to high volatility, high leverage, and short-term trading, but while U.S. stocks do have volatility, they fundamentally emphasize fundamentals, earnings, valuations, interest rates, and macro cycles. What do you think they most need to change about their trading habits?

Gracy: For users who are just transitioning from crypto to U.S. stocks, the most important reminder I want to give is: do not treat U.S. stocks as memes to speculate on. In the crypto space, users may be used to looking at sentiment, community heat, taking high leverage for short trades. But the U.S. stock market is a highly institutionalized market, focusing on earnings reports, EPS (earnings per share), interest rate environments, and macro cycles.

Users accustomed to the crypto market need to learn to closely monitor treasury yields and inflation data. For instance, when the 10-year U.S. Treasury yield approaches 5%, it could pressure overvalued tech stocks.

In addition, users transitioning from the crypto space to the U.S. stock market need to change another trading habit: reduce leverage and extend timelines. U.S. blue-chip stocks are backed by real profits, cash flow, and business moats, making them more suitable for asset allocation and long-term investing, rather than going all in like a meme stock and expecting to double the investment the next day. Be patient and cultivate a long-term perspective. To help crypto users better adapt to the pace of U.S. stocks, Bitget will also continue to launch educational resources related to U.S. stocks; everyone is welcome to follow along and learn to become “distinguished U.S. stock traders.”

In the past, crypto has been one of the most concentrated domains for young talent, venture capital, technology narratives, and speculative funds. But now AI has clearly become a stronger narrative: top talents are going to AI, VCs are investing in AI, and secondary market funds are chasing AI, with U.S. tech giants also delivering real revenues and growth.

How significant do you think the impact of AI on crypto is? What is the internal situation regarding AI usage at Bitget? Is it mandatory or included in assessments? What AI products do you use?

Gracy: The impact certainly exists, but I prefer to see it as a litmus test for the “de-bubbling” of the crypto industry. Making money in crypto was too easy in the past; now, with AI pulling away funds and talent, it may force the crypto industry to settle down to find truly valuable landing scenarios, such as stablecoin payments and RWA.

At Bitget, we require all employees to fully embrace AI. AI-driven innovation is one of our three core strategies for 2026. We do not rigidly enforce AI usage as a compulsory assessment because good tools will naturally be used proactively by everyone. For instance, I frequently use tools like Manus and NotebookLM to summarize materials, and I find it quite addictive.

Furthermore, we are providing support on an organizational level for employees to use AI. Bitget has procured enterprise access to Claude for all employees, covering 2,167 staff members, with a monthly cost of $200 per person. This isn't due to external requirements, but because after observing actual usage of AI tools by employees, we indeed found improvements in productivity and want to ensure team members do not fall behind in the wave of AI applications.

Even the design team, which does not have a technical background, has learned to use tools like Google AI Studio and has developed 6 or 7 AI tools to assist business operations, which automate the review of UI compliance issues in external materials. On the product side, we’ve also launched AI tools specifically for traders, such as GetAgent and GetClaw.

We have AI-related training almost every day. I attended the “AI Product Sharing Session by the Data Team” and the “Digital Employee Program and BG Agent Platform Introduction” this week.

AI is a leverage for productivity. Whoever uses it well can run faster in the next cycle. Now and in the future, we are definitely in an era where silicon-based life and carbon-based life work together.

More and more crypto exchanges are beginning to offer U.S. stocks, gold, forex, stock tokens, and Pre-IPO products. Optimistically, this is an expansion of crypto infrastructure into global assets; pessimistically, it may indicate that crypto lacks quality assets, forcing exchanges to bring in U.S. stocks to maintain growth.

What is your view on this issue? When crypto exchanges integrate U.S. stocks, are they enhancing the financial infrastructure value of crypto, or are they directing crypto user traffic towards traditional finance, ultimately transforming into an outsourced market for U.S. stock liquidity?

Gracy: I do not believe this is a black-and-white issue. Crypto exchanges integrating U.S. stocks, gold, forex, and Pre-IPO products may superficially appear to be “bringing traditional financial assets into crypto,” but on a deeper level, it is actually verifying a question: Is crypto just an asset class, or is it a new set of financial infrastructure?

My judgment is that the answer depends on how exchanges proceed. If they simply package exposure to U.S. stock prices as a trading product, it may indeed become a distribution channel for traditional financial liquidity, perhaps merely directing crypto user traffic to U.S. stocks.

However, if it can reorganize asset issuance, trading, settlement, custody, and risk control based on stablecoin accounts, on-chain settlement, global accessibility, fragmented trading, and a 7×24 market, then it enhances not just a specific U.S. stock but the value of crypto as the next-generation financial infrastructure.

Moreover, those who have used many traditional financial platforms will know that the user barriers in traditional finance are actually very high: it's hard to open accounts, there are high thresholds, and capital turnover is slow. Our goal is to bridge bottom-line assets through stablecoin settlements and on-chain RWA protocols, allowing 120 million Bitget users to trade high-quality global assets with just a smartphone and an email.

I believe this is not outsourcing; rather, it is using crypto's high efficiency and low friction to lower the dimensionality and improve the experience of traditional brokers. We are not only not losing users, but also through tokenization solutions like Reality pulling real assets onto the chain, making them a part of DeFi. This is expanding the domain of crypto. We believe that as the industry develops, the definition of crypto is also evolving. Initially, crypto only represented Bitcoin; later, crypto also became the much-discussed memecoin, and in the future, many cryptos will be RWA. Regardless of what the assets are, blockchain and other underlying technologies will be the cornerstone driving this new financial system. Our long-term optimism for the industry partly stems from confidence in the technology behind it.

Bitget’s proposal of UEX essentially allows users to trade cryptocurrencies, stocks, gold, forex, ETFs, and other assets within a single account. While this sounds like an expansion of the exchange's capabilities, it could also be understood as: relying solely on crypto can no longer meet user needs, so exchanges must transform into comprehensive asset platforms.

What is your view on this tension? Is UEX a natural evolution of crypto exchanges, or does it indicate that the ceiling has been reached for “exchanges that only do crypto”? How would you like the outside world to define Bitget?

Gracy: If we view the blockchain behind crypto as a fundamental value transfer network, the ceiling is still far off.

UEX is a natural evolution for exchanges. For example, Amazon originally only sold books, but now sells everything; the iPhone started as a touch-screen phone but became a digital life hub. Users need more than just “speculating on coins”; they want to earn money and allocate assets. Since stablecoins have become one of the best settlement tools globally, why not let users buy and sell the world's best assets with them?

We proposed the UEX vision in the second half of 2025, and for at least the next three years, we will steadfastly follow this transformative path. Here, I’d like to elaborate on the WHY and HOW.

WHY — Why persist in the UEX transformation?

From the perspective of the financial system’s structure, the current financial system is still built upon “walls.”

Asset fragmentation: buying stocks requires going to brokers, buying crypto requires coming to CEX, buying forex requires finding banks or IB (Interactive Brokers).

Geographical and temporal fragmentation: U.S. stocks, European stocks, and Asian stocks each have their own closing times, and capital cannot flow 24/7.

Account and technical fragmentation: traditional finance and Web3 are like two parallel universes, and users need to manage countless accounts and margins.

This leads to low capital efficiency, complex user experiences, and difficulty in standardizing risk management. Therefore, an all-asset trading platform is both a user demand and a trend of the times.

In the past 4 to 5 years, there hasn’t been a fundamental change in the exchange landscape; there is strong first-mover advantage under homogeneous competition. But crypto is becoming the bottom layer of finance, and an inflection point for the industry has already appeared. At this moment, platforms with stronger teams and more decisive actions have the opportunity to overtake. The future competitors aren’t just peers; traditional finance is also accelerating its layout. Whoever can establish user mindset first will gain the upper hand.

HOW — How can we achieve a UEX panoramic exchange?

One account, one interface, one-stop trading across assets. Crypto has always been our core business, but Tokens will become more diverse. Bitcoin is a Token; Tesla, Nvidia, and SpaceX can also be Tokens; gold and crude oil can equally be Tokens. RWA is a direction recognized by both Wall Street and crypto, and it is also where we aim to establish an advantage.

Based on this direction, we are building five core modules.

A unified account enables cross-asset margining, maximizing capital efficiency. A unified risk engine upgrades single-asset risk management to portfolio-level risk management. A unified liquidity routing integrates CEX, DEX, and external markets, making Bitget a liquidity dispatch center. A unified execution layer will continuously upgrade user access from manual trading to API and then to AI Agent. The asset standardization layer allows crypto, stock ETFs, forex, commodities, and RWA to all become programmable trading objects.

Three years from now, I hope the outside world will no longer define Bitget merely as a crypto exchange but will see it as a panoramic exchange where one can effortlessly buy and sell core global assets, experience smooth interactions, and feel secure on the safety front.

Recently, regulatory actions targeting cross-border brokers like Futu, Tiger Brokers, and ChangQiao have sparked considerable discussion in the market. Although Bitget's U.S. stock 2.0 path is different from traditional Internet brokers, it also involves users trading traditional financial assets across borders.

What is your view on these regulatory changes? Will they affect users' choices regarding entry points for U.S. stock trading?

Gracy: Compliance is an irreversible trend, which is why we have made “compliance first” our core strategy for 2026.

The essence of regulation is to protect users' asset safety, prevent money laundering, and mitigate systemic risks. When developing Reality and U.S. stock 2.0, compliance standards were directly maximized. We did not touch gray areas; instead, we collaborated directly with the U.S. licensed broker Alpaca, and the underlying assets are also operating under the U.S. financial regulatory framework.

Regulatory changes will indeed bring short-term pain, but in the long run, they will promote market reshuffling, eliminating non-compliant fly-by-night operations. For users, as long as our product experience is good enough—such as supporting 24-hour trading, reducing currency exchange losses, and allowing for composable on-chain assets—while achieving sufficient transparency in compliance and asset safety, like through Reality's daily audit dashboard, I相信用户会做出理性的选择。

很多 crypto 用户第一次真正接触美股,可能还是沿用币圈思维:追热点、追涨幅、上杠杆、看情绪、做短线。但美股背后有不同的估值体系、财报周期、利率环境、监管规则和公司基本面。

如果只能给这类用户一句最重要的建议,你会说什么?

Gracy: If I can only say one thing, it would be: look for good opportunities and invest in quality companies that you truly understand and that have real profits to support them, then leave the rest to time. In the crypto world, there are times when our trading resembles “speculation”; however, in U.S. stocks, we should strive to make more “investments.”

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。